From assessing organizational sustainability to creating value with it

Gaining competitive edge by unlocking the full strategic potential of materiality assessments and double materiality

Materiality assessments are central to regulators’ sustainability agenda

Materiality assessments are a methodology often used by companies to identify the sustainability challenges that they most need to prioritize. These help companies understand the impact of their business activities on the environment, society, and economy, and inform their decisions on how to manage and disclose these impacts.1

Current regulations on sustainability and materiality assessments vary by geography and even by industry. In the United States, the Securities and Exchange Commission has issued guidance on materiality and environmental, social, and governance (ESG) disclosures, stating that companies should consider whether ESG issues are material to their business and whether they should be disclosed in their public filings.2

In the European Union, the Non-Financial Reporting Directive (NFRD) has required large companies to disclose information on their ESG performance since 2014.3 This directive includes a provision on materiality assessments stating that companies should assess the relevance of the information they disclose and only include information on nonfinancial topics that is considered material, especially the concept of double materiality which includes outside-in and inside-out impacts of an organization, is one of the key terms introduced by the directive. From financial year 2024, companies already subject to the NFRD will be required to report under the new Corporate Sustainability Reporting Directive (CSRD), using European Sustainability Reporting Standards (ESRS)4; this includes entities with securities listed on an EU-regulated market with more than 500 employees.5 Further, the directive will apply to large companies that are currently not subject to the NFRD and are due to report under the CSRD in FY2025. Finally, additional listed small- and medium-sized undertakings, small and noncomplex credit institutions, and captive insurance undertakings are required to disclose their sustainability performance from FY2026.6 The reporting requirements include a mandatory double materiality assessment (reflecting an inside-out and outside-in perspective on nonfinancial topics) as the basis for the sustainability reporting. Specifically, the results of the analysis should serve to prioritize and deprioritize topics in the ESRS, which generally requires only material topics to be disclosed externally.7 In this way, the directive aims to provide a comparable and clear methodological path for future sustainability reporting.8

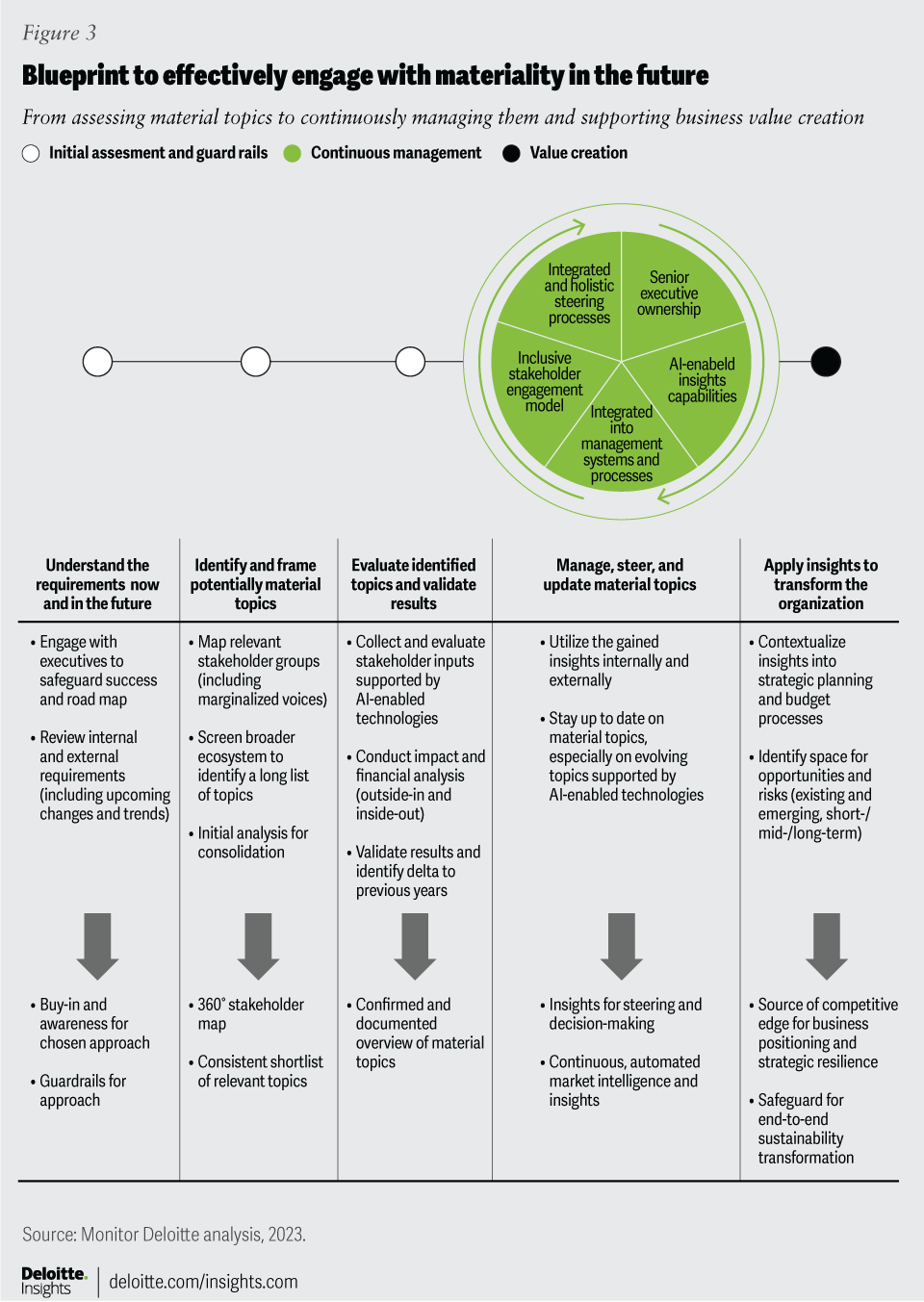

In this report, we are taking a deep-dive into the status quo of materiality assessments and their hidden strategic potential for creating business value. We are analyzing common pitfalls, differentiating between assessment archetypes and their strategic characteristics, and are proposing a blueprint for how companies can enhance their materiality assessments by considering five success factors.

Materiality assessments: How are they conducted?

In general, materiality assessments follow a standardized approach reflecting the requirements defined in different regulatory frameworks and standards:

- Define scope and objectives: Define the general methodology and approach to be applied during the materiality assessment in alignment with relevant regulations and/or industry standards.

- Map the stakeholder landscape: Identify relevant internal and external stakeholders who will be engaged in the assessment process, especially as part of different analyses.

- Develop a long list of potentially material topics: Identify a long list of potentially material sustainability topics and their related impacts, risks, and opportunities using a top-down or bottom-up approach and all available internal and external data sources.

- Conduct an impact analysis (inside-out perspective): Assess the materiality of current potential impacts on the external environment against a set of predefined objective criteria for all identified topics, including engagement with identified relevant stakeholders.

- Conduct financial analysis (outside-in perspective): Assess the materiality of the company’s risks and opportunities in each topic from a financial perspective, based on predefined qualitative and/or quantitative thresholds.

- Aggregate and validate results: Consolidate the results of the analyses into an overview—a materiality matrix—and deduce the company’s material topics, including the impacts, risks, and opportunities (figure 1).

7. Start reporting and communication: Disclose the results of the company’s analysis, including a description of the development process, how it is reflected in its strategy and business model, and relevant reporting KPIs. If the company desires any kind of external business assurance by an independent auditor on the nonfinancial information (including the materiality assessment), additional documentation on the process and/or execution is required.

Common pitfalls in materiality assessments

Materiality assessments have been around for a long time and have become more and more tightly regulated. But they can be reduced to become a reporting instrument and lose their potential to help guide company strategy. Eventually, this can lead to a lack of strategic thinking and a lack of alignment between the company’s sustainability efforts and its long-term business objectives as well as value creation.

Our experience suggests these are the most common pitfalls that limit the true strategic potential of materiality assessments:

- One-size-fits-all approach: Assuming that what is material for one industry or company will be the same for another can be misleading. Materiality is context-specific and can vary widely even within an industry or geography.

- Not linking to business strategy: For the generated insights to be effective, they should be linked to the business's core strategy and objectives.

- Failure to incorporate external long-term risks and opportunities: Materiality assessments should consider the potential impacts of disruptive technologies, climate change, and other emerging, global trends on the company and its stakeholders.

- Ignoring emerging topics: This means focusing only on current topics (the “known knowns”) and not considering potential future risks and opportunities.

- Neglecting adequate stakeholder inclusion: Not engaging a broad spectrum of internal and external stakeholders, or focusing on an inadequate, imbalanced set of stakeholders, can lead to an incomplete understanding of material issues.

- Limited use of big data analysis and technology: Artificial intelligence and other advanced analytics technologies can provide more accurate and comprehensive data analysis, enabling companies to execute the assessment in a more efficient way.

- Overemphasis on quantitative data: While quantifiable metrics are crucial, qualitative insights are equally important. Relying solely on quantitative data means that valuable perspectives can be left out.

- Bias in assessment: An organization might unintentionally prioritize issues that align well with its current strategies or portray these issues in a positive light, rather than addressing other material issues that it has failed even to recognize.

- Failure to act: Identifying material issues is the beginning. Not integrating the insights into business strategies, goals, and actions is a missed opportunity for long-term value creation.

- Lack of transparency: Not being open about the methodology, criteria, or sources used for the materiality assessment can decrease stakeholder trust in the long term.

From materiality assessment to materiality management

Below we differentiate between four ambition levels based on the maturity of the company’s material assessment process and level of strategic integration.

At the Starter level, companies attempt to understand the status quo and their internal setup, often characterized by isolated sustainability efforts without overarching coordination.

At the Advanced level, companies assess their materiality with a strong focus on reporting purposes. They understand external requirements and what is needed to achieve compliance. This typically results in exclusively nonfinancial reporting driven by a central entity, with limited coordination across the organization.

At the Mature level, companies seek not only to report but also to obtain inputs for their sustainability strategy to create additional value. They focus on creating snapshots of their inside and outside environments to meet compliance requirements and fuel strategic considerations.

At the Leader level of strategic materiality are the mature companies that take on a dynamic, continuous outside-in view, using state-of-the-art tools to explore and monitor their material topics, and apply these findings to comprehensive strategic steering and decision-making. By strategically managing materiality continuously and integrating the results into their organizations holistically, these leader companies can focus their efforts on creating additional value.

Where companies stand on reporting

In the EU, the NFRD has applied to around 11,000 large companies. The CSRD now increases this number to up to 50,000 companies (including about 10,000 non-EU businesses9) that must make sustainability disclosures by 2026. Around 18,700 companies already voluntarily disclose through the Carbon Disclosure Project,10 showing they are prepared to supply some of the critical information required under the ESRS on topics such as governance, strategy, risks and opportunities, and metrics and targets.11 We estimate that a majority of those companies conduct at least some type of materiality assessment, putting them at the Advanced or Mature levels according to our categorization. Additionally, large companies that are publicly listed and those that finance themselves on the financial markets and thus, are being rated as well as ranked in ESG ratings (e.g., MSCI and Robeco) tend to lead in the nonfinancial reporting discussion, as market demand and regulatory frames already require high transparency standards across all company activities and data.

How to enhance materiality assessments

Materiality assessments are evolving, with growing attention being paid to “double materiality” that is driven mainly by implementation of the EU’s CSRD and combines both financial (outside-in) and nonfinancial (inside-out) aspects of sustainability. This enables a more holistic approach to sustainability, aligning financial and nonfinancial objectives for the benefit of shareholders and stakeholders alike, but there are additional success factors that will help to advance the assessment and management of sustainability in the future, beyond today's regulatory requirements.

In the figure below we derive five success factors from our market observations and project experience that should be considered if a materiality assessment is planned or the current methodology is to be reviewed. Those success factors are especially relevant for organizations that are targeting strong strategic integration from the assessment.

Understand your organization’s impacts

The concept of “double materiality” ensures that both the company and its stakeholders are considered effectively during the materiality assessment process. This means that the assessment not only considers the impacts of the company’s actions on the environment and society (inside-out), but also the impact of these actions on the company’s ability to achieve its strategic goals and create value for its shareholders (outside-in).

First, companies must assess from an inside-out perspective the impact of its activities environmentally and socially as well as its influences—both negative and positive. This dimension of double materiality is highly relevant to a broad spectrum of the company’s stakeholders, including customers, citizens, business partners, local communities, and regulators.

Second, companies must assess from an outside-in perspective to understand how environmental, societal, and regulatory factors may impact the companies’ financial performance and, therefore, their value creation in the short, mid, and long term, considering potential opportunities and risks.

Design an inclusive stakeholder engagement model

Identifying the relevant stakeholders, their importance, and the topics they find crucial is a key part of any materiality assessment. It is important to ensure that all voices, particularly those that are often marginalized, are heard, and to foster a collaborative environment where stakeholders can contribute meaningfully.

Therefore, any materiality assessment must include comprehensive stakeholder mapping as well as stakeholder engagement throughout the entire process. By engaging with stakeholders—via interviews, surveys, workshops, and dedicated feedback loops—companies can understand their perspectives and needs and the topics that are material to the company. The best practice is to develop robust relationships and continuous engagement that is not limited to a single process activity.

Companies must engage internal and external stakeholders—such as employees, customers, investors, alliance partners, suppliers, and local communities—throughout the process in order to get the most from their perspectives. Their insights will enrich the assessment and provide valuable views on emerging issues and opinions.

As companies assign varying degrees of importance to individual stakeholders, taking account, for example, of their perceived influence on decisions and/or financial performance, they can then prioritize the identified materiality topics and the initiatives and activities that will follow the assessment.

Be aware of how topics are constantly evolving

Dynamic materiality refers to the concept that sustainability issues shift over time, depending on factors such as the evolution of the business environment, changing stakeholder expectations, or the availability of new technologies and data.12 This means that the defined process for the materiality assessment should be regularly reassessed and refined. This allows organizations to adapt far better to emerging trends in real time, for example, in the field of “sustainability foresight,”13 enhancing responsiveness, increasing organizational resilience, and eventually identifying innovation and market opportunities as early as possible. Materiality is not a snapshot but a continuous exercise.

Leveraging AI and automation

The broad field of solutions powered by AI and emerging use cases has the potential to significantly improve materiality assessments by providing more accurate, objective, and comprehensive data analysis, and by enabling companies to execute their assessments more efficiently. For example, AI-powered tools such as IBM Watson, Google Cloud Natural Language, or Deloitte Gnosis that apply natural language processing—a field of AI that focuses on enabling computers to understand, interpret, and generate human language—can help automatically assess sentiment through text analytics. Generative AI models, such as generative pretrained transformers (GPT by OpenAI, PaLM by Google, LLaMa by Meta, or Luminous), can help automate the subsequent report creation. Organizations can, in this way, gain the capability to not just analyze current impacts as a one-time snapshot but also continuously perceive emerging trends, new technologies, and potential future regulations that may affect the organization’s sustainability efforts and related business activities.

AI tools can significantly enhance the efficiency, accuracy, and effectiveness of materiality assessments. They offer real-time insights, predictions, and automated processes that enable organizations to be more agile and responsive in their sustainability efforts. Therefore, it is crucial to gain access to the right data points and the required technologies (such as AI and machine learning technologies) and to combine human expertise and artificial intelligence within the organization.

Conclusion: Materiality as a source of value creation

Materiality assessments are a must-have for any organization. They provide a holistic perspective into the most relevant, impactful topics in the context of sustainability. Sophisticated approaches to assessing and managing material topics can provide benefits for strategy formulation and long-term value creation, while safeguarding the sustainability transformation of the organization. Sustainability and business can be integrated consistently.

We recommend the following when developing the assessment and management of materiality:

- Define a senior executive sponsor at board level, for example, chief executive officer, chief sustainability officer, chief financial officer, or chief strategy officer.

- Set up the materiality assessment as a continuous, embedded strategy process—an input for strategy planning and review cycles to validate investments and mergers and acquisitions, product portfolios, or other opportunities for innovation.

- Assess the organization’s impacts (financial and nonfinancial) in all sustainability topics, applying a double materiality approach.

- Design the stakeholder engagement model with regard to inclusiveness and feedback loops, reviewing the stakeholder landscape, relationships, and touchpoints.

- Identify and implement enabling technologies to increase the efficiency and effectiveness of the process, using, for example, AI-powered solutions for continuous market intelligence, or automated insight and report generation with generative AI.

?$Responsive$&fmt=webp&fit=stretch,1)

{kind=link}

{kind=link}

{kind=link}