Abbreviation | Meaning |

AFIR | Alternative Fuels Infrastructure Regulation |

BVCM | Beyond value chain mitigation |

CapEx | Capital expenditures |

CRMA | Critical Raw Materials Act |

CSDDD | Corporate Sustainability Due Diligence Directive |

CSRD | Corporate Sustainability Reporting Directive |

Das | Delegated acts |

DPP | Digital product passport |

EFRAG | European Financial Reporting Advisory Group |

EPBD | Energy Performance of Buildings Directive |

ESPR | Ecodesign for Sustainable Products Regulation |

ESRS | European Sustainability Reporting Standards |

EU ETS | European Union Emissions Trading System |

GHG | Greenhouse gas |

ISSB | International Sustainability Standards Board |

NFRD | Non-Financial Reporting Directive |

PIE | Public interest entities |

PPWR | Packaging and Packaging Waste |

RED III | Renewable Energy Directive |

RRF | Recovery and Resilience Facility |

SME | Small to medium-sized enterprise |

VCM | Voluntary Carbon Market |

Sustainability regulation outlook 2024

Leveraging EU regulation to conquer sustainability reporting, drive decarbonisation and prevent greenwashing

Simon Brennan

Ramon Bravo Gonzalez

Magda Puzniak-Holford

Ruth Kilsby

Adithya Subramoni

Time is running out to act on climate change. In Europe, the transition to a lower carbon and more sustainable society is reshaping the economy, creating new opportunities, and altering the cost of doing business. For companies, the implications are stark. Failing to become more sustainable will leave them vulnerable to the loss of revenue and reputation, as well as to litigation and regulatory penalties.

Regulation is an important driver of these changes, and a critical consideration for companies as they plan how to meet the commitments they have made to transition their own businesses. 2024 will be a pivotal year for the roll out of sustainability-related regulations. Several key sustainability initiatives will be finalised and EU Parliament elections in June will determine the direction and level of ambition of the next wave of the EU’s sustainability legislative activity. Our Sustainability Regulation Outlook explores the most pressing developments in the year ahead and what these mean for business strategies and operating models.

The EU’s response to the imperative on climate begins with enhanced sustainability reporting and the EU Corporate Sustainability Reporting Directive (CSRD). For most companies, work remains to be done to meet new reporting requirements in full. What is more, sustainability reporting sits at the heart of the EU’s green strategy and the information companies need to disclose draws on data and activities across the organisation. CSRD can be exploited to generate change and efficiencies across other regulatory-driven developments.

Beyond reporting requirements, our outlook highlights four themes for companies to focus on this year.

Circularity is now a clear imperative. In 2024, companies should focus on understanding what circular design means for their products and services, with EU regulatory initiatives establishing requirements for product design, packaging and packaging waste, the ability to repair products, and provisions on end-of-life waste disposal, among other things. The focus on circular design can also create opportunity for companies. For example, in sourcing secondary materials, designing products using other companies’ waste, and providing repair services.

The EU is a frontrunner globally in shaping supply chain sustainability as part of its strategy to decarbonise the economy. CSRD obliges companies to report not only on their own operations but also their upstream and downstream supply chains. This means companies must invest more resources in relationships with their suppliers and integrate sustainability-related risk assessment into their purchasing decisions. Use of rare earth metals, contributions to deforestation and relationships with companies within countries with human rights abuses are amongst the factors companies need to assess. The deforestation-free regulation, for example, prohibits the sale, import or export of certain commodities unless it can be proven they are deforestation-free and produced in compliance with the relevant legislation of the producer country.

Decarbonisation is the ultimate goal of many of the EU initiatives. CSRD will affect most industries, obliging companies to track emissions and report their reduction targets. The carbon border adjustment mechanism is one of many other relevant EU regulatory initiatives. It makes it necessary to report emissions data on imported carbon-intensive products such as aluminium, steel and cement, which will be taxed on their carbon content from 2026. Buildings and real estate also present major challenges. From 2024 the Energy Performance of Buildings Directive will seek to ensure that buildings across the EU meet minimum energy performance standards. To reach net zero, companies should look to invest in projects or take action to avoid and reduce or remove from the atmosphere and store greenhouse gas (GHG) emissions.

Finally, to minimise their exposure to greenwashing risk, companies must ensure there is no mismatch between what they say they are doing and what they are doing. The EU Directive for Empowering Consumers for the Green Transition means that corporate communications must change to avoid greenwashing. As from 2026, generic phrases such as ‘green,’ ‘carbon neutral’, ‘biodegradable’ and ‘eco-friendly’ will no longer be permitted. Companies will have to ensure that their environmental messaging is clear and fully substantiated.

Companies need a plan of action that connects the moving parts on sustainability across regulation and business strategy, and identifies opportunities for increasing collaboration between finance, internal risk management and procurement departments. Within this plan, companies can factor in what leading practice looks like, the most effective way to manage and sequence the changes required and what further changes to requirements are expected.

Sustainability reporting enters a decisive phase

Sustainability reporting sits at the heart of the EU’s green strategy. Over the next few years, the journey towards greater transparency of companies’ sustainability credentials through disclosures will accelerate. The focus for companies in 2024 is to address corporate sustainability reporting requirements. Significant effort and resources will need to be dedicated to meet these requirements. The real opportunity for companies from reporting requirements, however – and the longer-term effectiveness of their approach – will come from looking beyond the compliance task to consider the broader ramifications of the regulations across their entire business and operating models. If positioned correctly, these projects can help drive a wider set of changes to harmonise understanding of and embed a firm’s sustainability strategy across the organisation. The European and international reporting landscape is changing.

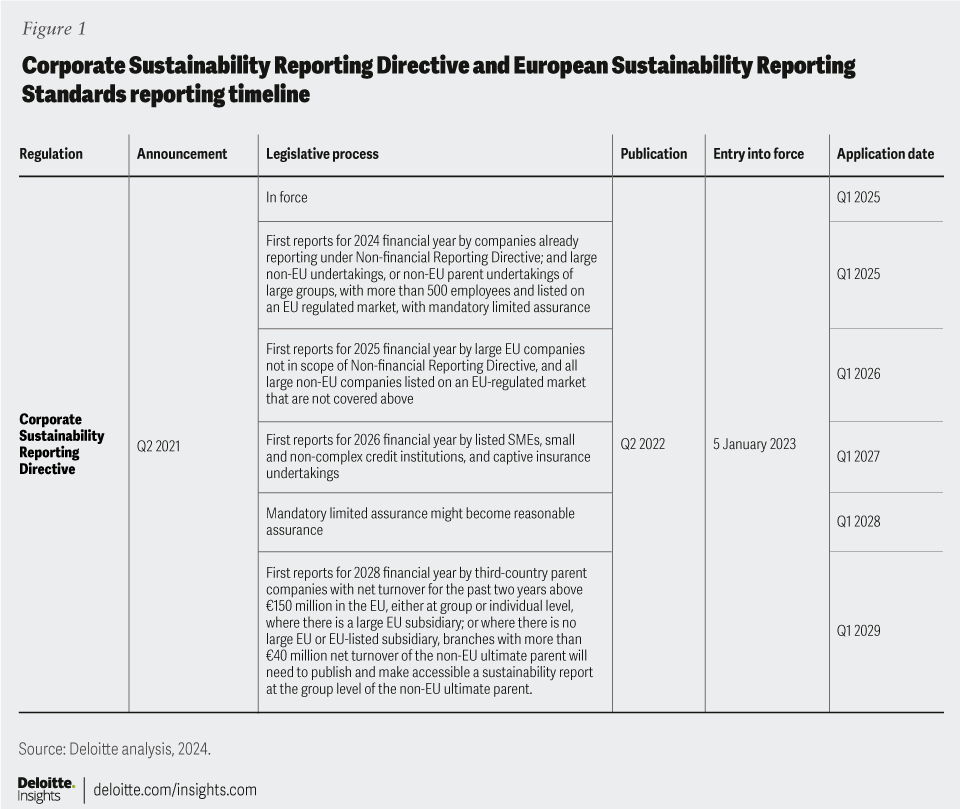

Now is the time that ambition for greater transparency needs to be put into practice. In 2024, all eyes are on the CSRD and corresponding European Sustainability Reporting Standards (ESRS). Even though the European Commission has reduced the scope of the reporting burden in the short term, around 50,000 companies are expected to publish data under CSRD – more than four times the number that reported sustainability information under the Non-Financial Reporting Directive (NFRD) that CSRD is replacing. For the largest companies the obligation, at this stage with a requirement for limited assurance, begins as early as January 2025, for the 2024 fiscal year. The Commission plans to evaluate the shift from limited assurance to reasonable assurance no later than October 2028.

CSRD has a material extraterritorial impact. Large companies headquartered outside of the EU with listed equity and debt securities on an EU-regulated market are in general also captured by the CSRD reporting rules. Further, subsidiaries outside of the EU may need to provide sustainability information to parent companies based in the EU, in addition to complying with disclosure requirements prescribed by the jurisdiction in which they are incorporated.

Enhanced CSDDD due diligence rules will also come into play

The Corporate Sustainability Due Diligence Directive (CSDDD) is a major piece of EU legislation that will require large EU companies (those with a net global turnover of over €150m and more than 500 employees) and large non-EU companies (those with an EU-wide revenue of over €300m) to conduct environmental and human rights due diligence across their operations, subsidiaries and value chains already from 2027. The scope of the CSDDD will extend to more companies in the years to follow. We expect the compliance burden the CSDDD presents to be significant, especially for companies with extensive, international value chains. Consequently, the 2027 implementation date is challenging. The requirements of the CSDDD are expected to dovetail with CSRD and will also be the first piece of EU legislation that mandates companies to adopt a climate transition plan. Companies should consider whether they are looking at sustainability reporting holistically and understand the links between the CSRD and other regulatory requirements, such as the CSDDD, or the EU Taxonomy Regulation (EU Taxonomy).

Interoperability of European and international standards is in focus for policymakers

Looking beyond the EU, international standards are also evolving. The International Sustainability Standards Board (ISSB) is expected to build on the two standards it published in 2023, with work underway on several topics: biodiversity, ecosystems, and ecosystem services; human capital; human rights; and connectivity in reporting.

The ISSB has collaborated closely with the European Financial Reporting Advisory Group (EFRAG) – the body responsible for creating the ESRS – to ensure that the ISSB standards and ESRS are consistent as far as possible, and to avoid duplication in reporting against both sets of standards. In 2024, EFRAG and the ISSB are expected to publish a table showing how the standards align and where incremental disclosures may be needed to meet both sets of standards. Several countries, including the UK, have committed to adopting the ISSB standards.

Reporting on emerging topics

We expect clarity in 2024 on whether or how the finalised framework from the Taskforce on Nature-related Financial Disclosures will be implemented in EU and international reporting frameworks. We expect it to be incorporated into the ISSB. As a result, companies may choose to focus on broader environmental issues beyond their initial climate change disclosures and consider their capability to report on other emerging topics such as biodiversity or circularity, among others.

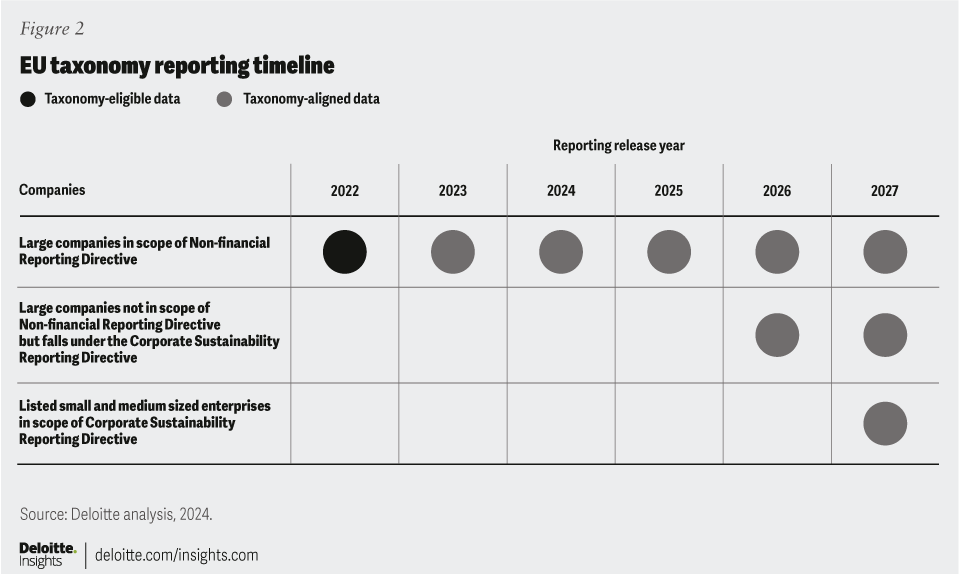

Taxonomy reporting gains traction

The EU Taxonomy is a classification system that includes a reporting mechanism and criteria for economic activities that can be considered as environmentally sustainable. Article 8 of the EU Taxonomy requires companies in scope of CSRD to disclose information on how and to what extent their activities are associated with environmentally sustainable economic activities, considering metrics such as capital expenditures (CapEx), operating expenses and turnover. This information will also be subject to independent assurance as required by CSRD.

In 2024 companies affected by EU Taxonomy reporting rules should turn their attention towards improving their data frameworks and data quality with the aim of increasing over time their EU Taxonomy alignment. Further, they should consider how to use the EU Taxonomy as a tool to design their transition plans. The quality of a company’s transition plan could also have a direct impact on lenders and bond investors’ assessments of the riskiness of a company from a transition planning perspective. Beyond 2024, the EU Taxonomy sector coverage and list of sustainable activities will be expanded, bringing more companies into scope.

The EU Taxonomy currently covers 13 sectors. Significant industries are missing, among them agriculture. The sectors currently in scope include: Forestry; Environmental protection and restoration; Manufacturing; Energy; Water supply, sewerage, waste management and remediation; Transport; Construction and real estate; Information and communication; Professional, scientific, and technical activities; Financial and insurance activities; Education; Human health and social work activities; Arts, entertainment and recreation. However, companies in sectors not captured by the Taxonomy still have an obligation to report on their capital expenditure if they have investments in activities included in the Taxonomy.

Looking beyond the EU, new taxonomies are proliferating globally, with varying objectives and priorities, aligned with the characteristics of national economies. However, the EU Taxonomy, as the most expansive and advanced framework, is often seen as a source of inspiration for others. The UK, for example, is expected to align with the EU Taxonomy, albeit with some revisions to reflect local economy specificities. Companies operating globally should monitor the developments at national level and the effect they may have on their business operations. The International Platform on Sustainable Finance – a dedicated working group comprising public authorities across the globe – is expected to promote best practices and compare different taxonomies to identify opportunities for the mobilisation of private capital towards environmentally sustainable investments and any obstacles.

What companies should do now

Sustainability reporting is more than a compliance exercise.

To respond fully to CSRD and the ESRS, companies need to consider how implementing the reporting requirements extends beyond the immediate compliance exercise and will drive broader changes to strategy, governance, operations, and data. In particular:

- Embrace a strategic approach: There is no “one-size-fits-all” approach. A business strategy that is both effective and cohesive should rely on the development of a suitable data framework that supports sustainable transformation of the business. In addition, a disclosure strategy embedding an understanding of the overall disclosure landscape will help firms to plan. Finance is likely to lead these projects but other parts of the business, such as procurement, accounting, legal, compliance, communication and human resources, should be involved.

- Evaluate the governance structure: Companies need to ensure they run an adequately resourced programme with appropriate governance in place, addressing key dependencies between different functions and projects. This extends to considering the relationship with boards of their subsidiaries that may need to sign off consolidated sustainability reports, depending on the reporting strategy taken at a group level. Given the broad impact of sustainability reporting requirements across all sectors, the skills required are likely to be in short supply.

- Get ready for assurance and manage mis-reporting risks: If they have not done so, companies should set up due diligence processes to identify and mitigate reporting risks in their supply chains. A closer look into engagement processes with their suppliers to ensure the transfer of information for reporting purposes is crucial. Companies should also allow sufficient time to build their internal capacity and test their assurance models. Investments made to upskill the organisation and embed relevant KPIs in the management and control cycle will pay off.

Making circularity and circular design the norm

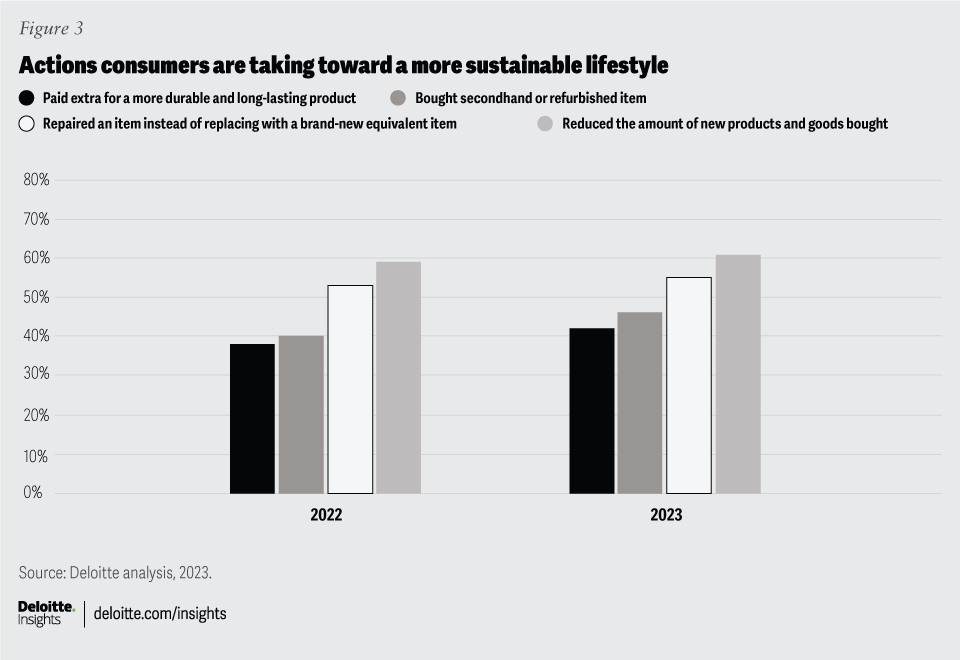

Circularity is evolving rapidly, driven both by consumer demand and new regulatory requirements. As recent research from Deloitte UK discusses, consumers are increasingly focusing on the circularity of products and services and are changing their behaviour in many areas.1 Some examples of these behavioural changes are set out below (Figure 3).

Most legislative actions proposed under the EU’s Circular Economy Action Plan have now been published by the Commission. They have either entered into force or are under consideration by the European Parliament and/or the European Council. Companies are in a position where they must determine how the regulations affect them and how best to prepare. For 2024 companies should focus on understanding what circular design means for their products and services and how best to incorporate new processes into their data and governance systems.

Linking regulatory priorities to business concerns

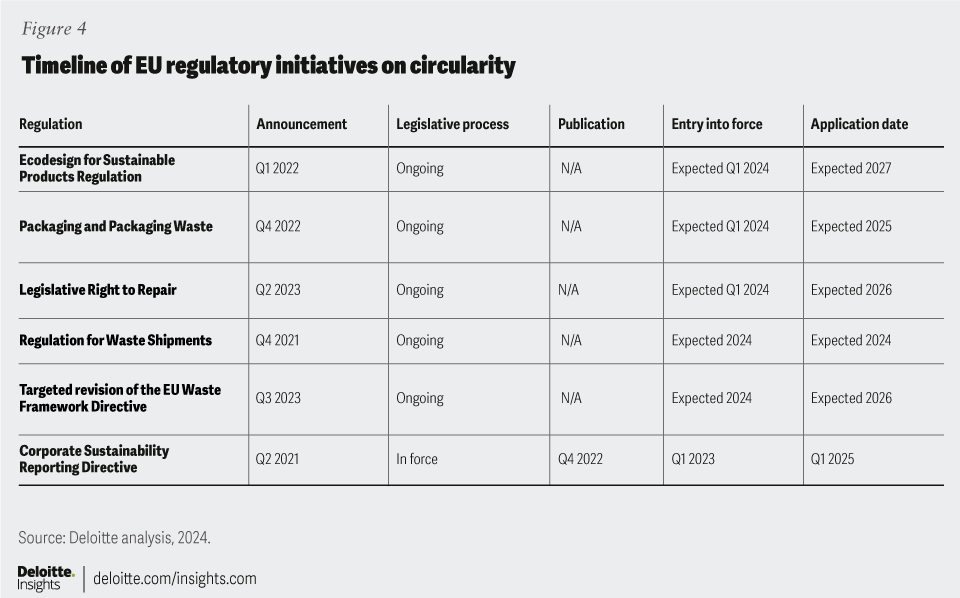

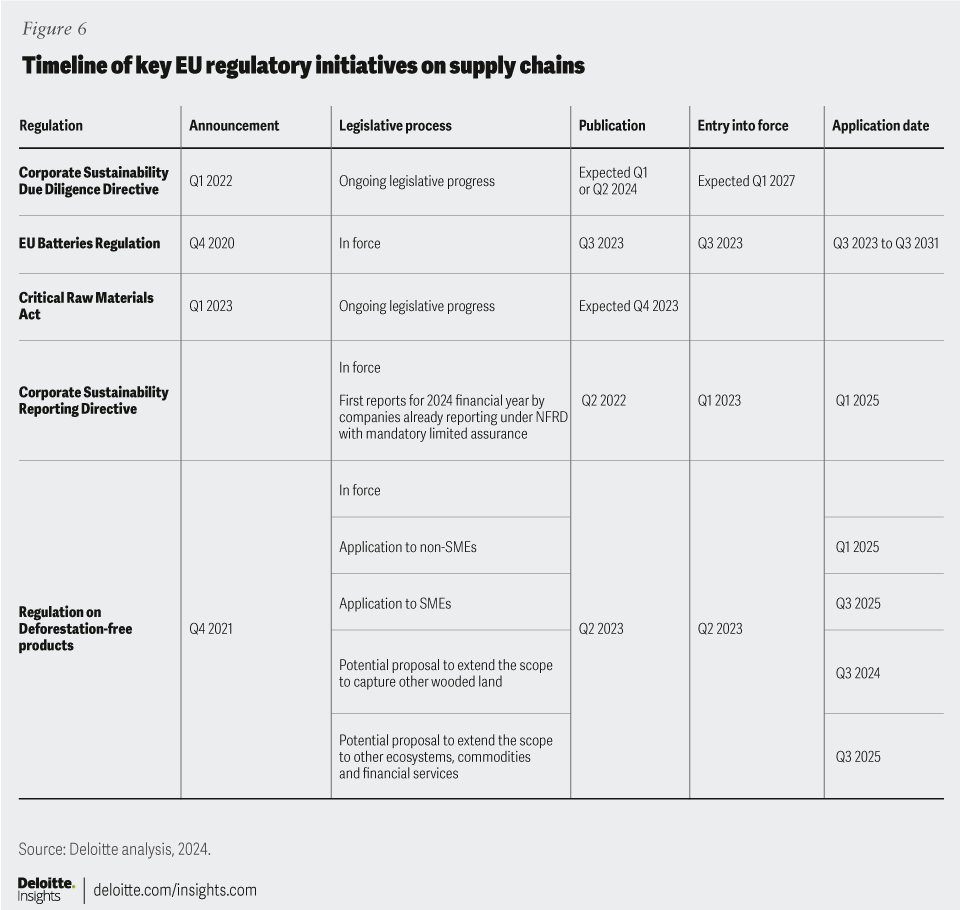

The flagship regulations within the Circular Economy Action Plan are expected to enter into force ahead of the end of the current European Parliament this year. These include the Ecodesign for Sustainable Products Regulation (ESPR), Right to Repair, and Packaging and Packaging Waste (PPWR). The following table shows the expected timeline for the setting of targets and application requirements, alongside the timeline for CSRD.

What is the link between circularity and CSRD?

Companies in scope of CSRD will have to report sustainability information using the ESRS developed by the European Financial Reporting Advisory Group (EFRAG). ESRS 5 requires companies to report on resources use and circular economy action plans. EFRAG has also provided some detailed circularity metrics that could be used by companies. Further, sector-specific standards will be adopted by the EU in 2026. Companies should focus now on creating robust data frameworks that can be leveraged in future for detailed reporting as needed by sector-specific standards.

Designing for circularity

ESPR will encompass a range of new product categories, including 12 end-use products such as textiles, cosmetic products and detergents, and seven intermediary products such as iron, steel and plastics, among others.2 The impact of ESPR on companies’ core operations is therefore expected to be significant. Beyond specific traceability elements, the requirements will directly affect products at all stages in the value chain, including recyclability, the use of recycled contents, and durability. Also, the legislative Right to Repair measure makes producers responsible for ensuring cost-efficient repair services are available to consumers post-sale, to extend the product’s life.3

Together the regulations create new opportunities for companies throughout the product life cycle, such as sourcing (and eventually scaling) secondary material or components for production, designing products based on other companies’ waste streams, and providing repair services. There will also be challenges. For instance, creating a market for secondary materials may be difficult for some products due to a lack of specialised recycling or of the ability to extract and reuse materials at identical material compositions.

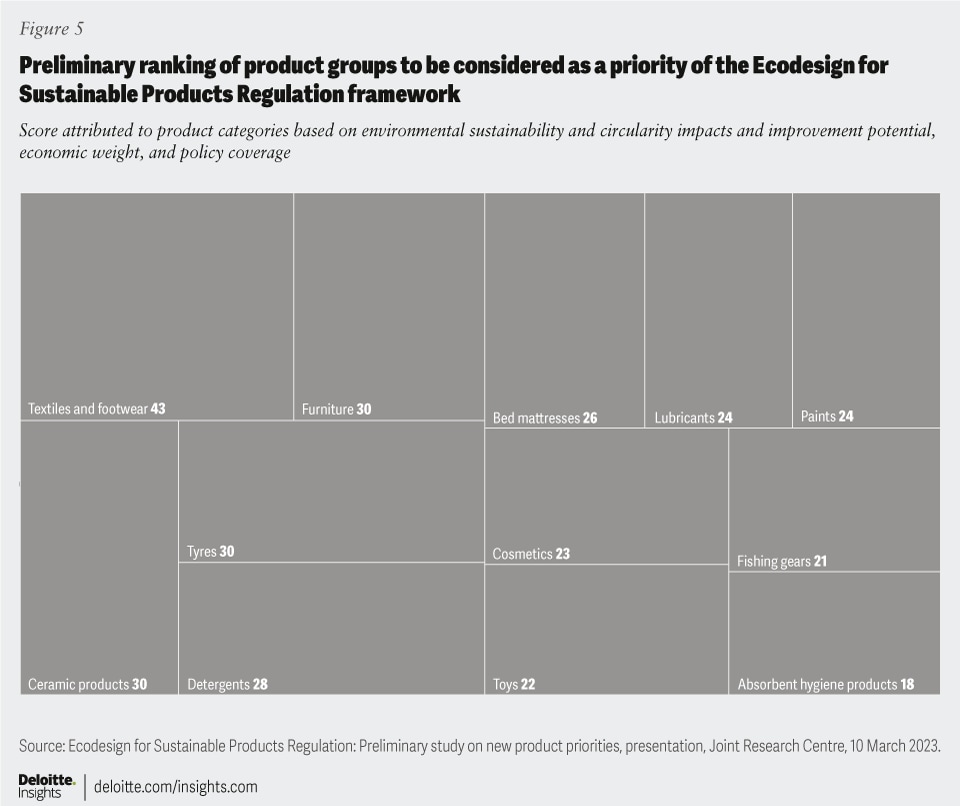

In early 2024 the Commission is expected to announce its priority product groups for product-specific Delegated Acts (DAs) under ESPR. The Commission will refer to the preliminary ranking provided by the Joint Research Centre for this product prioritisation. The ranking is reproduced below.4 Companies will need to stay abreast of these developments to identify how their operations may be affected and focus on data foundation and data governance policies that need to be in place.

Cross-sector partnerships

The new circularity requirements will oblige companies to make a systemic shift, away from virgin materials to reliable, quality secondary materials for products and packaging. To comply with the new requirements, companies could benefit from assessing whether cross-sector or cross-value chain partnerships may ease the burden. Such partnerships may include organisations from more than one sector, harnessing the competencies of different organisations and sectors to help solve complex challenges. Companies could, for example, assess whether such partnerships would be viable to set up joint hubs where products of multiple Original Equipment Manufacturers can be refurbished at reduced cost. Which segments of the value chain will benefit best from such partnerships needs to be assessed.

Branding, positioning and marketing

PPWR requirements include targets for the use of specific quantities of recycled content in different types of packaging products. These targets will rise progressively over time. Companies will want to assess the quality and durability of new packaging and market responses to it before scaling up production. This will be critical for products where packaging is a differentiator that drives revenue.

Similarly, companies will need to ensure any green claims made for a new product can be verified so that their marketing is in line with the requirements of the Green Claims Directive and, more generally, avoids greenwashing. The Empowering Consumers on the Green Transition Directive bans generic phases such as ‘green’ and ‘eco-friendly’ on packaging and in social media and advertisements.

The PPWR also aims to reduce the amount of packaging, promote reuse and refilling, and prevent packaging waste. The regulation sets reuse targets, introduces mandatory deposit return systems for plastic bottles and aluminium cans, and restricts over-packaging and use of unnecessary wrappings.5 Companies will need to consider how they can create business and operating models that can incorporate packaging reuse requirements and identify potential cost constraints in this transformation. Similarly, for industries such as e-commerce, companies will need to assess how to reduce packaging waste and design compact packaging for shipping.

End-of-life waste management

The EU Waste Shipments Regulation and targeted amendments to the EU Waste Framework Directive harmonise Extended Producer Responsibility for textiles across all EU Member States. These are expected to enter into force in 2024 and will set new rules for the export of non-hazardous waste outside the EU and treatment of textile waste inside it. As circular economy requirements oblige the use of recycled content, linking waste recycling units with production units will be essential. These regulatory developments will therefore be especially relevant to textile companies with production clusters in third countries.

Reviewing international plastic targets

Many plastic producers, packaging producers, brands and retailers have set ambitious targets for 2025 to tackle the plastic in their packaging through the United Nations’ New Plastics Economy Global Commitment.6 Targets include: ensuring that 100% of plastic packaging is reusable, recyclable or compostable; decreasing the use of virgin plastic in packaging based on determined percentages; and increasing the share of post-consumer recycled content across all plastic packaging used.7

As companies finalise the details of targets for their 2025 Global Commitment, they should keep abreast of developments on the EU Waste Shipments Regulation. The proposed regulation includes a ban on EU exports of plastic waste to non-OECD countries and phases out such exports to OECD countries within four years of its entry into force. When implementing strategies to meet their global commitment, companies will need to ensure that their operational strategies are aligned with EU regulations.

What companies should do now

With myriad sustainability regulation requirements becoming applicable in the near term, companies need to focus on the following for 2024:

- Identifying the design challenges: ESPR and the PPWR target companies’ core products and services. Companies need to assess their readiness to transform to a circular business model.

- Assess the impact of circular transformation on their business models: For instance, the impact of new packaging rules on the product portfolio, logistics and operations; or that of operational fees arising from packaging-related Extended Producer Responsibility and Deposit Return Systems.

- Review data foundation and governance policies: Assess data and data governance processes to identify how best to incorporate additional procedures. Investments in technology to address traceability- and transparency‑related requirements, such as the Digital product passport (DPP), may be needed. Once data gaps are identified, conduct an alignment exercise to determine ambition of transformation against reporting and regulatory requirements.

- Improve baseline reporting for circularity data: Business and sustainability KPIs need to be reconsidered to ensure that circularity is embedded. This will also help companies report on the Resource Use and Circular Economy standard under the European Sustainability Reporting Standards (ESRS E5).

- Prepare a road map for a circular transformation strategy: To go beyond regulatory compliance and complement their business strategy, companies can use metrics on the use of recycled material in production, assess the need to scale sourcing of recycled material, and ensure the availability of reliable suppliers for recycled materials.

Digital product passport

The DPP is a proposed tool for sourcing and sharing product-level data across a product’s life cycle, including raw material sourcing, emissions footprint, and supplier information. While the compliance timeline will vary by product group, it is expected that for all non-medical consumer products placed on the European market, companies will require DPPs in the near-to-medium term in order to do business in the EU.

Making supply chains sustainable and resilient

Supply chain disruptions, evident in particular during the COVID-19 pandemic and recent geopolitical upheavals, coupled with high inflation and interest rate volatility, are obliging companies to revise their approach to their supply chains. In 2024 companies also need to consider several EU sustainability policies and regulatory initiatives that in future will be crucial to selling products or services in the EU market. An integrated view of relevant regulatory developments can also unlock commercial opportunities that might be missed if companies only have compliance in mind.

What is the difference between a value chain and a supply chain?

Value chain encompasses the full range of activities, resources and relationships a company relies on to create its products or services, from conception to delivery, consumption and end-of-life. The value chain includes upstream and downstream actors. Downstream actors are distributors or consumers, among others, who receive products or services.

The supply chain comprises upstream actors only – providing components or services that are used by a company in the development of its own products or services.

This definition of the value chain is based on the one included in the ESRS, which is aligned with the ISSB and Global Reporting Initiative frameworks.

Sustainability regulation is shaping the future of supply and value chains

The EU is a frontrunner globally in shaping supply chain and value chain sustainability as part of its strategy to decarbonise the EU economy. The table below provides an overview of the portfolio of regulations relating to companies’ supply and value chains. Companies need to identify how these regulations apply to their business and subsequently tackle them in an integrated way.

Realising synergies between corporate reporting and supply chain data

In 2024 companies need to collect data across their operations, including their supply chains, to comply with the reporting requirements under the Corporate Sustainability Reporting Directive (CSRD).

The link between CSRD and supply chains

CSRD creates a requirement for companies to report on the sustainability of their activities. As part of this, companies are required to report information on their own operations as well as their upstream and downstream value chain, including supply chains. In order to be able to satisfy these reporting requirements, companies will need to take a more comprehensive approach to managing their supply chain than is typically the case currently. Companies will need to dedicate significant resources to managing relationships with their suppliers, especially those exposed to economic, environmental and/or social risks, and integrate risk assessments into their purchasing decisions. In 2024, EFRAG will publish final guidance on how to navigate value chain reporting and this will have an important bearing on supply chains.

Meanwhile EFRAG continues its work on voluntary reporting requirements for unlisted SMEs (ESRS) and mandatory reporting requirements for listed SMEs, small banks and captive insurers (ESRS) which will provide a cap on the information that can be required from SMEs by their larger counterparts, subject to CSRD reporting requirements.

Data points linked to suppliers’ carbon and environmental emissions could help companies respond to provisions in the ESPR, and the DPP within it. The DPP will require companies to provide detailed product-level data across a product’s life cycle, including raw material provenance, the carbon and environmental footprint and supplier information. The new rules may become applicable as early as 2025 for certain priority product groups that will be determined by the Commission in 2024. Similar provisions are also present in the EU Batteries Regulation, which is already in the implementation phase. Manufacturers of batteries or their components need to improve the traceability of the materials used in their products and ensure actors along the value chain can access ecodesign information relevant to them.

Critical raw materials and the green energy transition

The EU’s green energy transition is highly exposed to the risk of disruptions in the supply of selected materials and components.8 The upcoming Critical Raw Materials Act (CRMA) aims to increase the resilience of EU supply chains for these materials. It includes mandatory targets for companies sourcing strategic raw materials, according to a list produced periodically by the Commission that considers the extraction and mining, processing and refining, recycling and import dependence of these raw materials. The provisions of the CRMA are particularly relevant for companies operating in strategic sectors such as renewable energy, electromobility, energy-intensive industry, digital, and aerospace/defence, as they may benefit from shortened permit-granting procedures, relaxation of administrative burdens and easier access to financing.

The EU’s Joint Research Centre has published a study that underpins the CRMA and provides recommendations for companies on how to increase their supply chain resilience.

“Meeting the EU’s ambitious policy targets will drive an unprecedented increase in materials demand in the run up to 2030 and 2050. For example, in order to meet the REPowerEU targets for 2030, for the permanent magnet needs of wind turbines alone, EU demand for rare earth metals will increase almost fivefold. Lithium demand for the batteries in electric vehicles will also increase 11 times. Looking to the 2050 horizon, in the high demand scenario, EU demand in all the explored sectors for raw materials such as neodymium, dysprosium (the two main rare earths), nickel, lithium and graphite is projected to increase 6, 7, 16, 21 and 26 times compared with the current values, respectively.” - European Commission9

Increased focus on due-diligence policies and processes

The Deforestation-free Regulation does not include targets but rather goes one step further and prohibits the sale, import or export of certain commodities unless it can be proven they are deforestation-free and produced in compliance with the relevant legislation of the producer country. There may be instances in which producer countries are found to have poor governance or a lack of respect for human rights. In such cases inadequate human rights frameworks or breaches of human rights must be considered in the risk assessment phase of the due diligence and could contribute to a risk of non-compliance, effectively prohibiting companies from placing the goods concerned on the EU market.

The regulation will have a wide reach, particularly in the consumer industry, affecting companies that sell into or export from the EU market products made or fed with certain commodities, such as cattle, soya, rubber, wood, coffee, palm oil or cocoa. In 2024 the EC may extend the scope of the regulation by adding more commodities to the list. Further down the line CSDDD will introduce rules requiring EU and non-EU companies to conduct environmental and human rights due diligence across their operations, subsidiaries and value chains. Companies will have to take measures to prevent or mitigate any potential impacts they identify, as well as end or minimise any real impacts. If companies fail to comply and damage occurs as a result they may be held liable and face financial penalties.

Enforcement actions

According to CSDDD, civil society as well as trade unions and ombudsmen can initiate civil proceedings on behalf of a victim, which means that companies may be found liable for damage caused by their activities. Even though many legislative acts that make up the EU Green Deal, including CSDDD, have yet to take effect, companies are already having to contend with litigation risks stemming from comparable pieces of legislation in France or Germany. The German Supply Chain Due Diligence Act, applicable from 1 January 2023, has already resulted in a number of cases filed against major global brands. If litigation materialises it may not only affect companies’ ability to raise capital, but also their reputation and brand.10

What companies should do now

Take stock of their supply chain

Prohibitions, limitations or targets embedded in the regulations discussed above will require all companies in scope to evaluate their supply chains and will oblige some to find new suppliers because their existing ones do not meet regulatory requirements. For example, a supplier might be in a country with human rights abuses or poor governance; or it might itself choose not to produce or sell in the EU because of increased compliance costs. An understanding of the supply chain through this lens will enable companies to plan.

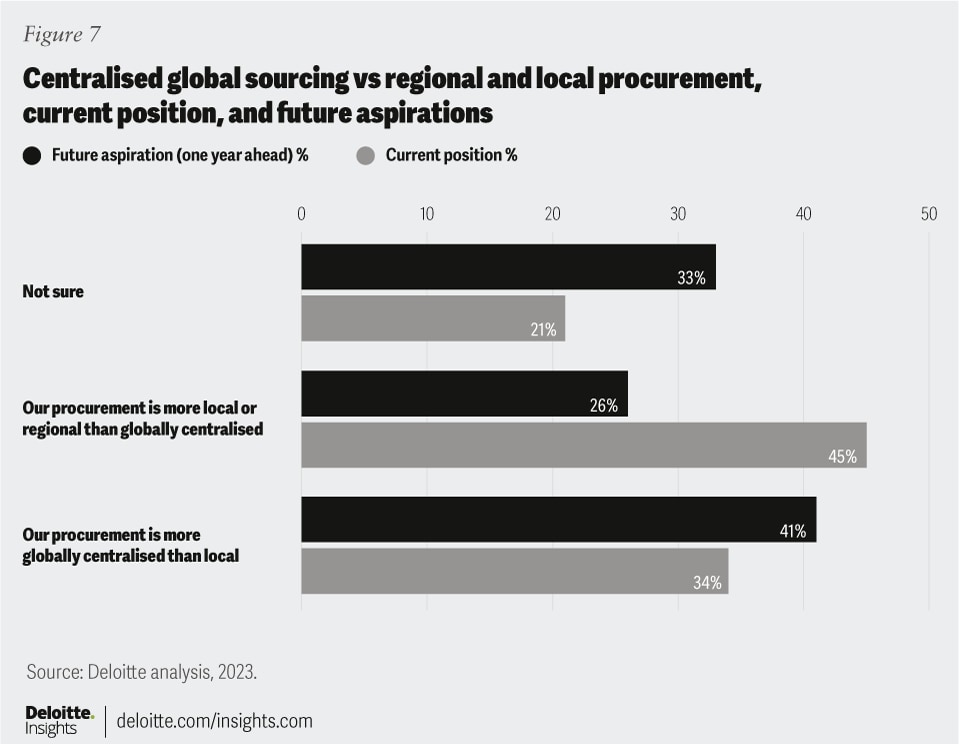

Some companies may take a strategic decision to rely more on regional and less on global supply chains, but the opposite choice might also be taken. A recent Deloitte study found that global procurement is likely to return to favour in many companies in the next one to three years.11 The results suggest that companies aim to benefit from the competitive price points and efficiencies a global supply chain can bring.

Notwithstanding their strategic choices, companies will need to ensure compliance with the upcoming regulations. Changing corporate operations may be time consuming and costly and companies should consider taking anticipatory steps before the deadlines prescribed by regulators. This could help to lock in better prices or secure business relationships with less vulnerable suppliers, reducing the risk of supply chain disruption.

Develop a joined-up view of relevant regulatory developments and take advantage of synergies

A thorough understanding of regulations at the EU and national level, as well as potential divergences between countries, should underpin companies’ strategies. Across industries we see an insufficient level of transparency between different actors in the supply chain. Systems and processes to improve communication, and solutions to gather, process and analyse data will pay off as they have the potential to identify weak points in supply chains. Internally data needs to reach those who make key decisions daily, such as procurement or supply chain officers.

Companies should therefore look into increasing collaboration and creating links between finance, internal risk management and procurement departments to ensure the adequate flow of information within the firm and along the supply chain. These investments can lead to positive outcomes for a company’s reputation and translate into positive stakeholder and shareholder impact. According to MIT’s State of Supply Chain Sustainability 2022 report, 76% of surveyed business leaders across the globe have reported moderate to very high pressures from investors to advance on supply chain sustainability.12

Create a strategic supply chain engagement plan

As an immediate next step, companies could take a closer look at their engagement with current suppliers to identify and mitigate (reporting) risks in their supply chains. Establishing targeted partnerships with actors along their supply chains and the introduction of incentives to reward desired outcomes may encourage behavioural change more broadly.

Decarbonisation gaps and focus areas

Many companies have set decarbonisation targets and are now implementing transition plans. They will have to make a sustained effort over a number of years to meet their targets. In the EU, regulatory developments, changes to operating models and market expectations within the field of decarbonisation are driving rapid change, creating both opportunities and challenges. In 2024 the key priority for companies is to ensure that they identify their Scope 1, 2 and 3 emissions, and have set emissions targets and a comprehensive strategy, especially for the short term.

The decarbonisation landscape in 2024

In the past year the EU has taken action in key areas within decarbonisation, including reporting under CSRD, carbon taxes, sustainable fuels, renewable energy, electricity markets, buildings and green infrastructure, and carbon removals. Figure 8 provides an overview of the timelines for the related regulatory initiatives.

Focus for decarbonisation in 2024 is CSRD

From all of the regulations driving decarbonisation in the EU, CSRD is likely to have the most significant impact in 2024 across industry sectors (except government and public services). Among the activities to address under CSRD are emissions tracking and reporting on emission-reduction targets, if these have been set. Companies need to ensure that they are actively reducing their carbon emissions across their entire value chain to meet their shorter-term targets (2025 and 2030). They will also need to be confident that their medium-term (2040) and long-term (2050) plans meet the expected carbon reduction trajectory, aiming to keep within the 1.5 °C global temperature rise target.

Implications of CSRD for decarbonisation

CSRD creates a requirement for companies to report on the sustainability of their activities. Some of the key implications of decarbonisation are:

- Companies need a track record of emission reductions. They should ensure they are actively reducing their carbon emissions across the entire value chain and in line with their disclosed plans. Given increased transparency, those that do not show tangible progress are likely to be closely scrutinised by key stakeholders, including customers, investors and financial institutions.

- Identify what needs to be reported and conduct scenario analysis. Under the principle of double materiality (impact and financial materiality) companies should assess which impacts need to be reported, as well as risks and opportunities. As part of this process it is essential to understand the impact that current and upcoming decarbonisation regulations may have on the company.

- Track and report Scope 1, 2 and 3 emissions. Starting for financial years beginning in 2024 (with the first reports due in 2025), companies already reporting under NFRD need to collect high-quality emissions data across their entire value chain. (Reports on Scope 3 emissions are not required in the first year for companies with fewer than 750 employees).

Priority areas for carbon emission reductions

Raw materials and renewable fuels: the EU has adopted regulation in key harmonisation areas, including taxes and renewable fuels, to tackle industrial emissions. For example, under the carbon border adjustment mechanism, the EU started to gather emissions data on imported carbon-intensive products such as aluminium, steel and cement in order to tax them, starting from 2026, on their carbon content. The EU Emissions Trading System (ETS) was also expanded to cover maritime transport from 2025 (for emissions reported in 2024) by reducing free allowances for the sector from 2026, with a total phase out in 2034. On sustainable transport fuel the EU has adopted the ReFuelEU aviation and FuelEU maritime regulations. These two regulations create obligations for aircraft and shipping vessels to use a minimum of two percent of sustainable fuels from 2025, increasing to 70% and 80% respectively in 2050.

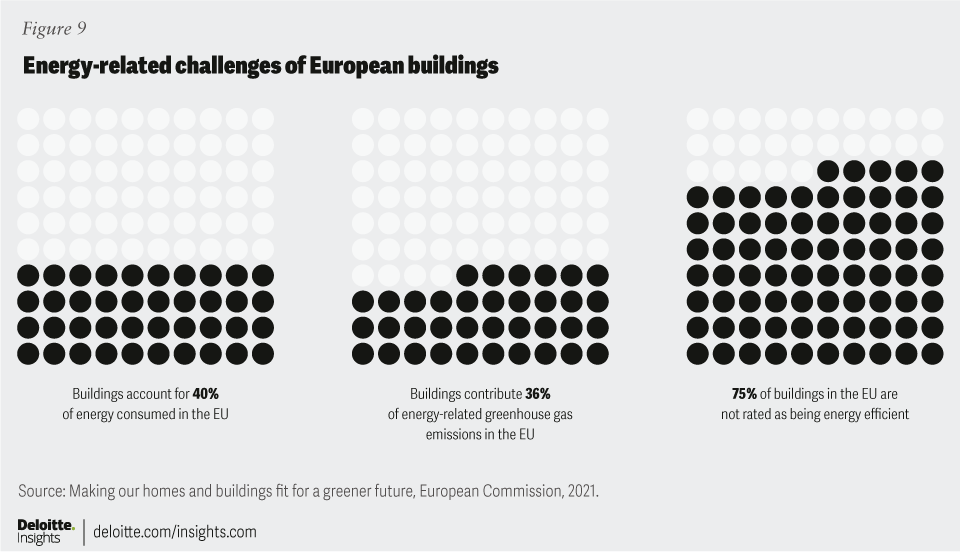

New energy efficiency standards for buildings: In 2024 the Energy Performance of Buildings Directive (EPBD) will enter into force. The EPBD seeks to ensure that buildings across the EU meet minimum energy performance standards, with the aim of having a fully decarbonised building stock by 2050. This is an important development as emissions from buildings represent over 36 percent of total energy-related emissions in the EU.13 A further challenge for companies is that standards for public charging still need to be developed. The Alternative Fuels Infrastructure Regulation (AFIR) calls for the rapid development of European standardised procedures for recharging and refuelling infrastructure to support planning, tendering, and building.

The big challenge in real estate

Decarbonising the real estate sector is essential for the EU to achieve its carbon reduction ambitions. The implications of the EPBD for building owners will be significant since the scope of the directive includes commercial, public and residential buildings. Due50 bn to the EPBD’s reliance on national measures, building owners operating across the EU will need to navigate local regulations to ensure that any new or existing buildings comply with the required energy standards. For non-compliant buildings companies will need to conduct an assessment of the upgrades needed. A further consideration is the interaction with regulations such as the new Renewable Energy Directive (RED III) or AFIR which will require the deployment of solar energy capabilities, pre-cabling and charging points for EVs.

The real estate sector will need to rethink and adjust its investment strategy and processes to increase value by taking into account not only new regulatory requirements but also market expectations and the resulting new capital expenditure needs. Achieving significant emissions reductions from buildings will be essential not only to support the sector’s own decarbonisation goals, but also to respond to the expected launch of the European Union Emissions Trading System (EU ETS) for buildings in 2027.

By starting to act now, capital expenditures could be allocated over a longer period, reducing the financial impact. This could also reduce potential risks, such as abandoned assets, or the loss of value if required standards are not met. Three key questions companies need to ask themselves are: do they fully understand the requirements imposed by the EPBD at the national level and the capital needed to retrofit buildings and deploy the required technologies? Are building materials with a lower carbon footprint being sourced for new buildings and retrofits? What is the current energy mix used for the building and can it be switched to renewables?

A push towards electrification, driven by renewable energy and green infrastructure

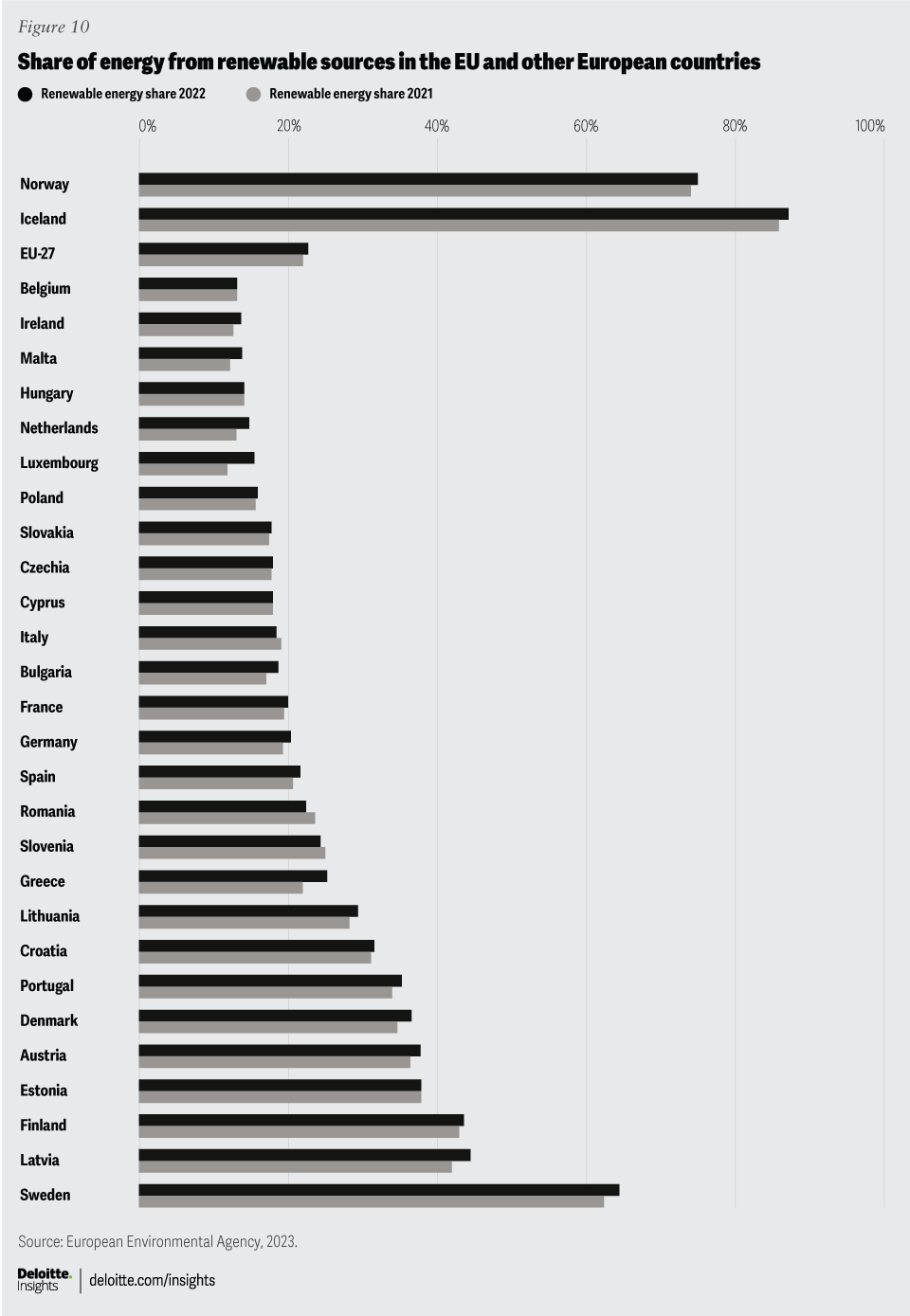

One of the major initiatives recently adopted by the EU was RED III, which seeks to raise the share of renewable energy consumption 42.5% by 2030. The EU is currently well below this target (Figure 10).

Under RED III, EU Member States need to contribute to the 42.5% goal by setting sector-specific targets:

- For transport, Member States can select between a 14.5% reduction in GHG intensity or at least 29% of renewables use.

- For industry, renewable energy use should increase at a rate of 1.6% per year.

- Buildings should obtain at least 49% of their energy from renewable sources by 2030.

To increase renewable energy production, RED III seeks to accelerate the granting of permit processes for fast-track deployment and will consider renewable projects to be of ‘overriding public interest’. This means that approvals for new renewable energy plants and the connections to those plants, the grid or storage could be fast-tracked.

At present, the EU needs almost 600 GW of solar PV capacity and over 500 GW of wind capacity to reach its climate change targets. This implies a need to add 48 GW of solar PV and 36 GW of wind capacity annually between now and 2030.14

RED III will interact with the EU Reform of the Electricity Market Design initiative, which seeks to offer protection to consumers and producers to boost renewable energy. Consumers will have the right to multiple contracts, including forward contracts that lock in future prices. Power Purchase Agreements will be promoted to protect against price volatility and boost investment in renewables. There will be public support for renewables through two-way Contracts-for-Difference to provide power producers with price stability and shield industry from price volatility. Member States will be encouraged to channel excess revenues to consumers.

The EU aims to reduce transport-related GHG emissions by 90% by 2050 compared with 1990. Zero-emission vehicles, mainly electric vehicles (EV), are central to achieving this, but the infrastructure for transmission, capacity enhancement and charging must also be widely available. EU estimates identify a need for three million charging points by 203015 – the current number is less than 500,000.16 The entry into force of the AFIR seeks to address this by setting binding deployment targets in EU Member States for recharging stations for cars, vans and heavy-duty vehicles, as well as for hydrogen refuelling. The requirements also apply to maritime ports and airports. The timeline to deploy the targets begins in 2025, with fast charging stations for cars and vans, and the supply of electricity for stationary aircraft at all gates, and extends until 2030, when all the infrastructure prescribed in the regulation will need to be deployed. Member States are required to report to the European Commission how they plan to implement the regulation and report progress by 31 December 2024.

There is therefore likely to be growth in green infrastructure deployment, especially for charging points. In 2024 companies, property owners, public sector authorities, maritime ports and airport operators need to monitor how standards are being implemented by Member States and then begin to consider how they are going to provide charging infrastructure in their own facilities.

New opportunities in carbon removals

At present carbon emitters in mandatory compliance markets such as the EU ETS have only been able to purchase carbon credit allowances to count toward the holder’s GHG emissions. Carbon emitters have also been able to purchase carbon credits in the Voluntary Carbon Market (VCM) to offset their own emissions, especially those that are unavoidable. The main distinction between carbon credit allowances from the EU ETS and carbon credits from the VCM is that the latter have not been legally recognised by the EU. This is mainly due to the lack of mandatory rules to monitor, report and verify carbon removals within the EU for voluntary projects.

In 2024 the EU is expected to approve the Carbon Removal Certification framework, the first EU-wide voluntary initiative to certify high-quality carbon removals. The framework includes carbon farming (for example, forest and soil restoration and wetland management), permanent storage (for example, direct air capture and storage) and carbon storage in long-lasting products and materials (wood-based construction) but excludes carbon capture and storage or carbon capture utilisation. Based on the framework, certification methodologies will be developed for each carbon removal activity. These activities will then be certified by a third party and the removals will be recorded in a publicly accessible central registry.

This framework is likely to change the voluntary carbon market (VCM) dramatically in years to come, as it will counter greenwashing and build trust by ensuring that projects are of high quality and removals are quantified, monitored and verified. This means that in the medium term companies will be able to use carbon removals as part of their overall decarbonisation strategy to reach net zero.

Public policy challenges

To support the transition there are still three areas where further work is needed by regulators, standard setters and the industry: funding gaps, emissions accounting challenges and mitigating emissions beyond a company’s own value chain.

Funding gaps

The European Commission estimates that €1.25 trillion will need to be spent by 2030 to meet the EU’s climate and energy security investment needs.17 This estimate represents an increase of over 65% from the past decade and is expected to come from the private sector, including firms and households.18

An example is the EU’s Net-Zero Industry Act which seeks to achieve at least 40% of its annual green technology needs by 2030. These technologies include solar, heat pumps, onshore and offshore renewable technologies, battery and energy storage technologies and carbon capture and storage. The EU has €250bn in funding available for green measures under the Recovery and Resilience Facility (RRF) and can mobilise over €370bn under InvestEU for net-zero investments.19 But the EU has made it clear that the greater part of the required investments will need to come from private funding.20

Emissions accounting challenges

A significant issue is data accuracy and harmonisation, the lack of which hinders comparability of targets and emission reductions data for Scopes 1, 2 and 3.

Companies in the technology sector have on average 125 tier one suppliers and more than 7,000 across the whole value chain. In the auto industry the value chain is even more complex, as an auto manufacturer can have 250 tier one suppliers but up to 18,000 suppliers across the entire value chain.21

For Scope 3 in particular, the issue becomes more complex when companies have global supply chains. Suppliers in some developing countries have limited access to renewable energy and alternative fuels, preventing them from significantly reducing their Scope 1 and 2 emissions. There is a need to find ways to account for these emissions while working with suppliers and stakeholders to reduce them.

Looking beyond value chain mitigation

To be able to reach net zero, companies should look beyond their value chain by investing in projects or conducting actions that avoid or reduce GHG emissions, including those that remove GHG from the atmosphere or store them. These investments or actions could then be reported by companies as part of their overall decarbonisation strategy. Looking beyond value chain mitigation (BVCM) is relevant for companies as once they have reached the point at which they cannot reduce emissions within the value chain any further (due to cost or technological effectiveness), the only option is to invest in projects that can reduce the remaining emissions. To make BVCM feasible the Science Based Target Initiative is planning to publish guidance in 2024 on minimum benchmarks for credibility and best practices.

The implication of BVCM’s guidance is that companies, especially those from hard-to-abate sectors, can help maximise climate mitigation and support the UN’s Sustainable Development Goals.

What companies should do now

Plan to make significant carbon emission reductions across the value chain

- Identify emissions, set targets and have a comprehensive reduction strategy in place, with emission reduction targets for 2030, 2040 and 2050.

- Establish for the medium term (2030) a clear annual CO2 pathway with milestones, correlated to the projected business growth and emissions trajectory. Quantify the costs of implementing the strategy and evaluate how it will be financed, taking into account carbon price uncertainty.

Reduce their carbon footprint in raw materials, fossil fuels and buildings

- Ensure they have carbon footprint data for their key raw materials and identify lower carbon alternatives to reduce potential carbon taxes and improve the company’s emissions record.

- Reduce consumption of fossil fuels in fleets by increasing use of alternative fuels or switching to zero emission alternatives. Engaging with suppliers of low-carbon transportation options is another alternative.

- Put in place a plan to quantify and reduce building emissions by conducting retrofits and deploying green technologies. Companies also need to understand the energy mix of buildings, fully switching to renewables and ensuring that low carbon materials are sourced for retrofits or new construction.

Focus on electrification, renewables and green infrastructure

- Companies should assess all feasible electric solutions. These solutions include the deployment of charging points for EVs, shore-side electric installations for vessels at ports, electricity supply for aircraft at airports, and the replacement of fuel-power equipment with fully electric options.

- The switch to electric requires the use of a 100% renewable energy supply to fully achieve environmental benefits.

- Companies can deploy wind and solar technologies to produce their own electricity on-site and negotiate long-term contracts for renewable energy supply with utility providers.

Averting greenwashing risks

Companies are responding to the green transition in different ways, from innovating their business models and working with new partners in the value chain, to marketing their environmental credentials and linking variable pay to sustainability goals. At the same time, investors, customers and wider civil society are increasing their expectations of companies where the green transition is concerned. To minimise their exposure to greenwashing risk, companies must ensure there is no mismatch between what they say they are doing and what they are doing.

Change needed in B2C communications

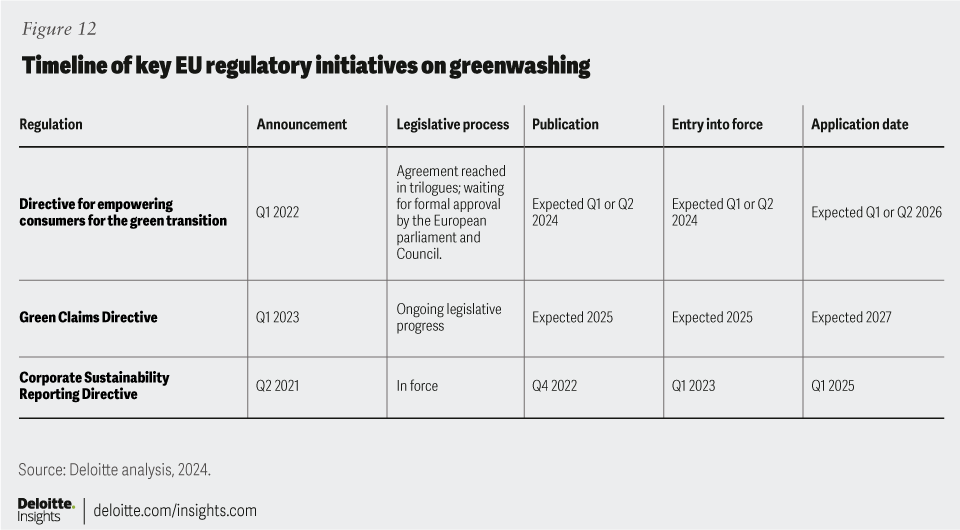

In 2024 the EU will finalise the Directive for Empowering Consumers for the Green Transition. The European Commission proposed the Directive in March 2022 to introduce specific rules to tackle unfair commercial practices that mislead consumers and may prevent them from consuming sustainably. The Directive amends the EU’s Consumer Rights Directive and Unfair Commercial Practice Directive. By defining which B2C communications should be banned or considered misleading, the Directive will provide greater clarity on how companies can market their environmental performance. Once the rules enter into force in the first half of the year the EU will become a global leader in regulating companies’ environmental claims. Every industry will be directly affected by the Directive unless it has existing or upcoming rules governing environmental claims made voluntarily to customers. Financial services firms are excluded from the scope of both Directives.

After the Directive for Empowering Consumers for the Green Transition is finalised and enters into force, EU Member States will have 24 months to transpose the requirements into national law. From 2026 companies will need to ensure that any environmental messages or representations made voluntarily about their products, brand and organisations that imply a neutral, positive or reduced environmental impact are clearly and accurately substantiated. Common generic phases, such as ‘green,’ ‘carbon neutral’, ‘biodegradable’ and ‘eco-friendly’ will be banned across packaging, social media posts and advertisements. Companies providing sustainability labels will also need to ensure that their schemes meet minimum conditions of transparency and credibility.

The EU Green Claims Directive combats greenwashing by setting out new communication, substantiation and verification criteria that companies must meet when devising and marketing their environmental claims to customers. The European Commission proposed the Green Claims Directive in March 2023, but lawmakers are now not expected to progress on the Directive until after the 2024 European elections We expect the rules to enter into force at the earliest in 2025, and to apply from 2027. We wrote about the Directive in more detail in our 2023 Sustainability Regulation Outlook.

Heightened litigation risk and regulatory scrutiny

Companies should not only consider new regulations when assessing the regulatory environment around greenwashing. Action by advertising or competition authorities, or litigation by investors and civil society, may also generate greenwashing risk, possibly sooner than new regulations. Consumer-facing industries, especially those selling and advertising more frequently purchased and essential items, are more likely to experience these impacts.22 Advertisers and organisations marketing products, services and brands online will also be particularly affected.

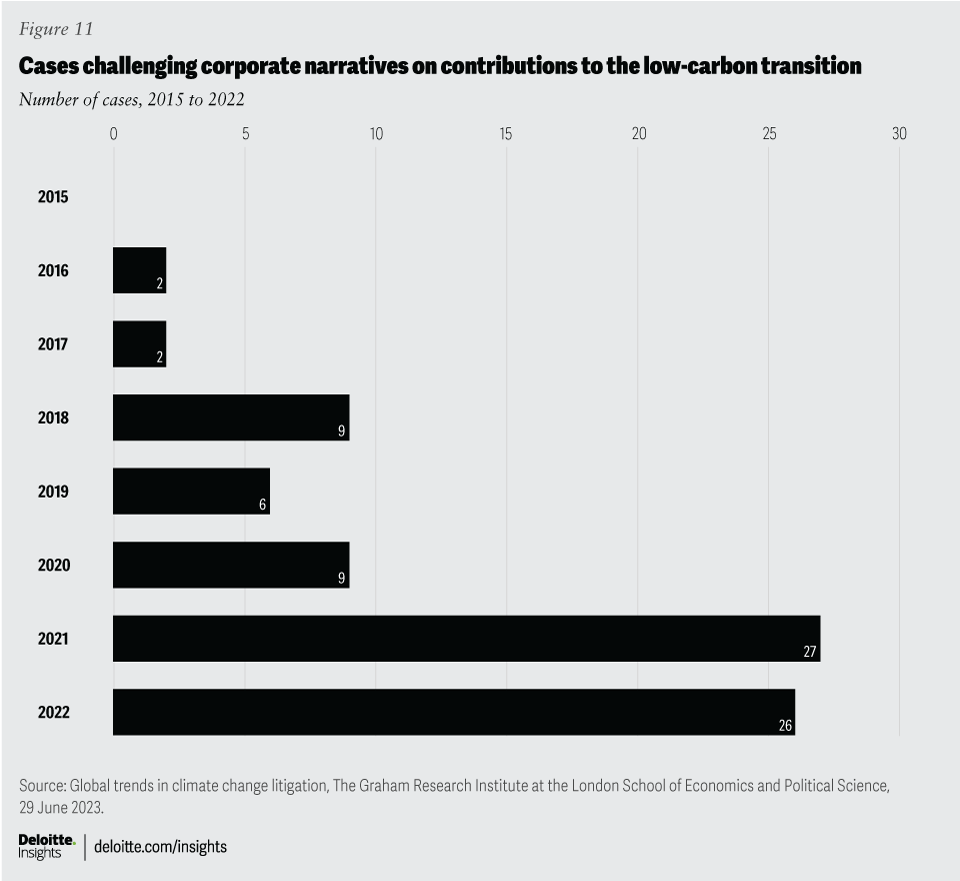

In recent years there has been an increase in allegations of greenwashing that have materialised in legal action (Figure 11) and in complaints to supervisory, advertising and oversight authorities (see case study below). Claims have been based on alleged misrepresentation and breaches of responsible advertising or fair competition legislation or standards, as well as accusations of fraud. The financial and reputational consequences of these actions can be severe, including on share prices.23

We expect litigation and supervisory sanctions to continue as more stringent sustainability regulations emerge, clarifying and increasing the obligation on companies to be transparent and accountable. In response companies may be tempted to stop making any environmental claims. But remaining silent may increase exposure to accusations of ‘greenhushing’, inviting further stakeholder scrutiny.

Corporate sustainability reporting

Companies across all industries also need to consider greenwashing risks in relation to the new corporate sustainability reporting requirements, most immediately CSRD. Drawing together information on more aspects of their sustainability activities and strategy, companies are more exposed to poor quality or misleading data, including data provided by third parties in the supply chain.

Companies can achieve efficiencies in their implementation of CSRD and greenwashing regulations through use of the combined data requirement, as the box below explains.

CSRD synergies can be used to achieve cost efficiencies. The CSRD requires companies to report information that can enable their stakeholders to understand a company’s impact on sustainability matters, as well as how sustainability matters affect the company’s development, performance and position. Information must be reported in line with the European Sustainability Reporting Standards (ESRS). The CSRD intersects with greenwashing risk, creating scope to realise costs efficiencies. For example:

- Responses to CSRD, the Directive for Empowering Consumers and the Green Claims Directive can be integrated if companies form organisational-wide policies on how to gather, analyse, use and review data for all sustainability communications. Data collected, processed and assured for companies’ sustainability reports can then be used to substantiate companies’ B2C environmental claims. This could range from information gathered on water consumption under ESRS E3 to the materials used to manufacture products under ESRS E5, which in turn can help determine a product or organisation’s environmental impacts and performance.

- Double materiality assessments can be used to inform companies of their customers’ sustainability preferences. This information can be fed into brand strategies and help reveal which target segments companies should market their environmental claims to, and how to do so.

- A joined-up regulatory response can streamline companies’ efforts to implement new governance. systems and ultimately instil the cultural change needed to ensure all sustainability messages can stand up to scrutiny.

Balancing short-term compliance costs against longer-term strategic gains

According to the European Commission’s impact assessment accompanying the Directive for Empowering Consumers, companies are expected to spend up to €3.1billion to remove unfounded claims from packaging and online messaging and to adapt their systems and processes to substantiate their environmental claims.24 The up-front costs of designing and implementing the processes needed will be high. Meanwhile, organisations providing sustainability labels are expected to incur costs of up to €3.5billion to implement changes to their internal processes. Manufacturers and sellers using sustainability labels will need to ask themselves whether they are ready when these costs are passed on.

Companies can avoid last-minute disruption and reduce compliance costs by starting the compliance process now. By acting early they can more fully understand how to leverage processes and controls, identify internal skills gaps, and roll out tailored upskilling programmes. They can also conduct peer analysis and determine levers to differentiate themselves from their competitors and begin to integrate new insights into strategic decision-making.

The scale and cost of the compliance challenge is likely to be considerable. But the investment not only reduces the risk of penalties for infringement, but also provides companies with greater agility to access sustainability-related market opportunities in the future.

Unlocking wider value

Investing in the changes required to meet the upcoming rules will not only enable companies to address greenwashing risks but also support their wider sustainability efforts. This includes the actions companies need to take to gather sustainability data and reshape their branding and market positioning.

By considering how to leverage their response to CSRD to generate efficiencies and share costs, companies can also develop a consistent process for devising, communicating and tracking environmental performance across the organisation – from their management reports and analyst updates to marketing brochures and social media posts. Companies’ communication on environmental performance can in this way be lifted to the same level of rigour and trust as their market sensitive and financial information. This will put them in a good position to meet future requirements under the Green Claims Directive.

What companies should do now

- Review the accuracy of sustainability data: Review the sustainability data underpinning the company’s environmental claims, as well as any associated metrics or targets. Data limitations (for example, in terms of quality or availability) should be identified and either rectified or fully disclosed.

- Review and test messaging: Review B2C environmental communications and test the messaging with customers to check if it is clear and well substantiated. This step will enable companies to devise or refine messaging guidelines and update supplier codes of conduct. Companies may also need to brief advertising or PR agencies, and update any corresponding scopes of work as well as contracts.

- Embed greenwashing risk within governance frameworks: It is vital for companies to update their governance processes to support a wider organisational commitment to managing greenwashing risk. Companies can review existing roles and responsibilities, develop management information, and amend executive remuneration to create appropriate incentives and accountability, as we have outlined previously.25

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}