Colombia economic outlook, November 2024

Colombia’s economy has shown significant year-over-year growth, but challenges like weak private investment and low business confidence remain. Improvements in these areas will be imperative to sustain long-term growth and prosperity.

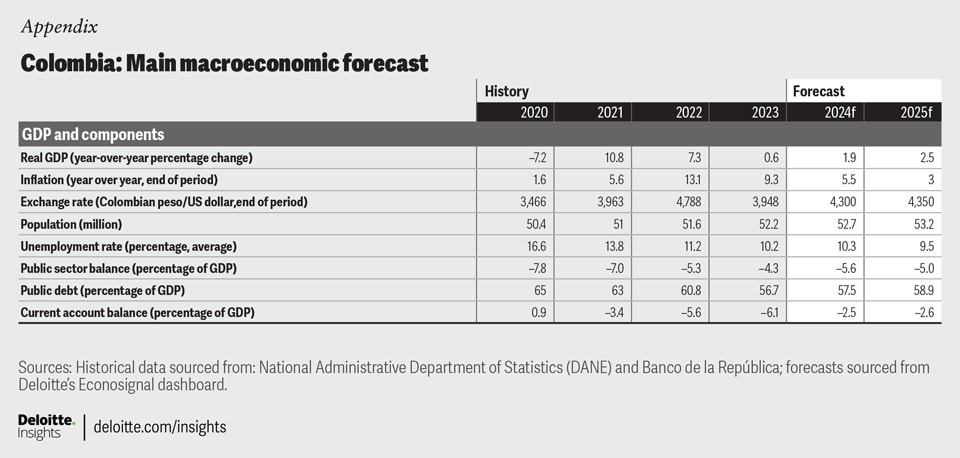

In 2023, Colombia’s economy experienced weak performance, growing only 0.6% compared to 2022. Declines in value added were observed in key sectors such as construction (4.1%), manufacturing (3.6%), and retail (2.8%).

Over the first half of 2024, the economy grew by 1.5% in cumulative terms. This data is undoubtedly encouraging, representing a significant improvement compared with last year. The sector experiencing the highest growth was entertainment (9.5%), likely due to sporting events occurring in June and July 2024. The agricultural sector ranked second, followed by public administration.

While all these sectors showed notable growth, the aggregate of private economic activity (approximately 70% of Colombia’s gross domestic product) grew 0.7% annually; if the entertainment sector is excluded, the number comes down to 0.2% annually.

Overall, the Colombian economy still exhibits certain weak links that require attention, despite showing strong signs of recovery. Lack of investment remains one of the main factors limiting growth. Although investment grew by 4.3% year over year in the second quarter of 2024, the cumulative total investment till then indicates a 1.3% decline compared with the same period in 2023. This decline is more pronounced in the private sector, which accumulated a loss of 2.4% over the same period.

Colombian economy: 2024 at a glance

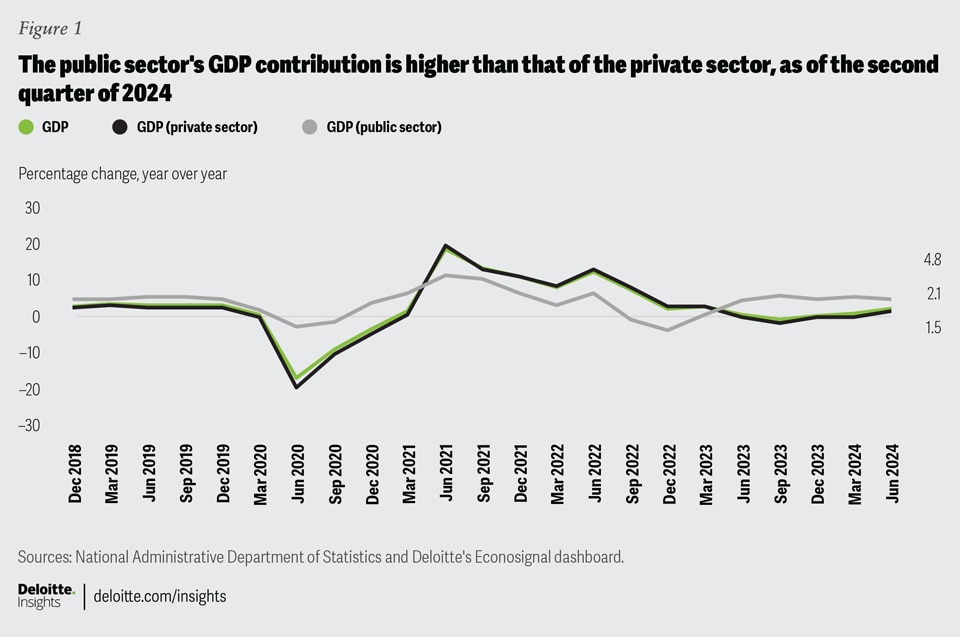

Colombia’s GDP showed an annual growth of 2.1% in the second quarter of 2024 (figure 1). This result significantly exceeded the 1.3% average annual growth expected by analysts surveyed by the nation’s central bank, the Banco de la República.1 While this is an encouraging outcome (elaborated later in this article), and several disaggregated indicators have improved (the private sector, which accounts for approximately 75% of GDP, grew by 1.5% annually), caution remains, as key sectors await reactivation for long-term economic performance.

Cumulative GDP for the second quarter grew by 1.5%, compared with the same period in 2023. Meanwhile, private sector GDP increased by 0.7%, and consumption grew by 0.8%. However, investment continues to accumulate losses, showing a negative annual growth of 1.3%.

Regarding productive sectors, the GDP result is explained by substantial increases in the agricultural sector (8.1% annually), the public sector (9.3% annually), and the entertainment sector (23.7% annually), driven by midyear sporting events that primarily boosted the online betting platforms subsector.

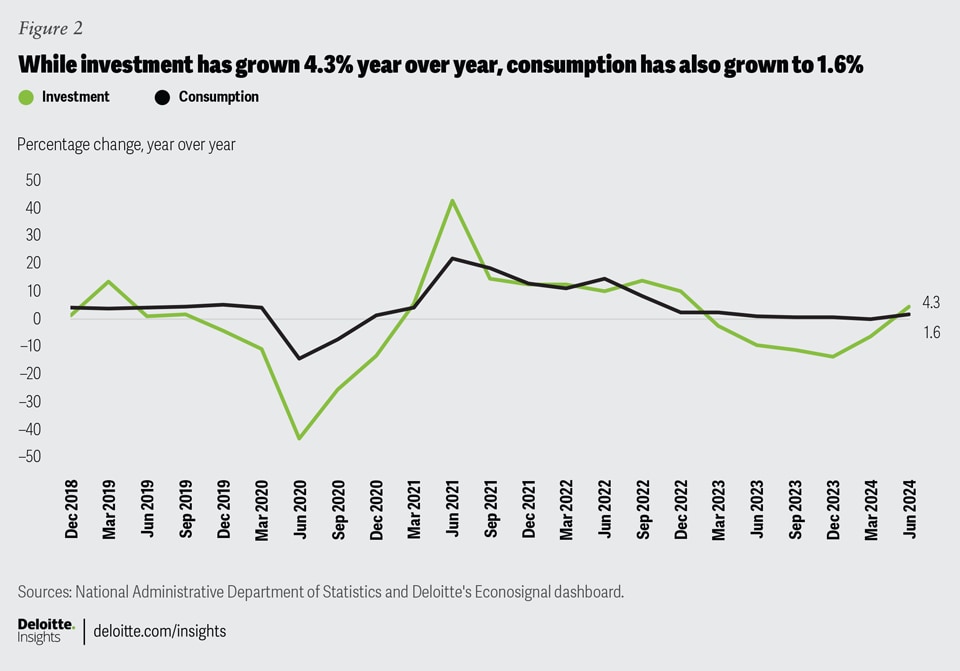

The higher numbers seen for the second quarter can be attributed to a moderate increase in consumption (1.6% annually) and a significant recovery in investment (4.3% annually) (figure 2).

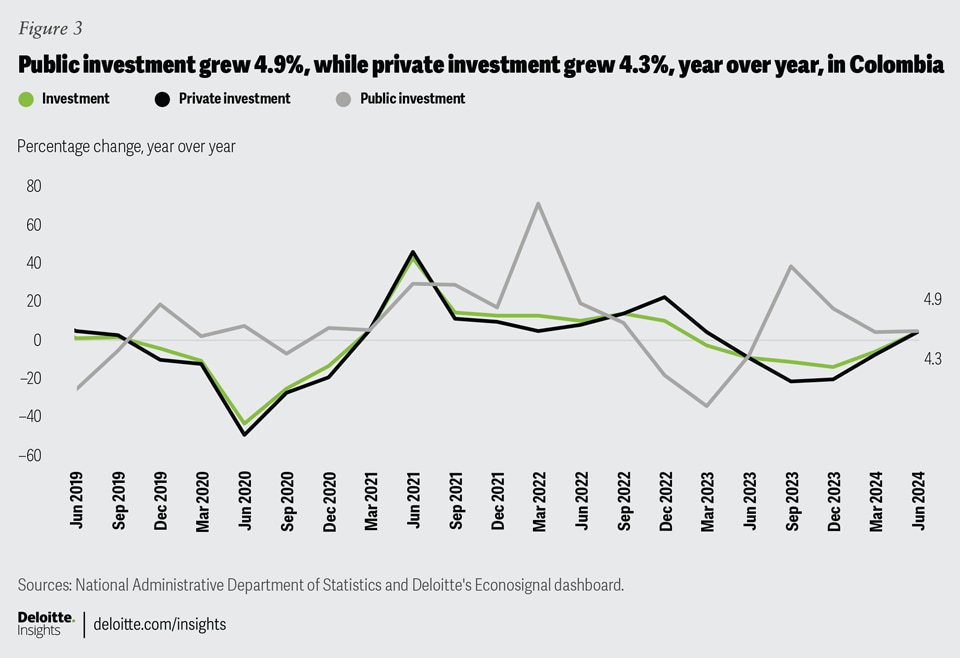

Investment: A considerable challenge to overcome

Private investment, which accounts for about 80% of total investments, grew by 4.3%, while public investment grew 4.9% (figure 3).

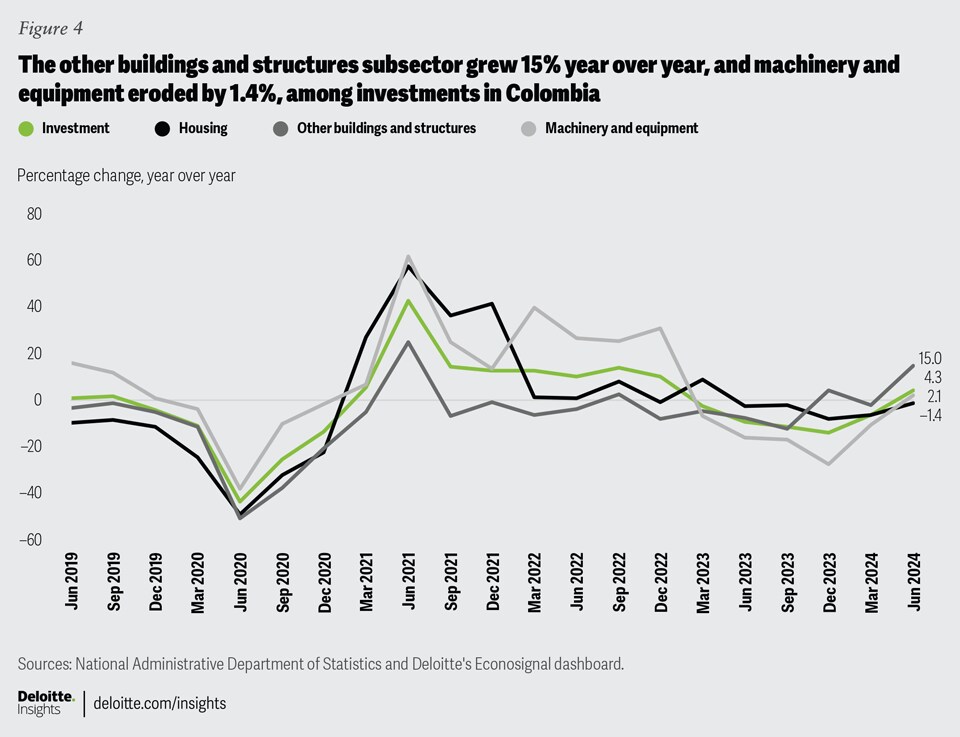

Investments in machinery and equipment, which form an approximate 40% share of total investment, had the poorest performance, eroding 1.4% year over year. On the other hand, housing, which contributes nearly 20%, showed an annual growth of 2.1%. Finally, other buildings and structures, which account for 30%, grew by 15% (figure 4).

According to Deloitte’s investment diagnostic report, the other buildings and structures subsector is the one that influences short-term GDP the most—a phenomenon consistent with the greater dynamism that the economy experienced in the second quarter of 2024.2

Meanwhile, the machinery and equipment sector has the biggest effect on long-term GDP—and it continues to deteriorate, although at a slower rate.

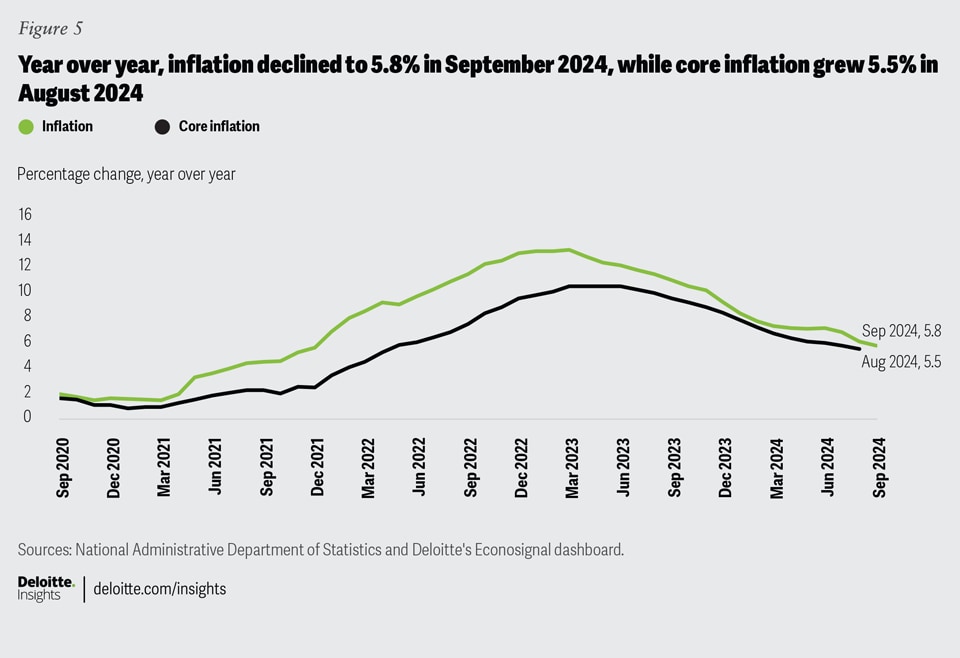

Inflation is decreasing and is under control

In September 2024, inflation decreased 5.8% annually (figure 5). At the sectoral level, the ones that saw the highest price increases were education (10.7%), restaurants (9%), accommodation (8.4%), and beverages (6.2%).

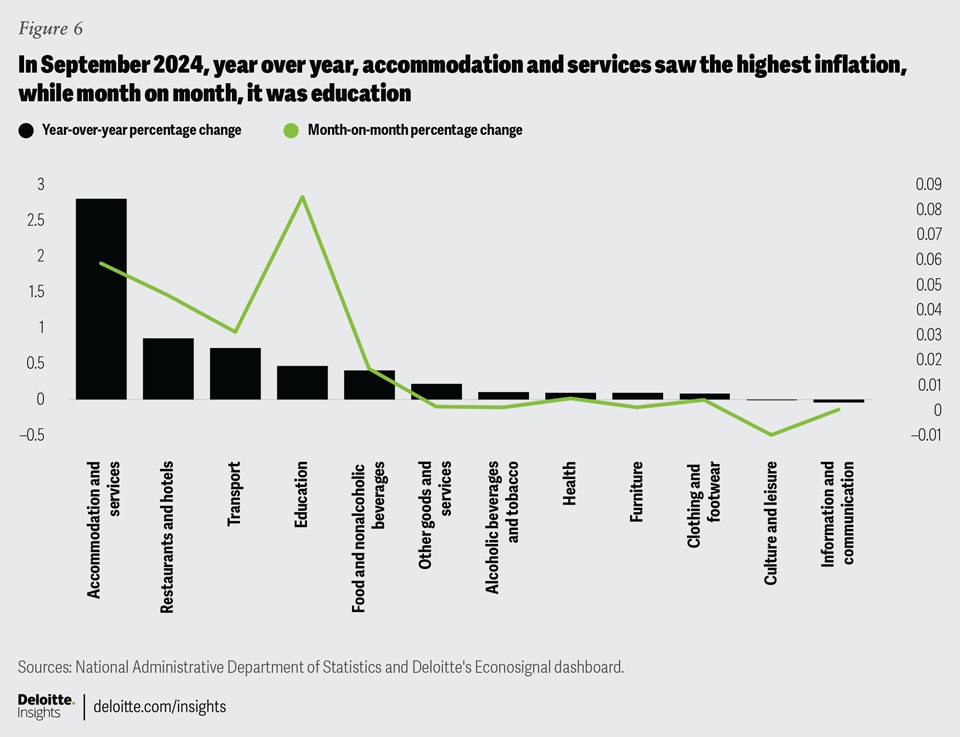

So far in 2024, the consumer price index category that has contributed the most to the increase in inflation has been accommodation and services—this time, it accounted for 48% of index variation. In second place was transportation, with 12.4%, due to adjustments in fuel prices, and in third place, restaurants and hotels accounted for 14.6% (figure 6).

It is also important to note that core inflation—which excludes food and regulated items—continued its downward trend in August 2024, reaching an annual rate of 5.5%.3

This suggests that Colombia’s central bank will continue to reduce its monetary policy interest rate.

Figure 6 illustrates the composition of the 5.8% annual inflation rate. Accommodation and services contributed 28 basis points, while restaurants and hotels added 8.5. The monthly inflation rate was 0.24%, primarily driven by an increase in education prices.

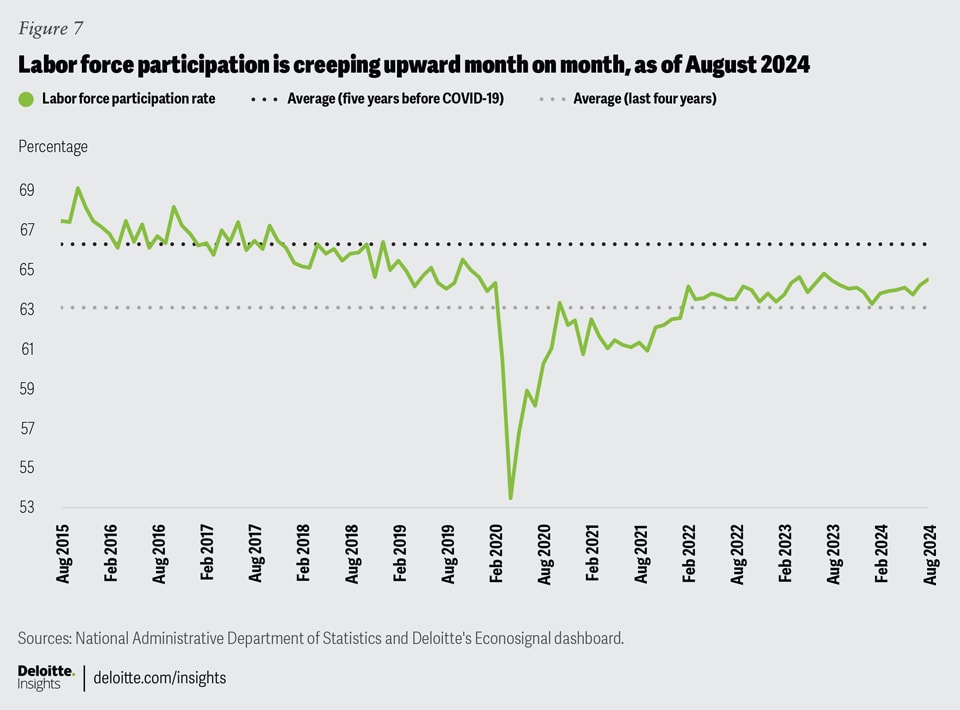

The labor market is recovering but is still weak

In August 2024, the labor force participation rate (including both employed and unemployed populations) stood at 64.5% (figure 7), indicating an improvement compared with last month’s figure of 64.2%. Compared with August 2023, the rate remained almost stable.

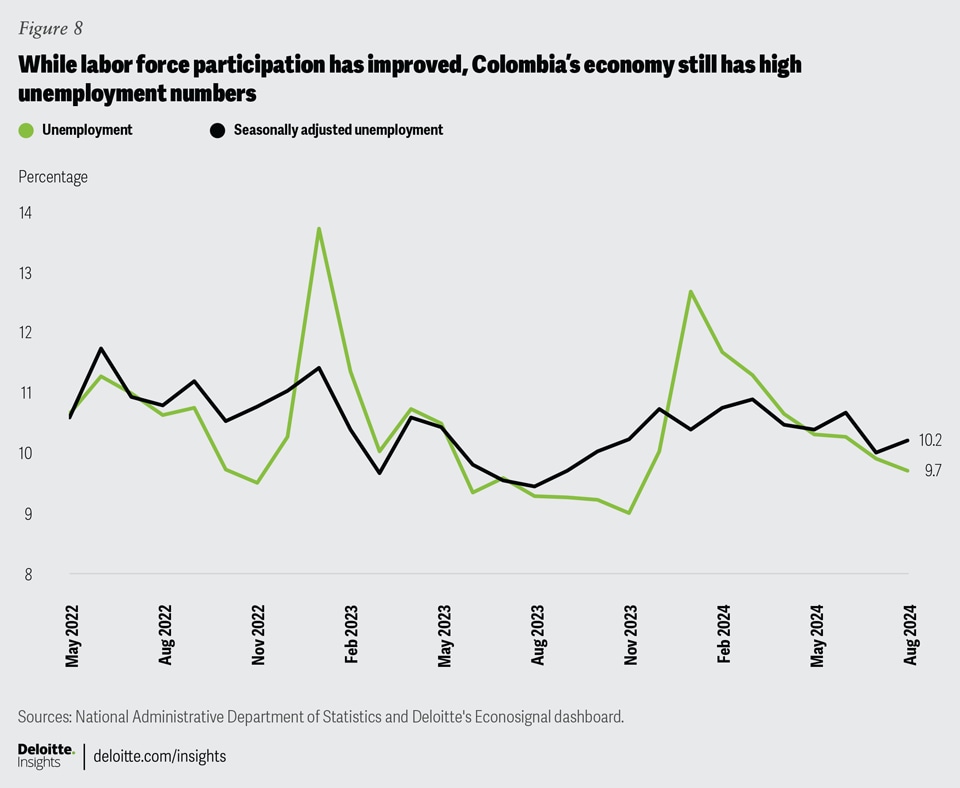

Meanwhile, the unemployment rate was 9.7% in August 2024, showing an improvement compared with the 9.9% observed a month ago in July. But it’s still higher compared with the same month last year.

The seasonally adjusted unemployment rate4 increased from 10% in July to 10.2% in August (figure 8) this year.

To combat this, government has proposed a labor reform: The project is being assessed by the Colombian Congress, which advanced in its evaluation during the second debate on Oct. 17, 2024. This initiative, rather than driving the creation of new jobs, aims to protect existing ones through increased surcharges for overtime, Sundays, and holidays. It also adjusts the night shift to start at 7 p.m. (currently, it starts at 9 p.m.). However, those changes could make payroll more expensive, which could lead to higher unemployment.5

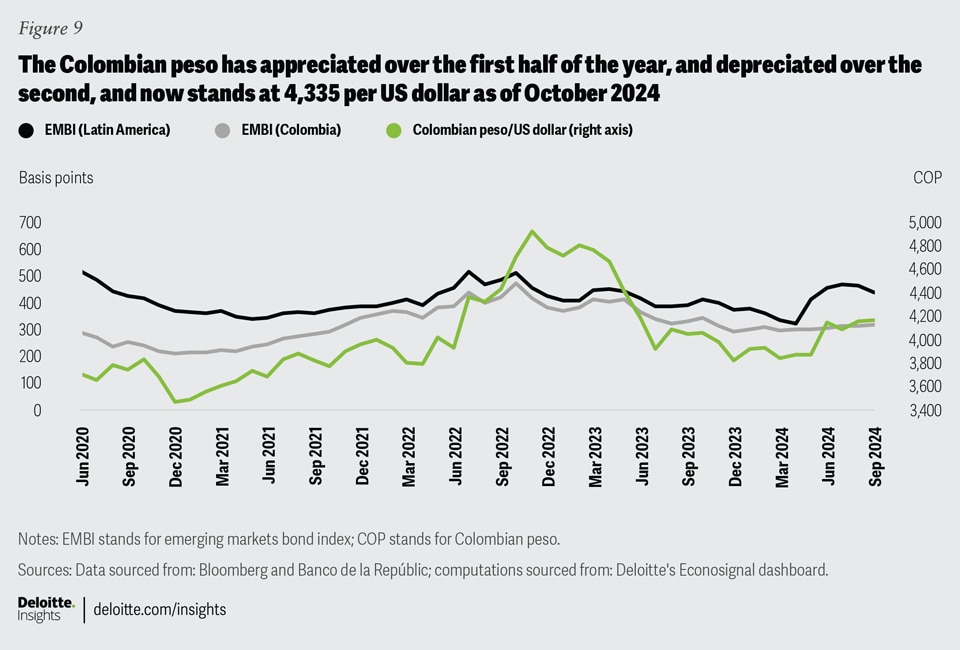

Exchange rate: Depreciation pressures

The Colombian peso (COP) appreciated in the first half of the year, against the US dollar, supported by a lower risk perception (figure 9).6 However, since May 2024, this trend has reversed.

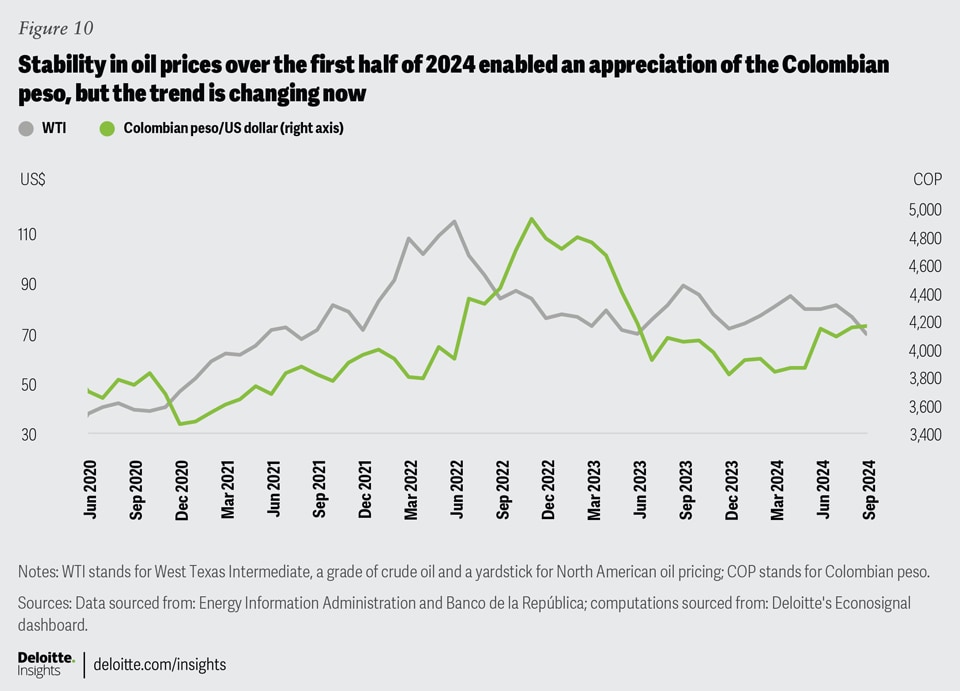

The stability of oil prices at levels close to US$80 per barrel during the first half of 2024 served as an anchor for the exchange rate, which, after episodes of high volatility, sought to return to levels close to COP4,000 per dollar (figure 10). However, since mid-July, there has been a marked decrease in oil prices (13% until the end of October), which drove the exchange rate up from COP4,030 in July to COP4,335 at the end of October.

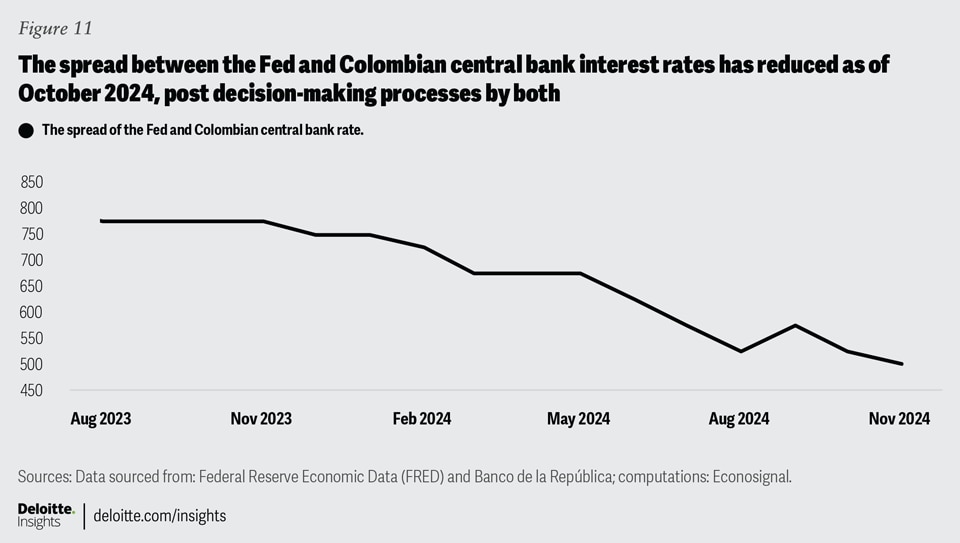

The spread between the monetary policy rate of Colombia’s central bank and the US Federal Reserve remained stable as both institutions cut their rates by 50 basis points: This means the spread has little to no effect on the exchange rate (figure 11).

In the second-quarter report,7 the exchange rate was expected to end the year below COP4,200 per US dollar; after the US elections, currencies in emerging markets have been under pressure. In Colombia, the exchange rate reached COP4,475 (Nov. 15); however, some appreciation is expected at the end of the year, and the exchange rate could end around COP4,300 per dollar. The average exchange rate in 2024 has been COP4,026: Decreasing oil prices and uncertainty in US trade policy next year could lead to higher levels over 2025 (the rate could reach around COP4,350 by the end of next year).

Fiscal framework

With the assumptions outlined in the Medium-Term Fiscal Framework,8 published last June by the Ministry of Finance of Colombia, the fiscal deficit at the end of the year is projected to be 5.6% of GDP, exactly the limit established by the fiscal rule for this year. However, according to the Autonomous Fiscal Rule Committee,9 in the Medium-Term Fiscal Framework, there are assumptions regarding projected tax revenues for the second quarter of 2024 that might not be met, posing a risk of a necessary adjustment equivalent to COP5.3 trillion. This would imply that the limit (5.6% for 2024) established by the fiscal rule would not be achieved unless an additional adjustment is made on the expenditure side.

Although the fiscal rule is still expected to be met with these adjustments, on the off chance it isn’t, the event would send negative signals to other markets and credit-rating agencies, which could translate into upward pressure on the exchange rate and increase the cost of external borrowing.

Meanwhile, the government has presented a new tax reform bill. This aims to generate COP12 trillion for the year 2025 by imposing value-added tax on digital betting platforms. It would also increase the same tax on hybrid cars from 5% to 19% and adjust the carbon tax. On the reduction side, there would be a decrease in the corporate income tax from 35% to 27%, depending on the size of the company.

Monetary policy

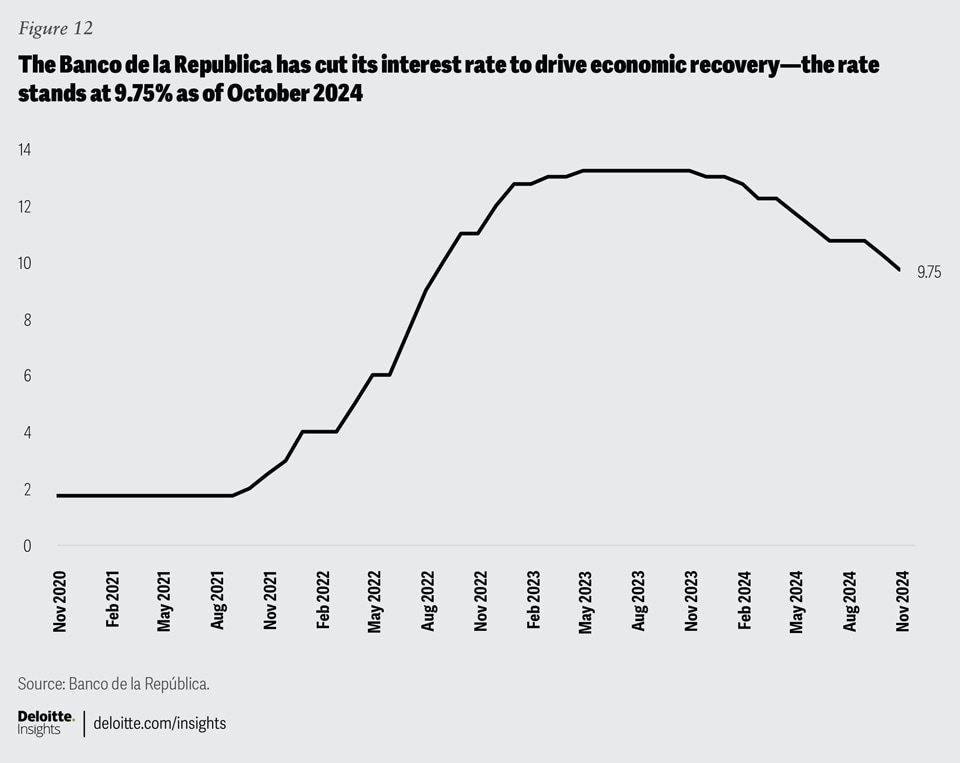

At its last meeting held in October, the board of directors of Colombia’s central bank decided to reduce the monetary policy rate by 50 basis points, setting it at 9.75% (figure 12). Four members voted for a 50 basis-point cut, while three voted for a 75 basis-point cut. In the meeting report, the board acknowledged the need to reach lower rates to support economic recovery but was cautious about a more aggressive reduction. The four members who voted for a 50 basis-point cut concluded that uncertainty on the fiscal side could imply exchange rate pressures, which would pose a risk to inflation.

The next board meeting is scheduled for the end of December. According to the analysts surveyed by the central bank, an additional reduction of 50 basis points is expected,10 which would set the monetary policy interest rate at 9.25%.

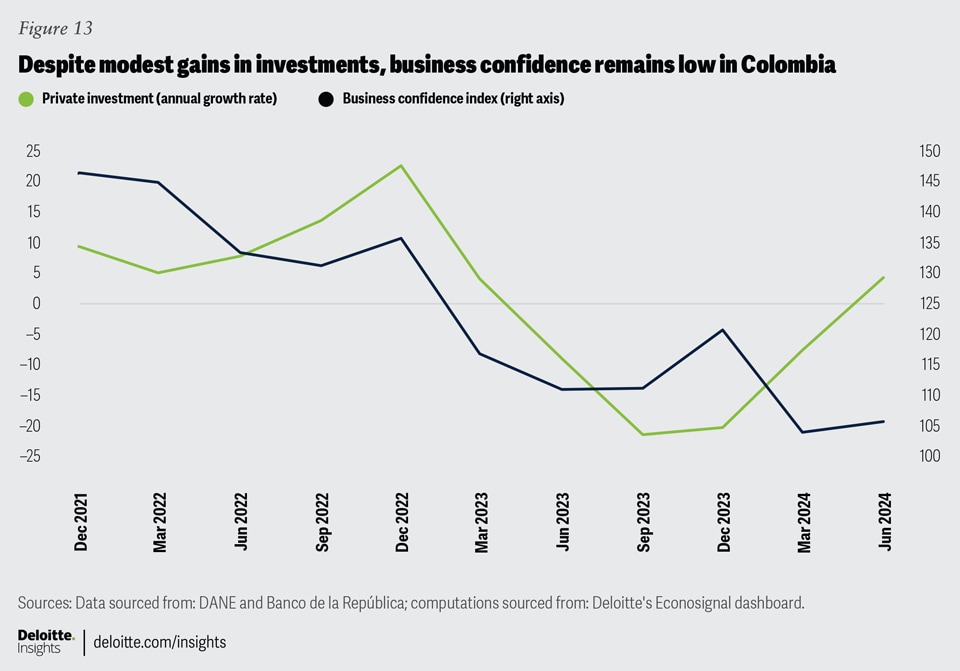

Business confidence

The deterioration in private investment, as explained in the investment diagnostic report,11 is mainly due to the lack of investor confidence and high interest rates.

Figure 13 shows how investor confidence12 is closely related to investment. From March to June this year, there was a slight improvement in the business climate indicator, which coincided with a significant improvement in the private investment growth rate (4.3%). However, the cumulative figure for the second quarter still shows a negative performance of 2.4% compared with the same period in 2023.

External sector

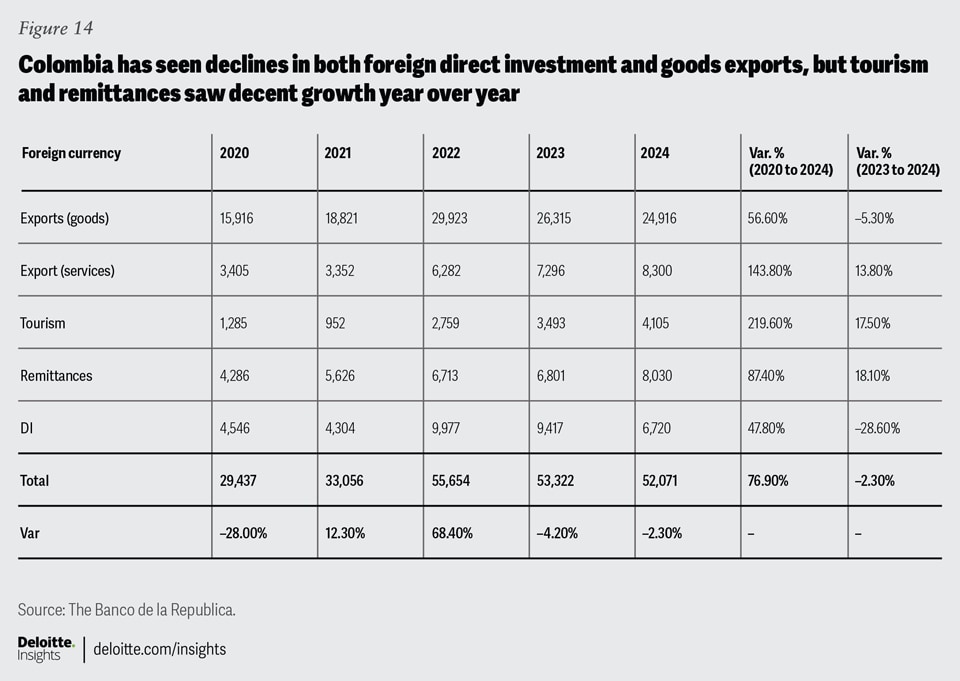

As of the second quarter of 2024, foreign currency inflows to Colombia declined by 2.3% year over year, compared with the same period in 2023.

This result is primarily attributable to a decrease in foreign direct investment (a 28.6% decrease year over year) and, to a lesser extent, a decline in goods exports (a 5.3% decline year over year) (figure 14).

In contrast, foreign currency inflows from tourism and remittances showed annual growth rates of 17.5% and 18.1%, respectively, compared with the second quarter of 2023.

Exports

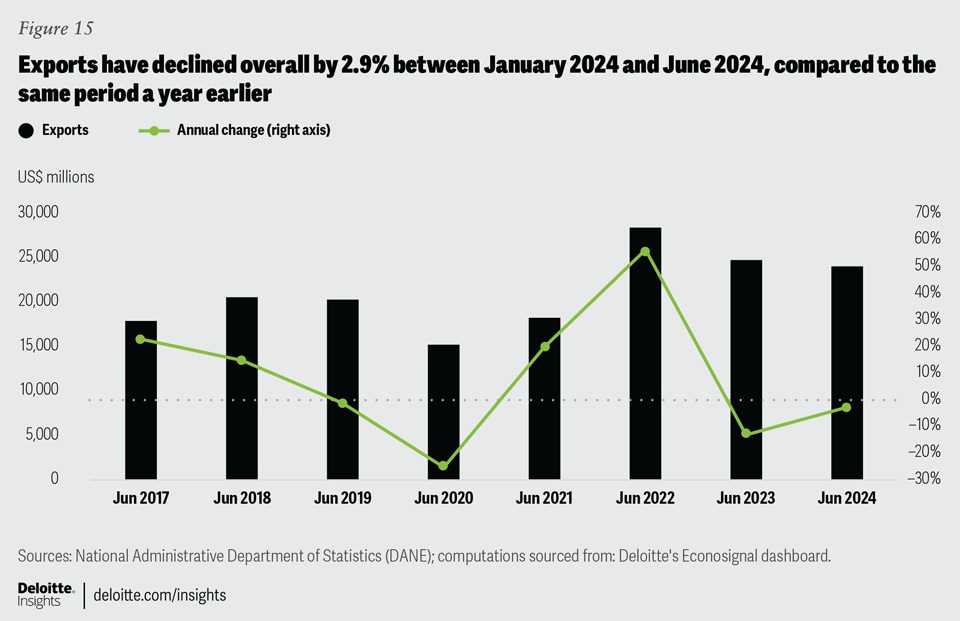

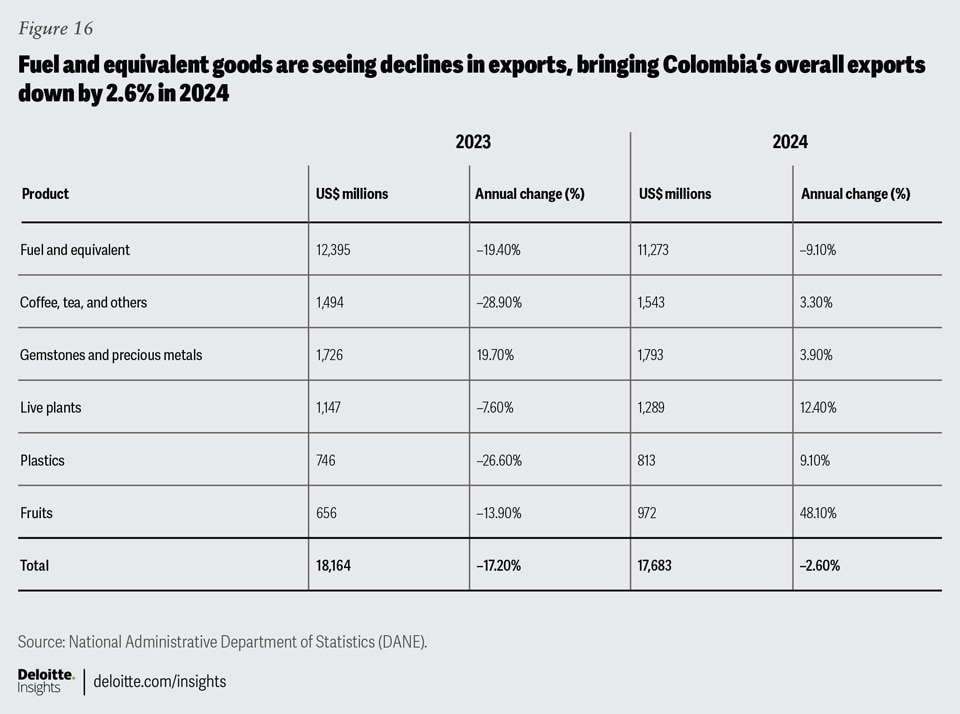

In the period from January 2024 to June 2024, Colombia’s total exports of goods and services decreased by 2.9% compared with the same period in 2023 (figure 15). This is mainly explained by a reduction in fuel exports (a 9.1% decline), which accounted for 47% of total exports. This reduction would mark the second consecutive year of declining exports, as exports fell by 17.2% from January to June 2023 (see figure 14 for more details by sector).

Figure 16 shows year-over-year growth and decline rates of Colombia’s major exports from January to June of 2023 to the same period a year later.

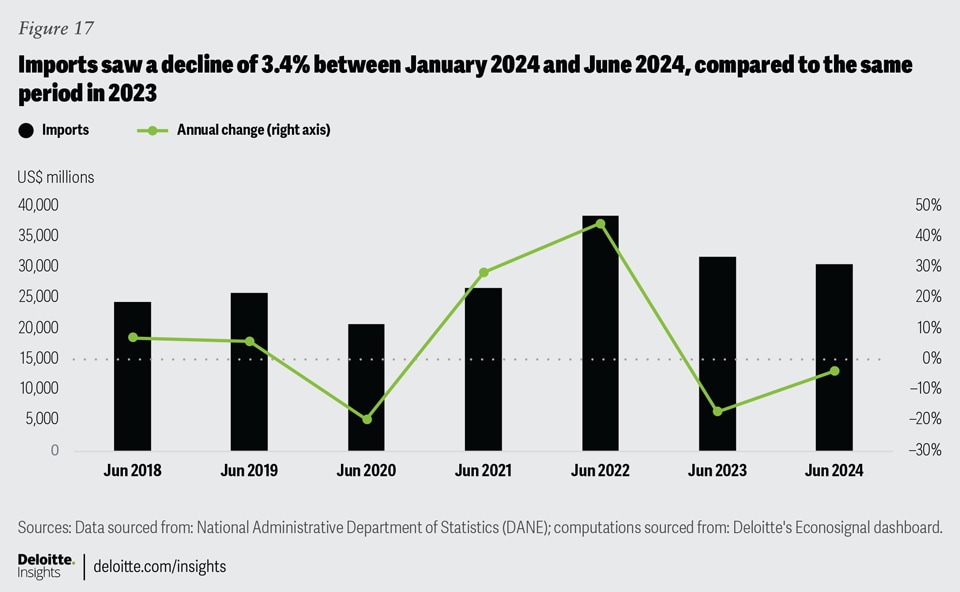

Imports

Between January 2024 and June 2024, imports decreased by 3.4% (figure 17) compared with the same period in 2023. This result is explained by a decline in capital goods (an 8.3% decrease) and, to a lesser extent, in inputs (a 4.9% decline).

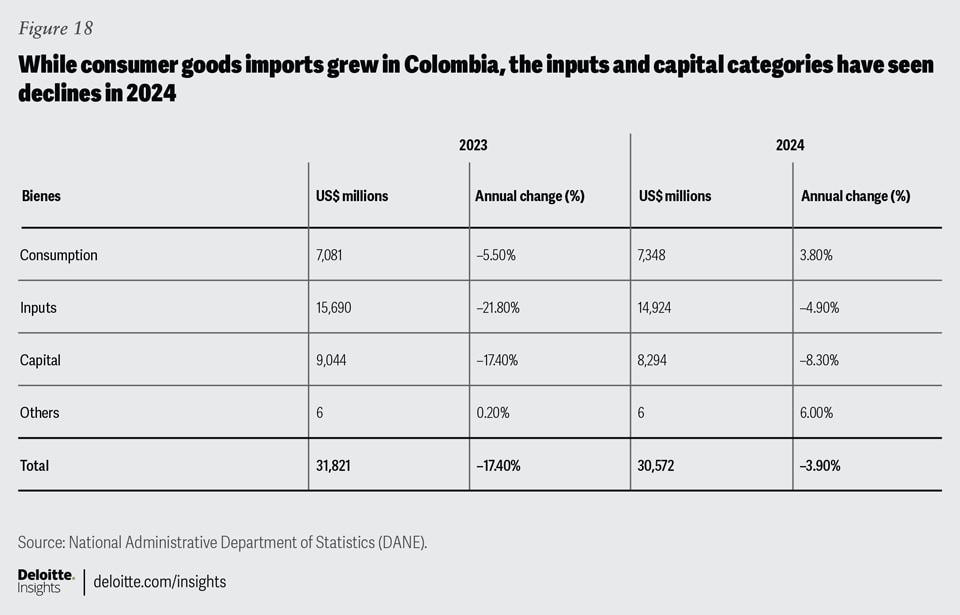

The import of consumer goods increased by 3.8%, but categories like inputs and capital have declined (figure 18).

Financial sector

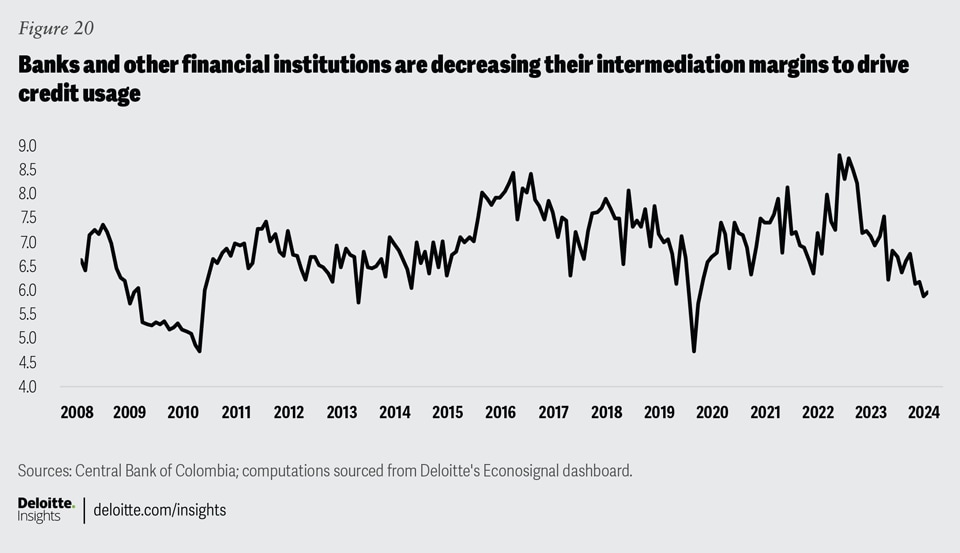

The loan-to-deposit ratio indicates how much banks are lending relative to the resources they receive from economic agents. Since June 2023, this ratio has deteriorated significantly, indicating a decrease in credit issuance (figure 19).

Currently, this ratio is below its historical average, prompting financial institutions to reduce their intermediation margins to encourage the use of credit (figure 20).

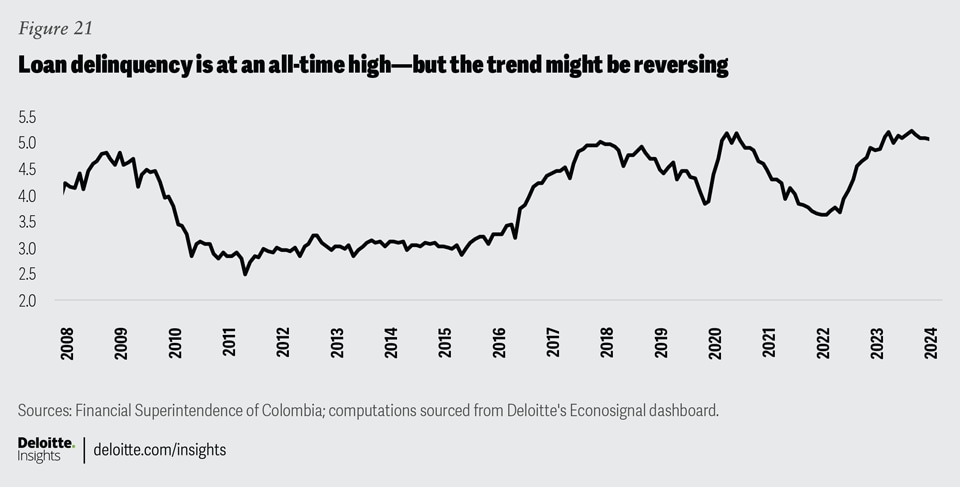

However, this will not be reflected in the short term, as delinquency, measured by the loan quality indicator13 (figure 21), is near its historical high. Nonetheless, it is beginning to show a change in trend, suggesting that there could be a greater willingness to borrow next year.

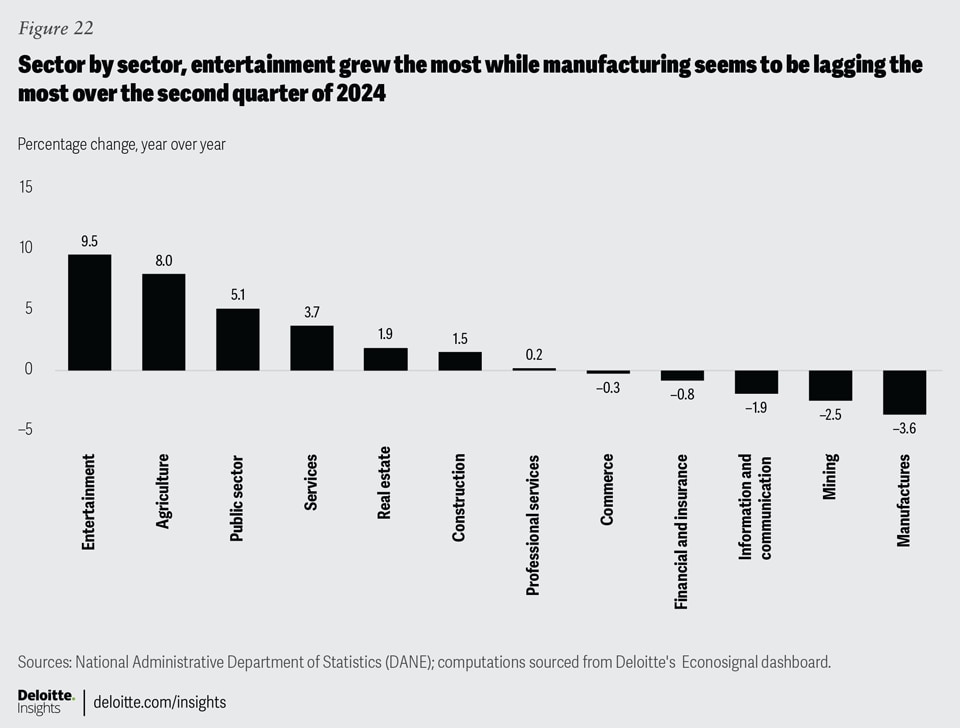

Sectoral trends

In the second quarter of 2024, the Colombian economy showed better performance (2.1% year over year) compared with the first quarter (0.8% year over year). For the cumulative period up to the second quarter, the economy grew by 1.5% year over year, compared with the same period in 2023.

The entertainment sector led with cumulative annual growth of 9.5% (figure 22), driven by a significant increase in betting associated with sporting events held between June and July 2024 (Copa América and UEFA European Championship). The agricultural sector (6% of GDP) ranked second, with cumulative annual growth of 8.0%. The public sector (16% of GDP) continued to show moderately high growth (5.3% cumulative annual growth). The construction sector experienced a significant recovery, with a cumulative annual growth of 1.5%, mainly driven by an increase in civil projects (10.9% cumulative annual growth), while building construction–related cumulative annual growth deteriorated by 2.7%.

Other sectors such as manufacturing (11% of GDP), mining and quarrying (4% of GDP), and commerce (17% of GDP) continued to face challenges, resulting in negative cumulative annual performances of 3.6%, 2.5%, and 0.3%, respectively. As mentioned in the previous quarterly report,14 a recovery was expected in the commerce sector, which, after five consecutive quarters of negative performance, showed a variation of 0.15% in the second quarter. Similarly, although still far from recovering, the manufacturing sector slowed its rate of deterioration, which in previous quarters had been above 5.0% year over year, and this time was 1.6% year over year.

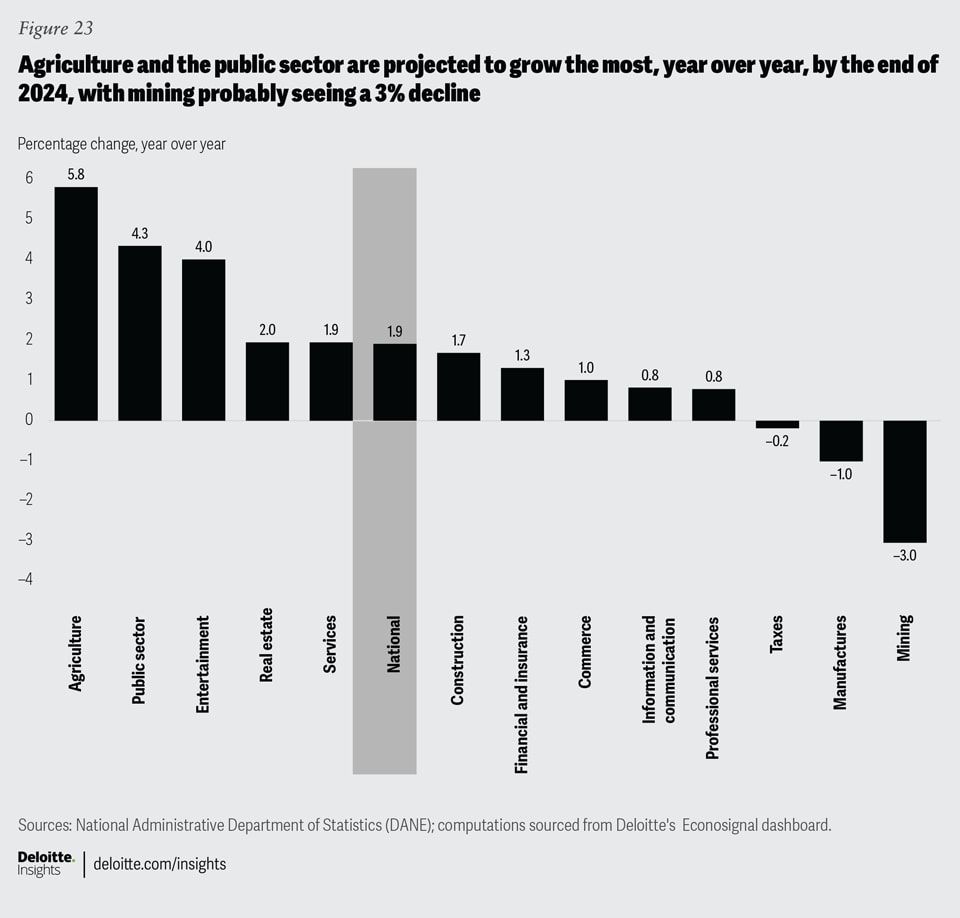

In the previous report, it was mentioned that the mining and quarrying sector had a negative bias. This sector deteriorated by 2.5% year over year in the cumulative period up to the second quarter due to a significant reduction in coal extraction. This sector has been affected by decreased investor confidence and other local factors and is projected to decline by almost 3% by the end of the year (figure 23).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}