Trouble on the horizon for consumer spending?

The September 2023 Economics Spotlight examines the higher costs of financing mortgages and other types of consumer debt, including credit card and auto loans. When combined with the return of student loan payments, rising debt is likely to put a dent in consumer spending.

Prices in the United States began rising rapidly as the economy emerged from the COVID-19 recession. The price rises were fueled by a combination of government income supports, which kept demand robust, and supply chain bottlenecks. For the first time since the 1980s, American households were faced with rapidly rising prices for everything from grocery staples to used cars. The Fed reacted with a relatively rapid increase in the federal funds rate, which, in turn, led to increases in a variety of rates directly impacting consumers—everything from mortgage rates to interest charged on credit card purchases and auto loans.

Now that inflation is moderating, consumers are getting some relief on current purchases. But the impact on financed purchases (i.e., those supported by consumer borrowing) remains substantial. Many consumers have been spending down the savings they accrued from pandemic-related government supports. Financed purchases have been increasing even as the interest rate on these balances has been rising—in some cases to over 20%, depending on the card or loan holder’s credit rating.1 And home prices continue to rise, while mortgage rates are at 20-year highs. That has made home ownership more expensive for those looking to buy.

In addition, the expiration of the federal student loan payment moratorium will add to the financial stress for federal student loan holders.2 Beginning October 2023, the requirement to make timely student loan payments will resume. However, loan holders who fail to make timely payments will not be reported to the credit agencies until the end of 2024, which will give student loan holders time to adjust other spending to make room in their budgets. But, unlike during the pandemic moratorium, interest will accrue each month for borrowers who don’t make their payments, raising (for those borrowers) the amount owed.

All this suggests that households will face considerable constraints on their budgets and spending ability in the next few years.

Buying a house is more challenging given high mortgage rates and rising prices

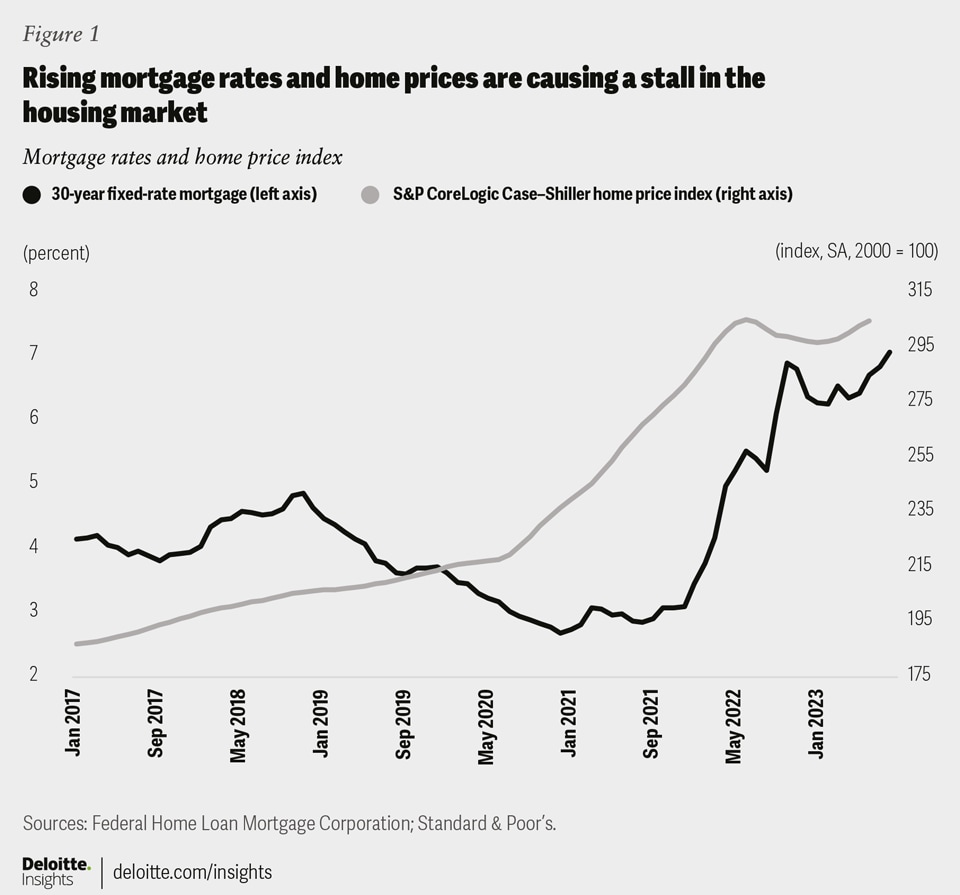

Mortgage rates have been on the rise since March 2022 and currently stand at just over 7%, a 22-year high (figure 1).3 Those looking to buy are faced with higher monthly payments because of the higher mortgage rates. Immediately preceding the pandemic, mortgage rates were around 3.5% (although the 30-year mortgage rate had been as high as 5% as recently as the end of 2018). The pandemic low was 2.7%. To understand the scale of the impact of these changes in mortgage rates, consider this: For a home price of US$400,000, the monthly payments at the prepandemic mortgage rate of 3.5% would beUS$1,796; at the pandemic low of 2.7%, the payment would be US$1,622; and at the current rate of 7.0%, it would be US$2,661. This means that even if the home price remained the same, a buyer in 2023 would pay about 50% more in monthly payments than a buyer in 2019.

But that’s not the only reason affordability has declined. Immediately after the start of the pandemic, home sales prices began rising at a rapid pace. Even with a decline in the second half of 2022, prices are currently 41% higher than they were at the beginning of 2020.

One of the factors pushing house prices up is that builders started pulling back on residential construction when mortgage rates began rising. Housing starts fell from a peak of 1.8 million units (at an annual basis) in April 2021 to less than 1.4 million units by the end of the year.4 At the same time, the available inventory of existing homes for sale started falling in 2022 and is now at a very low level. Homeowners who might have been interested in buying a larger house may have been discouraged by the prospect of significantly higher monthly payments. Those who may have been considering downsizing have been discouraged by a lack of potential buyers willing and able to carry the hefty monthly payment. On top of that, current homeowners have a strong incentive to stay put so they can keep their existing low interest rate mortgages. These factors have likely taken a lot of potential inventory off the market. Investor purchases have also played a role in pushing prices up. Despite some recent pullback in investor activity, investors still account for 16% of home sales, down from 20% in the first quarter of 2022.5

Meanwhile, rental inflation is slowing and this may be encouraging "build to rent" housing construction.6 While helpful in restraining rents, it is another factor reducing the inventory of homes for sale and propping up the cost of homeownership.

Credit cards and auto loans

The number of credit card accounts in the United States dropped slightly at the beginning of the pandemic but did not take long to start growing again. At present, US consumers are in possession of 578 million credit cards—13.0% more than there were at the beginning of 2020.7 Total dollar balances have grown by 15% compared to the prepandemic level. However, this is slightly less than total inflation over the period, so total real balances are actually slightly lower than just before the pandemic.

The number of auto loans outstanding—108 million as of the second quarter of 2023—is currently slightly lower than the number before the pandemic hit. The dollar value of these loans, however, has grown by 17.5% over the period.8 This reflects the fast increase in auto prices, particularly used auto prices, seen since the pandemic.

Interest rates charged on outstanding credit card balances tend to vary with the prime rate, which generally runs about 3 percentage points above the federal funds rate. Credit card rates are marked up over the prime rate to account for the credit rating of the individual. For example, in August 2023, the Federal Reserve reported that the average rate for all credit cards was 20.7%. However, WalletHub, a personal finance website, lists the average credit card interest rate as of August 2023 for those with excellent credit at 17.8% and those with only fair credit at 25.9%.9 In August 2023, the effective Fed funds rate was 5.3% and the prime rate was 8.5%, so the markup over the prime rate for the average credit card was over 12%, and for those with fair credit, 18%. In fact, markups for credit card debt have increased by about 2 percentage points since early 2020. This markup was rising even before the pandemic, but the recent increase is quite striking.

The relationship between the prime and auto loan interest rates is much looser because of the availability of dealer financing. According to WalletHub, car loan rates in early September ranged from 6.6% for excellent credit to almost 20% for a buyer with no credit history.10 An important difference between credit card rates and auto loan rates is that almost all auto loans are fixed rate—and therefore the monthly payment is set for the life of the loan (generally 5–6 years). Thus, payers of existing balances are not affected by subsequent rises in the Fed funds rate.

Federal student loan debt

Approximately 13% of Americans have student loan debt.11 The total amount of student loan debt outstanding was US$1.6 trillion in the second quarter of 2023.12 Student loans account for 9% of all household debt.13 Just before the start of the pandemic, about 11% of the total balance of student loans was in serious delinquency of 90 days or more. This was the highest percentage of any type of consumer credit.14 With the repayment of student loans now restarting, those who were struggling before the pandemic to make timely payments will likely be struggling once more. Analysis by New York Times showed that over half of borrowers owe more than they borrowed—in 2022, 54% of the student loans opened in 2019 owed more than they borrowed, and 57% of the loans opened in 2010 owed more than originally borrowed.15 The question is: Were those with outstanding student loans saving in anticipation of the eventual restart of the payment process? The overall low savings rate and strong consumer spending of the last year suggests that this is unlikely.

The actual state of student loan delinquencies will not be known until the end of 2024; however, we may see its impact on consumer spending earlier.16

Consumers’ debt burden and rising housing costs will constrain consumer spending

The rising cost of housing and consumer credit, combined with the restart of federal student loan payments, will likely continue to consume a growing proportion of households’ disposable income in the near future, creating additional stress on households. And indeed, we are already seeing new delinquencies of 30 days or more rising for credit card and auto loan debt.

There is no relief on the horizon in the near term as the Fed is unlikely to begin lowering interest rates anytime soon. Deloitte’s latest US Economic Forecast has the Fed holding interest rates at about the current level until the second half of 2025.17 One objective of the current Fed policy is to slow the economy, and the need to divert money from current spending to repay debt may well constrain consumer spending and help to accomplish this. In that sense, the stresses in the household sector are a result of the Fed’s understandable goals. But a potential rise in delinquencies poses risks for the financial system as well as for the households who took out the debt. This is all part of the delicate balance that the Fed is trying to strike—slow the economy to bring inflation down to its 2% target, without causing consumers to retreat so much that the economy slips into recession. Unfortunately, since monetary policy acts with a lag of uncertain duration, it will take some time before we know how successful the Fed has been.

{kind=link}