Blockchain: Democratized trust has been saved

Blockchain: Democratized trust Distributed ledgers and the future of value

25 February 2016

Trust is foundational to business, yet maintaining trust—particularly throughout a global economy—is expensive, time-consuming, and, in many cases, inefficient. Could blockchain applications become part of the answer?

Trust is a foundational element of business. Yet maintaining it—particularly throughout a global economy that is becoming increasingly digital—is expensive, time-consuming, and, in many cases, inefficient. Some organizations are exploring how blockchain, the backbone behind bitcoin, might provide a viable alternative to the current procedural, organizational, and technological infrastructure required to create institutionalized trust. Though these exploratory efforts are still nascent, the payoff could be profound. Like the Internet reinvented communication, blockchain may similarly disrupt transactions, contracts, and trust—the underpinnings of business, government, and society.

Explore

View Tech Trends 2016

Learn more about Deloitte Technology Consulting

Create and download a custom PDF of the 2016 report

Discussions of blockchain often begin with bitcoin, the cryptocurrency that gained notoriety as much for its novelty as for the volatility of its valuation. In a fog of media reports driven by bitcoin’s associations with dubious use cases,1 the far-reaching potential of blockchain—the technology underpinning bitcoin—remained largely obscured. Yet, that is changing. Organizations throughout the public and private sectors have begun exploring ways that blockchain might profoundly transform some of their most basic operations, from the way they execute contracts and carry out transactions to the ways they engage customers and more.

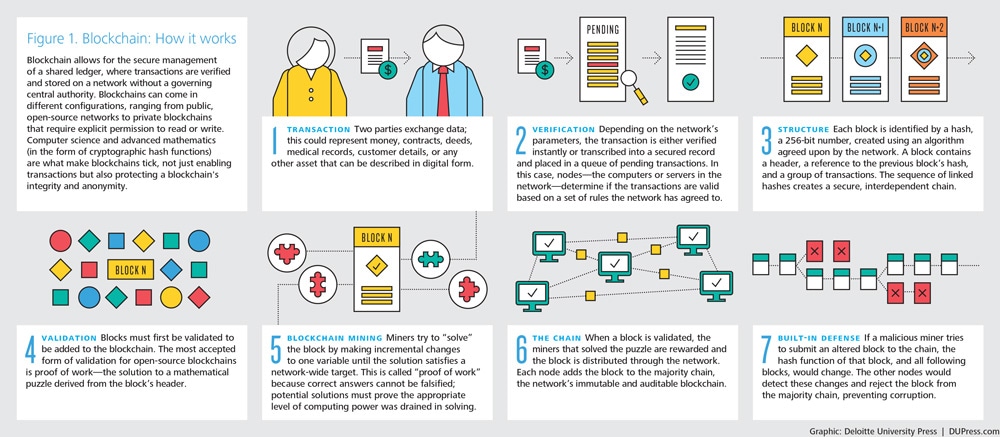

What is blockchain? Simply put, it is a distributed ledger that provides a way for information to be recorded and shared by a community. In this community, each member maintains his or her own copy of the information and all members must validate any updates collectively. The information could represent transactions, contracts, assets, identities, or practically anything else that can be described in digital form. Entries are permanent, transparent, and searchable, which makes it possible for community members to view transaction histories in their entirety. Each update is a new “block” added to the end of the “chain.” A protocol manages how new edits or entries are initiated, validated, recorded, and distributed. With blockchain, cryptology replaces third-party intermediaries as the keeper of trust, with all blockchain participants running complex algorithms to certify the integrity of the whole.

It seems ironic that as digital transforms the world, one of its more promising building blocks is a throwback to our decidedly analog past. Blockchain is the tech-charged equivalent of the public ledgers that were once used in towns to record everything of importance: the buying and selling of goods; the transfer of property deeds; births, marriages, and deaths; loans; election results; legal rulings; and anything else of note. Instead of a bearded master wielding a long-stemmed stylus to record minuscule entries into an oversized book, blockchain uses advanced cryptography and distributed programming to achieve similar results: a secure, transparent, immutable repository of truth, one designed to be highly resistant to outages, manipulation, and unnecessary complexity.

Rewiring markets

Blockchain’s ability to replace middlemen with mathematics is precisely why this technology matters. It can reduce overhead costs when parties trade assets directly with each other, or quickly prove ownership or authorship of information—a task that is currently next to impossible without either a central authority or impartial mediator. Moreover, blockchain’s ability to guarantee authenticity across institutional boundaries will likely help parties think about the authenticity of records, content, and transactions in new ways. Consider, for example, the efficiencies that shared ledger technology might bring to the labyrinthine global payments market. Or how a secure, transparent, transactional environment might help developing countries reduce the estimated $1.26 trillion they lose each year to corruption, bribery, theft, and tax evasion.2

The financial services industry (FSI) plays an important role as today’s institutional authority of record for payments and remittances, the issuing and trading of securities and trading, and ownership of financial instruments. It comes as no surprise, then, that FSI organizations are aggressively pursuing blockchain investment and experimentation. Outside of the financial sector, organizations across industries are also ramping up their own blockchain programs and exploring opportunities, with next-generation payments, loyalty and rewards platforms, smart contracts, asset management, and exchange scenarios leading the charge.

Meanwhile, venture capitalists have invested roughly $1 billion in 120 blockchain-related start-ups—half of that investment taking place within the last calendar year.3 Investors recognize that the blockchain ecosystem lends itself to different use cases and technology enablers, from payment processors and digital wallets to cryptocurrency exchanges and blockchain-based platforms. Analysts at one investment bank commented on this trend recently, saying, “We expect venture capital flows to accelerate in 2016 and lead to further development of the foundational and infrastructure services necessary to create a fertile ‘plug and play’ ecosystem for entrepreneurs and innovation that may ultimately escalate enterprise adoption from a trickle in 2016 to a multi-year boom starting in 2017.”4

Blockchain consortiums are forming as well. For example, R3 CEV, representing more than 42 of the world’s largest banks, is creating a distributed ledger platform to power FSI’s foray into blockchain.5 The Digital Currency Group, sponsored by MasterCard, New York Life, and others, manages and operates a portfolio of blockchain and cryptocurrency investments.6 Enabling technology players are also getting involved. The Open Ledger Project, backed by IBM, Cisco, Intel, the Linux Foundation, and others, has created a standards-based, open-sourced blockchain platform to accelerate adoption and the development of surrounding services.7

Patterns of value

And we’re only getting started. With new use cases emerging weekly, it’s worth examining both the underlying benefits of blockchain8 as well as the operational areas in which blockchain may add little value. Blockchain often works best when the following conditions are met:

- Transparency: Ease of sharing and visibility are essential features of a blockchain; lack of one or the other of these is often a central driver of blockchain adoption. They become particularly critical in transactions in which more than one organization is making blockchain entries.

- Trust: The immutability of blockchain makes it nearly impossible for changes to be made once established, which increases confidence in data integrity and reduces opportunities for fraud.

- Disintermediation: With blockchain, peer-to-peer consensus algorithms transparently record and verify transactions without a third party—potentially eliminating cost, delays, and general complexity.

- Collaboration: Blockchain can be programmed to instigate specific transactions when other transactions are completed. This could help parties collaborate without increasing risk on transactions with multiple dependences, or those authored by different parties.

- Security: With private and public key cryptography part of blockchain’s underlying protocol, transactional security and confidentiality become virtually unassailable. Trust zones can also be established, including open public ledgers and permission-based shared or private blockchains in which participation is limited to select entities.

Lessons from the front lines

Establishing trust in real time

With 16 million clients worldwide and operations in 40 countries, Royal Bank of Canada (RBC) executes large numbers of cross-border payment transactions each day, including bank-to-bank, business-to-business, and peer-to-peer remittances.9

The traditional process used throughout the banking industry to execute such transactions can be cumbersome, often involving multiple intermediaries, customer fees, and lengthy reconciliation tasks.10 Recognizing an opportunity to increase efficiency and lower operational costs, two years ago RBC began looking for technologies that could help it develop a new approach to cross-border transactions.

“At that time, many people in our industry were exploring possible uses for bitcoin,” says Eddy Ortiz, RBC’s vice president, solution acceleration and innovation. “As we came to understand more about the challenges we faced, we realized the underlying technology powering it was what was particularly exciting.”

RBC’s first step was understanding what blockchain was and, importantly, was not. Beyond technical and functional aspects, the RBC team needed to understand the business problems blockchain might help their organization solve. Cross-border payments emerged as a prime opportunity: Clearly, there was value in the ability to settle transactions in near-real time.

After researching numerous shared-ledger technology options, RBC settled on Ripple, a provider of global financial settlement and FX market-making software solutions. Ripple makes it possible for financial institutions to send and receive cross-currency payments more efficiently by connecting banks directly to each other via distributed financial technology. Because transactions are immutable and carried out in real time (five seconds), Ripple can also help mitigate fraud, credit, FX, and counterparty risks.

Ripple and RBC are working on a limited-production proof of concept now. As much promise as blockchain represents, it is crucial to validate its scalability, reliability, security, and performance for a large-scale deployment. RBC looks to do just that before expanding into other areas.

Meanwhile, RBC is currently exploring other distributed ledger use cases as well. One option involves creating a loyalty platform11 in which the bank engages customers in real time through a blockchain to help them better understand the points and rewards they are accruing as they use RBC products and services. Likewise, customers will also be able to engage directly with a variety of RBC partners via the blockchain for real-time redemption of reward points. “Our customers will be able to see their points accrue each time they use their RBC credit card,” says Ortiz. “And the reward points become like liquid cash, enabled by blockchain.”

Selling the idea within RBC of changing long-established cross-border payment processes with blockchain became its own challenge. “We either oversimplified our plan and senior leadership didn’t see the value, or we went too technical and lost them,” recalls Ortiz. By working with several RBC stakeholders to refine their pitch and focus more on the specific business problems to be solved, Ortiz and his team got the green light to proceed in exploring these opportunities with Ripple and other partners.

Whether cross-border payments, rewards programs, or more ambitious forays around smart contracts, RBC’s exploration of blockchain technology comes down to use cases—the business problems that technology can help alleviate.12

No good deed goes unrecorded

To help stem long-standing corruption in Honduras’ land title registry system, in 2011 the World Bank announced it would loan the Honduran government $328 million to digitize title files and upgrade tools and processes.13 While subsequent efforts did help modernize and standardize the government’s administrative capabilities, they also made it easier for corrupt players to hack into central databases and illegally alter digital land records.14

In May 2015, Factom, the organization that manages open source software for securely recording transactions through a distributed, decentralized protocol, announced that it would be working with Epigraph, a land title software vendor, to help the government of Honduras recreate its digital land title registry system in a blockchain. The goal of this effort is simple: Use blockchain technology to create a transparent land title registry system in which digitized records are tamper-proof.15

The system being developed addresses existing security vulnerabilities in several ways. First, individual land records are digitized—“hashed” or encoded with an immutable fingerprint—and stored permanently on the blockchain. The system then tracks and documents every change of ownership, every loan made against a single piece of land, and every contract made against mineral rights. Users can track the entire history of a land title instantly. They cannot, however, alter anything currently in the system. They can use a stored version to create a new document, but they will not be able to recreate or replace a hash once it is filed.

The Honduran blockchain initiative is in a pilot program for a single city, with a system built and capable of accepting entries. In the coming year, project leaders plan to roll out the pilot to additional municipalities.16

A Linq to the future

In 2014, blockchain technology made waves as the underpinning for the cryptocurrency bitcoin. In 2015, it’s making waves again, this time in the financial services market.

Currently, managing the issuance and exchange of shares in private companies is a paper-based, manual process. This can be cumbersome, time-consuming, and error-prone. Private companies typically handle sales and transfers of shares with informal mechanisms such as manually maintained spreadsheets. NASDAQ wants to replace that process with a system built on blockchain technology.

Earlier in October 2015, NASDAQ (MX Group Inc.) rolled out Linq, a blockchain-based platform and ledger system that manages the buying and selling of shares of private companies. Linq provides clients with a digital ledger that creates a record in the blockchain of every transfer of security among private users, providing improved auditing and increased transparency of ownership. Some of the first companies on the platform include Synack, Tango, and Vera.17

The experiment joins a slew of financial industry forays into bitcoin-related technology. While the innovation is an achievement in and of itself, it also represents the potential for future transformational change in the infrastructure of financial services. If the effort is deemed successful, NASDAQ, one of the world’s largest stock markets, wants to adopt blockchain technology, which could shake up systems that have facilitated the trading of financial assets for decades.

While a completely revamped digital infrastructure for financial services markets will take some time, there are promising initiatives underway across the world. NASDAQ is preparing to roll out blockchain applications in Estonia, where it owns the Tallinn Stock Exchange and the Estonia Central Securities Depository.18 The applications will focus on improving the proxy voting process for companies as well as company registration and public pension registration, programs that NASDAQ manages for the government of Estonia.

Some things should remain private

An individual’s digital medical records are often distributed across systems in physicians’ offices, hospitals, insurance companies, or other organizations. As such, any one doctor or service provider may not have access to all of the information necessary to meet a person’s health needs. Moreover, though these records contain highly personal, confidential information that should never be made public, no single authority controls them, thus making them vulnerable to cyber threats and unintentional leaks.

One global manufacturer of medical technologies is exploring how individuals might use blockchain technology to take control of their own medical records in a secure “distributed medical records system” similar to a bitcoin wallet. Though the model under development is still a prototype, its basic design spotlights the potential value blockchain may soon add in the arena of security and privacy.

Here’s how it works: A doctor notices that a patient is due for a certain medical procedure or test. The doctor initiates a transaction marked with the patient’s unique digital identity within the individual’s blockchain wallet. Then, via email, the doctor alerts both the patient and the relevant practitioner or specialist who will schedule and perform the required procedure. Upon completing the task, the relevant practitioner will assign a proof that the procedure has been administered to the patient’s blockchain wallet. At the same time, smart contract logic built into the blockchain sends this proof to relevant third parties. These could include organizations like the Centers for Disease Control, which tracks vaccination rates (among other statistics), or the patient’s insurance carrier, which will process payment or reimbursement. As the holder of the blockchain key, the patient—and only the patient—determines who else should receive this information.

Though this limited use case focuses exclusively on medical records, the ability for individuals to create digital identities and use them within distributed ledger systems to secure and manage personal information will likely underpin similar use cases going forward. The ultimate benefit? In the near future, individuals may be able to aggregate all of their personal information—such as their financial, medical, and purchase histories—into one secure ledger with a single digital identity, with full control over how and with whom credentials will be shared.

My take

Brian Forde Director of digital currency, MIT Media Lab

From the cover of the Economist to an eye-popping billion dollars invested in bitcoin-related start-ups, we are increasingly seeing companies explore business opportunities using bitcoin and other cryptocurrencies. The reason: This emerging technology could potentially disrupt the way people and organizations carry out a wide variety of transactions. For example, using cryptocurrencies, such as bitcoin, people can transfer money without a bank or write enforceable contracts without a lawyer or notary. Companies could make online payments more secure and inexpensive. In fact, similar to the Internet, which exponentially increased communication by reducing cost and friction to near zero, cryptocurrencies have the potential to exponentially increase transactions for the same reasons. Ultimately, new entrants will adopt this emerging technology and disrupt existing industries.

So what does this mean to your company right now? To understand the potential of cryptocurrencies, you should review how your company completes transactions with customers. Money transfer is one of the first types of transactions to think about. Identify the brokers and middlemen who are extracting fees from your transactions. Maybe it’s a credit card processor or an intermediary involved in a wire transfer. These parties—and the transaction fees they charge—may no longer be needed when you carry out transactions with cryptocurrencies. At its core, this technology enables transactions between two parties without requiring a costly middleman.

Consider other potential opportunities that are specific to your industry. The entertainment industry might leverage cryptocurrencies to manage event ticketing. By issuing concert tickets on the blockchain, fans can verify transfer of ownership from one digital wallet to another, rather than worrying whether the PDF of the ticket they received was sold to 10 other people. Financial services firms may be able to streamline legal and contractual interactions with customers. Media companies could transform their approaches to managing digital rights as well. In 2015, British musician Imogen Heap made headlines by demonstrating how a song could be released on the blockchain to manage who has the rights to listen to the song.19 Previously, artists have been forced to use more common proprietary digital rights management platforms. With the blockchain, the artist will receive his or her royalty payments sooner and you, as a customer, actually own the song and can resell it to others. With digital rights platforms, that’s illegal.20

The argument for embracing blockchain becomes more urgent given the risks associated with storing customers’ personal information. For example, to prevent fraud, many online retailers require customers to provide their name, home address, and other personal information associated with their credit card—just to make a purchase. However, these data repositories become honeypots that, in today’s world, increase the likelihood of a cybersecurity attack on your company. With bitcoin, you wouldn’t need to ask for, or worse yet, store any personal information to complete a purchase. What’s more, developers are now looking into using the blockchain for electronic medical records, educational transcripts, or other personal information stores that would benefit from better privacy and interoperability.

Today, we are seeing how the ability to transfer the ownership of assets directly from one party to another—safely, efficiently, and without an intermediary—can increase efficiency and reduce transaction costs for pioneering companies willing to experiment with this emerging technology. But before you embark on this journey, download a bitcoin wallet and try it for yourself. It might just spark a new idea for this nascent technology.

Cyber implications

To a large degree, current interest in blockchain is fueled by the security benefits this emerging technology offers users. These benefits include, among others:

- The immutable, distributed ledger creates trust in bookkeeping maintained by computers. There is no need for intermediaries to verify transactions.

- All transactions are recorded with the time, date, participant names, and other information. Each node in the network owns the same full copy of the blockchain, thus enhancing security.

- Transactions are authenticated by a network of computer “miners” who complete complex mathematical problems. When all miners arrive at the same unique solution, the transaction is verified and recorded on the “block.”

The distribution of miners means that the system cannot be hacked by a single source. If anyone tries to tamper with one ledger, all of the nodes will disagree on the integrity of that ledger and will refuse to incorporate the transaction into the blockchain.

Though blockchain may provide certain security advantages over more traditional transactional systems that require intermediaries, potential risks and protocol weaknesses that could undermine the integrity of blockchain transactions do exist. In 2014, for example, it was discovered that, in several instances, a single mining pool had contributed more than 50 percent of bitcoin’s mining. During these relatively brief periods, the pool had unprecedented power to circumvent the decentralization that differentiates bitcoin from traditional currencies. For example, the group had the ability to spend the same coins twice, reject competing miners’ transactions, or extort higher fees from people with large holdings.21 In a separate 2015 incident, Interpol cyber researchers issued an alert that it had discovered a weakness in a digital currency blockchain that would allow hackers to stuff the blockhain with malware.22

Given that there is no standard in place for blockchain security, other potential cyber issues could emerge. For this reason, there currently exists an overreliance on crowdsourced policing.

Blockchain is a new technology, and therefore discussion of its potential weaknesses is somewhat academic. But what if your whole financial system fell apart because of some underlying vulnerability in blockchain that was discovered down the road or because computing power caught up, allowing someone to break the system? Though you should not let fear of such scenarios prevent your company from exploring blockchain opportunities, as with all leading-edge technologies, it pays to educate yourself, work with partners on cyber issues, and remain secure, vigilant, and resilient.

Where do you start?

Early adopters—largely within FSI—are piloting blockchain in innovation labs and by investing in technology start-ups. Organizations across industries should aggressively explore scenarios in which blockchain could reinvent parts of their operations, value chains, or business models. They should look for ways blockchain could help bring new efficiencies to costly, slow, or unreliable transactions and introduce new models for partnership and collaboration. Are there new products and offerings that can extend the blockchain platform? What about designing products that leverage shared-ledger technology? Whatever the specific play, it is time to dig in, gain understanding and experience, and determine if—or, more likely, where—blockchain can help in your organization.

Specific areas of focus may include:

- Education: Unlike other emerging technologies such as mobile, analytics, or even the cloud, blockchain can be confusing—what it is, how it works and, most importantly, why it matters. Moreover, some of the earliest and most public use cases involving bitcoin may be deemed irrelevant or underwhelming. Concerted education efforts are required, ideally coupled with a disciplined approach to innovation and a prototype demonstrating potential use cases specific to a given organization and industry.

- Embrace the ecosystem: The blockchain community is seeing considerable investment from established industry institutions, technology vendors, academia, venture capital firms, and start-ups, among others. Now is not the time to worry about which blockchain technologies or standards will dominate. That said, any solutions should include abstractions around protocols and platform features to allow portability should it eventually become necessary to switch to a different standard.

- Partner? Perhaps: With the blockchain ecosystem growing, to accelerate ramp-up and adoption efforts, it may make sense to partner with one or more vendors. But before signing on the dotted line, try to understand what makes a prospective partner’s offering unique. Is the partner willing to co-invest in solutions (or even in proofs of concept) that will meet your specific needs? Typical caveats apply for tapping start-ups: understanding the leadership team, board, VCs, funding level, and financial viability. Whether the partner is big or small, define the exit strategy up front to remove hard dependencies and imbalances in future negotiations. Given the nature of the blockchain, partnerships with peers and competitors might be options as well.

- Know your trust zones: Public, “private” (permission-based), or hybrid? The implications are more pronounced than they may immediately appear. Established players often create permission-based, tightly managed trust zones that basically impose legacy thinking about what constitutes “trust” on a new architecture. Remember, each case will likely be unique and thus require its own trust-zone variation. With blockchain, the most effective option may not always be permission-based.

- Understand blockchain’s limitations: Blockchain is not a cure-all, just as it is not simply a glorified shared database. The computational requirements to run the blockchain’s consensus algorithms23 consume time and resources. The very features that protect blockchain against theft and fraud could also drive overhead if not correctly implemented. As such, high-volume transactions with latency sensitivity may not be ideal candidates for blockchain.

- Remember the miners: With bitcoin, miners earn bitcoins for carrying out mining tasks. In your use cases, what economic incentives will you put in place to entice miners to perform the mining and recording tasks?

- Regulation and compliance: Here, there are two points to consider. With blockchain technology, progress is outpacing regulation, which may help users gain momentum with their blockchain initiatives in the short term. Eventually, regulation—and legal precedents that recognize blockchain transactions—will almost certainly catch up with this technology. Public blockchains will most likely be subject to oversight by governing bodies similar to those overseeing various aspects of the Internet. Private blockchains will be managed under private agreements.

The second regulatory consideration is more interesting. Though costly and, in some places, inefficient, third-party clearing houses, exchanges, government agencies, and other central bodies play an important role in arbitration and conflict resolution. Each typically has authority to reverse transactions. Existing financial industry systems had very similar goals when they were introduced in the 1970s24—improve efficiency and instill trust by overhauling outdated legacy systems and processes. Though the technological differences between those systems and blockchain are enormous, regulation designed to standardize open-ledger transactions could prove beneficial for the financial and legal systems as a whole, and for early adopters who have already embraced blockchain.

Bottom line

Business, government, and society are built on trust. Even cynics who argue for more fiscally driven motivations only reinforce this basic point. After all, money is only a concept whose value is linked solely to collective faith in its value as tender for debts, private or public. As such, any promise to use modern computing principles to transform how we achieve and apply trust is disruptive—perhaps on an historic scale. Will the eventual embrace of blockchain mean that venerable institutions of trust disappear? That seems unlikely. It does mean, however, that very soon they may have to transform themselves if they hope to continue participating, substantively and efficiently, in blockchain’s brave new world.

Deloitte Consulting LLP’s Technology Consulting practice is dedicated to helping our clients build tomorrow by solving today’s complex business problems involving strategy, procurement, design, delivery, and assurance of technology solutions. Our service areas include analytics and information management, delivery, cyber risk services, and technical strategy and architecture, as well as the spectrum of digital strategy, design, and development services offered by Deloitte Digital. Learn more about our Technology Consulting practice on www.deloitte.com.

© 2021. See Terms of Use for more information.