Sourcing innovation New collaboration models are shaping the future of the automotive industry

8 minute read

04 January 2019

Marc Holzer United States

Marc Holzer United States Omar Hoda United States

Omar Hoda United States Jeff Glueck United States

Jeff Glueck United States Jason Karew United States

Jason Karew United States

Automakers are navigating new ecosystems and testing new collaboration models. They can succeed by preparing the organization for change before it occurs.

Today’s automotive original equipment manufacturers (OEMs) and suppliers face a complex environment unlike anything the industry has experienced before. Electrification, the sharing economy, autonomous vehicles, nontraditional entrants to the industry, the growth of new products and services enabled by digital business models—these factors combined are driving uncertainty about the future and significantly influencing strategy decisions around the globe.

Learn more

Explore the Future of Mobility collection

Subscribe to receive related content

Download Deloitte’s 2019 Automotive News supplement

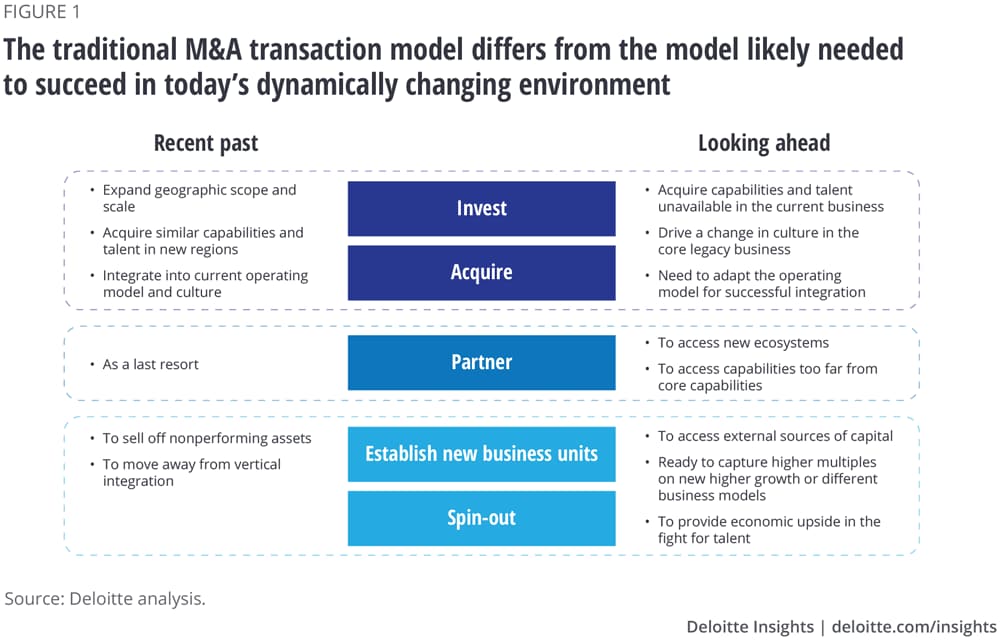

In response to these challenges, M&A and strategy executives should reexamine their approach and strategy around dealmaking. The traditional playbook for “where to play and how to win” has fundamentally changed. It’s no longer a question of simply finding, acquiring, and integrating competitors to realize cost savings. Rather, M&A executives often now need to better equip an organization to adapt, change, and grow in a world where the value system is changing, new ecosystems are emerging, cooperation among competitors is accelerating, and new business models are disrupting established industry players (figure 1). And it’s not just traditional M&A that can have this focus. A variety of collaborative efforts, from joint ventures to investments to partnerships, can be used to gain access to potentially transformative innovations and capabilities. This article explores a framework that M&A executives can use which goes beyond the traditional playbook to find and exploit opportunities for growth and innovation, focused around two key activities: engaging with ecosystems, and successfully integrating innovation and capabilities developed outside the organization.

Engaging the ecosystem: Meet me in … Tel Aviv?

Detroit, Stuttgart, Tokyo: These are the traditional hubs for the automotive industry’s ecosystems, where OEMs and suppliers headquarter, operate, and collaborate. But those aren’t the only places where the future is being built. Increasingly, innovative new technologies and business models are being developed and incubated in places that weren’t even on the automotive map five years ago—places like Tel Aviv, Silicon Valley, and Boston, among others. To gain access to innovations, a physical presence and substantive operations in these locations can be vital to an automaker’s strategy. This presence can take many forms, including office spaces to attract and retain talent in areas such as robotics, software development, and cybersecurity, or “working labs” that give automakers the opportunity to physically engage with startups to support product development and innovation.

To compete effectively, automakers should consider new models of collaboration and sharing that are both farther-reaching and more nuanced than traditional OEM-supplier agreements. This might mean investing in startups, either financially or through co-development arrangements, or becoming a limited partner in a venture capital fund to gain exposure to new ideas and business models. It also means that automakers may need to reach outside the industry for expertise—most likely to the technology industry to gain access to capabilities in areas such as cloud, connectivity, cybersecurity, and data management. An acquisition of, or investment in, a startup might be a strategic option—but more likely, a physical presence that drives collaboration and shared learnings within the ecosystem will be a smart first step and may, on its own, give the automaker the access to the talent and innovation it seeks.

Integrating acquired innovations and capabilities: “Landing pad” or “Launch pad”?

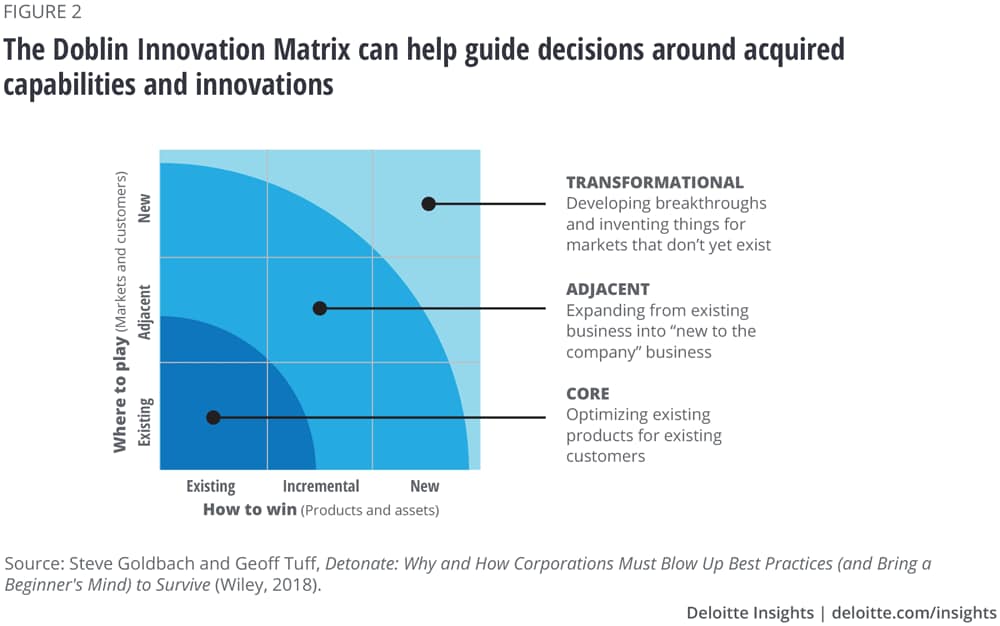

When considering how to integrate an externally sourced innovation or capability, the Doblin Innovation Matrix® (figure 2) can serve as the starting point of a road map to help companies determine “where to play” and “how to win”—that is, to figure out what to do with the innovation or capability being integrated. This calculus applies most obviously to assets acquired outright through M&A, but it also can be useful when deciding how to operate “assets” acquired through other means.

A simple perspective is that a core or adjacent innovation may help reinvigorate the core business by using it as a “landing pad” (to house, integrate, and operate the new business). However, to meaningfully unlock value, a transformational innovation may require the creation of a new business—a “launch pad” with a clear financial perimeter—that, though loosely linked to the core, may be housed in a separate entity that can be valued by markets independently of the legacy core.

We suggest that automotive companies look at externally sourced assets through a “landing pad”/ “launch pad” lens to determine how to approach the integration process. Companies should consider the trade-offs involved in either integrating the target into the core business—thereby determining how the acquired capabilities will operate after they become part of their core business—versus setting up the target as a separate business entity with its own distinct culture—thereby making it easier to strategically adopt the target’s capabilities without disrupting the legacy business. Each type of integration has its own well-defined success factors (figure 3).

Examples of recent actions by automakers include:

- Investment (“launch pad”): In June 2018, Toyota Motor Corporation announced a US$1 billion investment in Singapore-based ride-hailing service Grab. The investment provides access to Grab’s mobility data, which will benefit Toyota as the company continues its transformation from an asset producer into a mobility provider.1

- Partnership (“landing pad”): In October 2018, Honda and General Motors announced a partnership in which Honda will invest US$2.75 billion in General Motors’ efforts to develop autonomous vehicles. The investment will take place over 12 years, with a global deployment of autonomous fleets as the end goal.2

- Acquisition (“launch pad”): In 2017, Ford Motor Company acquired Argo AI to bolster its artificial intelligence capabilities. The acquisition gave Ford access to Argo’s robotics capabilities and startup ethos to bolster Ford’s autonomous vehicle development.3

Creating value

Successful enterprisewide change requires agility, something that many established companies—with their deep-rooted business models, hundreds of thousands of employees, and global operations—find hard to achieve. But to master change and successfully operate in new places with new partners, automakers should rapidly adjust their core to be able to work with new ecosystems. They also should remain open to changes created by the future of work, and they should get comfortable with the idea that the core may—almost inevitably—need to absorb new capabilities.

If managed correctly, acquiring (or collaborating with) the right talent, culture, and technology can jump-start a company’s innovation mindset. However, the reverse can also happen if the integration is forced and not effectively managed. To be successful, it can be critical to break down hardened silos so that the M&A, strategy, business development, and human resources teams can collaborate to execute the business case that prompted the collaboration in the first place.

Most importantly, to gain value from transformative talent and technology, automakers likely need a coherent model for how the acquired capabilities will operate after they become part of their core business. Typically, how to operate a new asset is rarely given as much thought as how to value and extract cost synergies, which we view as a mistake. Companies should solidify the new operating model before engaging in partnerships, acquisitions, and alliances, because given the significant capital requirements of being a leader in the new ecosystem, waiting until after the deal is announced or concluded could be risky. This approach is radically different than the typical merger integration approach of cutting costs, closing plants, and rationalizing operations. It can require a keen focus on growth, employee retention, and maintaining progress in developing (relatively) unknown technologies and business models.

Another critical success factor can be the courage to admit failure, cut losses, and move on when necessary. After all, the vast majority of startups fail, and the vast majority of new business models never take off.4 Automakers investing in the new mobility ecosystem should realize that a significant number of their bets will likely fail—but they should focus on learning as much as they can from the failures and adjust their organization’s capabilities and culture going forward.

It’s a complicated new world for automakers, their boards, and their executives. Strategy, M&A, and HR leaders are typically more important to success than at any time in recent memory. To remain competitive, automakers should engage with, and take advantage of, the new ecosystem of both old and new industry players. Some key considerations include:

- Make sure that the company participates, which includes having a presence or strategy, in the industry’s emerging ecosystems. The board and executives should decide what they want the company to be in the future, measure progress toward that vision, and revisit their goals regularly.

- Take stock of the ecosystem to determine which key players should be collaborated with, partnered with, or acquired outright to accelerate the path to the future. Companies should pursue new alliances and be prepared to both succeed slowly and fail fast.

- Get the organization ready for change before it happens. Don’t wait until the capital is deployed and the deal is made. Be ready to embrace new collaborators, skills, digital DNA, and alliances by determining the desired operating model in advance.

Services

Deloitte’s global automotive team helps automotive companies execute innovative ideas in exceptional ways. We offer a global, integrated approach combined with business and industry knowledge to help our clients excel anywhere in the world.

Deloitte’s dedicated M&A professionals have been serving corporations and private equity investors for more than 30 years. Our breadth of experience and industry insight enables us to deliver value-added services, from strategy and execution through integration and divestiture.

Get in touch

- Marc Holzer

- Partner

- Deloitte Advisory LLP

- mholzer@deloitte.com

- +1 415 783 5496

© 2021. See Terms of Use for more information.

Related content

Explore the Future of Mobility

-

Future of Mobility Collection

Future of Mobility Collection -

The future of mobility: Ben's journey Video8 years ago

The future of mobility: Ben's journey Video8 years ago -

The future of freight Article7 years ago

The future of freight Article7 years ago -

The future of auto retailing Article9 years ago

The future of auto retailing Article9 years ago