Business optimism is rebounding in Europe, but CFOs are still cautious

After a challenging winter for Europe's economy, Deloitte’s Spring 2024 European CFO Survey signals optimism is rising among finance executives

Rolf Epstein

Richard Muschamp

Dr. Pauliina Sandqvist

Ram Krishna Sahu

It was a tough winter for most European economies. Elevated inflation, even if already easing, weighed especially on the purchasing power of households and businesses. Restrictive monetary policy weakened demand for goods and services and increased financing costs in Europe and many other countries. Meanwhile, uncertainty about the economy and geopolitical tensions made both consumers and businesses hesitant to increase their spending or investments.

These challenges seem to be becoming less severe, however, as the spring 2024 edition of Deloitte’s European CFO Survey signals optimism is rising among finance executives.

Business sentiment is rising among European CFOs

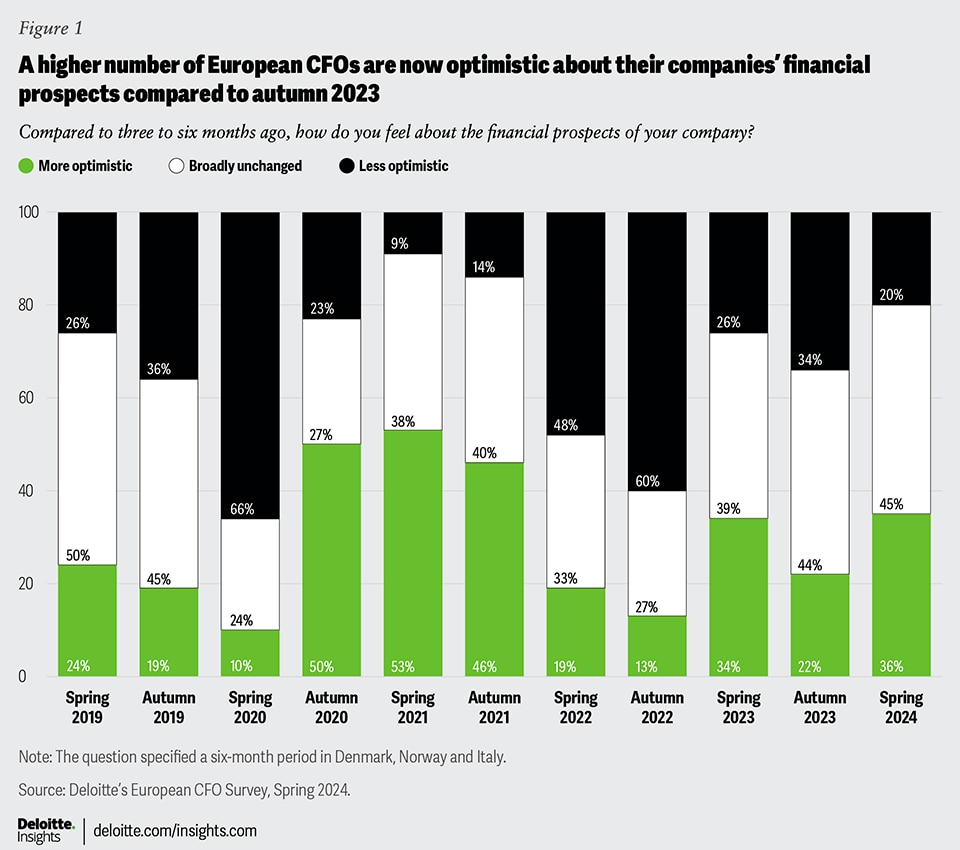

The survey, which took place between March and April 2024, included more than 1,300 CFOs across 13 countries in Europe. It finds increasing optimism, as 36% of CFOs are now feeling ‘more optimistic’ about their companies’ financial prospects than three to six months earlier (compared to 22% in the autumn 2023), whereas 20% reported feeling ‘less optimistic’. The remaining 45% reported an unchanged outlook (figure 1). Hence, the net balance of business confidence, which measures the difference between the share of positive and negative responses, increased to +16, up from -12 in autumn 2023 and above the average of 3 since the survey began in 2015. This indicates that the outlook is generally improving for European CFOs, but overall, many remain cautious.

Sentiment recovered in 12 of the 13 countries is represented in the survey. Ireland was the exception, but for encouraging reasons: There, already positive sentiment remained unchanged at a high level. (Irish CFOs continue to be the most optimistic in Europe.) Meanwhile, CFOs in Spain reported the second-highest level of optimism, which is not surprising given the Spanish economy has performed better than most European countries in the past six months. On the other end of the spectrum are Italy and the Netherlands. Even though business sentiment among Italian and Dutch CFOs is better than six months ago, the net balance is the lowest among the 13 countries participating in the survey.

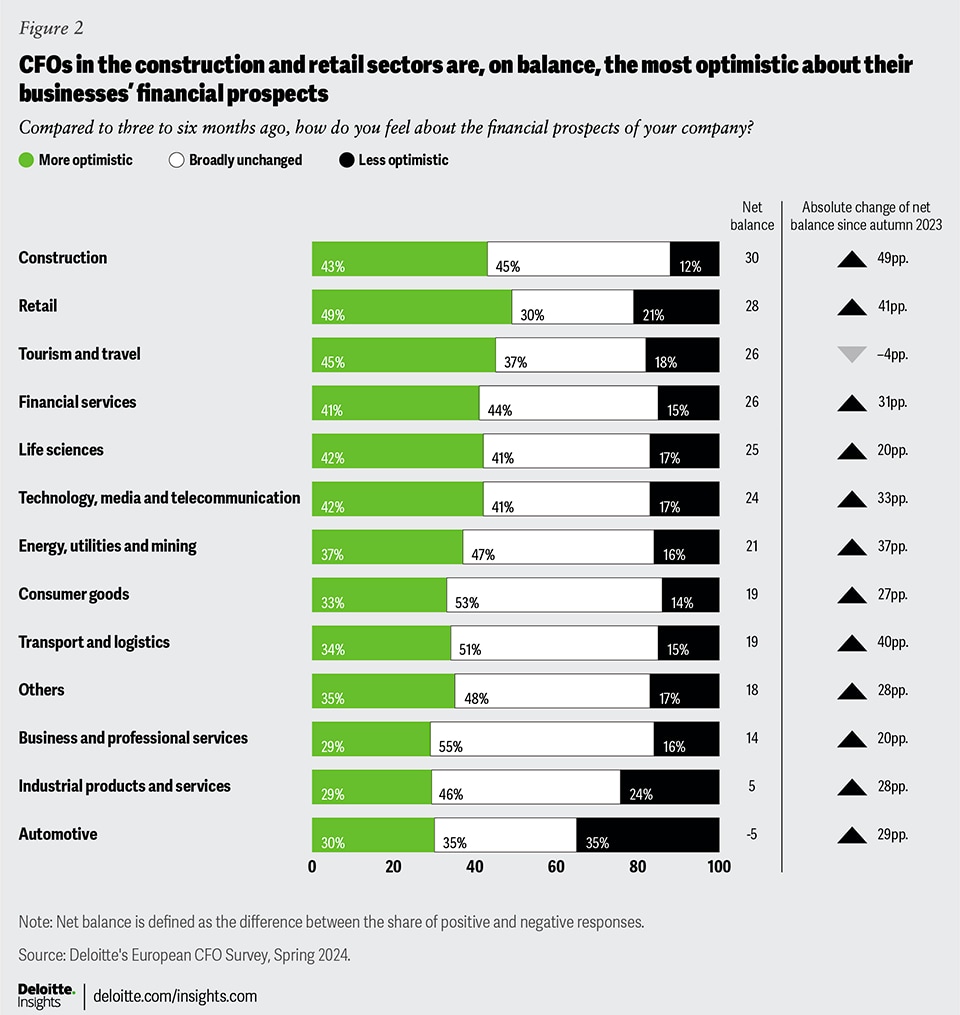

CFOs in the construction, retail and tourism sectors are the most optimistic

Business confidence has risen in all sectors except for tourism and travel, where it had already plateaued at an elevated level. Tourism and travel was the most optimistic sector when we last conducted our survey in autumn 2023, and it is still profiting from a post-pandemic recovery, but in the spring, optimism in the construction sector took the lead. Construction CFOs reported a remarkable upswing in sentiment, with expected interest rate cuts surely one of the factors boosting their confidence. A rebound in business sentiment is also evident among retailers, as easing inflation and robust wage growth should fuel more consumer spending.

Confidence among CFOs in the automotive sector also improved. However, the net balance is still below the zero line, indicating that more automotive CFOs describe their financial prospects as ‘less optimistic’ than those who describe them as ‘more optimistic’. European auto manufacturers still face many challenges, although to a smaller extent than in the autumn.

Geopolitical risks are CFOs’ top concern

For over a year, from autumn 2022 to autumn 2023, the economic outlook had topped the list of concerns for European CFOs. As the worst of the economic downturn should be behind us, it is not surprising that European CFOs no longer list the economic outlook as the main risk to their businesses. Now, they rate geopolitical risks to be the key threat to their businesses over the next 12 months. Russia’s invasion of Ukraine, renewed conflict in the Middle East and the continuing US-China rivalry, to mention a few, are clearly on the minds of CFOs as they contemplate where to invest and how to secure their supply chains. 2024 is also a year of elections with polls for the EU Parliament and the US presidency, as well as a potential UK general election. Commodity prices, supply chains and trade are increasingly intertwined with national security, technology development and energy transition.

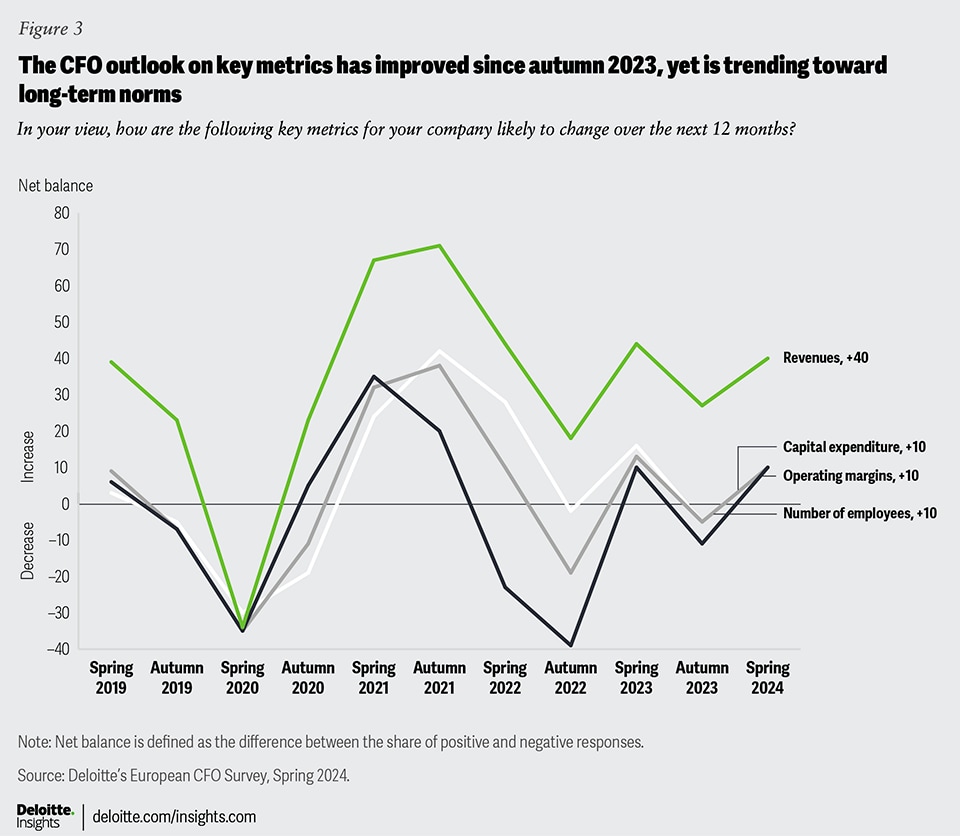

CFOs’ expectations for revenue, capex and head count improve (a little)

Looking at their key metrics over the coming 12 months, European CFOs indicate that while their expectations for revenue capital expenditures, margins and head count have improved since the autumn, they have not bounced back in the same way as their overall business confidence. This indicates that CFOs remain cautious in their planning, which is not surprising against the backdrop of increased geopolitical risks.

The revenue expectations of European CFOs are now more positive than in autumn 2023. However, this indicator has only just returned to the same level, as its long-term average, suggesting a reversion to the mean, rather than breakout levels of revenue growth, is expected over the next few months. As with business confidence, CFOs in Ireland and Spain currently report the highest expectations about future revenues. In contrast, survey respondents from Italy and Germany have the most cautious revenue expectations.

Looking across sectors, CFOs in life sciences, financial services, and tourism and travel expect the highest increases in revenue, whereas their peers in the automotive sector forecast decreasing revenue, although to a smaller extent than six months ago.

Meanwhile, CFO optimism about operating margins rose more than that of revenues. This is likely because the reduction in the rate of inflation is assumed to continue, although more slowly than now, and interest rates (and thus financing costs) are expected to start declining soon.

European financial executives plan to cautiously extend their capex over the next 12 months. CFOs in energy, utilities and mining expect the greatest increase in capex, followed by transportation and logistics, as well as tourism and travel. Not surprisingly, considering their low levels of financial optimism, CFOs in the automotive sector plan to decrease capex. Meanwhile, construction CFOs foresee stagnating capex in the year ahead, despite their strong business confidence. When it comes to the labour market, European CFOs are not expecting significant changes over the next 12 months. The net balance is marginally positive, indicating CFOs only expect a slight increase in headcount overall.

Given all these varied sentiments and expectations about business conditions, how are European CFOs shifting their strategic focus? Whereas in autumn 2023 most European CFOs were concentrating on cost-cutting as their strategic priority, now organic growth has become equally important. This shift in priorities appears to be a response to improving economic conditions and highlights an opportunity for businesses to refocus on expansion and growth, especially within their home markets at a time of high geopolitical uncertainties.

Is cautious optimism here to stay?

Deloitte’s Spring 2024 European CFO Survey highlights Europe’s evolving economic landscape, with CFOs exhibiting a more positive, albeit varied, outlook on their business prospects. Their cautious optimism, despite geopolitical tensions and economic uncertainty, is trickling through to their expectations for revenues, capex, headcount and operating margins, all of which have risen moderately since the autumn.

Taken overall, these findings represent a welcome improvement after a challenging winter marked by sluggish economic activity, strict monetary policy and geopolitical instability. Whether or not they signal a more lasting upswing in business sentiment, however, will depend on many factors. These include the future trajectory of disinflation and the timeline for central banks to begin lowering interest rates. Meanwhile, CFOs will also be closely watching how existing geopolitical conflicts evolve. Finally, the results of upcoming elections will also significantly influence their view of the future business landscape.

As CFOs navigate the challenges and opportunities that lie ahead, they’ll need to stay informed and adaptable to these emerging economic and political dynamics, prioritise risk management and balance growth and cost efficiency.

About the Deloitte European CFO Survey

Deloitte has conducted the European CFO Survey since 2015, giving voice twice a year to senior financial executives from across Europe. The data for the spring 2024 edition was collected in March and April 2024 via an online survey and reflects responses from 1,333 CFOs in 13 countries (Austria, Denmark, Germany, Iceland, Ireland, Italy, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom) and across a wide range of industries.

{kind=link}

{kind=link}

{kind=link}