Latin America economic outlook, November 2023

Latin American nations are faced with two forces—a 20-year Fed rate peak and a dramatic Chinese slowdown—each with its own unique challenges and opportunities.

Article

•

13-min read

•

Deloitte Global Economics Research Center

Daniel Zaga

Mexico

Alejandro Mina

Colombia

Daniel Gonzalez Sesmas

Mexico

Federico Di Yenno

Argentina

Alessandra Ortiz

Mexico

Summary

To set a scene, a robust US economy and a Chinese growth slowdown have brought Latin America to an economic crossroads. Not only does this mark a significant inflection point in the global economic landscape but also brings both challenges and unique opportunities for the region’s economies.

There are two significant aspects to fully understanding this scenario, however. First, the effects of the Fed’s highest fund rate in two decades on Latin American monetary policy; and second, the impact of slower Chinese growth on Latin American trade, investment, and finances.

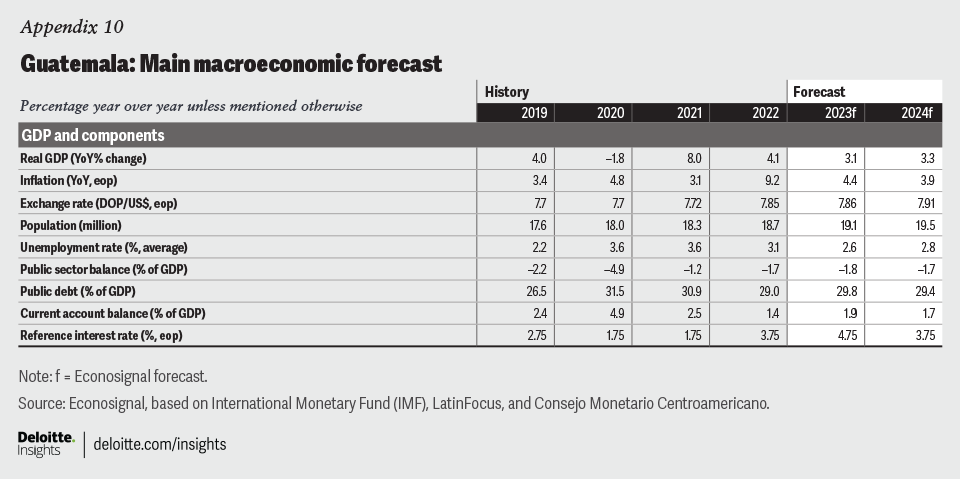

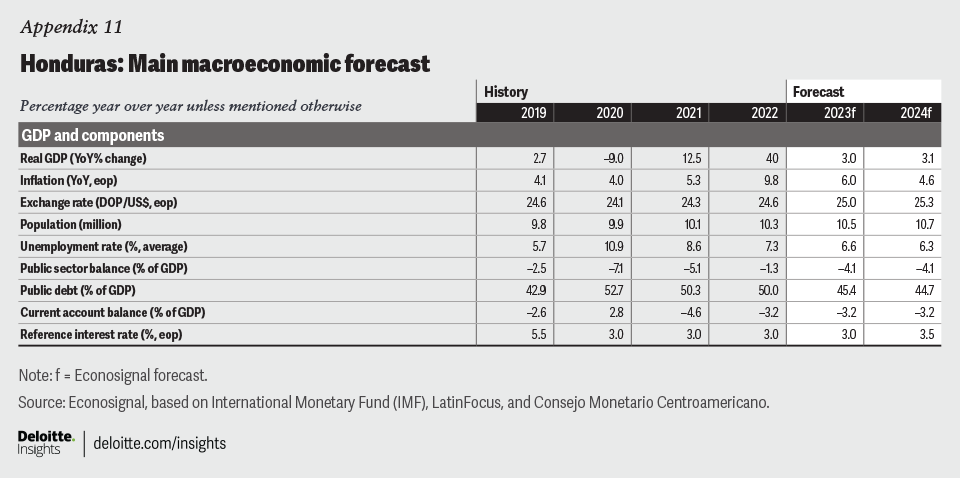

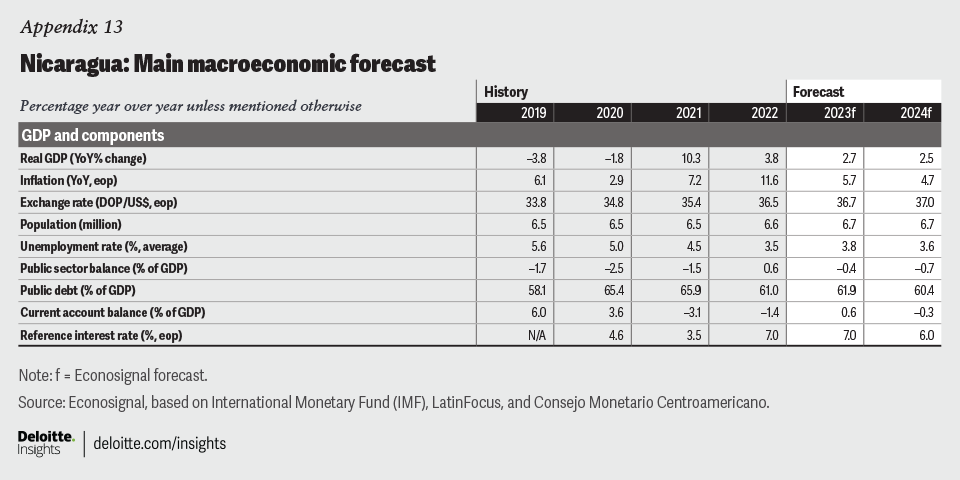

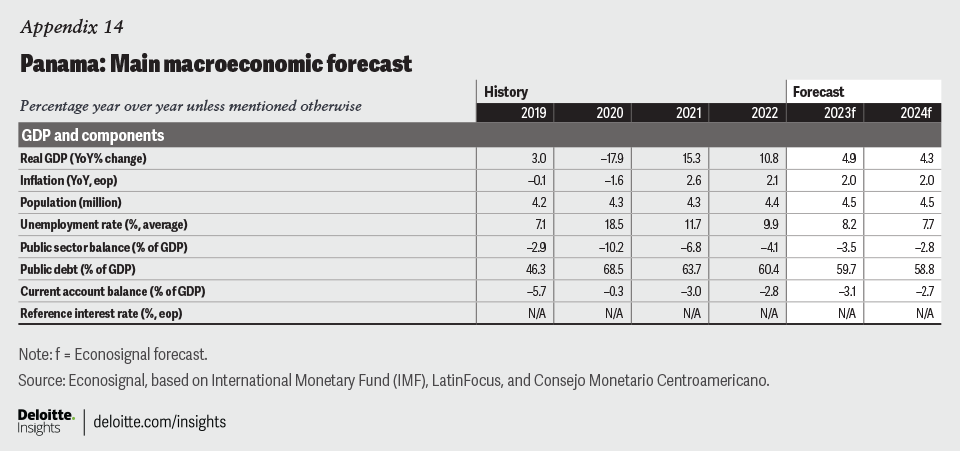

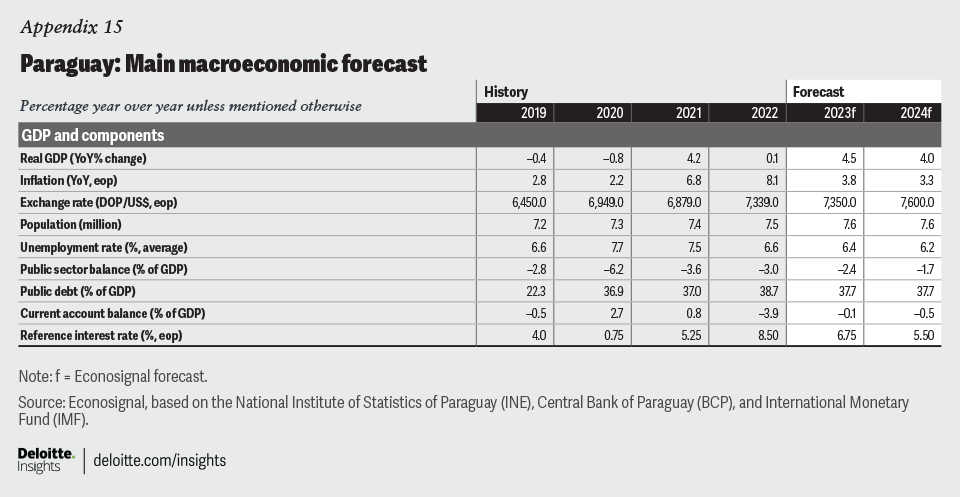

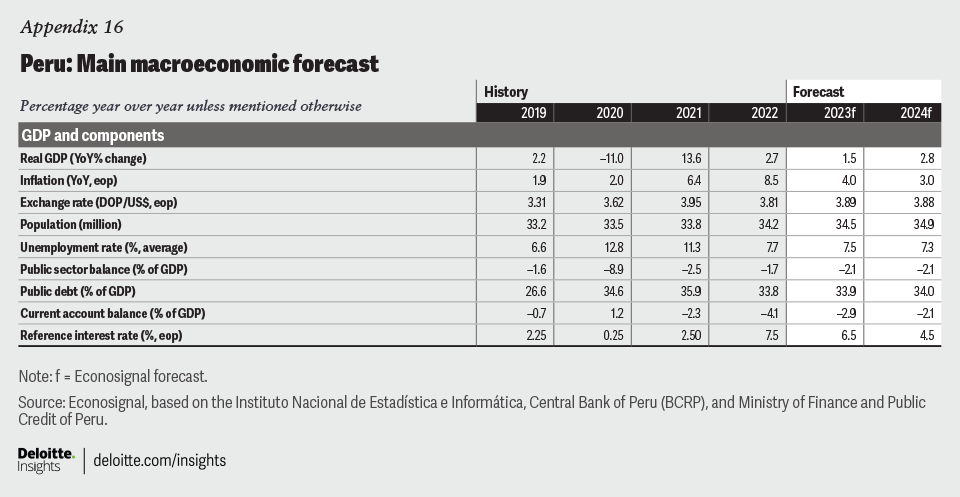

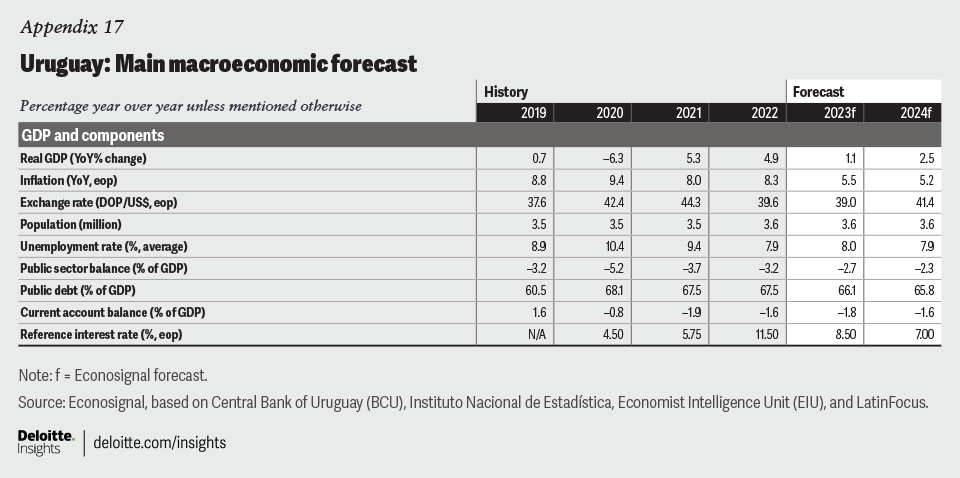

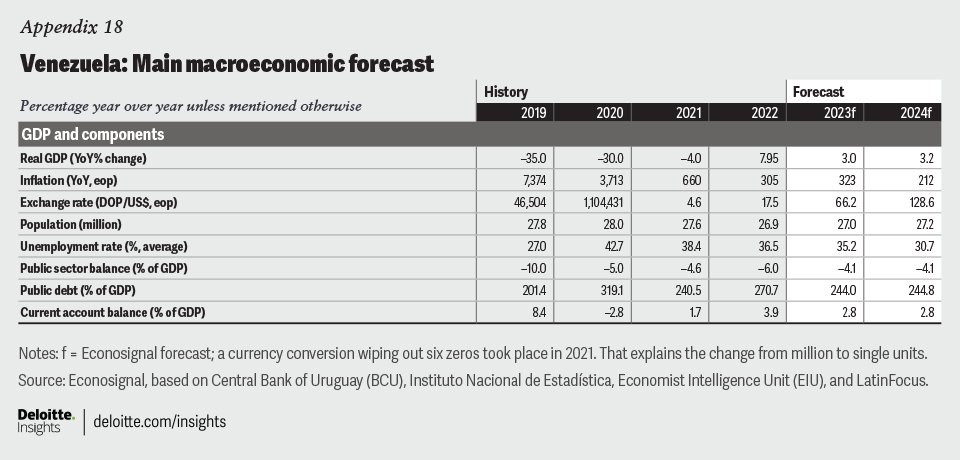

In this report, we analyze Latin American economic context and perspectives for 2024 amid these global forces. Lastly, we offer our forecast compendium for the economies of the region.

Introduction

In Latin America, the economic cycle has shifted from booming growth toward greater uncertainty. GDP figures soared when economic activities reopened at the end of COVID-19–induced restrictions, and most economies regained their prepandemic sizes by the end of 2022, growing 7% in 2021 and 3.9% in 2022.1 Despite this expansion, several supply-side shocks in the world economy triggered inflation and prompted central banks to raise interest rates.

As a result, Latin America began contractionary monetary policy before most advanced economies. Now that price pressures are mostly under control, the consensus is that monetary tightening should ease as well. However, this current juncture—embodied by the contradictory states of the world’s two largest economies, the United States and China—requires complicated decision-making.

In the United States, the Fed achieved what seemed like a “soft landing”—that is, overall price inflation was under control while the economy continued to outperform long-term expectations. Nonetheless, the Fed maintained its benchmark rate around 5.25% to 5.5% at its latest meeting. This peak would mark the end of the tightening cycle, but it is unclear when the Fed will start lowering rates. The American economy should slow down in the second half of the year and the International Monetary Fund forecasts GDP growth to stand at 1.8% in 2023.2 A strong economy and a more expensive US dollar would affect emerging market currencies and lead to capital outflows seeking less risky assets in the United States.

Meanwhile, China is facing major economic difficulties. GDP growth did not get a boost from the relaxation of the zero–COVID-19 policy. As a result, Q2 results (6.3%) were below market expectations (7.3%). The IMF expects China to grow 5.2% in 2023, up from 3% in 2022—below the lofty average of 9% observed since 1978.3 Moreover, several structural factors could be undermining China’s growth potential. First, aging demographics will progressively shift spending toward elderly care.4 Second, foreign investors are more cautious now and might be attempting to relocate—or at least diversify—supply chains away from China. Finally, domestic investment has weakened because of a downturn in the housing market. Once believed to be on the fast track to the top spot in the world economy by the 2030s, current prospects suggest that China might become a near-peer of the United States 10 or 20 years later. This is expected to have a profound effect on Latin America since much of its growth depends on China, which serves both as a buyer of commodities and a supplier of goods and capital.

This report looks at some of the consequences of this divergence in Latin American economic performance. First, we analyze the effects of the Federal Reserve’s decision to keep its rates unchanged on Latin American monetary policy. Then, we dive into the implications of slower Chinese growth, as it starts tempering its demand for commodities, impacting the Latin American economies heavily reliant on trade with China.

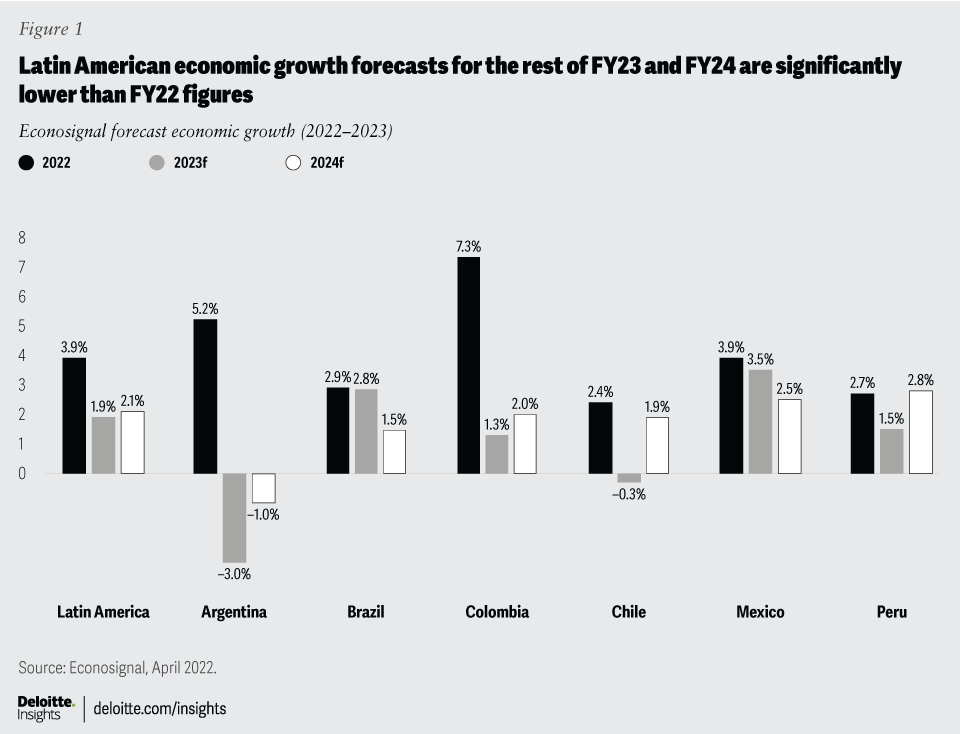

With that in mind, we expect GDP growth in the region to reach 1.9% in 2023. Our forecast considers three main factors:

- Weaking internal demand in the face of inflation

- Expansionary monetary policy possibly being less effective than expected

- Possibly dwindling export revenue from China

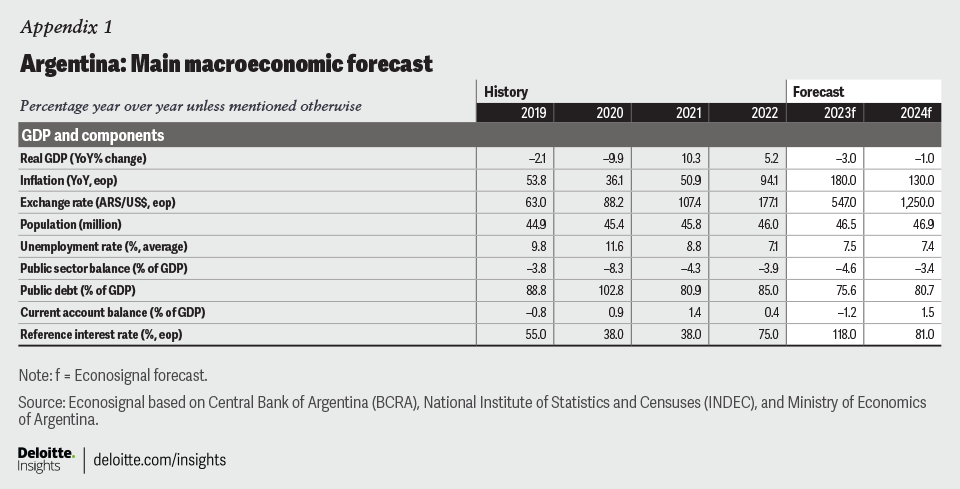

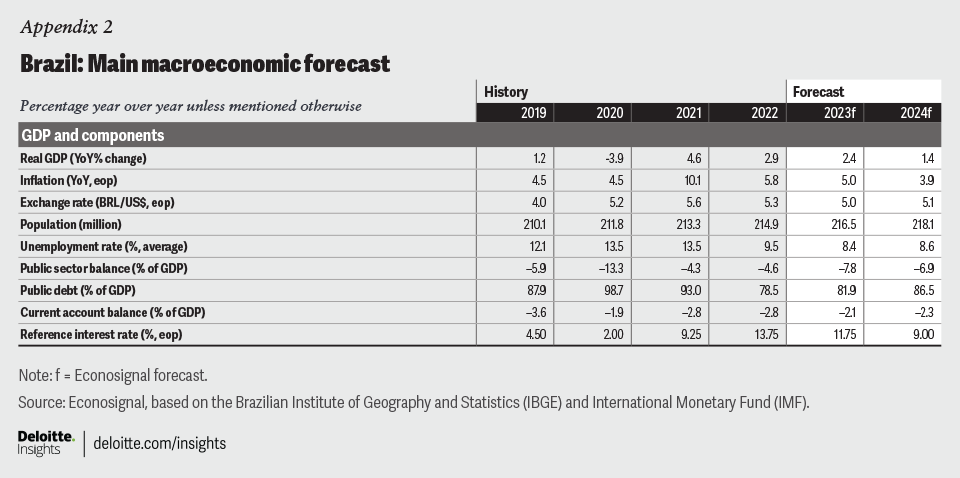

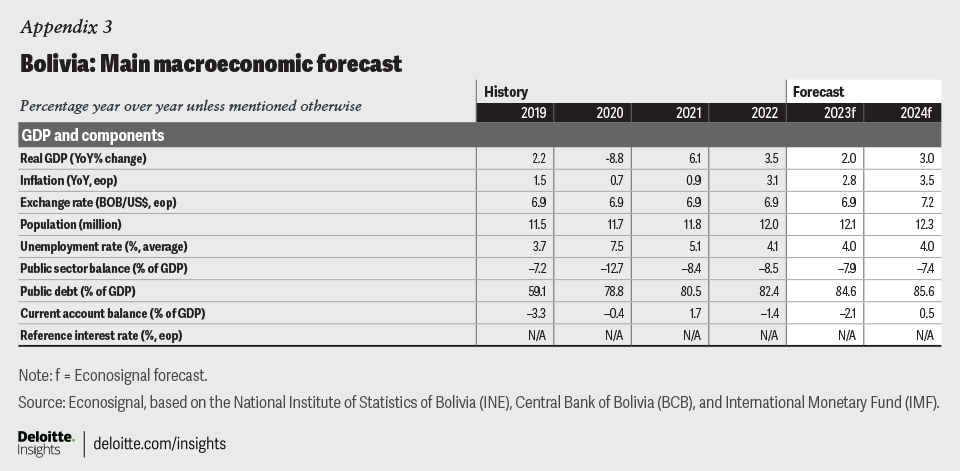

As for 2024, we expect growth to reach 2.1% on the back of a more stable inflation level, lower interest rates, and a favorable external sector (figure 1). The appendix has detailed forecasts for individual countries within the region.

{kind=link}

The monetary policy implications of a high Fed fund rate

A policy dilemma

In July, the soft-landing scenario looked like a reality in the United States: Inflation—at 3%—neared the Fed's target range; unemployment—at 3.6%—was close to a 50-year low.5 Several supply-side effects buoyed US economic activity, like dramatic drops in shipping costs and cheaper energy prices.

Although food and energy prices had fallen, core inflation proved to be sticky. Furthermore, recent inflation has increased because of higher oil prices. This prompted the Fed to maintain its funds rate in the current range of 5.25% to 5.5% at its latest meeting. This could spell trouble for Latin American nations depending on US trade.

The current monetary policy in Latin America presents a challenge to policymakers. A surge in inflation—primarily driven by external shocks like the war in Ukraine that elevated food and fuel prices—forced countries to hike interest rates. Now, the question is whether it is prudent to lower them at all. At the heart of the decision lies a trade-off between controlling inflation and encouraging economic activity.

On the one hand, inflation is subsiding as commodity prices are starting to stabilize—although production cuts by oil-producing countries have increased the price of oil since April6—and supply chain disruptions are gradually resolving. On the other hand, economic activity is slowing down in 2023. This decline can be attributed to numerous factors, mainly reduced consumer and business confidence amid economic and political uncertainty and reduced global demand.

The policy dilemma becomes more complex when considering the potential effects of the Fed’s decisions. Although there is a growing case for lowering interest rates to stimulate economic activity, a premature move could backfire. If Latin American countries lower their interest rates while the Fed maintains (or even raises its rates) its own, it could trigger a capital outflow, put stress on local currencies, and reignite inflationary pressures. Investors can shift their funds to the United States hoping for higher returns, potentially destabilizing the region's financial markets. Latin American economies are particularly vulnerable to these capital outflows due to their dependence on foreign investments to fund development projects and local economic activity.

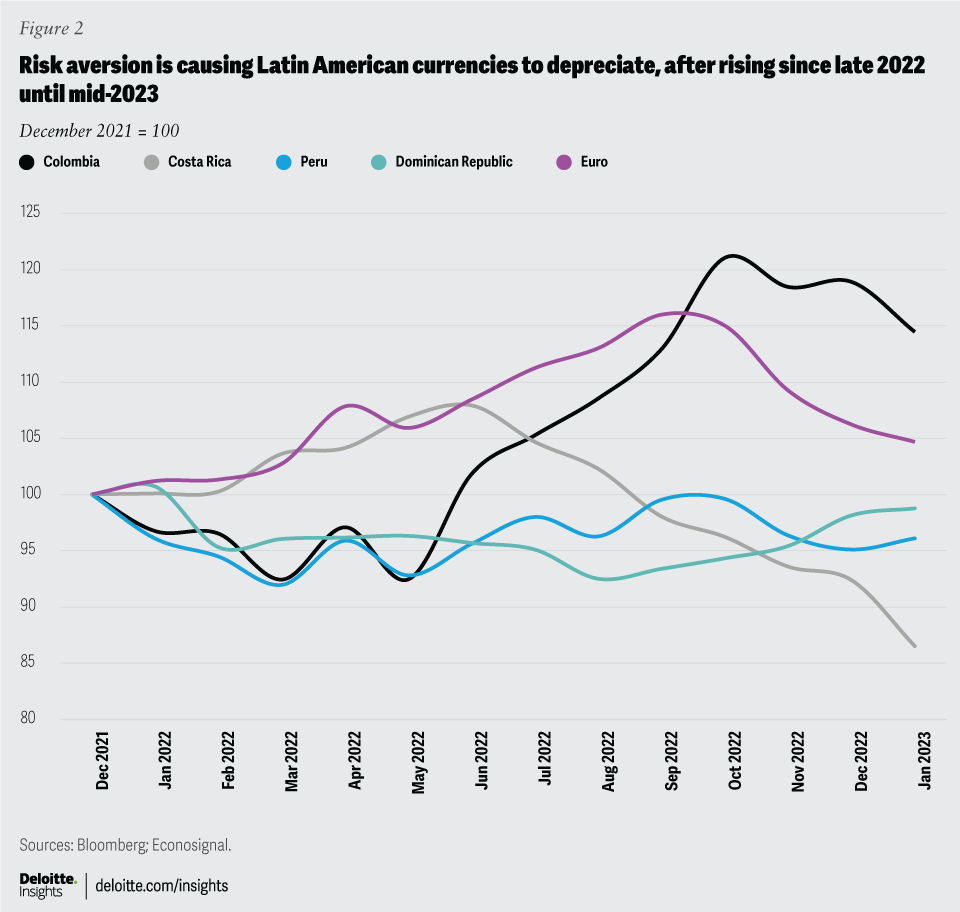

This problem is compounded by the increase in local exchange rates against the dollar. Since October 2022, currencies have appreciated strongly due to remarkably high interest rates. This has made Latin American exports less competitive and affected fiscal balances in places where export revenue is a crucial flow of government income. However, more risk aversion from the second half of the year has encouraged currency depreciations in the region (figure 2).

{kind=link}

Finally, public finances are also an important issue. In recent years, the rise in local and global interest rates has increased the proportion of public expenditure allocated for debt-servicing. Mexico’s share, for example, grew from 11% in 2022 to 14% in the first half of 2023, whereas the monetary policy interest rate from the central bank has risen from 4.0% to the current level of 11.25%. The increase in debt-servicing to expenditure between 2021 and 2022 can also be observed in Brazil (from 13.6% to 15.2%) and Colombia (from 10.5% to 15.0%).7

Finding the right course of action is paramount to maintaining stability and growth in the region. Thus, Latin American countries must engage in a waiting game, monitoring the Fed's actions and timing their own policy adjustments carefully, considering inflation, economic growth, public finances, and exchange rates.

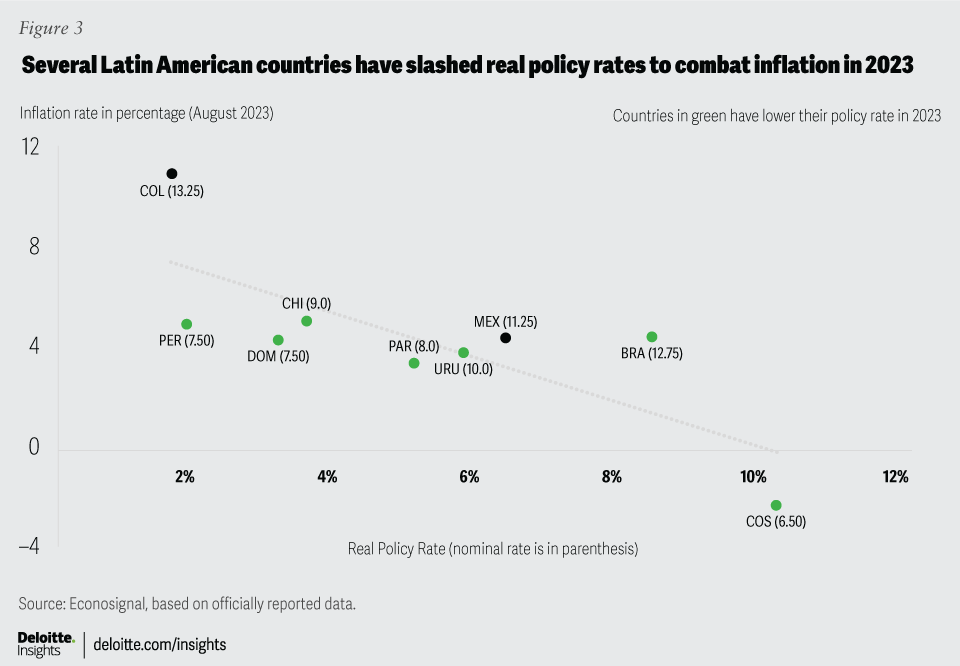

The early movers

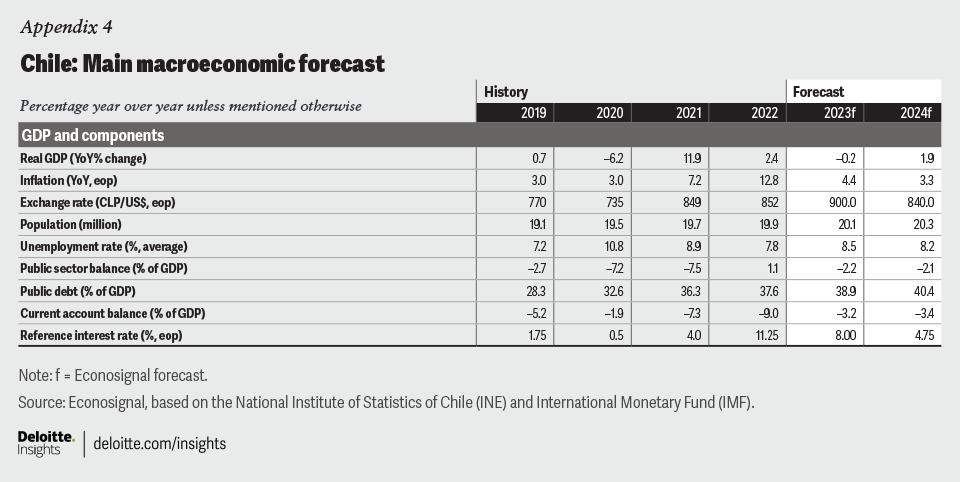

Costa Rica was the first Latin American economy to slash rates—by 50 basis points in March—first to 8.5%, and then after three more cuts, down to 6.5%. Uruguay cut rates on two occasions (by 25 and 50 basis points, respectively). Chile cut 100 points on July 28, partly because inflation had dropped from its peak in November (from 13.3% to 6.5%). However, the move coincided with an interest hike from central banks in developed economies. The Chilean peso was immediately under stress, dropping 1.6% against the dollar on the following day of trading and 7.5% to date. Nevertheless, before that central bank intervention, it had appreciated 12.2% from October 2022 to July 2023. Later, in September 2023, the bank announced another 75-basis-point cut.

Brazil’s central bank dropped its rate by 50 basis points to 13.25% in August and began its monetary policy tightening early by raising its rate from 7.75% in November 2021 to 13.75% in mid-2022. Consequently, the real interest rate jumped from 1% in April 2022 to 9% in July 2023—well within contractionary territory. The move paid off in the reduction of demand-led inflationary pressures, and the inflation rate shrank from 12.5% in April 2022 to a minimum of 3.0% in June 2023. Unlike Chile, Brazil has solid growth figures: Four percent in the first quarter and an expected rate of 2.1% for the rest of 2023.

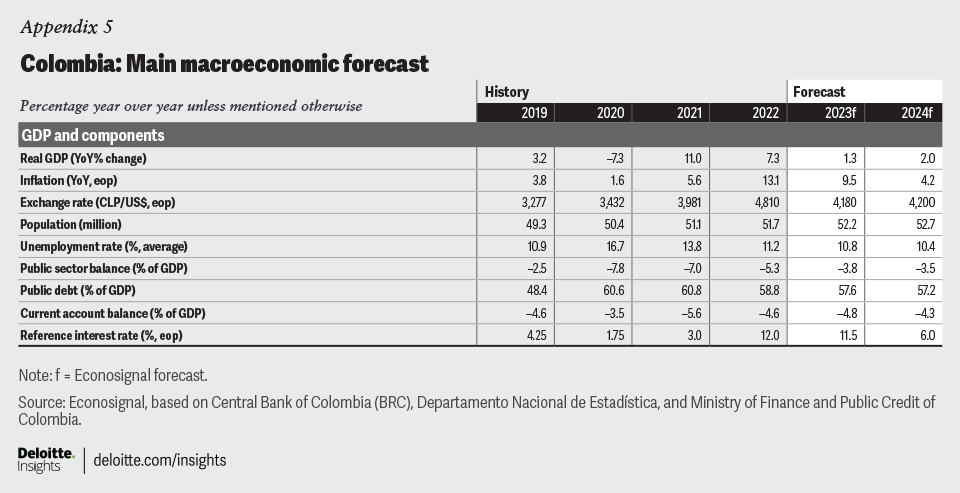

Other banks in the region—notably in Colombia and Mexico—have not started their monetary policy normalization. Odds favor at least one interest rate cut in Colombia before the end of the year, especially if growth figures continue to dwindle and inflation maintains its downward trend. Colombia is an interesting case because its inflation has been more persistent than in the rest of the region. Inflation peaked in March at 13.3% and has only dropped to 10.9% in September in Colombia. Even though the policy rate has been 13.25% since May, the real interest rate remains comparatively low. This combination complicates the timing of monetary policy normalization some more (see figure 3 for countries’ policy rate cuts in 2023).

{kind=link}

The impact of China’s slowing growth

The emergence of China as a global economic powerhouse profoundly affects Latin American economies. Over the past two decades, China has evolved from a distant trading partner to a central player in the economic landscape. Countries in the region supply vital commodities to China, while China has developed into an important trading and financial partner through investments, loans, and currency swaps.

Trade

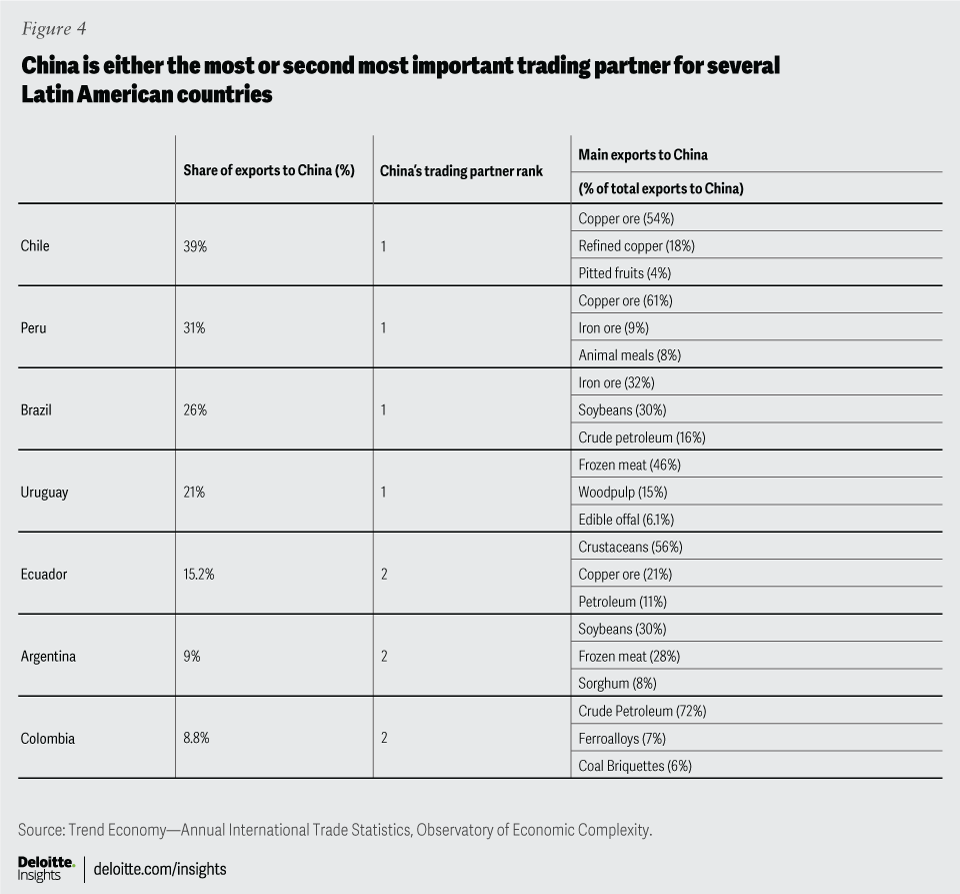

As illustrated by the sheer amount of bilateral trade, China has become a key trading partner for many Latin American countries (figure 4). Between 2000 and 2022, total trade between China and Latin America rose from US$12 billion to US$310 billion—more than 25-fold—with an average yearly growth of 15.9%. For comparison, global trade value has increased by only 6% rate per year since 1995, when the World Trade Organization was created.8 China has consistently been one of the largest trading partners for countries such as Brazil, Chile, and Peru. In South America, China is now the largest trading partner while being second largest in Latin America, behind the United States. The pattern of trade favors commodities from Latin America. For example, Brazil has become the main supplier of soybeans to China, with exports reaching 54 million tons in 2022. Furthermore, China has signed free-trade agreements with Chile (2005), Peru (2009), and Costa Rica (2010). In 2023, two more trade agreements were completed with Ecuador (May) and Nicaragua (August).

{kind=link}

Although this increase in trade has benefited the region, countries that export commodities to China may experience reduced demand and lower international prices, affecting their export revenues if China's growth remains subdued over the long term.

For example, the decline of the Chinese real estate sector. Once a major economic growth engine, it has seen a sharp decline in investment and new-home sales. This downturn led to a decrease in the prices of industrial metals such as copper, which dropped 15% since the end of January 2023.9 This immediately and profoundly affected metal exporters such as Chile and Peru, exposed as end markets to China. There are concerns that this may be a more permanent trend as China transitions from an investment-driven growth curve to a consumption-driven one.

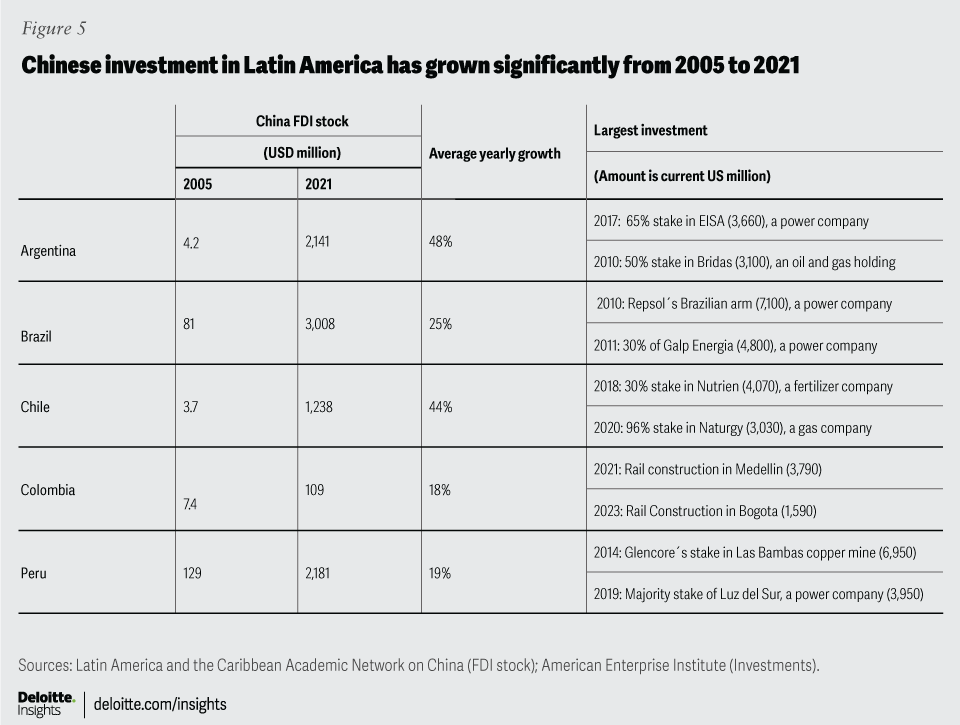

Investment

Chinese capital has emerged as a significant source of investment and loans for Latin America (figure 5).10 From 2000 to 2004, Chinese investment accounted for 1.44% of total foreign direct investment (FDI) in the region, increasing to 8.81% from 2020 to 2022. The main recipients were Brazil (47.5%), Argentina (24.5%), and Mexico (21.0%).11

{kind=link}

Chinese FDI can be channeled through Policy Banks (such as The China Development Bank) or through state-owned enterprises (SOEs) (such as the State Power Investment Corporation Limited). Investments favor projects in energy and mining, which account for more than 65% of all Chinese FDI in Latin America. Examples include the construction of a hydropower plant in Santa Cruz, Argentina, the second transmission line of the Belo Monte Dam in Brazil, and the Toromocho copper mine in Peru. China also invests in local companies; for example, China's National Petroleum Corporation (CNPC) holds a significant stake in Ecuador's oil industry, and companies like China State Grid Corporation and China Mobile have acquired assets in Brazil and other countries.

Countries in Latin America with substantial Chinese investment could experience varying effects. A slowdown in China may lead to a reduction in investment levels in the region. While China may continue to support certain infrastructure projects, financial assistance could become less generous. This would affect several areas, but most importantly infrastructure. If the funding flow is diverted from Latin America, countries with unfinished projects could be forced to look for alternative sources of funding.12

Debt and financing

Ever since the 2008 financial crisis, the People's Bank of China (PBC) has promoted the use of the yuan as an international payment currency. One way to ensure this was the introduction of bilateral swap lines—38 of which already exist in the world—including two in Brazil and Argentina.

Let’s take a closer look at the Argentinian agreement. In 2014, the Central Bank of Argentina (CBRA) agreed to exchange local currencies with the PBC for US$11,000 million. The agreement allowed CBRA to request a maximum of 70 billion yuan from the PBC and, in return, deposit an equivalent amount in Argentine pesos, with a repayment period of up to 12 months. The agreement was expanded in 2015 to 130 billion yuan, but a 2018 amendment indicated that if the IMF's standby agreement with Argentina was suspended or canceled, the PBC could reject BCRA drawings.

Following the meeting of the Presidents of the PBC and BCRA in January 2023, the activation of the currency exchange agreements was confirmed, and the nations committed to strengthening the use of the yuan on the Argentine exchange market. The agreement includes a special use of 35 million yuan to offset transactions in the foreign exchange market. When activated, this becomes part of Argentina’s external debt. As a result, Argentina transacts with China almost exclusively in yuan.

China made progress on the goal of extending the use of the yuan in Brazil as well. A March agreement established a clearing house to accelerate trade and investment. This means that a Chinese bank based in Rio has joined a yuan-based payment system supported by the PBC. The extent of these transactions is not available on official reports, but the yuan has recently surpassed the euro as Brazil's second foreign currency. However, the yuan only accounts for 5.37% of total reserves, and still markedly lags the dollar (80% of the total reserves) by a wide margin.

The Brazil example is emblematic of worldwide yuan use—although its usage has accelerated, it remains limited. Cross-border payments are by and large dominated by the US dollar (47.51%) and the euro (31.57%), with the yuan’s share reaching only 2.1%. Moreover, despite the creation of offshore clearing banks, liquidity shortages outside China persist.

Concluding remarks

Latin American economies, dependent on both the United States and China for trade and investment, face unique challenges and opportunities. The high-interest rates in the United States present a significant hurdle for Latin American economies to cross. The Fed’s monetary policy directly impacts capital flows, exchange rates, and inflation, making it challenging for Latin American countries to lower their own interest rates to stimulate domestic growth.

The growing importance of China in Latin America is strengthening exports, fostering economic diversification, attracting investment, and promoting economic growth. However, the recent lack of strong growth in the Chinese economy poses significant risks. Latin American countries that depend heavily on commodity exports could be confronted with reduced demand and lower prices, resulting, to some extent, in economic instability. In addition, if the region is too heavily reliant on Chinese investments, it may face market volatility and financial pressures.

The policymaker’s challenge is to get the most out of the global economy while trying to mitigate the impact of external shocks. Diversifying trade partners and strengthening domestic economic fundamentals (like productivity and innovation) are crucial strategies. Latin American countries may reevaluate their international alliances and partnerships based on the evolving dynamics between and within the US and Chinese economies. This could lead to diplomatic realignments and geopolitical implications in the region.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

by

Daniel Zaga

Mexico

Alejandro Mina

Colombia

Daniel Gonzalez Sesmas

Mexico

Federico Di Yenno

Argentina

Alessandra Ortiz

Mexico