India economic outlook, April 2024

Registering over 8% growth for three consecutive quarters, could India be progressing by leaps without bounds? The emerging consumer spending pattern and rising household debt are things to watch out for.

India’s GDP took a big leap on Leap Day in 2024: The country’s remarkable growth rate of 8.4% in the third quarter of the fiscal year 20241 surpassed all expectations, as market analysts had penciled in a slower growth this quarter, between 6.6% and 7.2%. Deloitte’s projected growth for the quarter was between 7.1% and 7.4% (as published in January 2024). With substantial revisions to the data from the past three quarters of the fiscal year, India’s GDP growth already touched 8.2% year over year (YoY) in these quarters.

We have revised our growth prediction for this year to a range of 7.6% to 7.8%, up from our previous estimates due to GDP revisions and stronger-than-expected growth in fiscal 2024. However, we expect growth in the fourth quarter to be modest because of uncertainties related to India’s 2024 general elections and modest consumption growth. Our expectations for the near-term future remain in line with previous forecasts with a slight change in the forecast range due to a higher base effect in fiscal 2024. We believe GDP growth to be around 6.6% in the next fiscal year (fiscal 2025) and 6.75% in the year after (fiscal 2026), as markets learn to factor in geopolitical uncertainties in their investment and consumption decisions.

The global economy is expected to witness a synchronous rebound in 2025 as major election uncertainties are out of the way and central banks in the West likely announce a couple of rate cuts later in 2024. India will likely see improved capital flows boosting private investment and a rebound in exports. Inflation concerns remain, however, which we believe may ease only in the latter half of the next fiscal year barring any surprises from rising oil or food prices.

In this edition of India economic outlook, the focus is on the emerging consumer spending patterns in India, highlighting the rise of the middle-income class. Not only has growth in consumer spending post pandemic been fluctuating, but there is also a shift in consumption patterns, with demand for luxury and high-end products and services growing faster than demand for basic goods. As we expect the number of middle- to high-income households with increasing disposable income to rise, this trend will likely get further amplified, driving overall private consumer expenditure growth.

But the challenge of rising household debt and falling savings could weigh on long-term growth sustainability. Controlling household debt to prevent it from crossing unsustainable levels will be essential to mitigate risks of debt overhang, maintain economic stability, and protect households against financial vulnerability.2

Decoding the growth seen in the third quarter of fiscal 2024

Real GDP growth climbed to 8.4% YoY in third quarter of the current fiscal year.

By the expenditure-approach method, GDP growth in the third quarter was aided by a strong uptick in private investment spending, which grew by 10.6% YoY. Investment growth remained above 8% YoY in the last four quarters, which indicates that India is on the cusp of a strong boost to the private capital expenditure cycle. High capital expenditure spending by the government over the past few years is now expected to crowd in private investments.

On the other hand, private consumption improved to 3.5% YoY from the third quarter of fiscal year 2024. The index of industrial production of consumer durables and improved passenger and two-wheeler sales indicated a revival in private consumption over this period. Data from the past three quarters points to India’s resilient domestic demand, which has aided its strong growth despite modest global growth and continuing geopolitical crises.

The biggest drag on GDP growth in the third quarter was government consumption, which contracted by 3.2% YoY, compared with growth of 13.8% YoY in the second quarter of the year. While growth in exports slowed in the third quarter (3.4% YoY), a faster decline in imports (8.3% YoY) due to falling crude oil prices helped net exports improve overall.

From the production side, gross value added (GVA)3 grew 6.5% YoY, which was in line with market expectations. Robust growth in manufacturing (11.6% YoY) and construction activities (9.5% YoY), along with a steady positive performance in services (7% YoY) kept economic activity strong. The contraction of 0.8% YoY in agriculture, however, weighed on the economy, with the sector contracting for the first time since 2019, which was partly expected as temporal rains impacted kharif crop production.4

Is the widening gap between GDP and GVA concerning?

The gap between the two measures of economic growth has led to confusion around the momentum of Indian economic activity.

While there is a wide gap between GDP (growing at 8.4%) and GVA (growing at 6.5%), this is not the first time that GVA growth has fallen far below GDP growth (figure 1). Over the past decade, there have been four other times when the difference between the two growth indicators has been over one percentage point. This quarter, improved net taxes together with a sharp contraction in agriculture led to this variation.

The actual concern that arises from this gap is that the demand side (measured by the expenditure-approach method) is growing faster than the supply side (denoted by the production approach). Thus, the signs point toward the fact that there could be excessive demand for too few goods. At the same time, poor agricultural output is likely to keep food supplies low, all of which could translate to higher inflation in the coming quarters.

{kind=link}

The near-term outlook

The strong growth observed this year has buoyed our outlook, and we expect India to grow between 7.6% and 7.8% in fiscal 2024 in our baseline scenario, followed by 6.6% and 6.75% over the next two years respectively (figure 2). (For more on our baseline and pessimistic scenario assumptions, see “Key assumptions for our projections”)

Key assumptions for our projections

Deloitte’s assumptions can be grouped into two buckets, namely an “optimistic” and a “pessimistic” scenario, with the former being more likely.

Optimistic scenario

Regional wars remain contained without having major implications for global supply chains and economy. Growth in the United States and the European Union likely rebound later in 2024. There is political stability after the elections in India and other major industrial nations such as the United States.

- The US Federal Reserve cuts policy rates twice this year as inflation moderates.

- Crude oil prices remain low and range-bound, as a Chinese economic slowdown and the pace of the global energy transition keep oil prices from rising.

- The Reserve Bank of India maintains a tighter monetary policy to ensure no strain on the lending sector, but eases repurchase rates later in the year.

- Government efforts toward expense consolidation continue, supported by buoyant revenues, even though expenses go up in election months.

- Indian state and central election results do not result in any political instabilities.

- Spending on infrastructure capital expenditure declines from next year on as production-linked incentive capacity investment and crowding in effect boost private investment spending after the elections.

Pessimistic scenario

The Russia-Ukraine crisis continues for a prolonged period. Tensions escalate, with several nations getting directly involved in the war. The United States and Europe enter a recession with significant political upheavals. The crisis in the global banking system raises significant tail risks for economic activity:

- Prolonged crises lead to second-order implications on financial stability and supply chain disruptions.

- Crude oil prices breach the ceiling of US$110 per barrel.

- Political instability ensues after Indian central and state elections impact market sentiments.

- Inflation spirals up both globally and domestically, impeding investment growth.

- Climate inaction leads to more natural disasters that weigh on growth, further dampening sentiment.

- The Reserve Bank of India effects further interest rate hikes but retracts these later as growth tumbles.

We are now seeing the difference between actual GDP from the potential (pre-pandemic GDP levels)5 progressively narrowing as growth picks up pace (figure 2). We believe that private investments will gain momentum later this year as election-related uncertainties are out of the way, while global liquidity conditions improve as central banks in the West ease their monetary policy stance and cut policy rates.

A synchronous global recovery next year will likely help improve exports while improved capital flows will drive higher investment and consumption. This may lead the Indian government to recalibrate its spending, leading to a faster decline in the fiscal deficit and an increase in private investments.

{kind=link}

Inflation concerns are likely to persist as we expect demand to exceed supply at least in the short term. Higher food prices will also exert pressure on overall prices. However, as private investment kicks in, the supply side will improve, and prices will come down. Although, prices are expected to remain above the Reserve Bank of India’s target level of 4% over the forecast period due to strong economic activity (figure 3).

{kind=link}

The post-pandemic tale of consumers

Consumer spending in India has been low after the pandemic, and the rebound has been inconsistent as well. One of the biggest reasons has been the prolonged impact of the pandemic across consumer segments, exacerbated by subsequent global uncertainties. According to a survey by the Reserve Bank of India, consumer confidence has barely reached pre-pandemic levels, and the improvement over the past few months has been gradual, despite a strong pickup in economic activity (figure 4).

{kind=link}

Indian consumers are becoming aspirational

That said, the rapid growth of the middle-income class has led to rising purchasing power and even created demand for premium luxury products and services. India’s per capita income has steadily increased by 140%—from US$1,673.95 in 2014 to US$2,341.10 in 2022. According to Engel’s law, luxury goods and services have a high income elasticity, indicating that the demand for such items is strongly influenced by changes in consumer income. As income grows, consumers tend to allocate a larger proportion of their budget to luxury goods, leading to a more pronounced increase in demand for these items compared with necessities such as food. At the same time, goods with low income elasticity, such as food and groceries, will see a stagnating demand with rising income.

We believe this trend is deep-rooted and may even be amplified going forward.

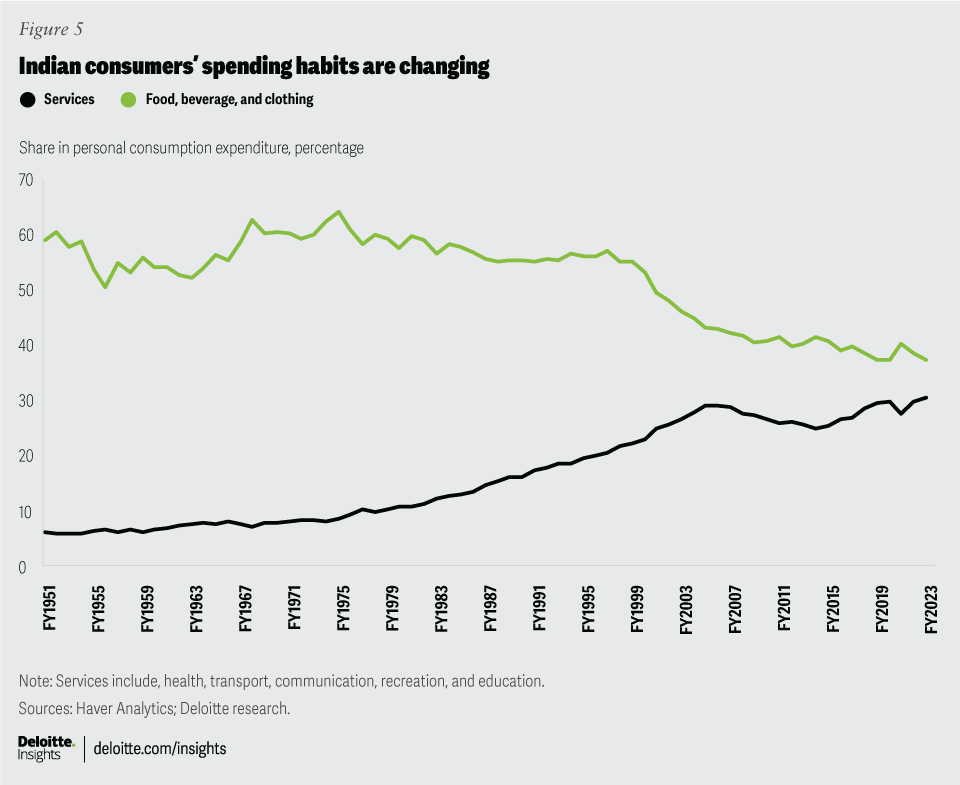

The results of the Household Consumer Expenditure Survey in India, conducted between August 2022 and July 2023, point toward this prominent shift in consumer behavior among Indian households over the last two decades.6 The falling proportion of spending on traditional products (such as food, beverages, and clothing) in the past decade, compared with rising spending in luxury and aspirational products and services categories (such as travel and entertainment) is considerable (figure 5). The country’s large young population, urbanization trends, and changing consumer preferences have also contributed to this shift.

{kind=link}

In the coming years, this trend will amplify. As India races to clinch the third spot in terms of GDP, the consumer market is also set to become the world’s third-largest by 2027. By 2030, close to one in two households will belong to either high- or upper-middle-income categories with growing disposable incomes.

That means the income pyramid is likely to get bulkier at the top half while the lower end of the pyramid will get narrower (and look more like a polygon) as more people move out of poverty and aspire to move up the pyramid (figure 6).

We expect that the rising number of people with higher disposable income will create a higher demand for luxury and premium products and services.

{kind=link}

India’s spending share in the luxury and premium goods and services category (such as spending on transport, communication, recreation, etc.) has traditionally been lower than nations such as the United States, China, Japan, and Germany (figure 7). There is, hence, potential for this ratio to increase further as consumer income grows.

{kind=link}

Rising levels of household debt is a concern

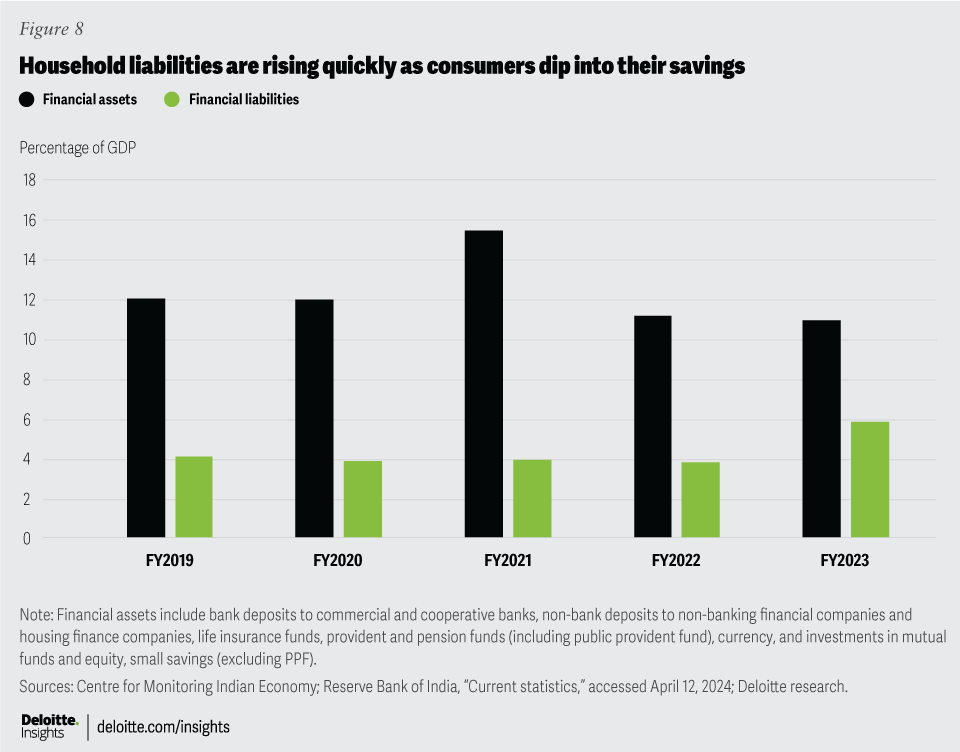

Amid the shift, there is another worrying trend that is emerging: Household liabilities (as a percentage of GDP) surged last year, going up from 3.6% to 5.8% of GDP (figure 8). Moreover, trends in credit deployment across different sectors of the economy have shown a rising share of household credit in the form of credit cards, consumer durables, and personal loans. Unsecured lending has gone up significantly as well, with its share accounting for close to 31.4% of total bank credit to households.7 To counter this, the Reserve Bank increased risk weights associated with unsecured personal loans (excluding housing, education, vehicle loans, and loans secured by gold). Consequently, banks’ risk weights for credit card loans and lending to non-bank financial companies (excluding core investment companies and priority sector lending) have increased.

This rising household debt-to-GDP ratio has led to a decline in household net financial assets, which indicates that Indian households are probably dipping into their savings, in addition to taking loans to support their consumption. Gross household financial savings, which surged to 15.4% of GDP in fiscal 2021 (the peak year of the pandemic) due to large precautionary savings, fell to 11.1% in fiscal 2022, and further to 10.9% a year later, reverting to its pre-pandemic trend (an average of 11% between fiscal 2012 and fiscal 2020). At the same time, household net financial savings (gross financial assets minus gross financial liabilities) fell sharply to 5.1% of GDP in fiscal 2023 from 11.5% in fiscal 2021—well below its long-running annual average of 7% to 7.5%.8

{kind=link}

That said, India has far less household debt than several other developing nations, despite the recent rise in financial obligations.9 In addition, India’s household-debt-service ratio is one of the lowest compared with many major economies. India’s debt-service ratio rose from 5.2% to 6.7% (as of February 2024) but remains lower than that seen in the United States at 7.6%, in Japan at 7.5%, in the United Kingdom at 8.5%, and in South Korea at 14.2 %.10 As a result, household debt stress is less likely in India.

Prudent consumer spending can help sustain growth

Wealth concentration among the wealthiest, the decline in household savings, and rising debt levels reflect the increasing divide in consumption expenditure and may impact the sustainability of consumption growth. Some of the following corrective measures can help ensure that household spending rises sustainably.

- More employment opportunities for those residing in rural and semiurban areas can help increase savings. The good news is that the number of salaried people has been rising consistently. The not-so-good news is that agriculture accounts for close to 44% of total employment, while the sector accounts for only 17.5% to 18% of GDP.11 The movement of disguised employment12 away from agriculture to manufacturing, construction, and services will likely improve income prospects. Government spending on infrastructure projects is also expected to create jobs, improve efficiencies, and drive consumption. The government’s emphasis on upskilling and reskilling ecosystems in emerging technologies (an initiative known as FutureSkills Prime 2021) and improving the health of citizens (through Ayushman Bharat) will also contribute to better employability and productivity.13

- While credit growth is needed for strong economic activity, credit availability to stimulate demand is contributing to rising household debt levels, potentially creating financial vulnerabilities for households. The Reserve Bank of India will have to keep an eye on rising debt. While it has taken proactive steps to check unsecured lending, it should also encourage banks to use data analytics for informed lending decisions.

- The emergence of financial technology firms offering alternative lending options should also be closely monitored to ensure that consumers do not increasingly rely on online platforms for debt to meet aspirational goals. In this regard, the Reserve Bank of India has proposed to create a Fintech Innovation Hub by April 2024 to improve transparency in fintech lending.14 In addition, the government can offer financial education programs and credit counseling services to inculcate responsible borrowing and repayment planning, to avoid long-term financial instability and debt accumulation.

- Income support programs or direct cash transfers to vulnerable sections of society can also help reduce income disparity, given the proportion of the population that is still in the low-income category. India is preparing to replace the minimum wage with a living wage by 2025 and has sought technical assistance from the International Labour Organization to create a framework for estimating and operationalizing it.15 Living wages—a minimum income necessary for a worker to meet their basic needs, factoring in key social expenditures such as housing, food, health care, education, and clothing—will help India mitigate poverty.16

India is seeing a prominent shift in consumer behavior toward aspirational spending, which is inevitable in any nation that experiences growing economic prosperity. While India must prepare itself for this shift, it must also ensure that the risks associated with increased household debt levels do not pose systemic risks to the macroeconomic environment, potentially amplifying economic downturns and weakening recoveries.