Minimum viable transformation has been saved

Minimum viable transformation Part of the Business Trends series

16 April 2015

Leaders are taking lessons from the startup playbook on “minimum viable products” to launch minimum viable transformations—lightweight and readily adaptable versions of potential new business models.

Ecosystems are dynamic and co-evolving communities of diverse actors who create new value through increasingly productive and sophisticated models of both collaboration and competition. Read more about our view of business ecosystems in the Introduction.

Ecosystems are dynamic and co-evolving communities of diverse actors who create new value through increasingly productive and sophisticated models of both collaboration and competition. Read more about our view of business ecosystems in the Introduction.

Leaders are taking lessons from the startup playbook on “minimum viable products” to launch minimum viable transformations—lightweight and readily adaptable versions of potential new business models.

Overview

EXPLORE

Create and download a custom PDF of the Business Trends 2015 report.

By now, top management teams have almost universally embraced the notion that their firms must innovate not only at the level of products and services but at the level of business models. Rethinking the fundamentals of how a business creates and captures value wasn’t a priority in an era of slow change and stable industries, but during a time of rapid convergence of enabling technologies, customer desires, and business ecosystems, it now must be. As early as a decade ago, an Economist Intelligence Unit survey found a clear majority of executives saying that business model innovation would be more important to their companies’ success than product or service innovation.1 Today, it seems the exception to find a strategy session that does not include challenges to—and ideas for reinventing—existing business models.

Yet the dramatic shift toward understanding that business model transformation must be done hasn’t been matched by an understanding of how to get it done. Excellent scholarship has defined what business models are and created a rich case file of innovative ones. But especially for established companies, the path to a new and different business model is far from clear.

This is why a trend we now see emerging is important to track. An analog to a proven approach in launching successful offerings—the use of “minimum viable products”—it has companies pulling together the essential elements of new business models into barely working prototype models, specifically designed to test key risks. Tomorrow’s most impactful business model changes are starting their lives now as minimum viable transformations.

What’s behind this trend?

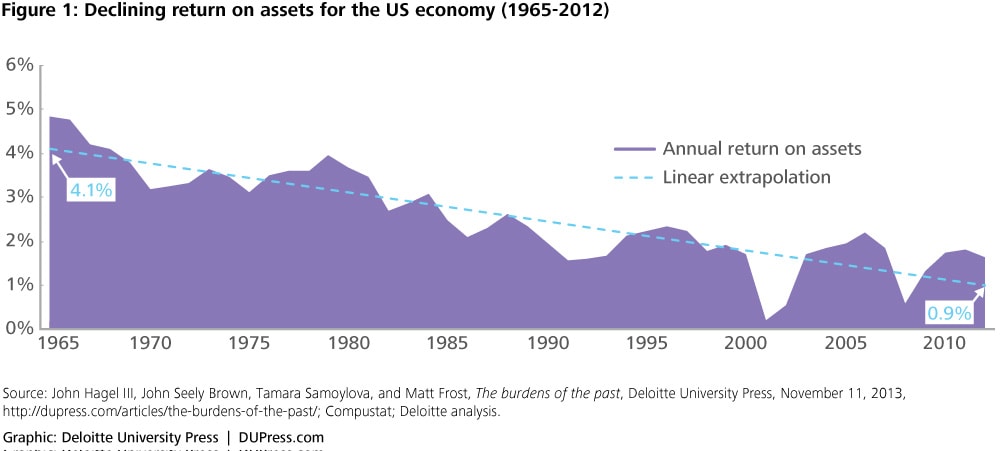

Businesses now need to change more frequently and in more fundamental ways. As documented in the Deloitte Center for the Edge’s Shift Index, they are experiencing intensifying competition, an accelerating pace of change, and growing uncertainty stemming from the increasing frequency of unanticipated extreme events.2 All this adds up to mounting performance pressures. For evidence, look at economy-wide firm topple rates, growing stock price volatility, and serious erosion in the return on assets generated by US public companies—a 75 percent decline since 1965.3 Across the past 50 years, a half-century of enormous technological advances, firm performance has been deteriorating, and the economy has become less predictable.4

But fast, large-scale change is enormously risky. Looking around for reassuring precedents of business model transformation at scale, we find precious few examples. On the contrary, we often hear the opposite—stories of audacious initiatives which flew too close to the sun and fell flat, at enormous expense. One often-referenced study concludes that over 70 percent of all major transformation initiatives fail.5

Some rays of hope, however, come from the growing understanding of what works in entrepreneurial settings. For example, serial entrepreneur (and now educator) Steve Blank has gathered important lessons and principles over the years into books like The Startup Owner’s Manual. His advice contains such valuable truths as “No business plan survives first contact with the customer.”6 Likewise, Eric Ries made important contributions with the work behind The Lean Startup. The praise accorded it by tech entrepreneur and investor Marc Andreessen—that it creates “a science where previously there was only art”7— applies broadly to the many thinkers now working to clarify the mysteries of new business creation.

One concept explored by both these authors has been embraced with particular enthusiasm: the idea of cobbling together a “minimum viable product.” What does that phrase mean? Telling the story of a successful venture he was part of, Ries paints a vivid picture. He recalls a time when he and his partners were out to launch a game-changing new product, and they broke all the rules:

Instead of spending years perfecting our technology, we build a minimum viable product, an early product that is terrible, full of bugs, and crash-your-computer-yes-really stability problems. Then we ship it to customers way before it’s ready. And we charge money for it. After securing initial customers, we change the product constantly—much too fast by traditional standards—shipping a new version of our product dozens of times every single day.8

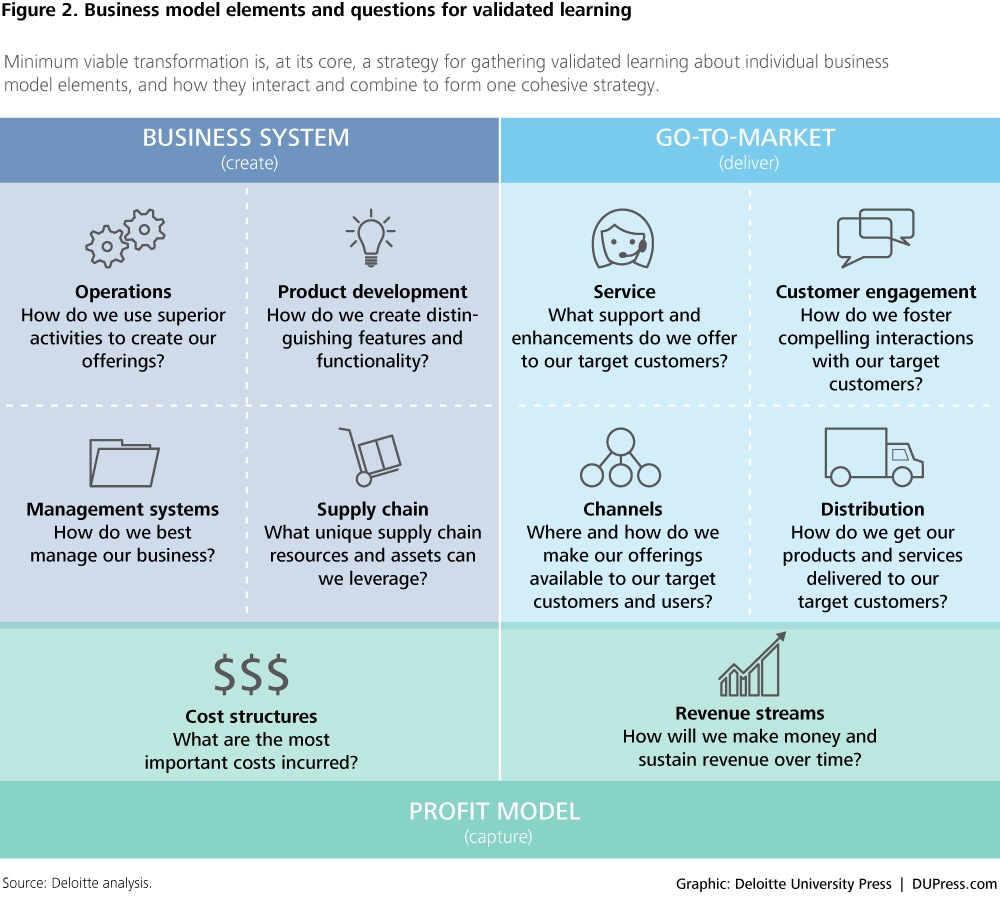

Minimal viable products, he makes clear, are like prototypes except that they are not simply passed around and tinkered with internally. They are immediately thrown at the market and subjected to trial by fire. The real revelation comes with his explanation of why a company would do such a thing. The minimum viable product, he explains, is all about identifying flaws and working to improve them as rapidly as possible. It must be specifically designed, not as a proof of concept, but to test hypotheses and gain knowledge about the biggest unknowns that could sink the new offering. The light bulb for management teams seeking to reinvent not only their products but their business models was that similar unknowns in business model construction—from minute changes to the operations elements to global restructuring of the go-to-market delivery strategy (see figure 2)—could be better understood by a similar process of iterative discovery. This discovery process must also be done with full disclosure to customers, who often prove surprisingly willing to join the journey of learning.

The trend

When Intuit began its transformation from a traditional, desktop software business to a new, software-as-a-service business model, it was certainly looking at some risks. As a market leader in the financial software space, Intuit didn’t have the advantages that a smaller player might—it was less nimble and arguably less amenable to changing market conditions. But it is succeeding: As of this writing, more than half of its customers are now using its software online, and Intuit is posting all-time-high revenue numbers ($4.5 billion, up 8 percent from 2013).9 Intuit’s management believes the company can continue its momentum to hit $6 billion with $5 EPS by FY 2017.10 What was the secret to the successful transformation? According to co-founder and chairman Scott Cook, the answer is simple: By “acting small,” and applying the principles of minimum viable product thinking to big business.11

True, Intuit’s fundamental strategy didn’t change. Its revenues come from the same customer segments paying for the same essential solutions, leaving much of its value proposition intact. But Intuit’s journey from shrink-wrapped desktop products to software-as-a-service required change and reconfiguration of many business model elements, from how it created value through a new hosting platform and new application technologies, to how it delivered value through new distribution channels and marketing messaging, and how it captured value through a subscription pricing model. Just as with the product itself, the innovation team had to understand where the transformation might go off the rails due to unforeseen problems, and find ways to reduce those uncertainties with early, minimally constructed versions of the change.

Business model transformations are not unprecedented in the history of commerce—they have always happened. Few people who read National Geographic today know that it was originally the journal of an explorers’ club whose operations were funded by member dues.12 Today, the enterprise (still a nonprofit) has revenue streams from advertising, books, video production, merchandise licensing, exotic tours, and cable-TV deals—which collectively dwarf the contributions of members who receive its iconic print magazine.13 State Street Bank, founded in 1792, began operations as a full-service financial institution. Today, it has long since abandoned those once-core banking operations, and earns its money providing back-office transaction processing for other institutions.14

Business model transformations are not unprecedented in the history of commerce—they have always happened.

It is not even new that business model transformations must consider the evolution of a company’s broader ecosystem. Consider the case of Charles Schwab about 20 years ago, when it transformed itself from a phone-based discount brokerage to a full-service financial institution by leveraging its ecosystem. This entailed integrating a broad array of third-party analytic tools and investment databases into its online platform and building a network of third-party advisors, allowing the firm to provide “anytime, anywhere” services while also benefiting others in its ecosystem.

What is new today is that such transformations must be considered and accomplished routinely—not as storm-of-the-century events. As management teams look for past practices to make part of their regular toolkit, they are reaching most for the ones that increase the speed and reduce the risk of large-scale change. The concept of the minimum viable transformation is bound to be refined further, and to spread.

Implications

Clearly, there is an implication here. As management teams increasingly pursue business model innovation, they should instruct and empower their strategy teams to launch, and learn from, minimum viable transformations. To put a slightly finer point on things, they should consider the five principles outlined below.

1. Learn how to learn. The central idea behind a minimum viable transformation is to learn from a true field experiment what has to be fixed or put in place before the envisioned business model can succeed at scale. Remember Intuit’s transformation to software-as-a-service. The Intuit transformation team reasoned that by “failing small,” and in a controlled way, it might gain tremendously useful information from the market before choosing which capabilities to scale. The in-flight learning continues through subsequent iterations and trials, allowing the business to keep adapting as the broader ecosystem in which it is situated responds and reacts to its new business model. As Chuck Schwab said in 2013, “If you are an innovator, you have to make mistakes. But if your clients don’t like it, you withdraw it quickly.”15

In other contexts, this data gathering and analytic approach has been called “double-loop learning,” a term coined by business theorist Chris Argyris.16 Rather than just “detecting error” against a pre-defined plan, double-loop learning allows the underlying plan (or the transformative strategy behind capability building) itself to be called into question.

2. Pick up speed. There’s a reason things have to be kept “minimal.” It’s because the learning has to happen fast. All the more so because, as soon as a company has created any instantiation of the idea it is pursuing, it has shown its hand to competitors—who are then in a position to learn from the market’s reception to it, too. Business literature is full of examples of companies who observed changing dynamics, understood pretty well how their ecosystems were evolving, and committed to major transformations—but simply allowed too much time to pass in planning all the details before actually making concrete moves.Conversely, Capital One Labs has found success experimenting with different service and product prototypes. Today, the company performs over 80,000 experiments a year with a focus on gathering big data from such diverse sources as advertising, product, market, and, indeed, business model differentiation.17 In their own words, Capital One Labs is looking to “push the envelope to explore The Art of the Possible.” Capital One understands the speed of modern business, and has been recognized for their insistence on pushing the pace of their own transformation.18

3. Embrace constraints. There is a rich literature concerning the counterintuitive effect of constraints on creativity. Much evidence suggests they don’t foil it; they fuel it. Perhaps most recent has been the celebrated concept of “jugaad” in emerging markets.19A Hindi word, it essentially means “overcoming harsh constraints by improvising an effective solution using limited resources.” While no one would advocate putting an innovation team on a starvation diet, it’s worth noting that the very constraints we’ve been talking about here—minimal bells and whistles, and scarce time—can be the key to forcing extreme creativity. At the very least, they compel a focus on the goal—the need to learn and reduce risk around some key point—and force designers to weed out nonessential elements.Many multinational organizations are finding success in resource constraints as they expand to emerging economies. Such constraints force companies to rethink their business models to not provide “less for less” but to retain the benefits while reducing resource intensity. Such corporations have certainly struggled, but as the Harvard Business Review reports:

. . . the opportunities of the future on a street corner in Bangalore, in a small city in central India, in a village in Kenya… don’t require companies to forgo profits. On the surface, nothing could be more prosaic: a laundry, a compact fridge, a money-transfer service. But look closely at the businesses behind these offerings and you will find the frontiers of business model innovation. These novel ventures reveal a way to help companies escape stagnant demand at home, create new and profitable revenue streams, and find competitive advantage.20

In the realm of business model transformation, there is an even greater benefit of harsh constraints.They give the design team a reason, right up front, to seek collaboration and cooperation from others who will be part of a new business model’s ecosystem. Ideally, these constraints can also give incentive for leaders to harness additional support from ecosystems of third-party participants who can provide complementary capabilities. It limits the number of in-house capabilities necessary for transformation and helps the company to mobilize innovation and experimentation from third parties seeking to participate in an emerging and evolving business model. Promoting ecosystem development from the earliest stages of business model transformation can help build collaborative, future-oriented logic into the very center of the new business; we expect that the most successful business models of the future will likely be those that have a significant ecosystem component.

4. Have a hypothesis. All transformation initiatives need a clear and simple articulation of both the need for change and the broad direction of change. This statement of direction helps leaders to identify key assumptions driving the change effort (assumptions that need to be tested and refined each step of the way) and to develop metrics that will help the participants in the initiative to measure progress in the short term and to learn in real time.

To accomplish such learning, minimum viable transformation efforts must have feedback loops in place for the collection and analysis of market-validated learnings. Such analysis is only possible, however, with an initial hypothesis already in mind. In other words, fully defined assumptions, strategies, and tactics are necessary to know what is being tested in the first place. Transformation leaders should be particularly invested in the initial stages of transformation where those conjectures are laid out, before the data begins to flow in and confirming (or disconfirming) analysis begins to mount.

5. Start at the edge. Earlier we related the story of State Street. One thing it teaches is that beginning transformation at the “edges” of a business is a more reliable strategy for change than attempting to directly transform the core.21 Any attempt to impose a fundamentally new business model in the existing core of the company is likely to invite resistance from existing power structures in the firm—often resembling antibodies rushing to oust an intruding virus—to come out in force. The core is where the bulk of the current revenue and profits are generated—who would want to take the risk of messing with the business model that supports the existing business?

Far better to find an “edge” of the current business—a promising new business arena that could provide a platform for showcasing the potential of a fundamentally different business model and that has the potential to scale rapidly. Crucially, the best edges will have the potential to become a new core, as the back-office capabilities eventually became for State Street Bank. Edges give the transformation team far more degrees of freedom to test and experiment with new approaches to evolving a fundamentally different business model.

Using these five key principles of minimum viable transformation thinking, companies may be able to bypass traditional barriers to transformation, ultimately allowing them to more effectively respond to mounting performance pressures.

What’s next?

“Success is a powerful thing,” said Intuit’s Scott Cook. “It tends to make companies stupid, and they become less and less innovative.”22 The big problem is that it’s a form of stupidity that, in the moment, can feel very smart. High-flying companies with so much to lose become cautious, their every move carefully considered. Indeed, a multiyear study of 526 public companies eligible for the Forbes “Most Innovative Companies List” determined that fewer than 50 companies had made significant jumps in their innovation premium scores between 2006 and 2013.23

The cure for too much risk aversion can’t be reckless abandon. The search for better knowledge of what works—of how to de-risk opportunities to the extent possible while increasing speed—will continue, because the imperative to transform will continue. Performance pressures will only continue to mount, and with them the need for more frequent and fundamental change by enterprises.

Translating the practice of using minimum viable products to the higher level of testing transformation ideas is part of this, but we don’t expect it will be the only part. Expect more “scaling up” of the approaches proving valuable to innovators in entrepreneurial settings and at the level of product and service innovation. The core principles of the minimum viable product—validated learning, rapid prototyping, frugal creativity—can help organizations limit the shortcomings of traditional transformation programs. Minimum viable transformations can reduce risk and increase speed, better enabling business model transformation at scale.

My take

By Rosalie van Ruler Thaker

Rosalie van Ruler Thaker is one of six global specialists responsible for business transformation challenges “from the outside in” for Philips Lighting, the world’s largest manufacturer of industrial, commercial, and consumer lighting. Based in Malaysia, Rosalie coordinates multidisciplinary teams driving end-to-end transformation initiatives in Asia, Africa, and the Middle East.

In the end, business transformation is about unlocking trapped value. In a place like Philips Lighting, which operates in a fast-changing industry, we need to be pinpoint focused to do that well. Where can we direct energy to start the kind of snow-balling change that naturally gathers momentum once kick-started?

In the end, business transformation is about unlocking trapped value. In a place like Philips Lighting, which operates in a fast-changing industry, we need to be pinpoint focused to do that well. Where can we direct energy to start the kind of snow-balling change that naturally gathers momentum once kick-started?

The required diagnostic work happens up and down the organization. I’m doing it deep inside of Philips Lighting pretty much constantly, and it is simultaneously happening at higher levels as well. This top-to-bottom dynamic allows us to identify the right priorities for business transformation at Philips as part of a company-wide effort, initiated by our CEO Frans van Houten, called “Accelerate!”

We always start a change effort from an outside-in perspective, conducting detailed customer interviews, and then working our way back into the propositions and capabilities that will meet our customers’ needs. The best opportunities can be anywhere in our value chain and can involve partners from throughout the dynamic ecosystem of digital lighting. My job is to find the handful of critical levers that will drive a solution end to end, from the source of the blockage all the way back down to customer satisfaction.

We launch transformation efforts with an intervention design, a hypothesis about the few lead dominoes most in need of a push. If our diagnostic work has been done well, getting those to tip in the right direction can often set off chain reactions of positive results. We seek to be opportunistic and view ourselves as catalysts. We also emphasize learning, to make sure that the organization can carry through the transformation after we leave and can initiate a new one whenever new challenges or opportunities arise. In effect, we send a pulse through the system and carefully monitor what happens. If I can’t see the cascade beginning, I stop and rethink initial assumptions. Hypothesize. Test. Learn. Adjust. And transform.

Ultimately, transformation isn’t something you do once, it’s a continuous journey. It means identifying impactful opportunities, and having the foresight to know when small initiatives can become big. It’s about providing that “something extra” to help Philips enhance shorter-term hit-the-numbers thinking with a vision of fast-evolving business environments. I’m always thinking about the “butterfly effects” of something that may look small today, but tomorrow, turns out to represent the future.

© 2021. See Terms of Use for more information.