Keeping the lights on during the COVID-19 pandemic: Tracking the status of mortgage and rent payments Economics Spotlight, July 2020

8 minute read

29 July 2020

Even in the best of times, the average American consumer is likely to struggle to keep up with housing-related expenses when faced with a loss of employment income. The COVID-19 pandemic has significantly increased the number of Americans facing a job loss. We look at how the pandemic is affecting individuals’ capacity to stick with rent and mortgage payments amid income uncertainty.

The average American consumer spends a lot of money on housing. Depending upon income, housing accounts for anywhere between 30% and 40% of total annual household expenditure.1 Loss of income at any point in time—even during an economic expansion—is likely to weigh heavily on the average household’s ability to pay mortgages or rent on time, as well as on the ability to make other housing-related payments such as paying for utilities, housekeeping supplies, furnishing, or household equipment. In October 2019 (the month of the survey), 4% of the adult population in the United States left their mortgage or rent obligations unpaid or paid partially; 5% didn’t pay for utilities.2

Learn more

Learn how to combat COVID-19 with resilience

Explore the Economics collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

The COVID-19 pandemic, which has resulted in millions of Americans losing jobs or working fewer hours and for less pay3 has put households across the United States in the unenviable position of having to keep the lights on while also making a stream of fixed mortgage and rent payments on an uncertain flow of income. Fiscal support has provided temporary solace; a more permanent solution is unlikely until an effective medical intervention stops the pandemic.

In this report, we use the Census Bureau’s weekly household pulse survey data from week 1 through week 8 (April 23 to June 23) to gauge how the consumer is faring with respect to payment of mortgages and rent.4 Taken together, mortgages and rent account for 35% of annual spending on housing and 11.5% of total annual household spending.5 Mortgages are crucial to the financial system because they account for roughly 70% of US$15 trillion in outstanding household debt.6

Mortgage and rent payments have been held up by fiscal support, but how long will this last?

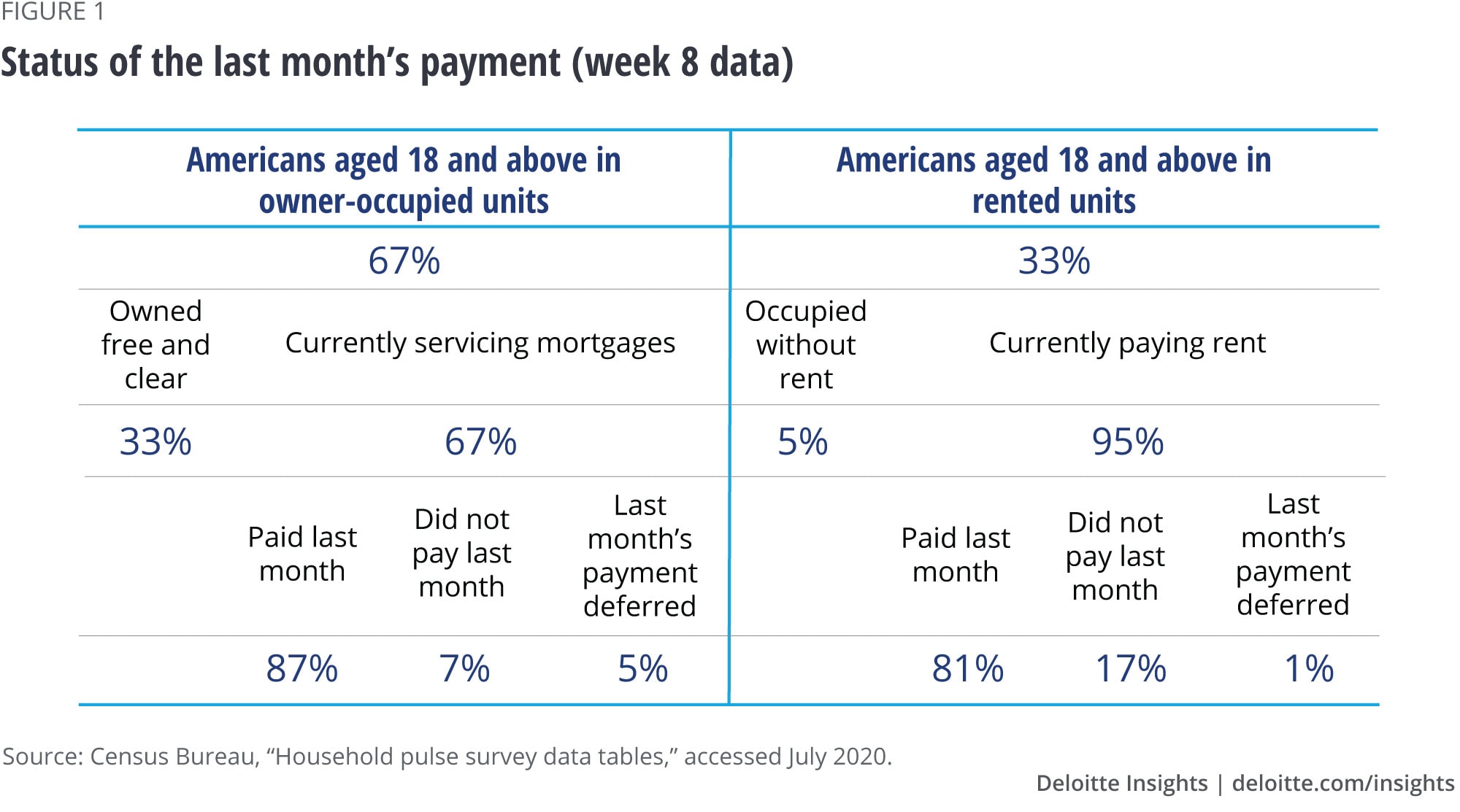

Two-thirds of Americans aged 18 years and older live in owner-occupied housing units. The remaining third live in rented housing units. This ratio varies by age—younger cohorts are more likely than older cohorts to rent rather than own—and by race—Black Americans are much less likely to own relative to White Americans or Asian Americans.

According to the latest survey data (week 8—June 18 to June 23—at the time of writing), a third of the population aged 18 years and older living in owner-occupied housing units are covered by fully paid-off mortgages and therefore do not carry the burden of monthly payments. The remaining two-thirds of adults in owner-occupied units continue to service mortgage payments since they don’t own their houses free and clear. This accounts for 45% of the total population aged 18 and above. Of those with a mortgage, 87% made the previous month’s mortgage payment, 7% didn’t, and 5% had mortgage payments deferred. This means roughly 5.5% of the adult population either left mortgages unpaid or had payment deferred in May. This is not a terrible figure compared to 4% in October 2019, especially given the scale of the pandemic’s impact on the labor market.

Fiscal stimulus payments and enhanced unemployment insurance have enabled some mortgage payers to stay current with their payments despite losing their job. Data from week 8 of the survey indicates that almost 20% of adults in owner-occupied housing units currently servicing mortgages used stimulus payments or unemployment insurance to meet spending needs in the last seven days. Mortgage delinquency tracked by the Mortgage Bankers Association, though down from its peak in the wake of the financial crisis, increased to 4.4% in Q1 2020 from 3.8% in Q4 2019.7 If fiscal support and forbearance are withdrawn, missed payments are likely to push the mortgage delinquency rate higher. According to estimates made by the Dallas Fed, the mortgage delinquency rate in the absence of the CARES Act would be 6.2% in Q2.8 A further rise in delinquency is likely in subsequent quarters, especially if the labor market recovery is slow and long drawn out. Early signs of a recovery in May and June might not be sustainable as a resurgence of the virus is causing a rollback in reopening plans in many parts of the country.9 Deloitte research indicates that 30-day mortgage delinquencies will peak at 14.2% in 2021, higher than the previous peak of 12.1% during the financial crisis in 2009.10

Among the 33% of adult Americans who live in rented units, 5% occupy without rent, according to survey data from week 8. Out of those who pay rent, 81% were able to pay their rent in the previous month, 17% didn’t, and 1% had payments deferred. This implies 5.9% of the adult population left rent unpaid or partially paid in the previous month. At least 25% of American adults currently paying rent used stimulus payments or unemployment insurance to meet spending needs in the last seven days.

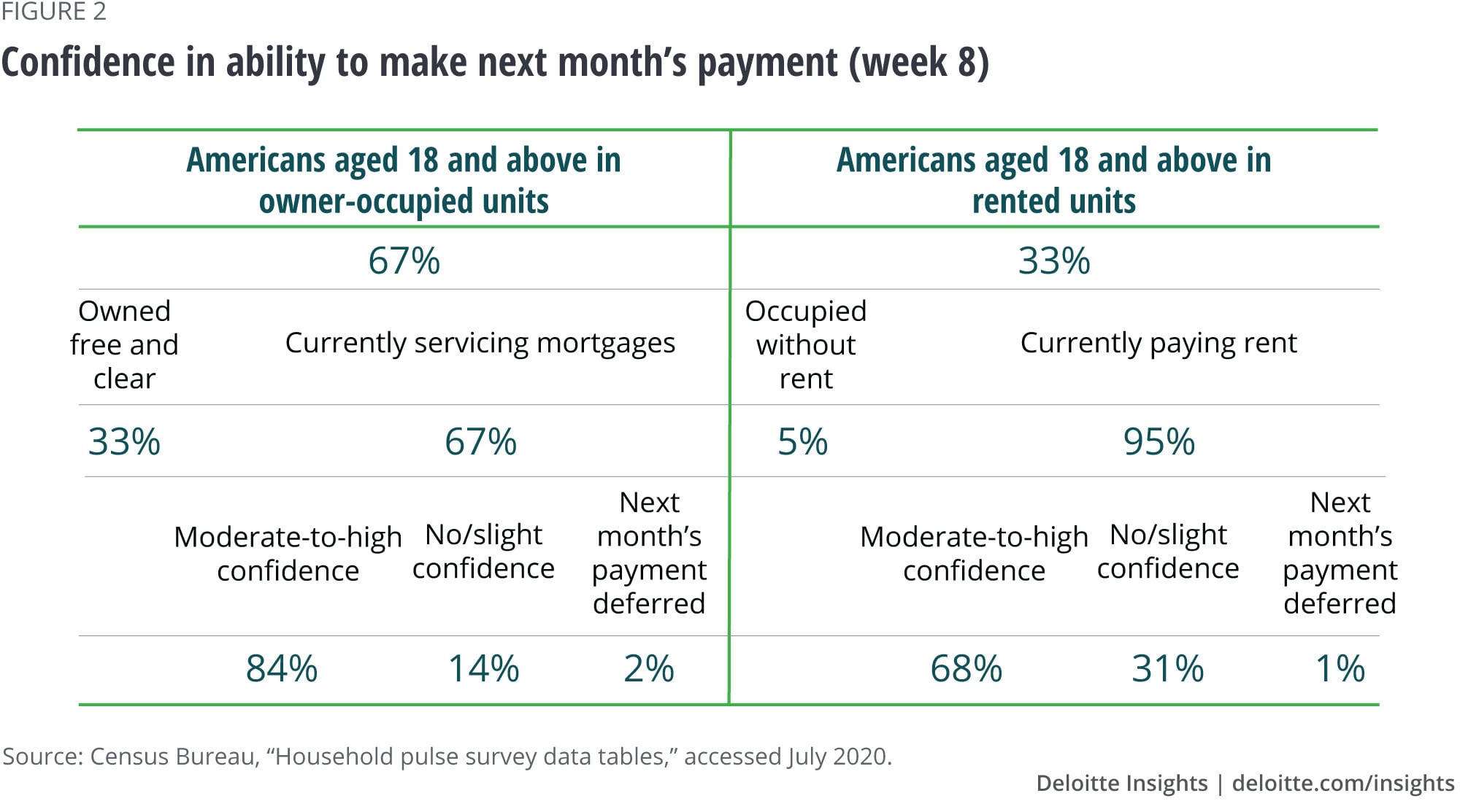

While 7% of adults in an owner-occupied unit with a mortgage didn’t make their payment in the previous month, 14% had little or no confidence in their ability to make next month’s payment, according to week 8 survey data. This is relatively unchanged from 15% in week 1 of the survey. Among renters, while 17% of adults in rented units did not pay rent in the previous month, 31% had little or no confidence in the ability to make next month’s payment according to week 8 data, again relatively unchanged from 30% in week 1. Confidence in the ability to make payments could deteriorate as the impact of one-time stimulus payments recede and enhanced unemployment benefits end.

The pandemic is weighing more heavily on low-income households

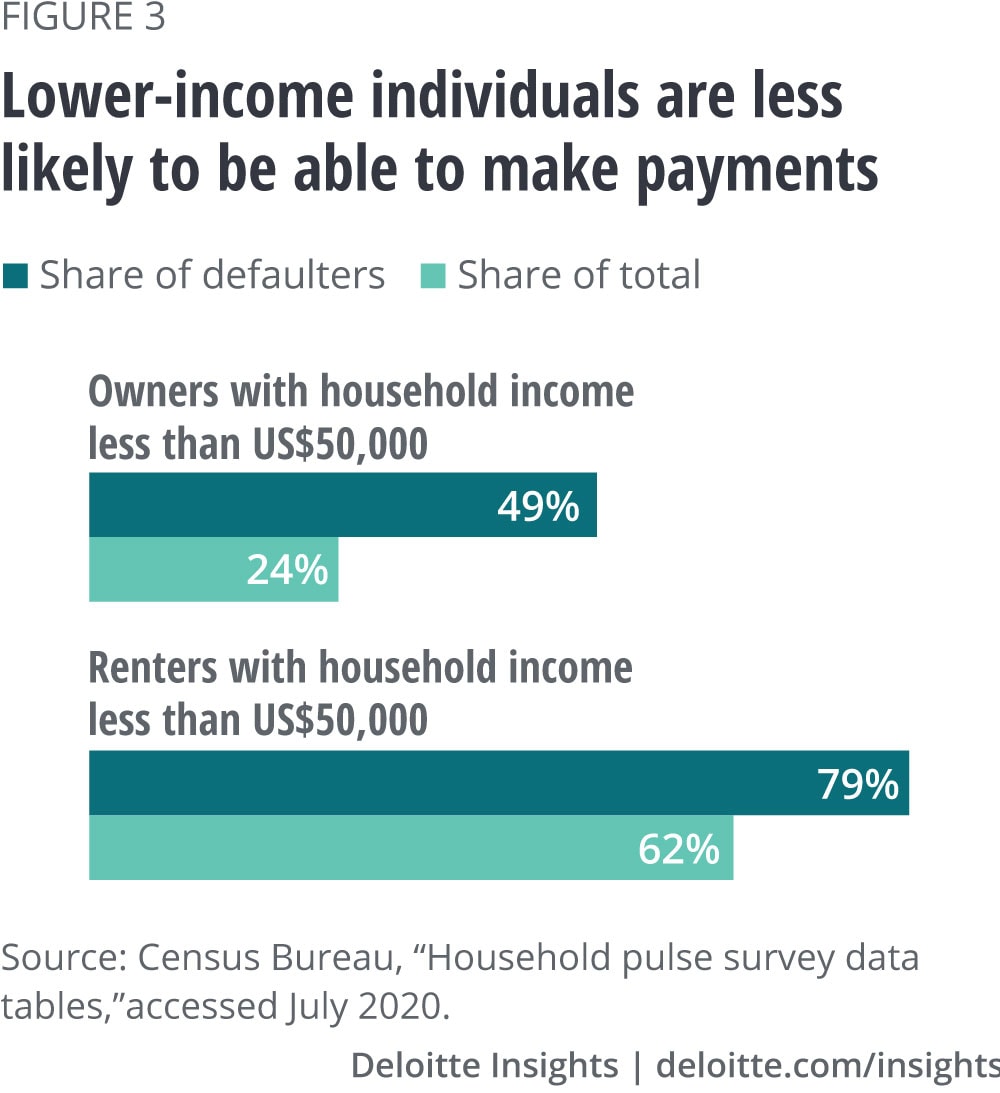

Unsurprisingly, 75% of those who didn’t pay the mortgage in the previous month and 80% of those who didn’t pay rent in the previous month belonged to households in which someone had experienced a loss of employment income. Job losers with lower incomes are less likely to have savings to fall back on and are therefore less likely to be able to make payments. Adults with annual income less than US$50,000 accounted for 25% of those with a mortgage but nearly 50% of all those who missed a mortgage payment in the previous month (figure 3). The same income group accounted for 60% of those paying rent but nearly 80% of defaulters in the previous month.

Overall housing insecurity remains very high and could get worse

Overall housing insecurity—defined by the Census Bureau as the percentage of adults who did not pay last month’s rent or mortgage, or who have little or no confidence that their household can pay next month’s rent or mortgage on time—has remained very high in the United States at 24.6% in week 8, remaining relatively unchanged from 24.8% in week 1 of the survey. According to data from the 2017 American Housing Survey (latest available annual data), 5.2% of households defaulted on either rent or mortgage payments in the last three months (in the month of the survey).11 Assuming a similar or slightly larger proportion of the population was not confident in their ability to make payments in subsequent months, we calculate a roughly comparable pre-COVID-19 housing insecurity metric of 10.4% to 15.7%.

While housing insecurity declined slightly from 15.5% in week 1 to 14.0% in week 8 for adults in owner-occupied units, insecurity for those in rented units increased from 42.9% in week 1 to 46.0% in week 8.

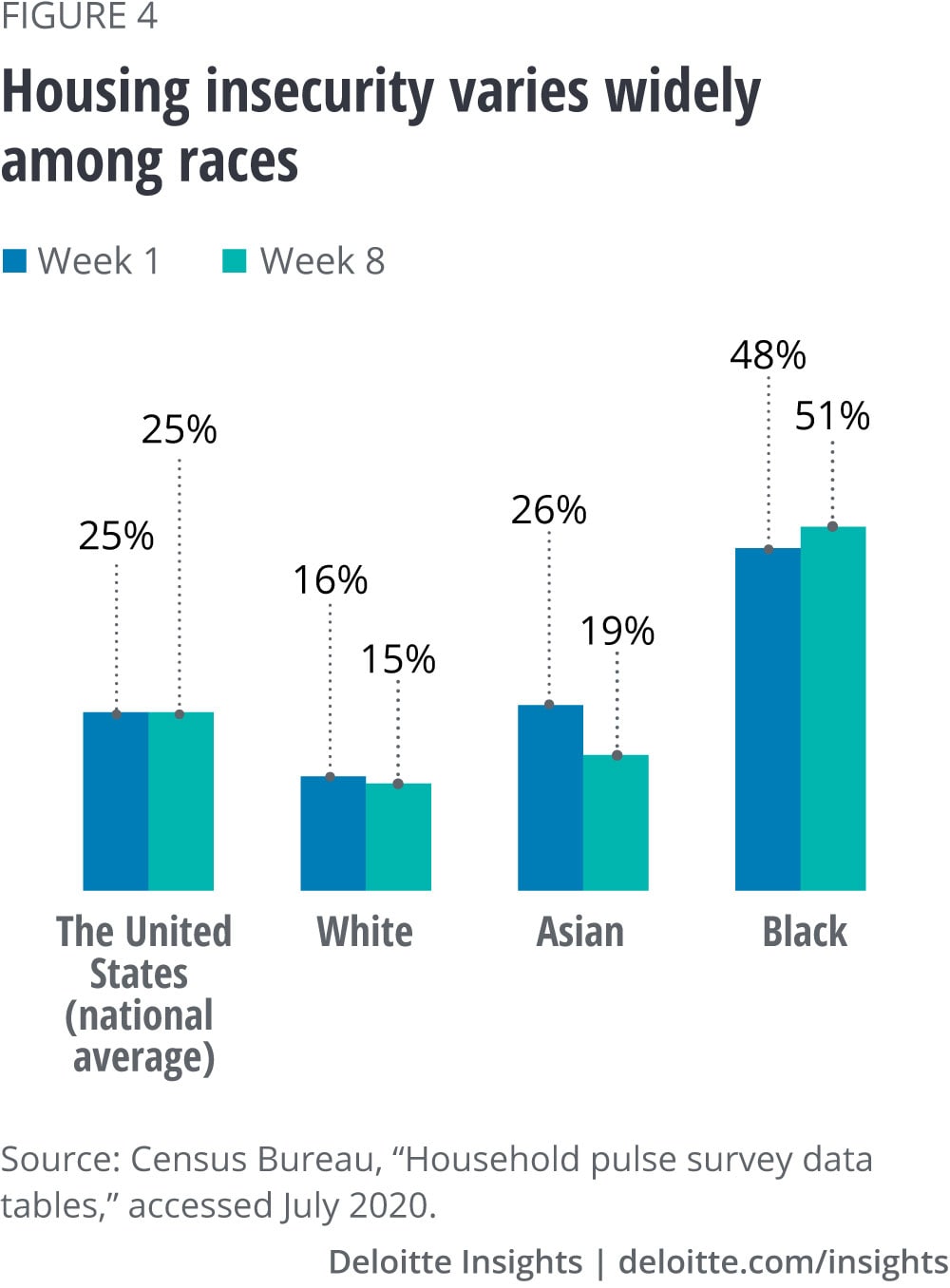

Housing insecurity varies widely among races (figure 4). Insecurity among White Americans stood at 15% in week 8. For Asian Americans, insecurity was at 19.0% in week 8, while it stood at an extremely high 51.0% for Black Americans. Black renters are particularly at risk, with an insecurity score of 71%. As eviction moratoriums expire, this demographic is likely to bear an outsized impact.12

At the national level, rising infections; persistently high unemployment; and a withdrawal of fiscal stimulus, moratoria, and forbearance could lead to further deterioration in housing insecurity. An uptick in delinquent payments is likely to have far-reaching economic implications.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- Lester Anthony Gunnion

- Senior Analyst | MK Marketing

- Deloitte SVCS India Pvt L

- lgunnion@deloitte.com

- +1 615 718 8559

© 2021. See Terms of Use for more information.

Explore our COVID-19 content

-

The heart of resilient leadership: Responding to COVID-19 Article5 years ago

The heart of resilient leadership: Responding to COVID-19 Article5 years ago -

The long and short of short-time work amid COVID-19 Article4 years ago

The long and short of short-time work amid COVID-19 Article4 years ago -

Managing the recovery phase of COVID-19 Article4 years ago

Managing the recovery phase of COVID-19 Article4 years ago -

Potential implications of COVID-19 for the insurance sector Article5 years ago

Potential implications of COVID-19 for the insurance sector Article5 years ago -

Opportunities for private equity post-COVID-19 Article4 years ago

Opportunities for private equity post-COVID-19 Article4 years ago -

US policy response to COVID-19 aims to set the stage for recovery Article4 years ago

US policy response to COVID-19 aims to set the stage for recovery Article4 years ago