Private capital innovation: Using artificial intelligence can accelerate the portfolio valuation process

More frequent portfolio company valuations may open doors for new private equity investors and enhance transparency in portfolio management.

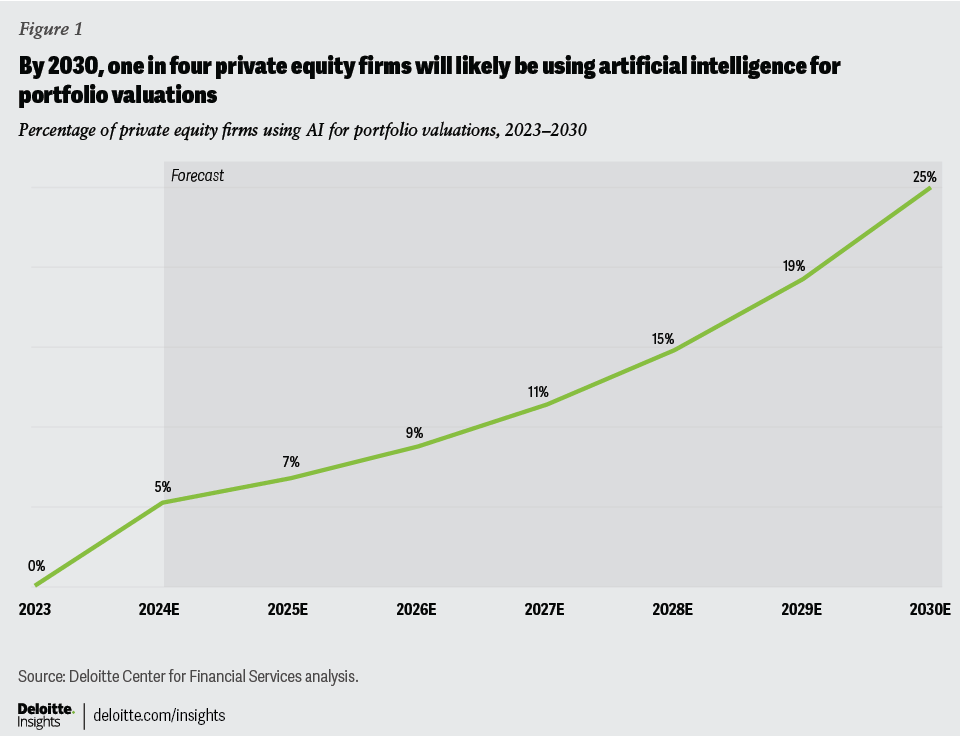

As advanced technologies, particularly artificial intelligence, continue to improve, private investment firms have an opportunity to rethink—and transform—how they value their portfolio holdings. By the end of the first half of 2023, less than 10% of private funds had implemented AI in core functions.1 Over the next five to seven years, Deloitte predicts that as many as 25% of private equity (PE) firms are expected to be using AI to augment their portfolio valuations (see “About this prediction” for more on our methodology). Artificial intelligence will likely help increase the frequency of portfolio valuation (figure 1).

About this prediction

By the end of 2023, about 10% of private investment firms started to use AI-based solutions for relatively complex tasks such as identifying investment opportunities, research, deal sourcing, contract management, and due diligence. Based on adoption curves for recent technological advancements, the percentage of firms using AI for similar-intensity applications is estimated to grow at least at a 30% compound annual growth rate for the next five to seven years. Deloitte estimates that each year, about 40% of firms that use AI for complex tasks are expected to also use AI for higher-intensity tasks, such as portfolio valuations.

AI can help firms open private capital to retail investors with transparency

In recent years, regulators across the globe have taken action to broaden private market access to retail investors. For example, the US Securities and Exchange Commission (SEC) relaxed its definition of accredited investors to include knowledge-based qualification in addition to wealth and income-based qualification routes, while the European Commission recently reduced barriers to retail investor participation in private markets through amendments to the European Long-Term Investment Fund rules.2

The regulatory trajectory is also moving in the direction of more disclosures and transparency. The SEC recently passed rules for private fund advisers that, among other things, increase compliance requirements for performance reporting, event-based reporting, and audit reporting.3 Meanwhile, the International Organization of Securities Commissions, a global securities forum, recently pointed to stale valuations as one of the factors that pose a significant risk to the financial system.4 The EU’s European Securities and Markets Authority and the United Kingdom’s Financial Conduct Authority have issued statements on these issues as well.5 As regulators dive deep into the private markets, regulations should continue to evolve. More frequent, AI-powered valuations could help firms stay ahead of compliance and reporting requirements.

While the high returns, resiliency, and diversification benefits of private investments attract investors’ interest in the asset class, some have been deterred by PE’s lack of transparency and low liquidity. Having more frequent valuation may lead to greater transparency, which should make private capital more attractive for new retail investors as well as current private capital investors. The increased transparency could also make secondary transactions more efficient and scalable. Industry regulators will likely favor more frequent valuation as they consider opening the asset class to retail investors.

While some private investment firms value portfolio holdings more frequently, many still perform valuations quarterly. Given the timing of information from portfolio companies, there’s also an inherent lag of weeks to months for the financial data of portfolio companies considered in the valuation models. This time-consuming valuation process is one reason private capital is considered an opaque asset class. Detractors of the PE industry also maintain that lags in the valuation process contribute to systemic risk due to stale pricing.6

Most portfolio companies report their financial data to general partners at least quarterly. For many, structured and unstructured nonfinancial key performance indicators, such as subscription data, shipping data, app usage data, hiring data, and foot traffic data are available on a more frequent basis. Traditional and generative AI tools can ingest and process this nonfinancial data, along with the latest news and industry updates, to modify valuation assumptions and parameters. Incorporating these updates in a timelier manner into the valuation model may help firms arrive at a more holistic valuation based on more frequent data inputs in addition to periodic financial data.

Some private investment firms are already using AI for investment discovery and deal sourcing.7 For these firms, a natural next step could be to pivot these capabilities from pre-deal processes to post-deal processes and incorporate AI into portfolio management, which includes portfolio valuations.

As retail access to private investments becomes more democratized through a combination of AI-enhanced operational changes and more regulatory support, general partners may attract more committed capital from the expanded retail investor segment. Even if general partners are not required to report their valuations more frequently, they may benefit from additional capital earned through having greater transparency and more frequent valuation.

AI-based valuations could also yield additional key benefits

A higher frequency of portfolio valuation can help mitigate issues arising from the denominator effect, where a valuation drop in one asset class can make the other asset classes appear overallocated, triggering portfolio rebalancing. Many institutional limited partners, such as pension funds and sovereign funds, have allocation limits for asset classes like private capital. In a bearish market, private investment valuations may remain unchanged for a longer duration than frequently traded securities. Unchanged, time-lagged valuations can make institutional LPs appear to be overallocated to private capital. This denominator effect can also lead to selling private investments in secondary markets, which tend to be less efficiently priced than active public markets. In addition to reducing the need to sell, having more transparency may also encourage more buyers to enter the market, which would likely reduce the bid-ask spread on the secondary market.

An up-to-date valuation could change this picture. AI-based frequent valuations may benefit institutional LPs by allowing them to avoid potentially unnecessary denominator effect-driven secondary transactions. More frequent valuations may also help satisfy limited partners’ desire for more information about investments and performance.8

However, introducing AI into the valuation process will likely also introduce model risks, cybersecurity risks, and other AI-related risks in the system. If firms don’t have proper controls and oversight in place, AI issues can lead to financial penalties or reputational damages. The SEC is exploring how investment advisers are using AI in developing marketing materials, algorithmic models, and compliance training.9 Self-regulation and following industry-leading practices will likely be a way forward to responsibly use an emerging technology in novel ways, such as with portfolio valuation.

Personalization, flexibility, transparency, and oversight will be critical to successful AI implementation

Increasing the frequency of portfolio company valuation could benefit not just retail investors, but also limited partners, general partners, and regulators. But many stakeholders will likely have concerns about the use of AI in the process. Addressing these stakeholder concerns could be important for successful implementation.

Below are some potential industry-leading practices.

- Customization: AI solutions should be customized to follow the investment principles and values of the private investment firm. The solution should be able to answer an analyst’s questions on valuations, including clarifications on parameters, adjustments, assumptions, risk, and methodology used. For example, the AI tool should be able to help an analyst understand why a particular comparable was included or dropped.

- Transparency: Providing more disclosure and transparency to limited partners could help appease concerns that a black box is taking over the valuation process. Providing valuation methodology transparently to limited partners will likely also help them become more comfortable with the potential for the higher volatility of frequent valuations, and in turn, could aid them in ongoing management of their portfolios including public and private investments.

- Compliance: To stay current and compliant, the AI model should be able to periodically check for the latest valuation guidelines, summarize them for human approval, and then incorporate any approved updates into the valuation process. Furthermore, the use of AI can bring added risks; firms may need additional control measures to be compliant.

- Training: It is important to ensure that AI applications are trained on a sufficient volume of diverse financial and nonfinancial data sets. This can help minimize data biases that may skew ongoing portfolio valuation results.

- Oversight: Although the AI-based valuation model can work independently, human oversight should be incorporated to ensure the model output is accurate and explainable, especially in the early stages. The AI solutions should be flexible enough for analysts to dive into the details of the valuation process and apply tweaks at any step, if required.

Responsibly using AI for frequent valuations should help alleviate many stakeholder concerns about lagged valuations without proportionally increasing resource requirements. Private investment funds that offer more transparency are expected to attract new investors who favor more timely information about the valuation of their investments. Private capital may no longer be considered an opaque asset class if it can achieve more frequent valuations.

{kind=link}