Trend 2: M&A in an altered world has been saved

Cover image by: Stephanie Dalton Cowan

As mining companies seek to strengthen their portfolios and develop the commodities that can help power the energy transition, merger and acquisition (M&A) activity is picking up. To finance M&A deals however, miners should work to win back the trust they lost during the peak of the last cycle when numerous deals destroyed value rather than creating it. To win back investor confidence, companies may need to find new ways to deliver consistent shareholder returns; enhance their environmental, social, and governance (ESG) performance; and improve their capital and operational discipline.

While the rapid onset and spread of COVID-19 resulted in a slowdown initially in M&A activity across numerous sectors, volumes have picked up from these lows; historical evidence suggests that M&A markets quickly recover once uncertainty subsides.1 This is true in the mining sector as well, where companies remain on a relentless search to build robust portfolios, a quest that is expected to be fueled, at least in part, by M&A transactions and consolidation.

Companies without deep coffers, however, may find themselves the victims of simmering investor displeasure. Much of this can be traced back to the historical track record of shareholder returns in the mining sector.

“Significant wealth was destroyed subsequent to the peak of the last mining cycle, and a good amount of that was due to richly priced M&A transactions that failed to deliver,” says Robert Noronha, partner, M&A Advisory, Deloitte Canada.

Stung by poorly performing transactions, many investors have lost confidence in the mining sector over the past decade. As a result, small and mid-sized miners on the hunt for capital have often struggled. This is doing more than obstructing market activity; it’s also leading to a limited pipeline of new projects being developed and put into production.

Addressing this could be key to unlocking the next set of minerals that can help power the energy transition and drive a new wave of economic growth. Miners should focus on winning back investor trust by addressing a range of fundamental issues.

In seeking M&A financing, mining companies should be aware of the criteria investors are looking at in making their capital allocation decisions. First, many investors want comfort around a company’s ability to deliver stable dividends over time. This means maintaining dividends even if commodity prices dip.

Beyond returning excess cash flow to shareholders, mining companies are also expected to have cohesive and compelling growth stories. With many miners issuing relatively flat future production guidance, investors often feel there is limited upside potential or opportunity for capital appreciation in the sector. This, combined with lower yields and the relatively high risk of mining operations, has resulted in fewer generalist investors targeting the industry.

But shareholder returns are just one area of focus for most global investment firms. Another area is mining’s ESG performance. With each passing year, investors are pressing harder for detailed information about companies’ ESG targets and how they are tracking against them.

ESG investing continues to be a major trend. According to a study released in January 2020 by the HEC Paris Business School, the Toulouse School of Economics, and MIT Sloan, investors are willing to pay US$0.70 more for a share in a company that donates at least one dollar per share to charity.2 That trend has strengthened following the outbreak of COVID-19, as sustainable funds began to attract record levels of investment, with inflows rising to US$45.7 billion globally in the first quarter of 2020 alone.3

In the mining sector, the ESG movement is translating into vocal calls for companies to reduce the carbon intensity of their asset portfolios, eliminate exposure to geographies where human rights violations and corrupt practices are common, and follow through on their commitments to link social investments to sustainable community outcomes.

Given the limited universe of sector-focused investors, mining companies are acutely aware that they are competing with their peers for these pools of capital. To capture investor attention, new strategies may be required.

Some companies are attempting to attract financing by widening their potential investor base. Australia’s Newcrest, for instance, recently listed on the Toronto Stock Exchange4—and it is by no means the only company to have sought a secondary listing outside its home jurisdiction. Two Canadian companies—Wheaton Precious Metals5 and Yamana Gold6—were recently approved to trade on the London Stock Exchange, and others are poised to follow.

Dual listings however, are not the remedy to solve a mining company’s capital needs. To truly win back investor confidence, mining companies should strengthen their capital and operational discipline. Additionally, mining companies should undertake M&A transactions at no or low premiums, as opposed to the typical 30% to 50% ranges of the past.7

To truly win back investor confidence, mining companies should strengthen their capital and operational discipline.

“With investors increasingly reacting negatively to high-premium deals that fail to deliver sustainable value, low-premium to no-premium transactions are becoming more common,” says Ian Sanders, Mining & Metals leader, Deloitte Australia. “Success under such a structure requires a relentless focus on capital discipline.”

Mining companies may also succeed in attracting investors with longer time horizons by building a pipeline of projects to achieve growth. Before this can happen, however, exploration and development budgets must rise. Globally, the mining sector’s exploration budget fell by US$958 million between 2019 and 2020, a mere 19% increase since the lows of 2016.8 Only gold exploration stayed steady, rising 1% year over year.9

“Companies with excess cash flows often choose between M&A and exploration, which is why exploration budgets often fall subsequent to a transaction,” explains Dan Schweller, Global Energy, Resources & Industrials Financial Advisory leader, Deloitte US. “Yet, it doesn’t have to be this way. Instead, larger miners can partner with junior explorers to help them build out their assets. It all comes down to intent.”

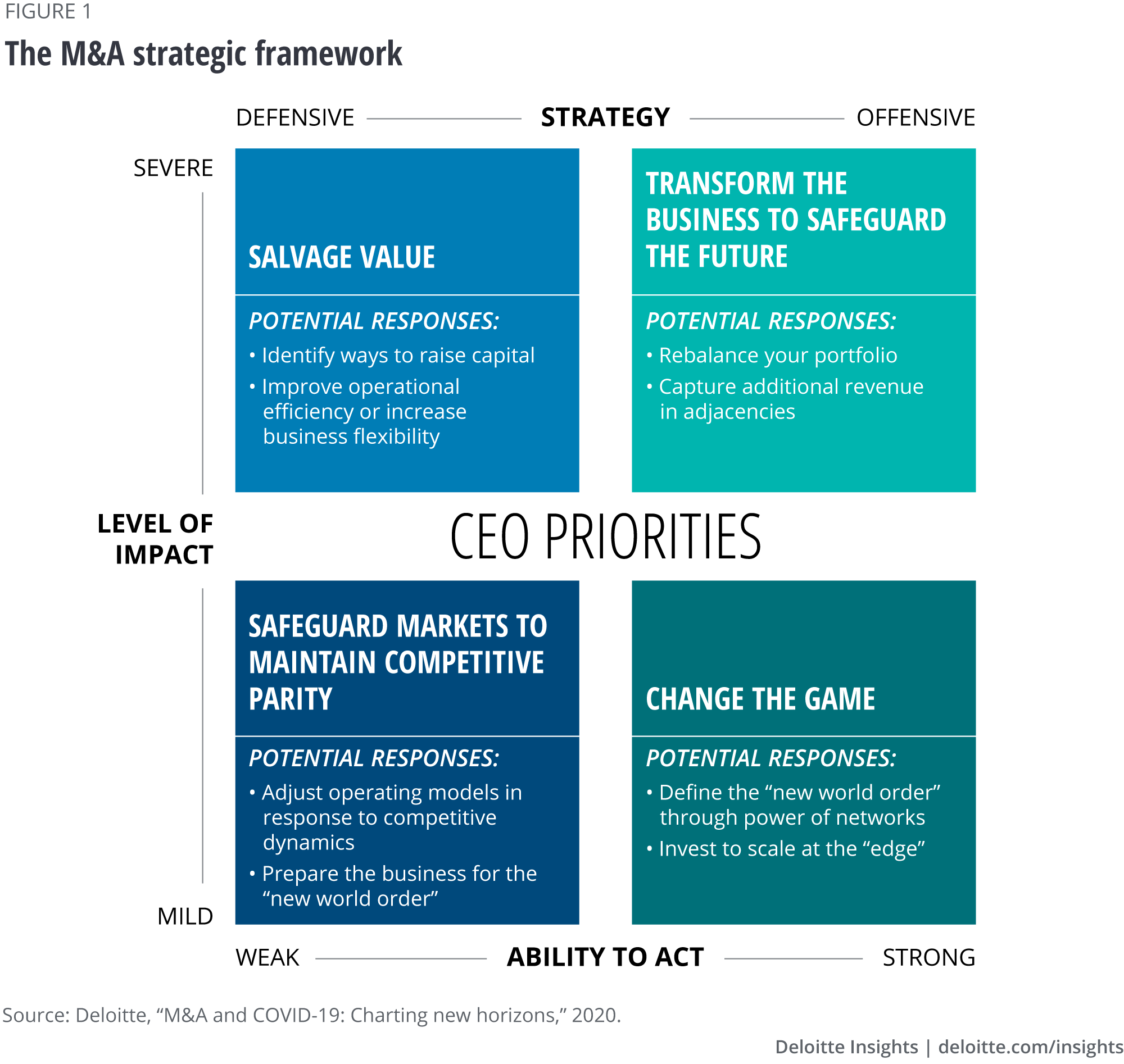

Beyond just addressing the table stakes issues for investors, it is important that mining companies think about the strategic possibilities through M&A. The post–COVID-19 world will unleash structural and systemic changes that could have a direct impact on end markets for commodities. Mining companies should think about using M&A as a strategic tool to embrace scenario planning and build this into their strategic thinking as they navigate these uncharted waters. This can help companies decide the direction of their strategy, identify the new capabilities required, and prioritize the markets in which they need to operate to drive growth and profitability. Redefining M&A in terms of these scenarios and choices can bring much needed clarity of purpose while confronting these uncertainties.

A combination of defensive and offensive M&A strategies should emerge as a result, as companies try to safeguard existing markets, accelerate recovery, and position for future success. Figure 1 shows some of the key strategic choices that are facing mining companies as they seek to win back investor trust.

Within these quadrants, there are a range of potential strategic moves that mining companies can undertake, and we are already seeing many firms exploring these options.

1. Salvage value. Mining companies will likely face a range of investor pressures here. This can span the gamut of shedding nonperforming assets, selling off assets that don’t meet the ESG expectations of investors, or divesting noncore assets to free up cash.

BHP, for instance, has continued on its course to divest thermal coal assets to meet its decarbonization agenda.10 Anglo American also laid out a plan to divest its thermal coal assets in South Africa within the next three years.11 Although many miners are struggling to find a balance between a focus on economic recovery and the need to meet their sustainability objectives, investor demands for improved environmental performance will likely see many more miners restructuring their portfolios in the years to come.

2. Safeguard markets to maintain competitive parity. Companies can also use M&A defensively to safeguard markets and maintain competitive parity. These defensive plays can emerge in several ways. The next tier of gold miners emerged in a set of mid-market consolidations in the past year. Many of these firms need to double down on extracting the synergies that they promised, not least to defend themselves from future predators.

Over the year, we have seen a range of announcements that have included the strategic alliance between Kirkland Lake Gold and Newmont Canada with respect to exploration and development opportunities around the company’s Holt Complex and Newmont’s properties in Timmins, Ontario.12 With predictions that gold prices could hit US$2,300 per ounce within the next year, and ongoing concerns about the length and magnitude of the second wave of the pandemic, more deals could emerge.

Likewise, in a sector where investor confidence is low, mining companies should again explore alliances and partnerships to bring promising projects online and share the risk between parties.

3. Transform the business to safeguard the future. On the offensive side, there are significant opportunities for mining companies to transform their portfolios through acquisitions or alliances. For many, this is about looking at their portfolios and doubling down on minerals or businesses, particularly those that are key to a lower carbon future.

Exxaro Resources, an African mining company with interests in various minerals and a large-scale coal producer, is putting down key positions in renewable energy.13

4. Change the game. There is also an opportunity for the sector to explore more transformative moves by exploring adjacent markets, scaling “edge” businesses, or creating alliances. Given the importance of battery minerals to a long-term energy transition, it is likely that we will see more nontraditional mining companies enter the space by either taking positions in critical minerals or even disrupting the traditional mining models.

For example, the US government recently acquired a stake in TechMet, a Dublin-based mining company, to create supply around key battery minerals.14 There are likely to be more of these kinds of deals emerging over time, with technology companies and motor manufacturers also expected to enter this market.

The companies that emerged strongest from the 2008 global financial crisis were those that took decisive measures to rebuild their balance sheets through a combination of rigorous cost optimization programs and divestment of noncore assets. The current situation, partly brought about by COVID-19, provides an opportunity for mining companies to use strategic M&A to position themselves to become the clear winners 10 years from now.

{kind=link}