Enhancing supply chain resilience in a new era of policy

Managing risks and evaluating US manufacturing investments to improve operational agility

Jim Kilpatrick

Kristine Dozier

Kate Hardin

John Morehouse

Key takeaways

1. A number of new federal policy measures and proposals could impact domestic manufacturing, including tax, regulatory, energy, and trade policy.

2. The new administration’s policy approach could support continued investment in the US manufacturing sector. It could also drive a notable shift in supply chain strategy by prioritizing reshoring while potentially altering recent nearshoring and global sourcing trends.

3. US manufacturers import a variety of products, parts, and raw materials from around the world, and supplemental tariffs levied on these items could potentially impact supply chains, costs, and the industry’s profitability.

4. Economically viable opportunities for reshoring production to the United States are likely to be higher-value, complex products with strict quality standards, produced with technologically advanced, higher-capital intensity processes, and a workforce with higher-level skills.

5. To help position for growth in the face of uncertainty that may lie ahead, manufacturers can assess their risks, implement near-term risk mitigation approaches, and explore supply chain strategies that emphasize resilience and minimize costs.

Click here to download a copy of the key takeaways PDF.

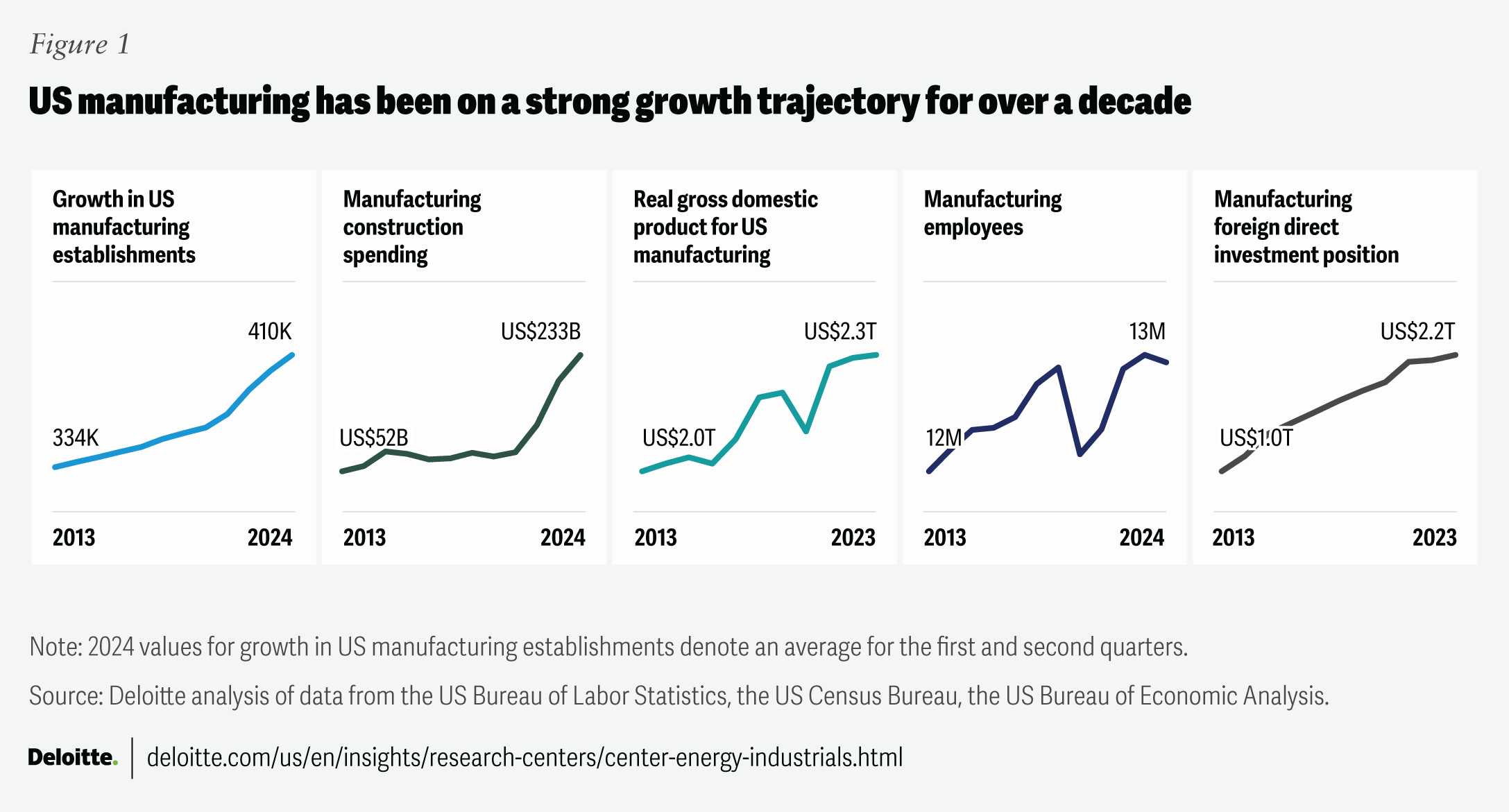

For more than a decade, US manufacturing has achieved noteworthy growth in employment, output, the number of manufacturing establishments, and investment to expand or construct new facilities (figure 1). This growth appears to have been partly driven by a desire to derisk supply chains and establish facilities closer to US customers. Increased supply chain volatility in recent years due to the COVID-19 pandemic, geopolitical dynamics, trade tensions, rising costs, labor shortages throughout the value chain, and natural disasters1 has led organizations to shift their supply chain strategy from cost minimization to a focus on balancing cost with resilience.2 To help achieve this, some manufacturers have reconfigured their supply chains by reshoring portions of their production, by nearshoring—leveraging the United States-Mexico-Canada free trade agreement to source more from Mexico and Canada—and by growing trade with countries such as India and Vietnam, which offer cost advantages.3 And this trend is likely to continue: A recent survey by The Conference Board of over 1,700 global C-Suite executives found that 71% of US chief executive officers plan to alter their supply chains over the next three to five years.4

President Trump’s policy priorities include cutting taxes, reducing regulations, lowering energy costs, and bolstering fair trade.5 These measures could collectively support—and potentially accelerate—continued investment in the US manufacturing sector, a major goal of the Trump administration.6 The administration’s policies could also potentially drive a notable shift in supply chain strategy by prioritizing reshoring while potentially disrupting recent nearshoring and global sourcing trends. Tariffs comprise a component of President Trump’s economic strategy, with stated aims of boosting US manufacturing, collecting tariff revenue, addressing unfair trade, and strengthening national security.7 For instance, invoking the International Emergency Economic Powers Act,8 the President has imposed 25% “supplemental tariffs”9 on imports from Mexico and Canada (with the exception of a 10% tariff on Canadian energy resources), and 20% tariffs on all goods from China.10 He later amended the tariffs on Mexico and Canada to temporarily exclude goods that comply with the United States-Mexico-Canada free trade agreement (USMCA)11 and levied 25% tariffs on all aluminum and steel imports.12 President Trump has also signed several trade-related executive orders such as the “America First Trade Policy.” This policy directs various federal agencies to investigate the impact of international trade dynamics on US workers and businesses as well as the USMCA,13 which could result in new tariffs or other changes to trade policy in the future.

This shift in policy approach and the potential for ongoing supply chain volatility could present opportunities and challenges for US manufacturers due to factors such as the geographic location of their supply base, the size and financial health of the company, and their ability to flexibly respond to supply chain shocks. If steps are not taken to build resilience and agility, some companies—including smaller firms that make up a significant portion of the US manufacturing landscape14—may struggle to absorb added costs, which could lead to reduced business or even closures.15 Conversely, a company with an international production footprint could instead shift production to its established US manufacturing facilities and potentially gain market share from competitors. In this paper, Deloitte’s Research Center for Energy and Industrials examines the current global nature of US manufacturing supply chains, explores the potential impacts of tariffs and ongoing supply chain volatility on the industry, and identifies considerations for companies to sharpen their focus on resilience and agility while minimizing costs.

The potential impact of supplemental tariffs and trade tensions on US manufacturing

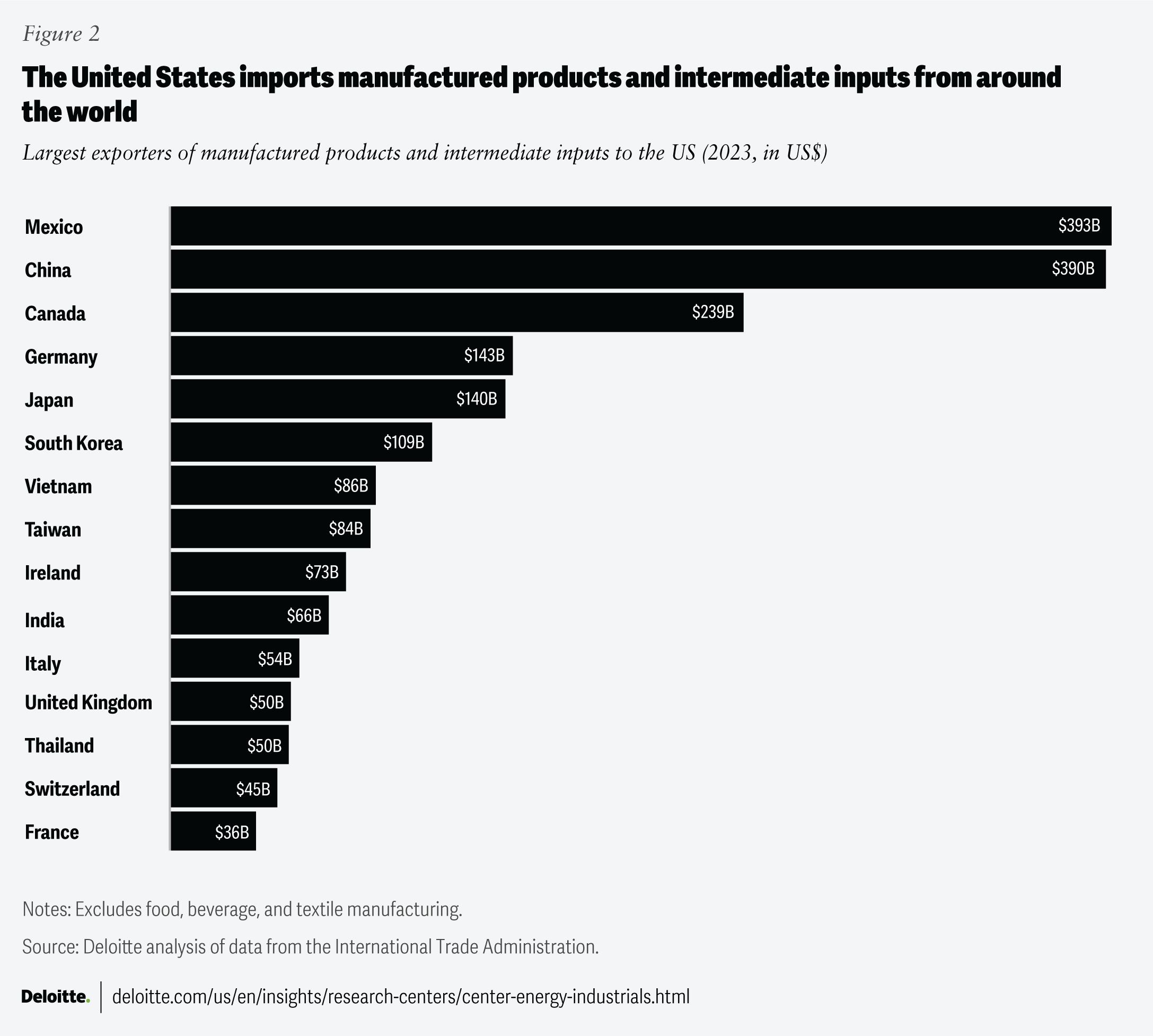

While the stated intent of tariffs is to support investment in US production,16 they can also impact global supply chains and current cost levels. In fact, in the National Association of Manufacturers 2025 first-quarter outlook survey, 73% of respondents cited trade uncertainties, including tariffs and trade negotiations, as their top business challenge, up from 56% and 37% in its previous two quarterly outlook surveys, respectively.17This may be because US manufacturers import a variety of products and intermediate inputs18from around the world (figure 2).

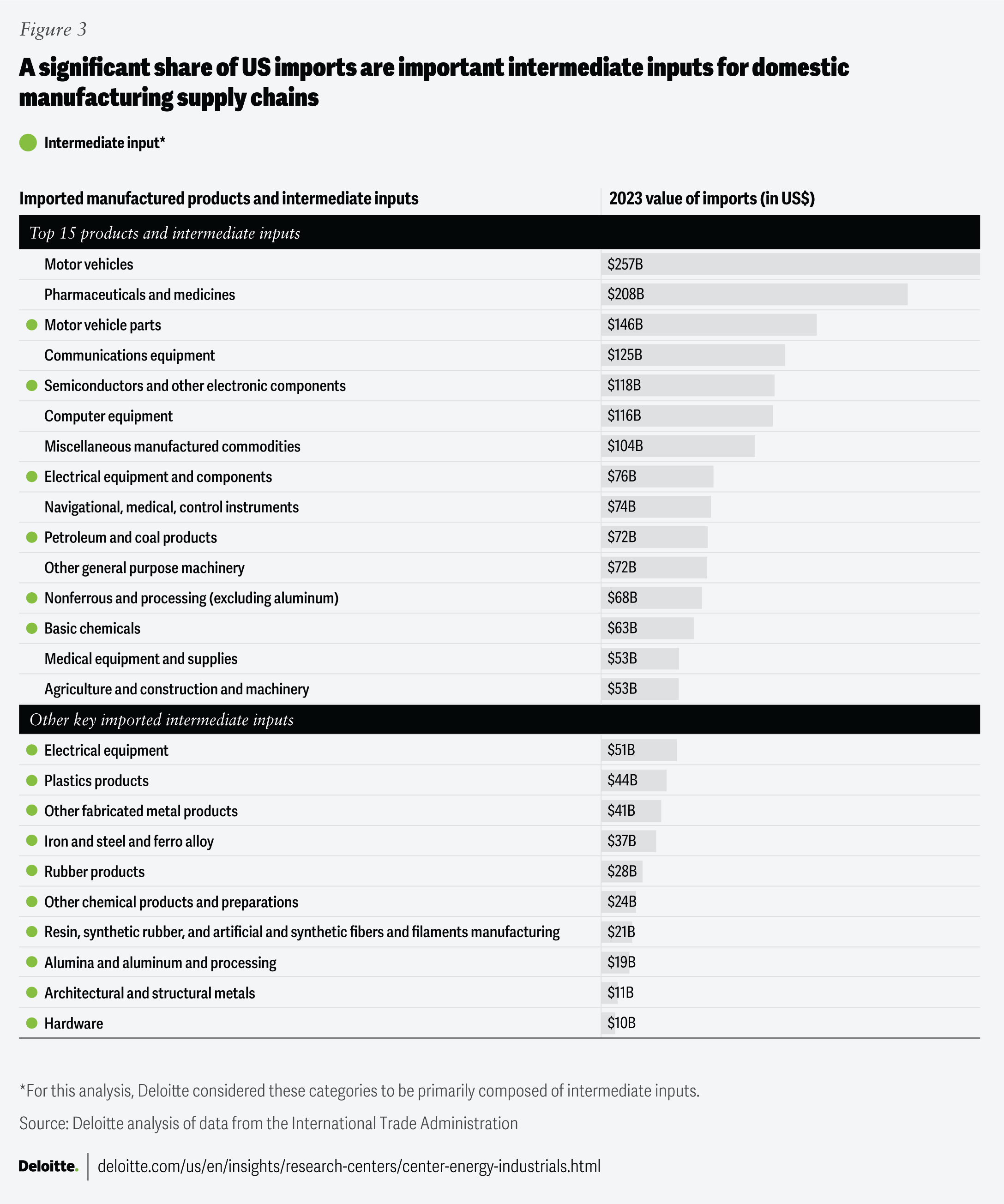

In 2023, Mexico surpassed China as the leading US import partner for manufactured goods, followed by China and Canada.19 Germany, Japan, and South Korea round out the top six import partners, primarily due to motor vehicle imports, while Vietnam and Taiwan lead in computer and electronics devices and components.20 Of the top 15 manufactured goods imported by the United States, six are important intermediate inputs for US manufacturing supply chains and operations, including motor vehicle parts, electrical and electronic components, and non-ferrous metals (excluding aluminum) (figure 3). The remaining intermediate inputs imported by the United States also comprise a substantial import value.

The largest impact is likely to come from tariffs placed on Mexico, China, and Canada—the United States’ top three trading partners21—which supply important intermediate inputs to the leading US manufacturing subsectors (see “US manufacturing subsectors appear to emphasize advanced technology and likely demand workers with higher-level skills”).

US manufacturing subsectors appear to emphasize advanced technology and likely demand workers with higher-level skills

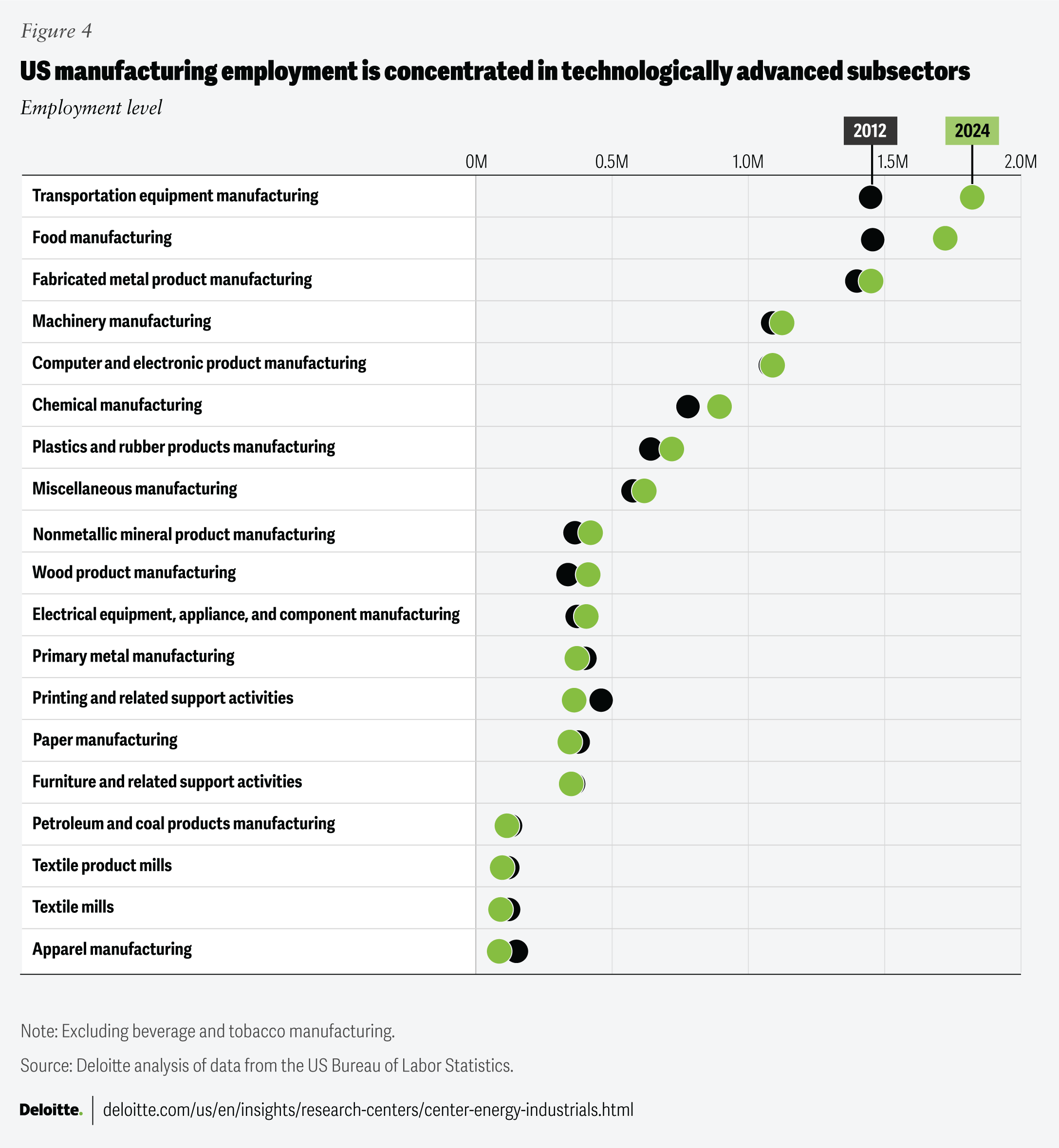

US manufacturing employment today is concentrated in subsectors that produce products such as transportation equipment, computer and electronic products, and machinery as well as their suppliers like fabricated metal products, and plastic and rubber products manufacturers (figure 4).22

Due to their complexity, high standards for precision and quality, and manufacturers continued journey toward smart operations, these products are often made using technologically advanced, high capital-intensity processes, which are likely to require more workers in higher-skill roles.23 Collectively, the US manufacturing subsectors that grew between 2012 and 2024 produce nearly 1.5 times more output per production worker compared to the subsectors with declining employment.24 These growing subsectors also employed over 80% of the workforce in 2024.25

The current makeup of the US manufacturing industry is important when considering tariffs and trade tensions because changes that impact the supply chains of any of these subsectors could impact domestic manufacturing overall. And because of higher labor costs in the United States compared to several other countries,26 if manufacturers were to reshore some of their production, it may be in advanced manufacturing27 facilities that produce high-value products or goods that are critical for national security. International sourcing is likely to remain in place for products like apparel or footwear that may not meet these criteria and are typically produced with labor-intensive processes that tend to be less economically viable in the United States.28

Excluding food manufacturing, the three largest US manufacturing subsectors by employment—transportation equipment, fabricated metal products, and machinery manufacturing—could be affected by tariffs on imported steel and aluminum (figure 5). Similar to the machinery, computers, and electronics products subsectors, transportation equipment also relies on imported semiconductors, electrical equipment, and components; and plastic products, in addition to motor vehicle and aerospace parts.

In addition to intermediate inputs, motor vehicles are the top imports from Mexico and Canada.29 An IBISWorld analysis found that the average profit margin for cars and light-duty vehicles manufactured in the United States in 2024 was around 5.4%.30 Upticks in cost could quickly erode these margins.

In general, the global nature of manufacturing supply chains means that if supplemental tariffs are levied on countries that supply key products and intermediate inputs, it’s likely to raise costs and could impact profitability for US manufacturers. If manufacturers raise their prices in response, it can lead to higher inflation for consumers.31 Price increases due to imposed tariffs on Mexico, Canada, China, and expanded tariffs on steel and aluminum could potentially lower Americans’ disposable income by an average of 1% in 2026, according to estimates by the Tax Foundation.32 This could reduce consumer spending, especially on nonessential items, leading to lower demand for manufactured goods (see “Balancing price and cost when facing tariffs”). Additionally, these price hikes could prompt the Federal Reserve to limit or delay planned rate cuts for 2025,33 which could further reduce demand.

Balancing price and cost when facing tariffs

When tariffs are levied, manufacturers will likely need to be strategic about the amount of cost they pass on to their customers through price increases. While passing on some portion of the cost may be beneficial to the business, it could also negatively impact revenue through decreased demand. Manufacturers should carefully consider the price sensitivity of their products when developing potential pricing strategies in response to tariffs. Meanwhile, digital transformation, automation, and the continued push toward smart operations could help companies reduce costs34 and potentially offset some of the impacts of tariffs.

Tariffs could also affect US manufacturing exports (figure 6). Retaliatory tariffs by other countries35 could force some US exporters to lower prices to remain competitive abroad, which could cut into margins.36 Retaliatory tariffs on industries such as agriculture could reduce demand for its products abroad,37 which could, in turn, reduce demand for machinery manufactured in the United States like tractors, combines, or other harvesting equipment.

Considerations that could help bolster growth in the face of tariffs and supply chain volatility

Deloitte’s analysis identified a three-pronged strategy that manufacturers can consider to help position themselves for growth, despite the uncertainty that may lie ahead. Each strategy varies in complexity, time horizon, and relative capital cost (figure 7).

#1: Assess supply chain exposure and risk

A step US manufacturers could take is to perform a detailed analysis to determine the potential impacts of tariffs and any trade tensions on its supply chain. This includes scenario planning for direct tariff impacts as well as potential retaliatory actions that other countries could levy on US exports. It should also include understanding “second order risks” from suppliers (including tier 1, tier 2, and beyond) that source inputs from abroad and may need to raise prices or might face financial distress that could lead to disruptions. Here are a few steps for US manufacturers to consider taking throughout their supply chains.

- Map your exposure. Analyze import transaction data and determine the country of origin for all components and raw materials that are sourced from outside the United States.38 Verify that imported components are classified under the correct HTS Code and determine if tariffs apply to those components.

- Assess the likelihood of ongoing trade tensions. Supplemental tariffs can be levied even on countries within free trade agreements like the USMCA.

- Estimate added costs for various tariff scenarios. By considering the country of origin and the potential for trade tensions, US manufacturers can gain insights into potential tariff scenarios. Early identification of components and products with higher volumes and values that may be subject to tariffs can help prioritize and focus mitigation strategies.

#2: Consider near-term tariff mitigation approaches

Before making substantial changes to their supply chains, manufacturers can take steps to help mitigate the impact of tariffs on their bottom line. These approaches may be particularly prudent if supplemental tariffs are levied temporarily and later removed.

Some US companies “front-load” imports by stocking up before tariffs are imposed.39 Although the benefits are temporary, several companies used this strategy ahead of tariffs levied on China in 2018 and again in late 2024.40 Another strategy is to collaborate with partners to renegotiate contracts based on current market conditions.41 Although the importer of record is legally required to pay tariffs,42 manufacturers can work with their suppliers to offset the cost of the tariff. If the existing contract has a “change in law” clause, that may allow for revisions to terms, including pricing.43

There are also duty-reduction strategies that companies can investigate to help manage the financial impact of tariffs.44 These can include applying for exemptions and exclusions, if available; implementing available customs valuation planning strategies such as unbundling non-dutiable elements from the price of imports; evaluating transfer pricing strategies; and assessing first sale for export customs valuation structures.45 Supply chains may allow companies to take advantage of foreign trade zones or bonded warehouses, while moving production to or sourcing from another country (discussed next) can change the country of origin and potentially reduce the duty.46

#3: Explore supply chain strategies to help minimize cost and emphasize resilience

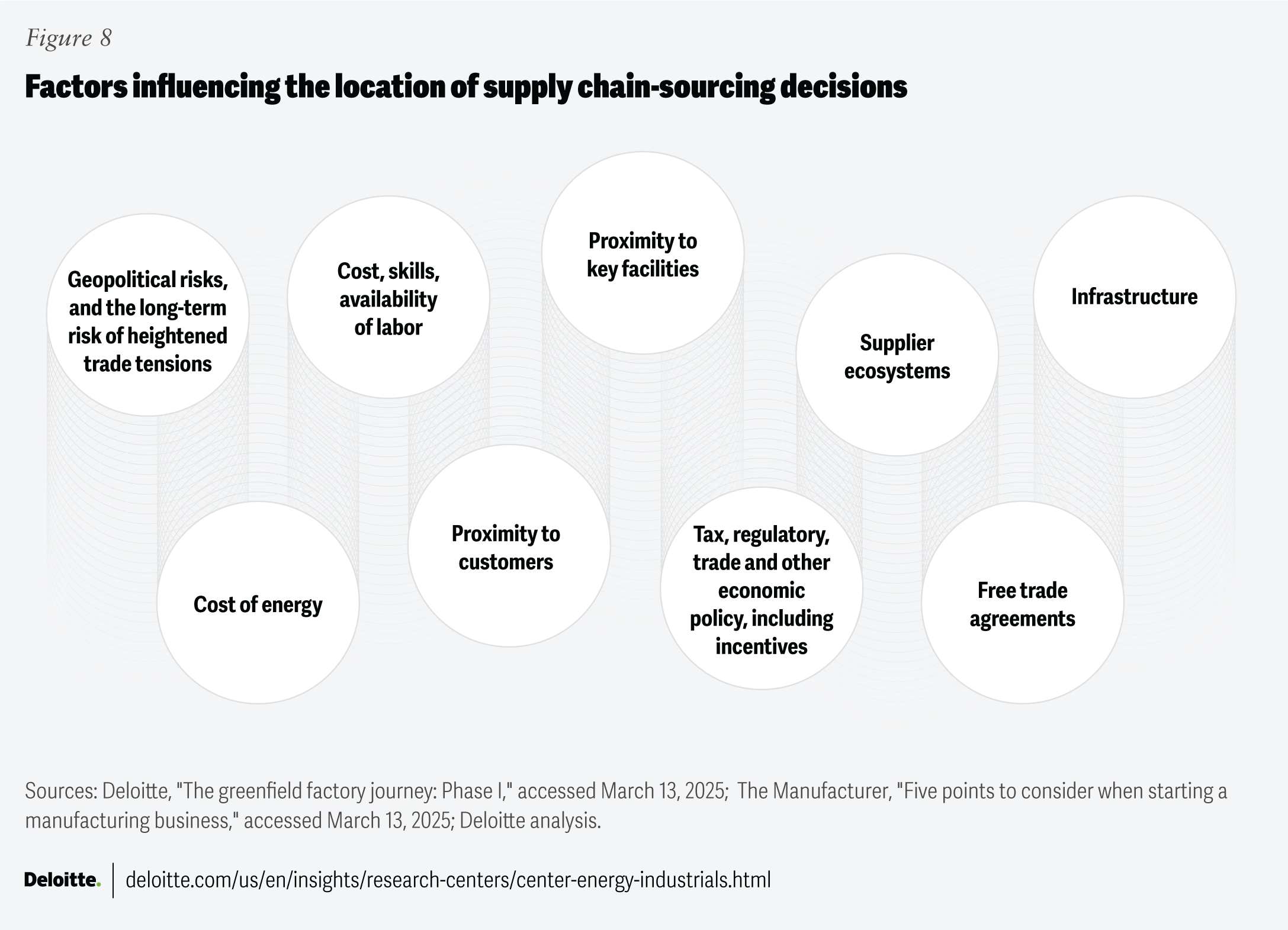

After considering near-term tariff mitigation approaches manufacturers may need to evaluate their overall supply chain strategy and decide which products and intermediate inputs they should manufacture domestically versus in other countries. In addition to tariffs and trade policy, several factors can play an important role in this decision (figure 8).47

There may be a tipping point where the combination of various factors and the risk or implementation of supplemental tariffs could make it more attractive for manufacturers to reshore additional production to the United States (see “Identifying a tipping point for reshoring production to the United States”). However, because these investments can be significant, manufacturers may seek clarity and certainty on US policy before making them.48

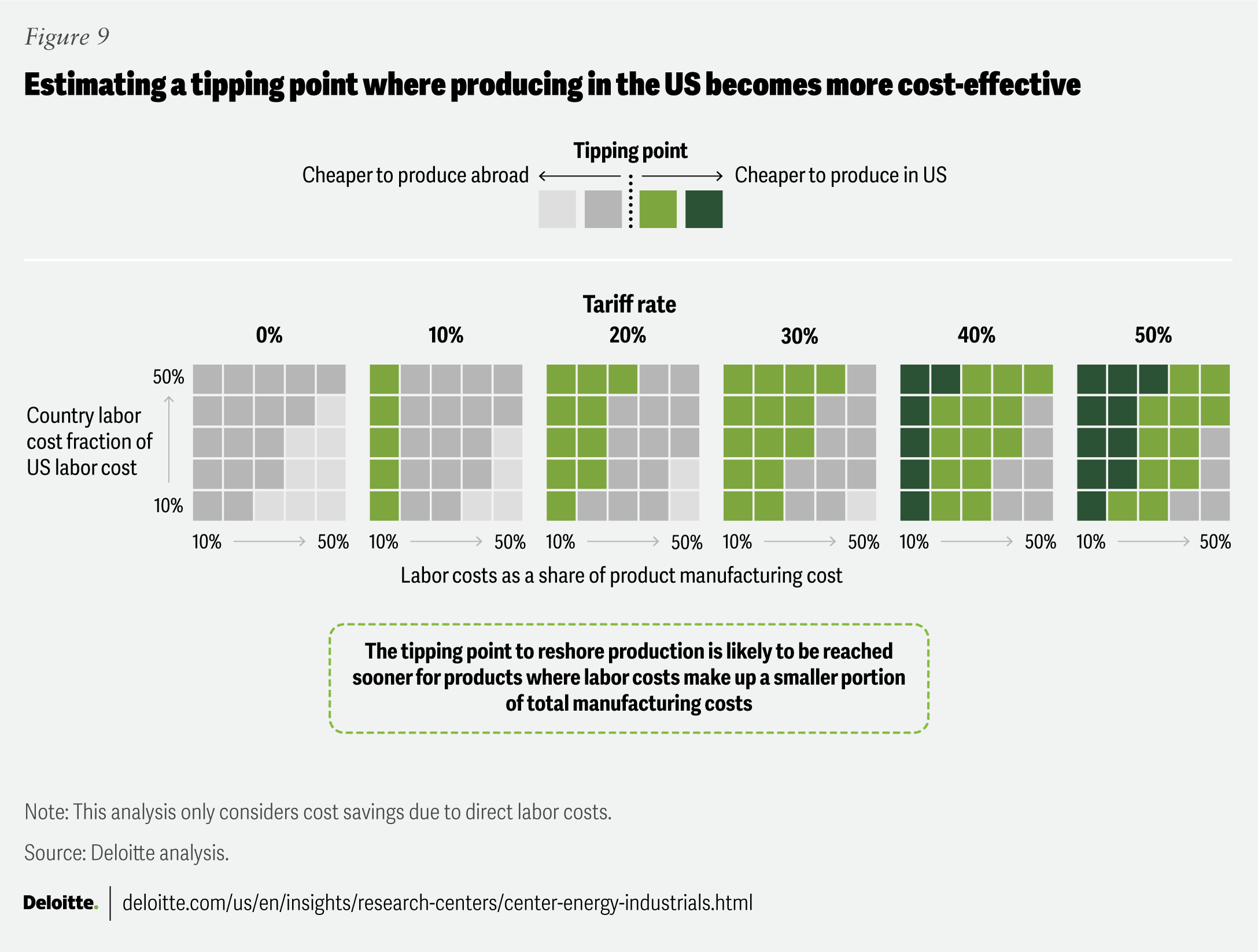

Identifying a tipping point for reshoring production to the United States

To understand how supplemental tariffs and long-term trade uncertainty could affect reshoring decisions, Deloitte used a simple cost model to estimate the tipping point where producing in the United States becomes more cost-effective (figure 9). The model assumes that total manufacturing costs are the sum of material and labor costs directly related to making the product, plus overhead. In general, the model shows that when labor costs make up a lower share of the manufacturing cost (that is, less labor-intensive) companies reach a tipping point for reshoring production to the United States sooner.

Considering a hypothetical example, if it costs US$15,000 to manufacture a car in the United States and labor makes up 15% of the manufacturing cost (US$2,250), then companies could achieve cost savings of US$1,575 by shifting production to a country where the labor rate is 30% of the labor rate in the United States.49 If a 25% tariff is applied to goods imported from that country, however, the added costs erase the savings making it potentially cheaper to reshore production.50

Several other factors can provide cost benefits when manufacturing abroad, such as potentially reduced overhead due to lower rent, energy, and indirect labor costs, or lower material costs if more intermediate inputs are sourced from nearby, lower-cost suppliers. However, a comprehensive policy strategy that includes tax, regulatory, and permitting reform could lower costs and support investment in US manufacturing, according to the National Association of Manufacturers,51 which could potentially lower the tipping point for reshoring some production to the United States. In general, manufacturers should calculate their tipping point based on the part or product they are currently sourcing outside of the United States, the country from which the item is sourced, and a detailed analysis of how all factors combine to influence the decision.

For labor-intensive or lower-value goods, it might not be as economically viable for manufacturers to reshore production to the United States. Instead, manufacturers may diversify their supply chains by seeking suppliers in countries that offer labor cost advantages—and minimize the long-term risk of supplemental tariffs, trade tensions, and geopolitical friction. Countries that are geographically closer to US manufacturing facilities and those that are likely to have long-term free trade agreements in place can offer additional advantages in terms of minimizing duties and disruptions and maximizing resilience. As part of their risk assessment, manufacturers may need to consider the time it could take to reach full-scale production, the potential for quality issues and delays with onboarding new suppliers and facilities,52 and the impacts of potential changes to free trade agreements, such as the USMCA.53 To help themselves remain agile, companies should plan for all scenarios, and focus on long-term supply chain strategy.

Economically viable opportunities for reshoring to the United States are likely to be higher-value, complex products with strict quality standards, produced with technologically advanced, higher capital-intensity processes, and a workforce with higher-level skills. Here are a few approaches US manufacturers may consider to reshore production, which could minimize the impact of supplemental tariffs and maximize supply chain resilience.

- Utilize current internal US manufacturing capacity.

Companies that already have a manufacturing footprint in the United States may be well-positioned to shift some or all production to existing US facilities. In fact, two electronics product manufacturers have begun to contemplate shifting some production from Mexico to their US plants, while several automakers are considering plans to ramp up production at their existing US facilities.54

- Expand existing supplier capabilities and production with deeper partnerships.

US manufacturers can look for opportunities to further leverage the capabilities and capacity of their current US supply base and help them scale up production. For example, a tier-1 supplier might be able to produce a key assembly currently sourced abroad, while a tier-2 supplier may be able to expand from producing only individual components to assemblies as well.

Partnering closely with suppliers will be important to help them boost capacity. Not only can it facilitate knowledge transfer and visibility, but it could also be particularly important in cases where suppliers need to make investments in new technology, equipment, workers, or even expand their facility. Contracts may be necessary to help them mitigate risk, especially given the potential for rapid changes to supplemental tariffs, negotiation of new free trade deals, or other shifts that could impact the advantage of the partnership. Establishing joint ventures with suppliers can take partnerships to the next level to share risk and resources and open new doors for increased communication, technological innovation, and operational efficiency gains.55

- Explore mergers and acquisitions to support vertical integration.

Mergers and acquisitions are another way manufacturers can quickly gain access to supplier production capacity, know-how, labor, technology, and capital equipment while reducing risk and eliminating the need to start from scratch.56 By vertically integrating suppliers with mergers and acquisitions manufacturers can enhance communication and visibility, build resilience and agility, accelerate innovation, improve quality, and potentially reduce their environmental impact.57

- Expand existing facilities or build new greenfield US manufacturing plants.

Investments in expanding existing US facilities or building new greenfield manufacturing plants are likely to yield highly automated, capital-intensive processes that require fewer, but highly skilled, employees. They also take time to build. It can take 2.5 to 7 years to reach full production from the start of the planning phase of a greenfield manufacturing plant.58 Because of the timescale and capital investment, manufacturers will likely need to take a long-term view and base investment decisions on the fundamentals of how they plan to grow their business.

Supplemental tariffs may influence the decision, but a holistic approach that considers all important factors in deciding where to manufacture products and intermediate inputs will be important. Several global automakers and electronics manufacturers recently announced that they are planning or considering investments in new US manufacturing facilities ahead of heightened trade tensions.59

- Support new investments in US manufacturing by securing the workforce.

The makeup of the US manufacturing industry, with its increasing focus on advanced manufacturing and push toward smart operations, requires technical expertise and advanced training. Leading sectors like automotive, fabricated metal, and aerospace manufacturing demand a combination of digital skills, soft skills, and advanced technical skills, such as those required to work with composites and specialized alloys.60 Yet, according to the 2024 Deloitte and the Manufacturing Institute talent study, 1.9 million jobs in the US manufacturing industry could go unfilled by 2033 due to a gap between the skills available in the workforce and the advanced, technical skills increasingly required for many manufacturing jobs.61 For instance, according to the World Economic Forum’s Future of Jobs 2025 report, technical skills such as AI and big data, networks and cybersecurity, and technological literacy will see the largest increases in advanced manufacturing by 2030.62 At the same time, worker expectations are changing and labor participation rates in the United States are expected to fall through 2030.63

An acceleration in reshoring could add more pressure to the talent landscape in manufacturing and potentially create a tighter labor market that demands higher wages, especially since these investments are likely to create higher-skill jobs. To remain competitive, companies will likely need to secure the required workforce. They can start by improving the worker experience and leveraging digital tools that support training, make jobs easier, and enable advanced workforce management capabilities.64 Companies can also take an ecosystem approach to find and develop talent, while federal, state, and local governments may play an important role by fostering public-private partnerships to help build the manufacturing talent ecosystem.65

Finally, investing in digital tools and technology is likely to play an important role in any supply chain strategy that seeks to minimize cost and maximize resilience. For example, simulation, supply chain planning tools, and enhanced visibility can help mitigate risks in global supply chains.66 Additionally, leveraging technologies like generative AI and smart operations is likely important for maximizing operational efficiency and minimizing costs in US manufacturing facilities.67

Moving forward in a new era of policy

As the United States transitions into a new policy landscape, its manufacturing industry is poised to continue its growth trajectory of over a decade. Could adjustments to tax, trade, and regulatory policies further accelerate this growth and help more manufacturers expand their US manufacturing footprint in the coming years? While the future remains uncertain, manufacturers should remain flexible and agile to seize potential opportunities and navigate emerging challenges. Heightened supply chain volatility, supplemental tariffs, and ongoing trade tensions may become the new normal. Therefore, a supply chain strategy focused on resilience, agility, and cost savings will likely help US manufacturers thrive in this evolving business climate. Gaining an understanding of global supply chains and mitigating potential risks are important steps. Remaining focused on the drive toward smart operations will be important to enhance supply chain visibility and reduce costs. And maintaining a winning workforce strategy could become even more important than it is today—especially if reshoring accelerates.

BY

Jim Kilpatrick

Kristine Dozier

Kate Hardin

John Morehouse

Continue the conversation

Meet the industry leaders

Steve Shepley

Ben Holocher

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}