In-app payments should take social commerce to the next level

As social media platforms gear up to support consumers’ shopping journeys from discovery to checkout, payments firms can help deliver safer and more convenient experiences.

Zachary Aron

Ravneet Randhawa

Richa Wadhwani

Val Srinivas

Social media platforms such as Facebook, Instagram, YouTube, TikTok, and Snapchat have increasingly become the new “storefronts,” where consumers can not only discover new products but also buy them.1

Until recently, such shopping experiences involved a limitation: breaking up the customer experience. While many social commerce platforms in the United States introduced native checkout capabilities, where shoppers can pay for their purchases within the app, they often acted as marketing channels, directing consumers to merchants’ websites to complete the transaction and pay for the purchase (see sidebar, “Blurring the lines between social commerce and e-commerce”).

These platforms are now recognizing an opportunity to direct more payments through their native checkout experience and keep shoppers within their ecosystem. For instance, beginning April 2024, Meta will require all Meta Shops merchants in the United States to use Checkout on Facebook and Instagram2 to provide an end-to-end discovery and shopping experience. The benefits of bringing payments in-house for social platforms include: 1) access to customers’ transactional data for richer insights, with additional opportunities to monetize this data in the future; 2) new transactional revenue on payments processed; and 3) the potential to offer complementary financial products, such as cash advances. The merchants, too, benefit from a wider reach to millions of social shoppers, stronger analytics due to more immersive customer experiences, and faster cart conversions.

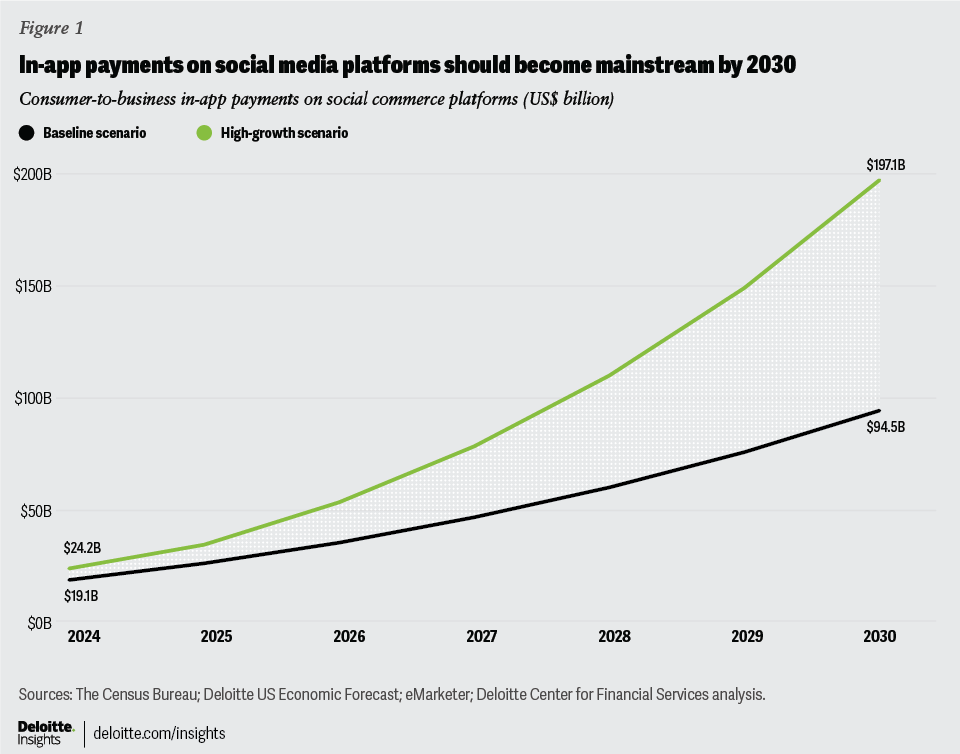

The Deloitte Center for Financial Services predicts that in-app payments on social media sites could grow at a compound annual growth rate (CAGR) of about 30% from US$19.1 billion in 2024 in the United States to US$94.5 billion in 2030 (figure 1). Additionally, in-app payments could constitute as much as one-half of overall social commerce payments by 2030, emerging as a dominant shop-and-pay model. In a high-growth scenario, Deloitte expects these in-app payments could increase at a CAGR of 42%, to US$197.1 billion by 2030 (see “About this prediction” for our methodology).

Blurring the lines between social commerce and e-commerce

According to a 2023 Deloitte article, many "US consumers use social media platforms to view product recommendations from creators, make purchases directly on the platform or through a link, and get inspiration for future purchases. This shopping experience on social media is known as social commerce.”3

By integrating shopping, social platforms have entered the space long dominated by e-commerce portals. In turn, US e-commerce players are also embracing some social capabilities to make shopping more interactive and engaging. For instance, in 2022 eBay launched a beta version of eBay Live—a dedicated shopping portal to discover and buy products in an interactive format.4

While some may have expected heated competition, e-commerce and social commerce platforms are demonstrating healthy co-opetition to mutually benefit from changing consumer behavior. In 2023, Amazon entered into separate partnerships with Snap and Meta to allow consumers to buy select Amazon products directly in their social feed using their Amazon checkout credentials (shipping and payment details).5

In addition to payments, social platforms can learn from their e-commerce counterparts in owning customers’ journey and becoming the be-all and end-all shopping destination. While this ambition often includes native checkout capabilities, it can also entail having seamless processes for shoppers to earn loyalty points, track purchase orders, initiate hassle-free returns, request refunds, report fraud, and raise chargeback disputes.

How could payments firms influence the future of in-app social commerce payments?

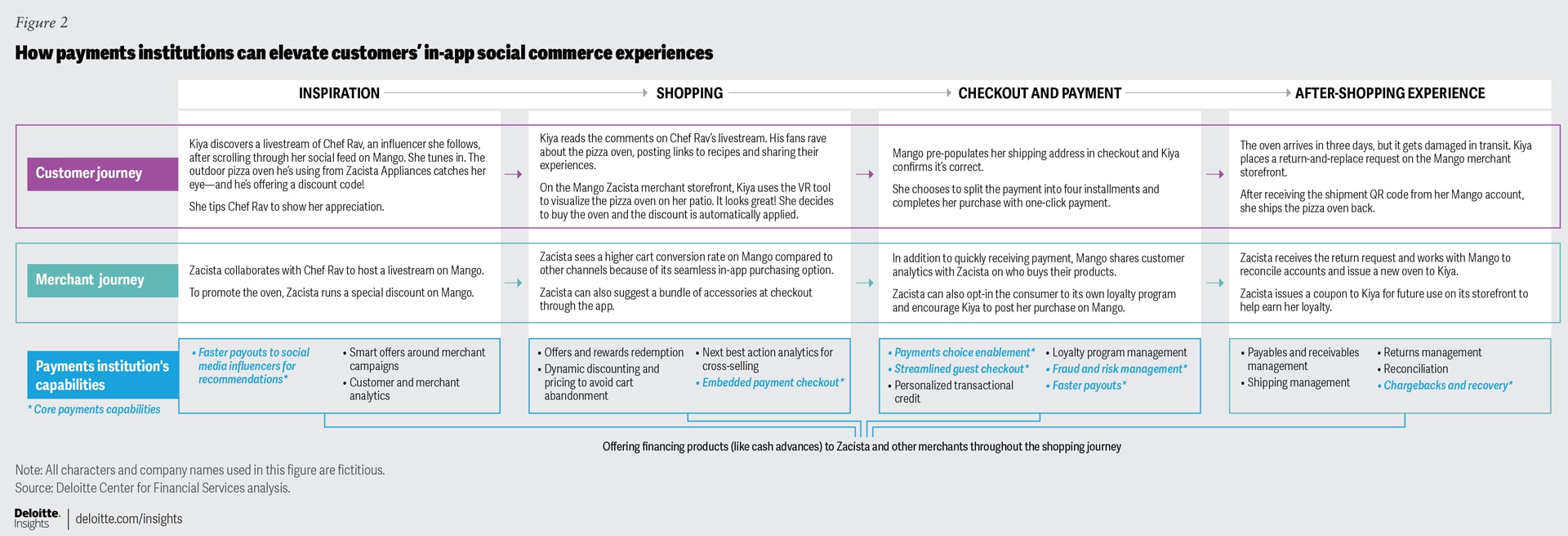

Payments institutions, which include card issuers, networks, merchant acquirers, and payment facilitators, can influence the future of social commerce payments by adding value throughout the customer shopping journey (figure 2). Even more important, in the future, the lessons of enabling in-app payments capabilities on social platforms could be applied in other shopping formats to provide secure and convenient, in-context customer experiences.

Payments firms can partner with social media platforms to help them achieve the following goals:

1) Secure payments and identity protection. Consumers today expect brands and platforms they interact with to be respectful about their data privacy, and transparent about how their data is managed and, if they’ve given due consent, shared with other companies.6 But social platforms have lagged in winning customer trust: According to the 2024 Edelman Trust Barometer, social media is the least trusted industry.7

The rise in social media shopping scams could have further contributed to this lack of trust. Scammers can manufacture fake identities from shoppers’ social profiles and hack into consumers’ accounts. A 2023 Federal Trade Commission study suggests that US consumers reported about US$216 million in fraud losses originating from social media commerce between 2021 and mid-2023.8 Perhaps more alarming, of all the social media scam reports filed in the first half of 2023, 44% were from consumers who tried to buy something marketed on social media.9 Generative AI may further boost such fraud in the future. (See our prediction on generative AI-fueled fraud.)

Social platforms should elevate their game in fostering digital trust with privacy, transparency, and redressability (the possibility of obtaining recourse when harmed by malignant forces) as key tenets. For customers to become comfortable making in-app payments, platforms should collaborate with payments institutions to enable secure shopping experiences. For instance, payments firms can use their AI and machine learning algorithms to generate behavioral patterns and a 360-degree view of customers from their offline and e-commerce transactions to help platforms detect fraudulent and synthetic identity transactions. Moreover, with the advent of open banking, payments institutions can play a significant role in data sharing and collaborating with social platforms to help authenticate identities and prevent illicit solicitations of money from fake accounts or threat actors.

2) Frictionless payments with optionality for consumers. Most shoppers engage on social media on their smartphones, not on a PC, so a seamless checkout and payment process is generally a baseline expectation. Features like one-click payment could make in-app social commerce payments not only frictionless, but also invisible.

Additionally, consumers may want the option to pay with both traditional and alternative payment methods, including digital wallets, cryptocurrencies, and buy-now-pay-later financing products, like they have in online and in-store shopping. In this regard, social platforms have already or are partnering with payment facilitators, who have well-established one-on-one integration with traditional and alternative payment methods.10

However, given greater optionality, how can card issuers become the preferred method for contextual, in-app payments while presenting most optimal choices on a six-inch smartphone screen?

Card issuers could offer exclusive loyalty rewards or launch co-branded cards to position their cards as the preferred choice (directly or via digital wallets) for in-app transactions on social platforms. They can also integrate value-added features, such as dynamic pricing and tailored rewards based on customer lifetime value, automatic points redemption, and loyalty program management, to differentiate their positioning and become the top choice for social shoppers’ in-app purchases.

3) Faster settlement with additional financing options for merchants. In-app payments are expected to improve the conversion rate not only for brands and merchants, but also for content creators who value getting paid quickly. Payment facilitators and networks can help with this piece of the puzzle and enable social platforms’ transition from earners to payers. For instance, Visa offers products and partnerships that enable faster payouts because content creators are paid directly.11

Additionally, small and midsize businesses (SMBs) and content creators may also appreciate integrating features, such as cash advances and the flexibility to draw funds without having to accumulate a significant balance. With in-app payments, social platforms could have a 360-degree view of merchants’ performance on their marketplace, including their sales records, inventory positions, cash flows, and even customer feedback. This data should empower social and payment platforms to support each other and offer financing products beyond payments, as some e-commerce platforms do. For instance, Amazon launched a cash advance program for SMBs on its platform in November 2022,12 allowing them the flexibility to repay as they earn on its marketplace.

Drafting the blueprint for the broader shoppable media landscape

Shopping will potentially integrate in consumers’ day-to-day digital interactions at a breakneck pace in the next few years. A 2023 Deloitte article summed it up: “This expanded commerce experience, which is known as shoppable media, will make use of interactive content across any media—not just social platforms—to encourage consumers to make a direct purchase and enable them to buy instantly.”13 From streaming video on-demand services to shopping for outfits in the metaverse, any and every media content consumed may already be or is becoming “shoppable.” For instance, the Walmart debut romcom Add to Heart 23-part video series integrates 330 shoppable products, creating a new channel for the brand to connect with and sell to consumers through content.14

Payments institutions should collaborate with media companies to enable in-context secure transactions and integrate more value-added features to elevate the customer experience.

Additionally, the in-app payments capabilities that payments institutions champion in social commerce could migrate to other shopping formats and make consumers’ overall experiences more seamless and secure. Payments firms can play the long game and apply many of the lessons and capabilities from social commerce to alternative platforms, including subscriptions on-demand (such as video), augmented reality, or the metaverse. Are they ready?

About this prediction

Deloitte’s Center for Financial Services in-app social commerce payments prediction uses macroeconomic variables, such as US personal disposable income and US total retail and e-commerce sales data between 2000 and 2023, to forecast social commerce dollar transaction volumes through 2030. Our research and technical discussions with Deloitte payments specialists helped build two scenarios for the percentage of in-app social commerce payments. Applying these percentages to the forecasted social commerce volumes yielded us the in-app social commerce dollar payments volume from 2024 to 2030.

{kind=link}

{kind=link}