Front-burner trends in commercial real estate, early 2025 edition: All eyes on tax policy

How the Trump administration's proposed tax policy changes could impact the commercial real estate industry

Elections inevitably hold both promise and peril for business leaders, and commercial real estate is no different. In a mid-2024 survey of US real estate managers, investors, and advisors conducted by PERE, nearly 90% of respondents said that results from the 2024 election would impact the real estate industry, and 75% thought it would directly affect their businesses.1

The policy positions of the new Trump administration could have a major impact in reshaping the macroeconomy. Key pieces of the Tax Cuts and Jobs Act (TCJA) of 2017, the signature tax legislation from the first Trump administration, are set to expire by the end of 2025. With Republicans in control of the House, the Senate, and the White House, the odds improve that those provisions will be extended, but that effort is not without its own challenges. President Donald Trump hopes to renew and enhance the TCJA2 and has proposed other tax-related policies. These plans, if enacted, could have near-term impacts on the real estate industry’s financial performance, not only in the United States, but globally as well.

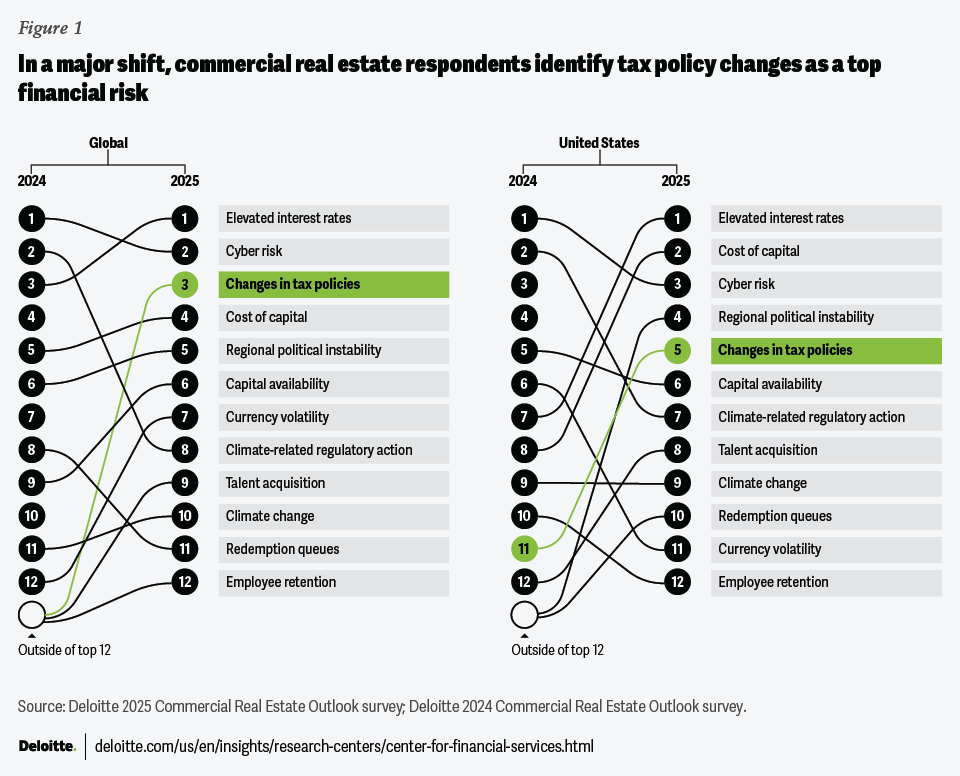

Now, all eyes are trained on tax policy as commercial real estate (CRE) leaders prepare their organizations for what may come next. In Deloitte’s 2025 commercial real estate outlook, nearly 900 global C-suite level survey3 respondents and their direct reports at CRE owner and investor organizations identified changes to tax policy as the third greatest macro concern for 2025, jumping from the 14th position the year before (figure 1).4 Among US respondents, tax concerns jumped from 11th to fifth, the second largest year-over-year change behind concerns about elevated interest rates.

CRE leaders are likely focusing more on tax policies in 2025 for three main reasons. First, Pillar Two, the 15% global minimum tax, continues to be implemented in many jurisdictions in 2025.5 Second, about 80 countries held elections by the end of 2024; collectively, these outcomes may hold long-ranging implications for fiscal policy.6 Third, with key pieces of the US tax code expiring at the end of 2025, there is a strong likelihood that major tax legislation will move through Congress this year.

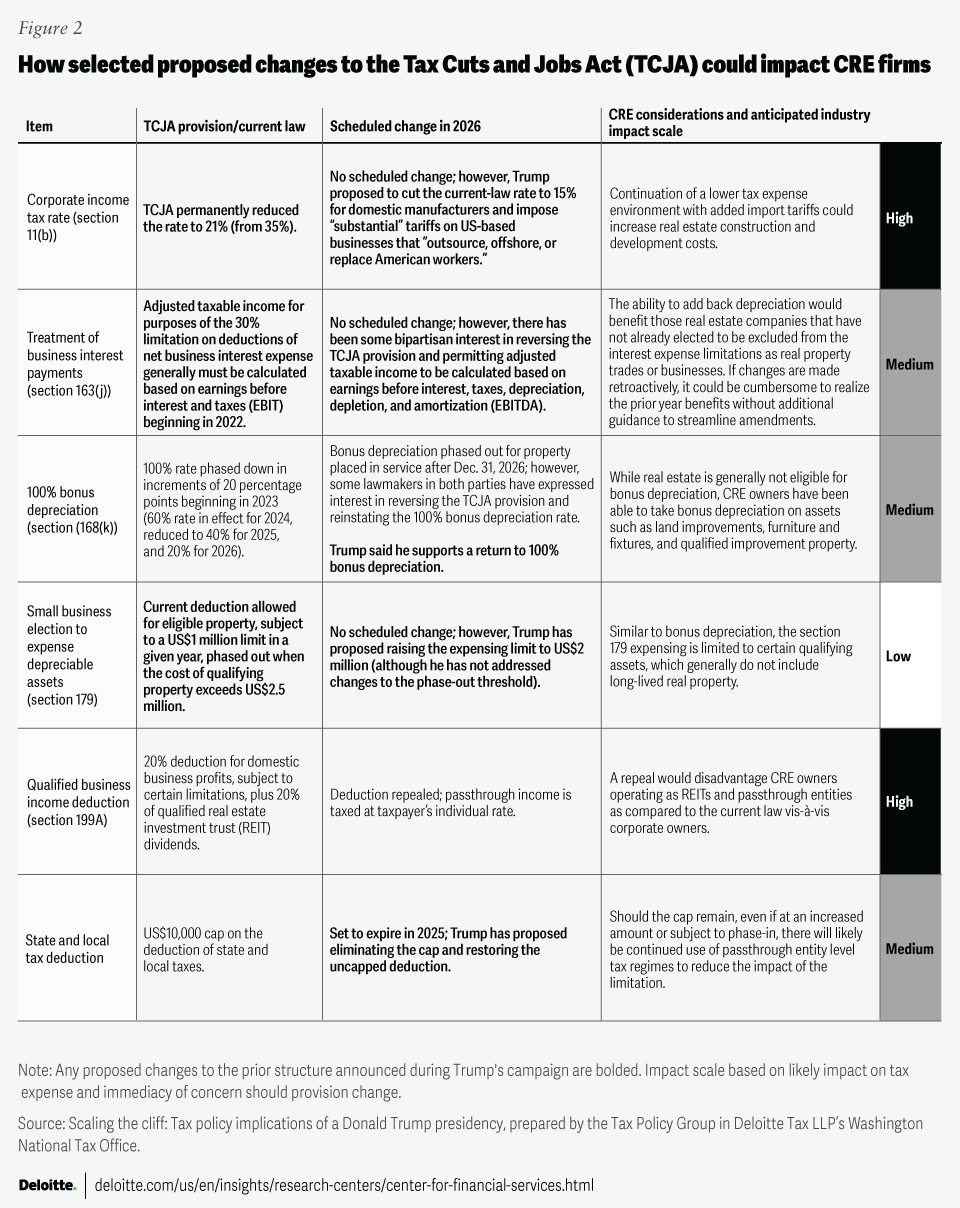

A recent Deloitte Tax Policy Group publication outlined the many provisions of the TCJA that are due to expire at the end of 2025. Unless Congress intervenes, pre-TCJA provisions will again take effect in 2026. During the presidential campaign, Trump expressed support for extending the TCJA and promised to expand and revise the law (figure 2).

Beyond provisions of the TCJA, commercial real estate leaders should also be aware of other policy provisions that could change or expand during the second Trump administration. Below are some of the major potential policy shifts and key questions that would need to be explored:

- The introduction of tariffs. On the campaign trail, Trump called for tariffs ranging from 10% to 25%, with some select cases even as high as 100%.7 To what degree will these tariffs be rolled out—which categories of goods and which trade partners will be impacted? Will there be exemptions? How might these tariffs impact prices and inflation for real estate companies?

- The enforcement of Pillar Two. While not signed into US law, multinational organizations headquartered in the United States could still face top-up levies, the difference between the 15% minimum tax and the effective tax rate,8 in jurisdictions that have enforced Pillar Two.9 There are considerable open questions about how the rest of the world will proceed with Pillar Two following two related executive orders signed by President Trump on his first day in office. These executive orders indicate the US may raise taxes or take other retaliatory measures on nations that impose taxes on US taxpayers that are deemed to be discriminatory or extraterritorial.10 Will the rest of the world change plans with respect to Pillar Two? What sort of retaliatory measures might the US take if other countries proceed with Pillar Two implementation? How might the rest of the world respond to such retaliatory measures?

- Sustainability credits and incentives. Many clean energy and energy efficiency credits and incentives were enacted or expanded as part of the Inflation Reduction Act of 2022. Could some of these incentives be modified or scaled back in the future? To what extent will modifications impact real estate companies?

- The Opportunity Zones program. Trump enacted this program during his first administration to spur investment and development in economically distressed areas in the United States.11 How could this program be extended or expanded?

The above provisions could impact the health of the macroeconomy, existing CRE business operating conditions, or even the planned path of the Federal Open Market Committee (FOMC)’s rate cutting cycle, a catalyst for further recovery for CRE capital markets.12 Post-election, Deloitte economists expect the Federal Reserve’s target rate range will be between 3.75% and 4% by the end of 2025.13 In our baseline scenario from the end of 2024, potential tariffs could raise inflation enough to force the FOMC to pause rate cuts until mid-2027.14

Maintaining CRE industry recovery momentum through the transition

While much about what a new administration might enact is still unknown, tax policy will be an immediate priority for legislators in 2025 with the expiration of key components of the TCJA on the horizon. To maintain the recent recovery momentum and mitigate potential business disruptions, leaders in commercial real estate can prioritize the following:

- Stay focused on long-term growth. Commercial real estate investment priorities could outlast the spans of several presidential administrations. Leaders should continue to have a long-term growth horizon for portfolio performance. Looking at sales activity, leasing, or total returns, there is no direct correlation between CRE industry performance and election results regardless of party.15

- Stay informed about the latest developments on Capitol Hill. There are no guarantees around whether, to what extent, or when proposed changes could be enacted.

- Plan proactively. Developing scenario plans for what might become law could help real estate firms avoid potentially costly surprises.

{kind=link}

{kind=link}