Climate change impacts elevate US commercial real estate insurance costs

The CRE market is expected to face rising premiums, especially in states most vulnerable to extreme weather. What can owners do to help protect themselves and their properties?

Atmospheric rivers. Superstorms. Cold waves. Wildfires. These are just a few of the extreme weather events that have impacted regions across the United States over the past few years. Due to its location and topography, population growth and development in climate-vulnerable areas, and the growing impact of climate change, the United States leads the world in extreme weather catastrophes.1

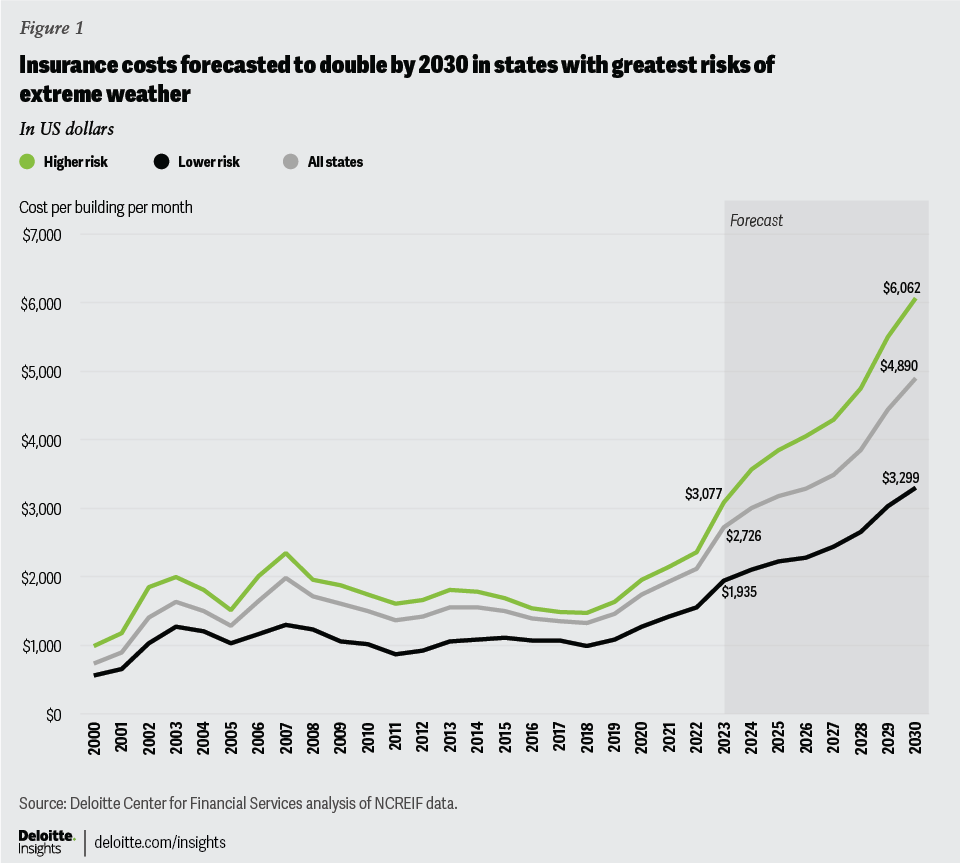

The insurance industry is responding to the proliferation of extreme weather events and the risks associated with operating commercial buildings in vulnerable areas by increasing premiums. The Deloitte Center for Financial Services projects that the average monthly cost of insurance for a commercial building in the United States could increase from US$2,726 in 2023 to US$4,890 in 2030, at an 8.7% compound annual growth rate (figure 1). For states with the greatest extreme weather risk, current costs of US$3,077 could almost double to hit US$6,062 per building per month, a 10.2% CAGR by 2030. Among states at lower-risk levels, current insurance costs of US$1,935 per building per month could rise at a 7.9% CAGR to US$3,299 by 2030.

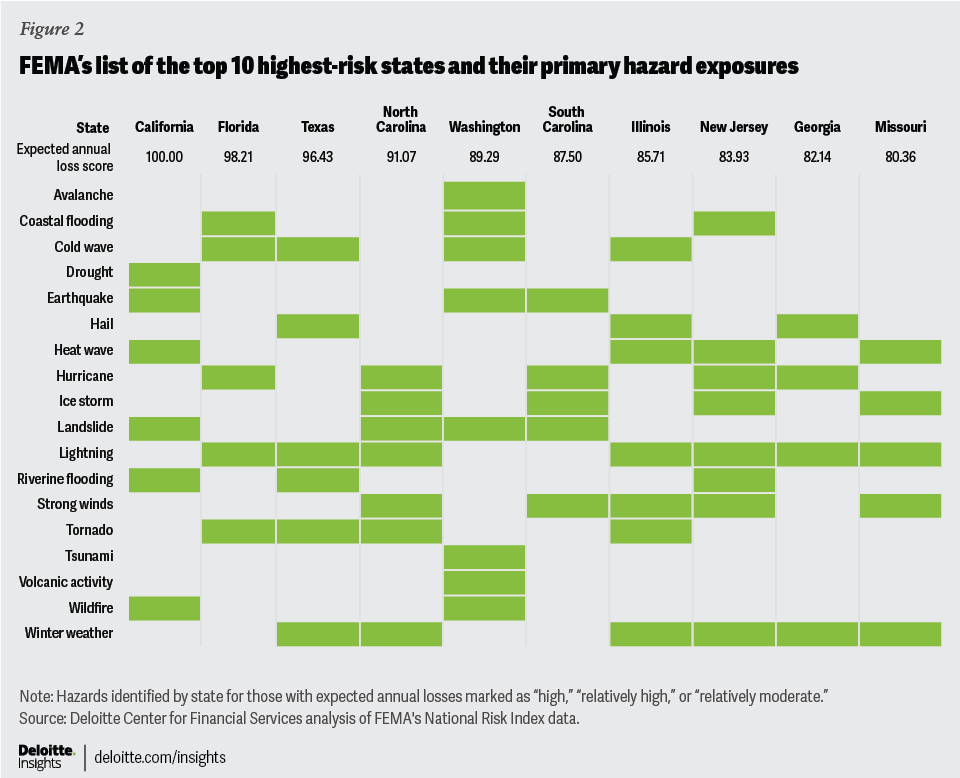

Commercial buildings located in states with the 10 highest expected annual loss (EAL)2 totals according to Federal Emergency Management Agency (FEMA), based on their exposure to natural hazards, have seen a 31% increase in insurance costs year over year and 108% increases over levels from five years ago.3 This compares to 25% and 96% increases, respectively, for states outside of the top 10 (figure 2).

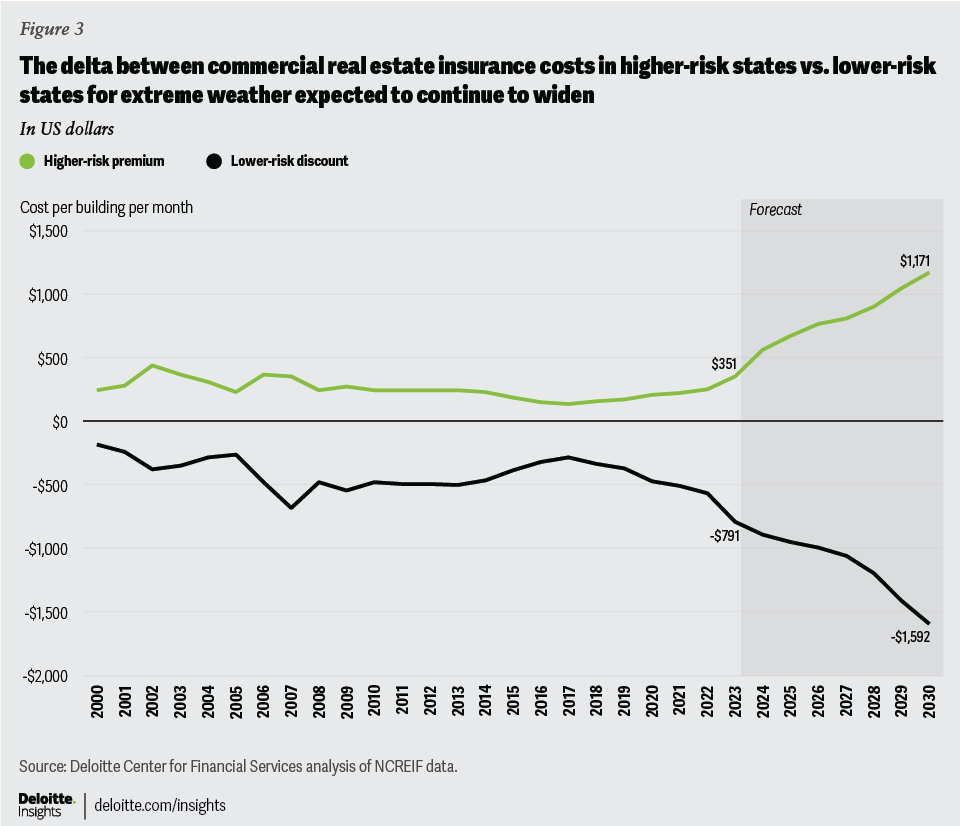

By 2030, the cost premium of being in a higher-risk, extreme weather state could be 24.0% greater than the national average, compared to a 32.5% discount in lower-risk states (figure 3).

What's behind the hardening cost of insuring commercial real estate?

Average insurance costs for commercial real estate properties across the industry have nearly doubled over the past decade, from US$1,558 per building per month in 2013 to US$2,726, a compound annual growth rate of 5.75%, by the end of 2023.4 The proliferation of extreme weather events across the United States has been a contributor to these increases. This added risk has caused certain insurers in some states to reduce coverage or vacate altogether.5

Insurers have also been playing catch-up from increased losses in recent years. For more on the impact of climate-related risks on personal property insurers, read our climate change and home insurance prediction. Coming out of 2020, the lingering effects of the COVID-19 pandemic along with emerging issues, such as rising inflation and interest rate uncertainty, likely influenced pricing reassessments. From the first quarter of 2021 through the fourth quarter of 2022, US property insurance premium growth rates trailed the pace of inflation growth for eight consecutive quarters.6 In 2023, that relationship flipped: Insurance premium growth rates, those imposed by providers, outpaced inflation through three of the first four quarters. Central bank efforts to tame inflation have so far proven positive, dropping monthly core inflation growth (less food and energy) from as high as 6.5% year over year to closer to 3.1% in early 2024.7 As inflation and rate uncertainty soften slightly, the lasting impacts of extreme weather will likely remain as a driver for continued pricing growth for the near future.

In 2023, there were 28 separate billion-dollar extreme weather events with estimated recovery costs totaling US$92.9 billion, exceeding the records for both count and cost from 2020.8 These included 19 severe storm events (tornadoes, high winds, and hailstorms), four flood events, two tropical cyclones, one wildfire event, one winter storm and cold wave, and one drought and heat wave. In total, these events accounted for a 56% increase from 2022, and up 180%, or a compound annual growth rate of 10.8% per year, from levels 10 years ago. Assuming a similar annual trajectory, there could be as many as 42 separate billion-dollar extreme weather events annually by 2030.9

About this prediction

Insurance cost forecasts were created using comparable historic compound annual growth rates from 23 years of available property insurance expense data from commercial properties within the National Council of Real Estate Investment Fiduciaries (NCREIF), in conjunction with 20 years of historic growth patterns for billion-dollar extreme weather event cases from the National Oceanic and Atmospheric Administration National Centers for Environmental Information. NCREIF sample data consists of over 50,000 buildings across geographies and property sectors from contributions by member organizations. States were excluded from this analysis if they did not meet sufficient building counts of at least 15 properties over an average five-year period. Thirty-one states qualified via this criterion.

Strategies to consider in helping to protect properties and mitigate rising costs

Building owners can explore several approaches to help protect their investments and help mitigate rising commercial property insurance costs. To thrive they may look to adapt to volatile market changes with the help of tailored sector-specific insights.

First, they should explore prevention measures they can take themselves. These include conducting regular risk assessments—or, for those who already do this, they could do these assessments more frequently to help inform decision-making and keep pace with the rise in weather-related events. Commercial real estate owners can also focus on enhancing security and monitoring measures, such as cameras, access control, flood monitors, and fire prevention tools, to better protect their properties.

Brokers and advisors can play a key role in helping owners anticipate and even reduce costs. Owners can work with their broker or advisor to discuss policy renewal options well in advance of deadlines to help level-set pricing expectations for the road ahead. Brokers and advisers can also help CRE owners find cost savings opportunities or more competitive pricing since many have negotiating power with insurers—assuming insurers are still supplying the immediate vicinity. Brokers and advisors can also avail owners of any resiliency efforts and discount programs insurers may offer.

For some CRE owners, self-insurance may be worth exploring to have greater control of their insurance costs and coverage options. By setting up a captive insurance company, CRE owners can improve their own purchasing power and gain direct access to the reinsurance and alternative capital markets, which could reduce the impact of volatility from both a price and availability perspective through traditional insurance channels. Having greater access can help owners better stabilize their risk financing over time and optimize risk retention based on market cycles.

Finally, location-agnostic owners and investors can consider relocating some or all of their properties. In some circumstances, relocating can help reduce risk exposure to extreme weather or gain access to insurers who no longer service certain regions in the United States. When making relocation decisions, owners and investors should ensure they or their insurer are using the most updated peril risk maps. For example, historical wildfire risk maps are becoming obsolete due to changes in climate and environment, and government agencies are increasingly relying on satellite imaging and AI technology to map risk zones more dynamically.10 Understanding the current and future location risks can be vital to making informed relocation decisions.

The links between climate change, the proliferation of extreme weather, and the rising costs to insure commercial real estate will likely remain for the foreseeable future. But owners have viable options to consider in helping to stem the tide and ensure that their buildings can withstand the elements and help keep their bottom lines afloat. By availing themselves of the latest insights, and by targeting the right solutions, owners adapt, and even gain a competitive advantage, in this time of extreme transformation.

{kind=link}

{kind=link}

{kind=link}