Driving purpose and profit through financial inclusion has been saved

Cover image by: Jaime Austin

The challenges created by the global pandemic and recent racial and social injustice events have increased awareness of inequities and financial instability across the globe. They highlight the need for financial institutions to make a global commitment to advance financial inclusion—providing access to useful and affordable financial products and services1 —to meet the needs of the underserved2 market.3 The Global Findex4 database shows that 1.7 billion adults worldwide are unbanked,meaning they donot participate in any basic financial products or services. In the United States, more than 30 million households are considered unbanked or underbanked5—they have limited access to basic financial products and services. Therefore, a range of opportunities exists for financial services providers to be a force for change.

Right now, financial industry leaders have an opportunity to endorse a meaningful and sustainable shift toward performing fundamental roles in more direct, personalized, and socially responsible ways. Doing so would not only demonstrate resilience in uncertain times; it would signal to stakeholders that financial firms place just as much value on safeguarding our planet and people as they do on making profits. By addressing the strategic business imperatives that serve the greater good through financial inclusion, financial leaders can make a decisive step toward achieving a higher bottom line.6

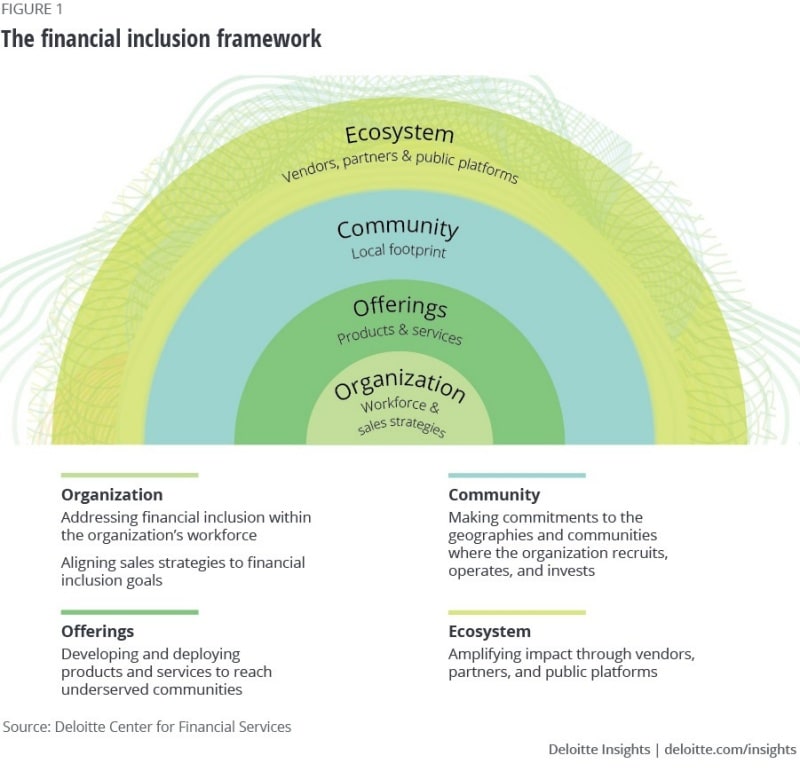

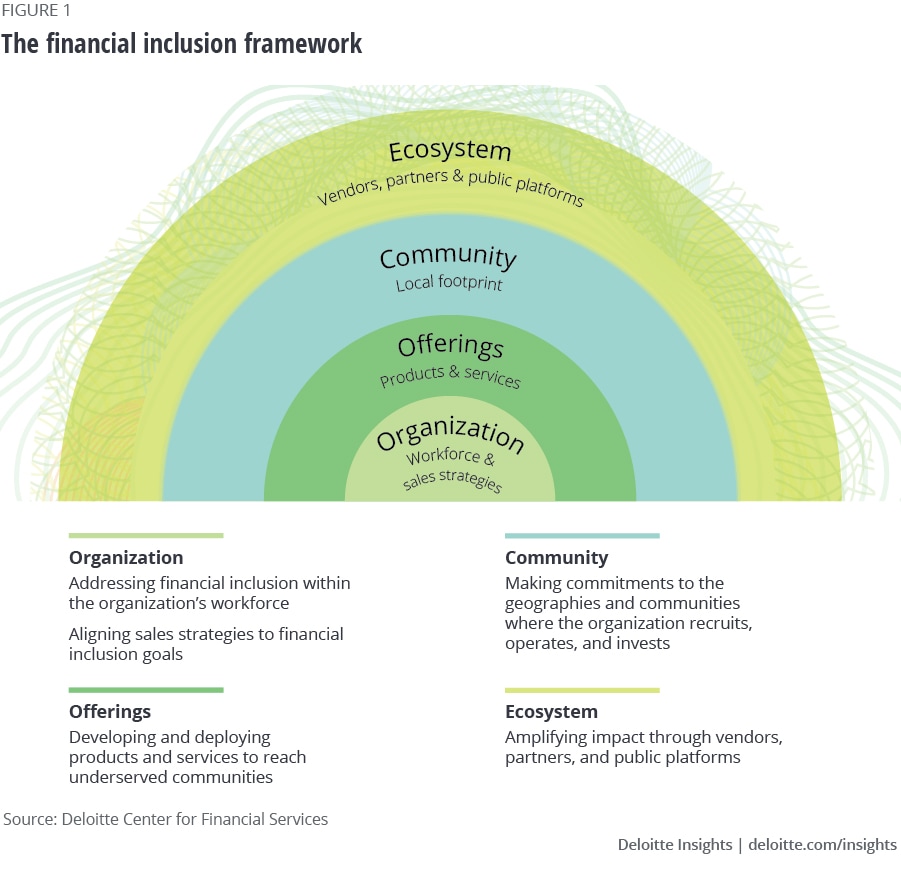

This is the first report in a series Deloitte has designed to assess and address the market landscape of financial inclusion. As a key part of this series, we have developed the financial inclusion framework (figure 1) to outline the drivers of change. The framework serves as a tool for financial services organizations to spark discussion across leadership teams and their stakeholders as they evaluate the progress they are making in their pursuit of purpose-driven, societal impact and profitable shareholder value.

Global C-suite surveys have shown that CEOs, when asked to measure and evaluate their business performance, ranked making a positive societal impact high on their list of factors.7 Creating positive social impact is clearly a worthwhile goal. But it is in how an organization devotes meaningful effort, time, and experience toward public well-being—its corporate social purpose8—where committed, sustainable change can be realized. While businesses have a responsibility to pursue profits for their shareholders and their organization, having a well-defined corporate social purpose can also build brand and reputation, attract and retain talent,9 and contribute to the betterment of the communities they serve. This, in turn, helps the firm appeal to socially conscious customers, promotes innovation, and stimulates opportunities for profitable growth by penetrating new market segments.

Sustainability; climate risk; diversity, equity, and inclusion (DE&I); ESG investing; and financial inclusion are important considerations in defining an organization’s corporate social purpose.

Financial inclusion usually falls within an organization’s corporate responsibility programs, and investments within that model have yielded some progress. For example, an ongoing study by the Federal Deposit Insurance Corporation (FDIC) shows that the share of US households deemed unbanked or underbanked remained static from 2009 to 2017. Within that trend, though, the number of unbanked households actually decreased by 600,000, while underbanked households increased by over 3 million. And the unbanked population continued to shrink, by another 1.3 million, from 2017 to 2019.10 Ultimately, industry leaders should transition from a mindset of financial inclusion being solely a responsible endeavor, to one that equates corporate social purpose with return on investment.

The financial inclusion framework (figure 1) enables leaders to assess and address their organization’s financial inclusion strategy across four dimensions: organization, offerings, community, and the broader ecosystem. Firms should evaluate the strategic, operational, and technological impact on an organization’s stakeholders—its workforce, customers, vendors, partners, and the external marketplace–within each of the four dimensions. This exercise can help leaders determine priorities, develop strategies, and forge new market relationships to move from strategy to action. To uncover unique competitive advantage, financial institutions should consider the issues broadly, while addressing them specifically within an organization’s financial inclusion strategy. They can achieve the highest potential benefits of financial inclusion when leaders address and align the four dimensions within their financial inclusion goals.

Organization

Addressing financial inclusion begins with assessing how an organization is supporting its own workforce through programs that advance financial literacy, and through DE&I and recruiting efforts that communicate organizational commitment to a diverse workforce. Organizations should also evaluate their operating models, which define sales strategies to reach underserved communities and businesses.

Studies show that employee concerns regarding their own financial challenges or financial health can negatively impact both productivity and performance.11 Meanwhile, companies that provide financial literacy programs report reduced health care costs and higher productivity among employees, due to lowered financial stress.12 One recent study on employee financial concerns reported that 70% of respondents ranked comprehensive financial wellness as a primary need.13 Firms that promote financial education internally often help employees manage student debt, plan their retirement and investments, assess their options for securing credit products, and understand how to manage their current finances to meet their financial goals.14

Shifting the focus to the external marketplace, sales strategies should enable expansion of existing products and services and be sustainable in the long term,to help achieve market growth and shareholder value. Measuring the growth of impact insurance and microinsurance for low-income households for more than a decade, the International Labor Organization reports at least 60 of the largest insurers now serve low-income and previously underserved global clients through inclusive insurance products.15 In 2005, only seven large insurers were focused on the underserved market. Growth and scale were achieved, in part, by bundling products, client-centric sales strategies, and leveraging distribution partners.16

Financial institutions should aim to develop sales strategies that promote entry and access for the underserved, coupled with a diverse financial services workforce—from strategy and investment decisions through to delivery of products and services. These can help ensure that the voice of the underserved customer segments, including race, gender, and education level, is represented.

Questions for financial leaders to consider:

How are we addressing financial inclusion among our workforce?

How is our organization recruiting and developing diverse talent?

What barriers to access are there for our services across different groups?

How are our sales strategies aligned to our financial inclusion goals?

Offerings

The underserved market spans the financial services industry. For underserved households and businesses, entry into a relationship with a financial institution typically begins with deposit accounts, payments, credit, or insurance products. According to the FDIC’s 2019 How America banks report, 7.1 million (or 5.4%) of US households were unbanked. Among these, one-half do not have a bank account because they struggle to maintain minimum balance requirements, and one-third noted their lack of trust in banks as their reason for not owning an account.17 When financial institutions assess current and future products and services to meet financial inclusion goals, they should consider the barriers to access, the reasons the underserved are not participating in financial services offerings, and the demographic makeup of the underserved market.

Underwriting practices, fee structures, balance thresholds, and credit history evaluation may be systemic barriers to access products and services. To begin dismantling those barriers, financial institutions could develop revenue models less reliant on penalty-based fees, design or modify products specifically for low-income customer and small business needs, and invest in projects in economically distressed communities.

Artificial intelligence (AI) and digital technology can help address these barriers by helping institutions profitably access and serve the underserved. For example, AI has enabled insurance firms to realize new efficiencies in the underwriting process.18 According to the Consumer Financial Protection Bureau, 26 million Americans lack a credit record and are considered “credit invisible” and 19 million do not have enough credit history to generate a credit score.19 ZestFinance’s Zest Automated Machine Learning platform is an example of one AI underwriting solution that helps companies assess borrowers with little to no credit information or history.20 AI utilization in credit decision-making and credit risk analysis can help remove some of the biases that have historically prevented the credit invisible from accessing credit products.

Understanding how and where a financial services provider deploys its products and services is just as important as the products and services it offers. Financial institutions can tap into existing outlets in underserved communities, such as retail stores, grocery stores, pharmacies, or postal services locations, to expand distribution opportunities for financial products. Technology has enabled new distribution strategies and allowed companies to reach some in underserved communities, but barriers to access of widely used applications should be considered when developing sales strategies. According to a 2019 study related to smartphone ownership and usage, a smartphone was the sole access point to the internet for 17% of Americans, almost double the amount in 2013. While 81% of adults report owning a smartphone, only 53% over the age of 65 and 71% living in rural areas own one.21 Measuring profitability of products or services through the lens of a purpose-driven financial inclusion sales strategy can help financial institutions identify and mitigate the barriers to access as well as identify alternative distribution.

Questions for financial leaders to consider:

How can we develop and deploy products and services for underserved markets that balance shareholder, societal, and employee expectations, yet do so at scale to drive financial growth?

How does our organization mitigate inherent bias in product design; reach and distribution; and credit risk modeling?

What key performance indicators (KPIs) can we use to measure the success of new and existing programs in addressing financial inequities?

Community

Unite with purpose. Aligning financial inclusion goals and values to partnerships and community action for the underserved in ways that matter to them and their communities is central to corporate social purpose and is a foundational element in building mutual trust. Bank of America’s US$1 billion, four-year commitment to help local communities address economic and racial inequality accelerated by a global pandemic reflect its commitment to support communities of color, small businesses, and workforce development and draws on its dedication to foster economic recovery and growth in the communities it serves.22

Industry organizations also recognize the importance of committing to long-term community investment. The Business Roundtable supports Community Development Financial Institutions (CDFIs) and Minority Depository Institutions (MDIs) that drive growth in their communities. Their 2025 goals include supporting Black and Latino community CDFIs with US$1 billion in grants and low-cost debt, and investing US$600 million to support vetted Black-led and Latino-led MDIs with capital and deposits.23 The idea of community transcends geographic boundaries. It’s truly connecting with community stakeholders to make a positive impact.

As with efforts to improve financial literacy among a financial services provider’s workforce, financial education for the underserved can sow the seeds of trust and form new customer segments. Programs can be tailored to specific demographics, such as single-parent households, income thresholds, and generational segments. They can be offered and delivered through partnerships with community organizations, and on technology platforms and devices accessible to the underserved market. Fidelity, Prudential, Principal Financial Advisors,24 and BlackRock25 have committed to financial literacy programs within their organizations. Programs provide education on planning for retirement, train educators to teach financial literacy concepts in classrooms, and facilitate community financial education workshops in underserved communities.

Regulators are an important stakeholder in the ecosystem; they have taken steps to ensure a fair, equitable, and inclusive financial system. Within the banking sector, the OCC’s June 2020 update to the Community Reinvestment Act rule,26 the first update in over 25 years:

• Encourages banks to make long-term investments to support community development by evaluating on-book activities while providing full credit for mortgages to increase affordable housing

• Increases support to small businesses and small and family-owned farms

• Fights harmful gentrification and displacement by focusing on activities that benefit low- and moderate-income (LMI) populations and areas

• Helps to reduce banking deserts by providing more credit for branches that serve LMI areas

Questions for financial leaders to consider:

What investments can we make to improve economic, social, and environmental factors for the underserved in our community and more broadly?

What investment programs and financial education curriculums can we deliver to our diverse community?

How do we partner with underrepresented, minority third parties?

What data collection and analysis approaches should we implement to create a holistic view of community impact and outcomes?

Ecosystem

The inside-out view from organization to offerings to community leads us to the ecosystem that supports and sustains financial services providers and stakeholders. The challenges in reaching and serving the underserved market are complex and multifaceted. Solutions should be sought through public and private collaborative partnerships that democratize costs while pursuing the common goal of an inclusive financial services system.

Large financial institutions could work with fintechs to help achieve financial inclusion goals. Fintechs have been able to lower transaction and service costs, fees, and penalties to reach underserved consumers who previously were unable to benefit from most financial services. They have also helped underserved small businesses gain access to working capital and manage their corporate expenses via digital platforms and tools.27 Traditional banks, insurers, and investment firms could adopt or partner with fintechs to help achieve competitive advantage, lower cost for delivery of services, and align with the corporate social purpose.28 Strategic partnerships, innovative technology solutions, and leveraging successful models that have already penetrated the underserved market can help fill the need to scale products and services.

Questions for financial leaders to consider:

How will you partner with diverse providers and improve systemic factors impacting equity across the ecosystem?

What can we learn from the success of fintechs reaching the underserved communities?

What are the big bets to make in alliances and new fintech partners that can increase inclusion?

Profit is the tangible value derived for shareholders, but it is also the advantage or benefit that is gained from doing something. Economics alone is not enough to achieve inclusive financial services systems. Achieving financial inclusion requires a multifaceted strategy. Addressing the gaps in financial literacy; removing the biases that are embedded in processes, systems, and thinking; and providing access to lending, insurance, deposit, investment, and credit products, requires systemic and cultural organizational change. To create a truly inclusive financial services system, financial institutions will need robust corporate social purpose programs that include strategies and incentives to innovatively develop products and services, invest in underserved communities, and partner with institutions outside of the industry to bring the best and brightest together to solve the challenges. Only then can the financial services industry collectively achieve a higher bottom line.

{kind=link}