2025 Oil and Gas Industry Outlook

Focus on capital discipline, increasing customer centricity, and investments in new technologies may help companies navigate economic, geopolitical, and regulatory uncertainties in 2025

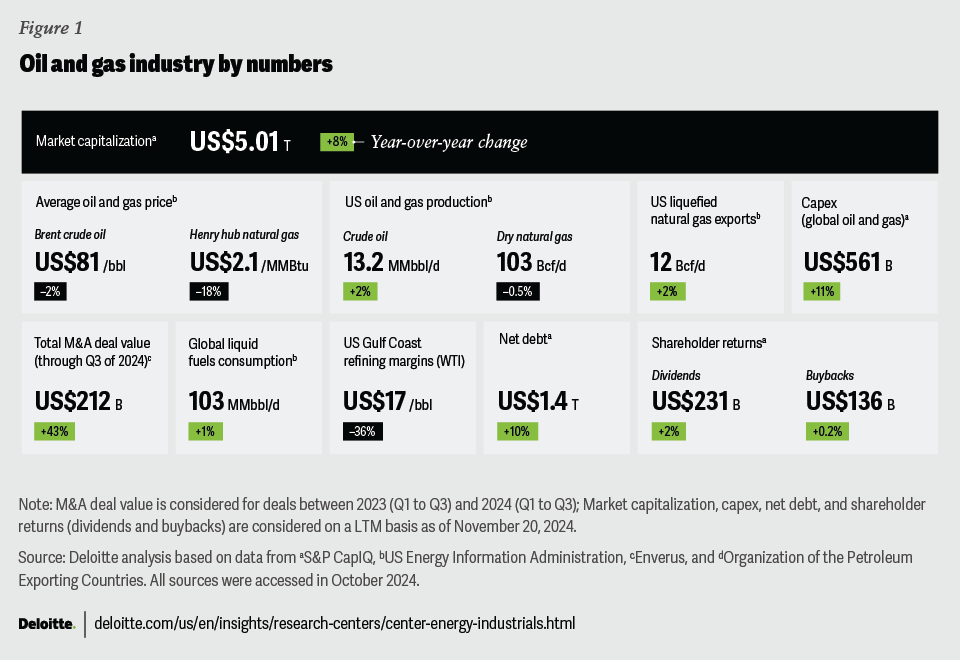

In 2024, the crude oil and natural gas market navigated a complex landscape of controlled OPEC+ supply and variable demand, heightened geopolitical tensions, macroeconomic weakness, and a continued focus on energy transition. This resilience is reflected in the stability of oil prices: Brent crude oil prices exhibited a minimal average monthly change and a monthly range-bound movement between US$74 and US$90 per barrel in 2024, making 2024 one of the most stable years in the past 25 years.1 Globally, the oil and gas industry distributed nearly US$213 billion in dividends and US$136 billion in buybacks between January 2024 and mid-November 2024 (figure 1).2

By prioritizing high-return investments and maintaining a focus on production efficiency, oil and gas companies have worked to ensure robust financial performance and retained investor trust. Over the last four years, the industry’s capital expenditures have increased by 53%, while its net profit has risen by nearly 16%.3 In fact, oilfield services reported its best performance for the 2023 to 2024 period in the past 34 years.4 Additionally, some companies are engaging in increased investments in low-carbon technology projects to help balance the risks associated with the traditional oil and gas market. These investments will likely help companies position themselves as key players in the future energy landscape.

As 2025 begins, the market could be expected to experience interest-rate cuts, clarifying some of the previous uncertainty about the US Federal Reserve’s stance on rate cuts. In addition to the 75- to 100-basis-point reduction in 2024, the Fed foresees the scope for a total of close to 150-basis-point rate cut in 2025 and 2026.5 Moreover, some energy policy changes can be expected under a new administration following the 2024 US elections. Additionally, there is still global uncertainty regarding the trajectory of OPEC+ cuts and potential disruptions to energy trade flows. Despite these uncertainties, the oil and gas industry’s capital discipline, increasing customer centricity, and investments in new technologies are poised to drive a robust 2025. The following five trends are expected to play a significant role:

1. The Permian Basin: Repositioning for growth

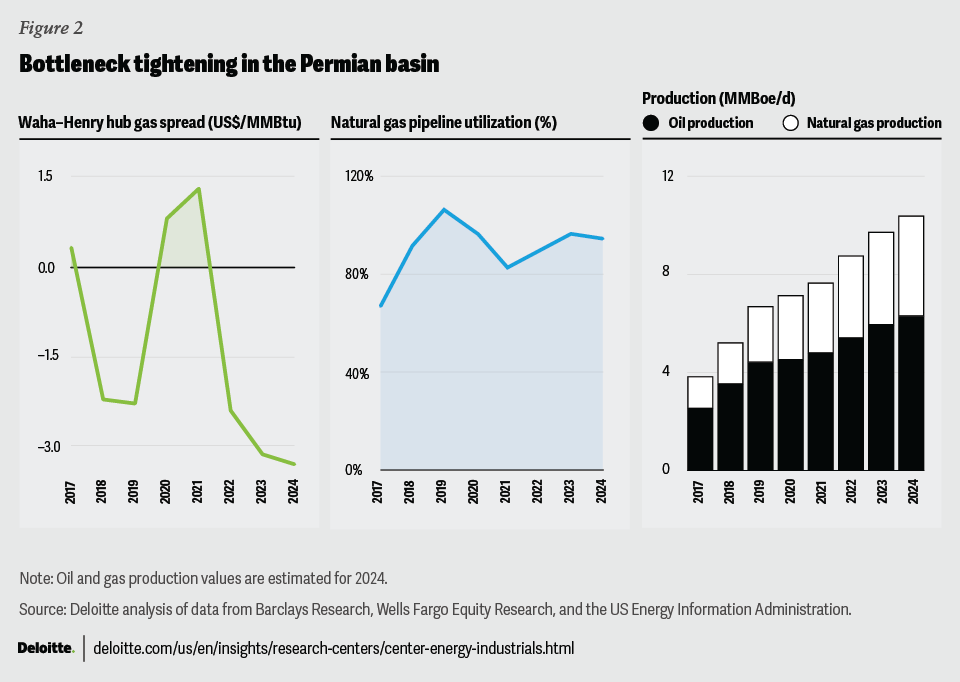

The Permian basin is synonymous with US oil and gas production, contributing to 46% of US crude oil production, 20% of US gross natural gas production, 51% of rig count activity, and nearly 40% of the total mergers and acquisitions deal value in the US upstream sector in 2024.6 In fact, the basin’s oil production is growing at an annual average of 485 kilobarrels per day (kbbl/d)—equivalent to Colombia’s annual consumption—highlighting its importance in both domestic and international energy markets.7 But with great significance and rapid growth come formidable challenges (figure 2).

Waha woes

Relative strength in crude oil prices—the US oil-to-gas ratio is at a 10-year high of 40:1—has incentivized leading operators in the Permian basin to prioritize oil operations, resulting in an abundance of associated natural gas production.8 Additionally, large shale operators are exploring tier 2 and tier 3 acreage—which are generally much more gas-heavy—to help offset flattening production from their tier 1 acreage, unlock invested capital, and test new productivity and cost-efficiency measures.9 The result: The Permian Basin’s natural gas production has nearly doubled to 25 billion cubic feet per day (Bcf/d) in the last five years.10 However, the takeaway capacity of natural gas remains highly constrained in the basin, with natural gas pipeline utilization exceeding 90% in 2024, pushing regional Waha Hub spot prices below zero.11 As of early September 2024, prices at the Waha Hub were below zero for 46% of trading days in 2024, including every day since July 26.12

However, new midstream infrastructure, such as the 2.5 Bcf/d Matterhorn Express Pipeline, which began transporting natural gas in October 2024, is expected to alleviate some bottlenecks.13 In addition to Matterhorn, three new Permian Basin pipeline projects with a combined capacity of 7.3 Bcf/d are in various stages of development and are expected to be completed between 2026 and 2028.14 However, any slowdown in shale production growth over the next 6 to 18 months, especially if large shale operators reduce their drilling and completion activity due to weak prices, could lead midstream companies to shift their focus toward optimizing existing pipelines, rather than constructing new ones. Some major midstream companies have already highlighted this cautious investment approach for the Permian Basin.15

Stable production and timely completion of pipeline projects can help reduce volatility in natural gas prices and support the broader liquified natural gas (LNG) export market, but also meet the rising power demand driven by increasing numbers of data centers. It is projected that data centers will consume 9% of US electricity by 2030, driving over 3 Bcf/d of new natural gas demand by the end of the decade.16

Growing responsibly

Over the past decade, US upstream companies have prioritized capital discipline, digital transformation, and strategic acquisitions to grow profitably. This strategy contributed to a 7% rise in their net income from 2014 to 2023, despite an 18% drop in oil prices.17 In the coming year, companies will likely adapt their strategy to address challenges including low oil prices, peaking productivity gains (with rigs in the Midland basin having drilled an average of 47 miles of horizontal lateral wells over the year to June 2024), an all-time low inventory of drilled but uncompleted wells at 4,500, and the forecasted resurgence in global liquids consumption that is expected to increase by 1.5 MMbbl/d (million barrels/day) in 2025.18 Against the backdrop of major acquisitions, eyes will be on US shale majors to share and execute their “what’s next?” strategy for the Permian Basin.

Consolidating acquired assets and leveraging investments in new technologies, while benefiting from strengthening natural gas prices due to new pipelines, will likely support the profitable growth strategy of shale majors in 2025. However, a bigger prize could be in how shale majors rethink their tier 2 and tier 3 acreage across shale basins. By adopting new refracturing, enhanced oil recovery, and innovative completion techniques, they have the potential to enhance their capital returns and well productivity. Development in tier 1 acreage is growing by 5% to 10% annually in the Bakken Shale Play, while tier 2 acreage is growing by 20% annually.19

Additionally, by implementing new water-treatment protocols and oil-skimming technologies, shale majors may also strive to reduce their environmental footprint and costs associated with managing produced water. In fact, the industry’s cost of reusing water now stands at US$0.15 to US$0.20 per barrel, which is cheaper than the disposal cost of US$0.25 to US$1 per barrel.20

M&A frontiers

With nearly US$136 billion in deals since 2023, the upstream sector has seen major M&A consolidation in the Permian Basin.21 However, higher acreage prices and limited high-quality acquisition targets in the basin, combined with favorable financial markets, may lead to increased drilling and buying activities in other basins, primarily Eagle Ford and Bakken. In fact, the availability of acquisition targets and refracturing opportunities, without significant infrastructure constraints, makes these basins strong rotational candidates for the short to medium term.22 In the first three quarters of 2024, these two basins have already seen a buying interest of around US$7.7 billion.23 This competition, or rotation, can be necessary and healthy. Not only can it reduce the concentration risk on the Permian Basin, but it can also bridge the valuation gap across the shale basins, keep the overall production profile of US shale basins stable, and help bring back private equity or venture capital players. This is especially true in the US upstream sector, where public company consolidations offer more favorable valuations for undeveloped inventory, compared to private equity buyouts, with premiums remaining modest at 10% to 15%.24

2. Oilfield services: Emerging from the shadows

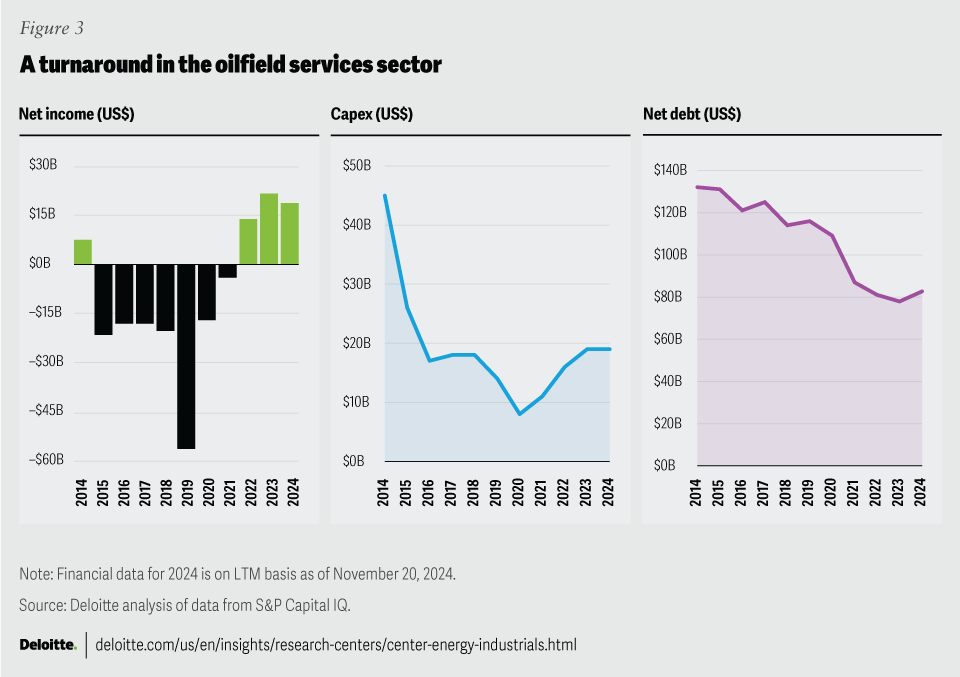

In the last 10 years, the oilfield services sector has lagged behind the rest of the oil and gas industry, as efficiency and productivity gains in the shale market reduced the business and margins of this sector. Simply put, the sector became a victim of its own technological success for its customers, reporting US$155 billion in losses between 2015 and 2021.25 However, there are visible signs of a reversal in fortunes. Over the last three years, the sector’s net income has cumulatively exceeded US$50 billion. Currently, its capex is at the highest level, while net debt is at one of its lowest points since 2016 (figure 3).26 Similarly, oilfield services M&A deal-making within the first nine months of 2024 reached US$19.7 billion, the highest since 2018.27 In fact, oilfield services companies seem to be repeating what their upstream shale customers did years ago—growing profitably without a commensurate increase in capex. There are several drivers of this change, with each having different implications for companies in the upcoming year.

Innovating the core

The sector’s transformation can be attributed in part to a strategic blend of innovation and cost-reduction measures. Oilfield companies are leveraging their digital capabilities to deliver high-margin, lower-carbon solutions to their customers. For example, SLB is developing an all-electric subsea infrastructure aimed at reducing costs, improving efficiency, and lowering carbon emissions.28 Concurrently, these companies are often implementing various cost-reduction measures, including restructuring operations, exiting nonprofitable business lines, implementing variable cost management programs, and streamlining corporate structures. These initiatives have yielded substantial financial benefits—for instance, NOV Inc. reported US$75 million in annualized cost savings and Weatherford reported a 160-basis-point increase in gross margin.29 By recalibrating its strategies, the sector has navigated the challenges posed by reduced demand for certain services, while continuing to drive efficiency and maintain capital discipline.

Transitioning into energy technology

Some oilfield services companies are transitioning into “energy technology companies” by diversifying their portfolios to include low-carbon ventures such as carbon capture and hydrogen generation. They are building niche capabilities in these areas and expanding their customer base, thus decoupling their business from the energy industry’s cyclicality. For example, Baker Hughes is developing supercritical carbon dioxide turboexpanders to support NET Power’s low-cost, emission-free, carbon-capturing power system.30 Similarly, SLB is developing an integrated direct lithium-extraction solution that could be significantly faster than traditional methods, while lowering resource usage, thereby possibly reducing operational costs.31 Additionally, cross-sector partnerships are being leveraged to develop advanced technologies—for instance, SLB and Baker Hughes are collaborating with Genvia and Air Products, respectively, to create new solutions for producing clean hydrogen.32 These new technology solutions are expected to drive the long-term growth of oilfield services companies, with companies like Baker Hughes targeting approximately US$6 billion to US$7 billion in new orders by 2030.33

Leveraging M&A offshoots

A period of financial strength amid an easing macroeconomic environment and a highly fragmented sector is generally followed by consolidation. SLB’s acquisition of Champion X in an all-stock transaction valued at US$7.8 billion, the largest deal within the sector, focused on expanding presence within the less cyclical and growing production and recovery space that covers the asset life cycle from completion through decommissioning.34

Similar synergistic considerations were also at play with the acquisition of Parker Wellbore by Nabors Industries Ltd., where Parker’s casing-running business complements Nabors’ tubular services.35 Considering their large upstream customers have completed megamergers in the Permian region in 2023 and 2024 and will require scalable and tech-powered oilfield services, many small-sized companies could seek exits at favorable valuations, spurring consolidation across the sector. Meanwhile, buyer interest for drilling rigs increased in 2024 with deal value reaching US$3.8 billion, its second-highest level since 2018.36

3. National oil companies: Breaking barriers

National oil companies (NOCs), particularly those in the Middle East and members of OPEC, face challenges in the near term, including: 1) balancing crude oil supply and demand and maintaining stability in prices; 2) fulfilling COP28 commitments to reduce the industry’s carbon footprint; and 3) helping to sustain their economies if oil prices remain below their fiscal breakeven for 2025.37

Navigating these challenges is not expected to be easy for NOCs. However, they now operate in a unique ecosystem that may enable them to innovate differently and potentially faster. Many Middle Eastern nations (including Saudi Arabia, Qatar, Kuwait, and the United Arab Emirates) have started to diversify their economies, and their regulatory environments support a balanced energy transition.38 Aligning all stakeholders could be more straightforward for some NOCs than for integrated oil companies (IOCs), as in some cases, governments are both investors and decision-makers for NOCs. Additionally, government-backed financing and vertical integration can help facilitate financial stability and mitigate risks. In fact, over the past three years, Middle Eastern NOCs have entered into at least 20 strategic alliances, including with logistics and technology-related firms; signed M&A deals worth US$4.8 billion for various assets ranging from refining to shipping and retail distribution; and taken equity ownership in cross-border projects, such as LNG export terminals in the United States.39

Strengthening the core

OPEC+ has cut output by a total of 5.86 MMbbl/d, or about 5.7% of global demand, in a series of steps agreed since late 2022.40 OPEC+ plans to restore roughly 2.2 MMbbl/d in monthly tranches in 2025.41 A few NOCs are heavily investing in increasing hydrocarbon production capacity and developing the associated midstream and downstream infrastructure. ADNOC, for example, has set a target to increase crude oil production capacity from the current 3 MMbbl/d to 5 MMbbl/d by 2027, moving up its earlier 2030 target by three years.42 Additionally, some NOCs are also making changes in their project, partnership, and go-to-market strategy. Saudi Aramco and ADNOC are investing in mega refining-chemical-low-carbon integrated projects, partnering with technology firms to boost their digital capabilities, and adopting more customer-centric strategies in their operations.43 ADNOC reports generating US$500 million in value by deploying AI solutions through its digital partnerships in 2023.44

Building new capabilities

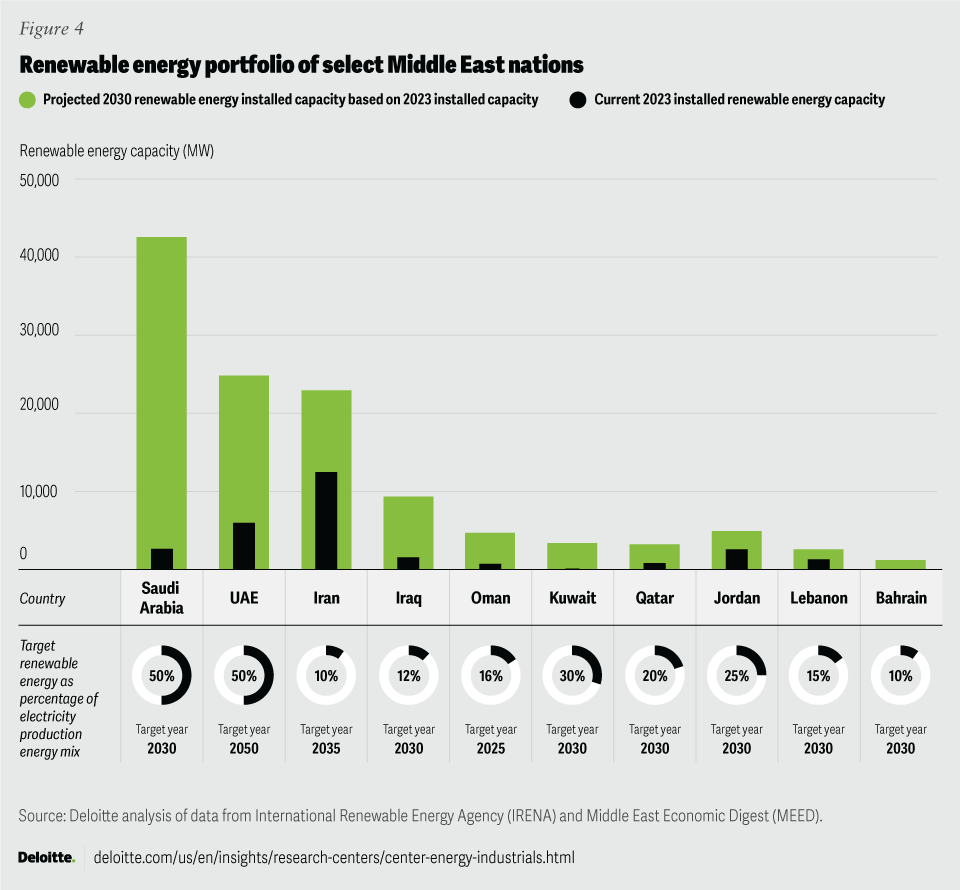

In the wake of COP28, some Middle Eastern nations are working to scale technologies such as carbon capture and storage and hydrogen (figure 4). The United Arab Emirates, recently approved two carbon capture, utilization, and storage projects designed to capture emissions from gas-processing plants and also aims to produce 1.4 million tons of green and blue hydrogen annually by 2031.45 Oman and Qatar are also advancing in hydrogen production, with Qatar planning the world’s largest blue ammonia plant by 2026.46 The United Arab Emirates announced the world’s largest single-site solar park, and Saudi Arabia’s NEOM project represents a US$500 billion investment in a city powered entirely by renewable energy.47

Managing their finances

To help fund their expansion and diversification, NOCs are exploring various financing mechanisms like public-private partnerships, M&A, and green bonds. The United Arab Emirates has committed to a US$30 billion global finance fund, with its banking sector aiming to mobilize US$270 billion by 2030 for green finance.48 Diversification into renewable energy such as solar and wind power has provided economic stability and effectively reduced the fiscal breakeven burdens for the companies. At the same time, sovereign wealth funds in the Middle East, managing US$3.8 trillion in assets, are pivoting investments toward green energy and decarbonization efforts.49

Put simply, NOCs appear poised not only to support the growth in global energy demand, which is expected to grow at a compound annual growth rate of 1.3% by 2030, but also to help lead the charge in scaling new technologies over the next few years.50

4. Refining and marketing: Navigating under uncertainty

The refining and marketing sector is at a crossroads, with modest long-term growth projections for traditional fuels and significant profitability challenges in the newly invested renewable fuels segment. Global demand for road transportation fuels (gasoline and diesel) is projected to increase by only 1% between 2024 and 2034; however, 2025 is projected to be a year of strong growth following monetary easing worldwide.51 Renewable fuels, on the other hand, are facing an oversupply in the United States, driven in part by lower-than-expected renewable volume obligations set by the US EPA and cheap imports from Europe.52 Additionally, profitability is low due to falling renewable credit prices, with average D4 RIN prices dropping by 63% between January 2023 and September 2024.53 The electric vehicle market is facing similar challenges, with growth rate falling from above 30% year over year in 2023 to less than 13% year over year in the first half of 2024.54

The result: 2024 turned out to be one of the weakest years for the sector. The WTI-US Gulf Coast and Oman-Singapore crack spreads plummeted by 83% and 64% year over year to reach US$12/bbl and US$2/bbl in September 2024, respectively.55 Moreover, the addition of new refineries, particularly in Asia and the Middle East, alongside the completion of refinery maintenance activities, would likely result in higher supply and suppressed crack spreads in the coming year.56 Pure-play independent refiners have reported up to 75% year-over-year declines in their operating profit before tax for their renewable diesel segment in the second quarter of 2024.57 Consequently, some analysts believe that a considerable number of site closures could curb almost 22% of global refining capacity.58 In the face of this uncertainty, refiners may need to adopt a strategic approach to navigate such challenges and transition effectively to low-carbon alternatives.

Optimizing and integrating value chains

Faced with challenges across both traditional and new low-carbon businesses, refiners could boost their resilience and create new value by optimizing their existing hydrocarbon value chains and integrating new low-carbon value chains with the existing business. Optimizing existing hydrocarbon value chains, from feedstocks to final products, may require leveraging digital technologies to integrate people, processes, and assets across an organization’s functions, businesses, and geographies. This is essential to break down functional silos, improve value chain visibility, and minimize value leakage across various functions and processes. For example, an integrated artificial intelligence/machine learning solution could facilitate cross-product, cross-business analytics that shape marketing, supply, and trading decisions in conjunction with operational and commercial constraints to maximize key outcomes.

Integrating low-carbon technologies with traditional operations, where synergistic, rather than treating them differently, is another way to unlock new areas of revenue expansion and cost synergies for companies. To achieve this, companies may need to repurpose their facilities, leverage shared utilities, adapt existing distribution networks, scale demand by targeting large industrial consumers (primarily for hydrogen, ammonia, etc.), and forge new cross-industry partnerships.

Some downstream companies, such as Chevron and Marathon Petroleum Corporation, have formed partnerships with agricultural firms—Chevron with Corteva and Bunge and Marathon with ADM.59 These collaborations can help secure a consistent feedstock supply and strengthen their biofuel supply chains. Meanwhile, policy support can be crucial in stimulating demand for low-carbon fuels. For instance, the United Kingdom and the European Union have implemented a 2% sustainable aviation fuel mandate from 2025 onwards.60

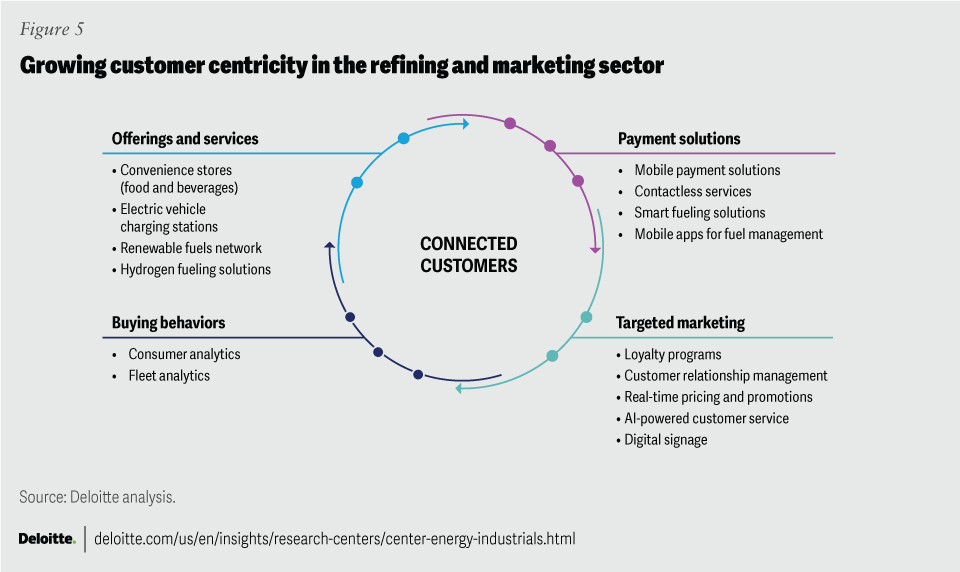

Reaching connected customers

Refining and marketing companies have enhanced the efficiency of and sales from their retail fuel and convenience outlets by integrating digital technologies. The integration of AI and the Internet of Things has enabled the development of smart fuel management systems, thereby optimizing inventory, reducing waste, and enhancing supply chain efficiency. Companies are also maintaining a strong focus on customer engagement by leveraging digital technologies and data analytics to understand consumer behavior, optimize pricing, and tailor marketing efforts (figure 5).

Innovations for convenience continue with connected car payment solutions—for instance, Shell’s The Shell App and BP’s BPme app support phone-based payments from within the car.61 As a result, over half of merchants (53%) that accept payments at the point of sale are planning to implement or are considering connected car payment options.62 These options may also extend to alternative fuels like hydrogen, renewable diesel, and compressed natural gas. However, such increased digitalization necessitates enhanced security infrastructure. In fact, some large oil companies are already testing biometric authentication and implementing robust digital protocols to protect digital payment systems and customer data.63 With electric vehicle consumers spending more time at fuel retail stations compared to their gasoline counterparts, such enhanced convenience solutions can help boost the sale of ancillary products including foods and drinks.64

5. Global energy policies: Government priorities to come into play

The year 2024 marked a significant milestone for global policy, with over 70 countries—representing more than half of the world’s population—holding national elections.65 Energy policy emerged as one of the critical issues, with voters assessing the success of their national energy strategies. The outcomes of these elections could influence the pace of the energy transition across various regions, shaping policy approaches to fossil fuels and low-carbon alternatives. What could be the net impact on the energy transition? While it may be too early to provide a definitive answer, analyzing key policies and recent developments across select geographies can offer guidance on the potential direction of energy transition in the coming year.

United States of America

President-elect Trump’s energy priorities include energy independence and lowering energy costs. His proposals seek to increase production of oil and gas, in addition to other energy sources such as nuclear.66 Some of the proposals can be carried out by executive action or through the regulatory process, while others, such as changes to legislation, would require congressional action. Some steps the next administration plans to take include measures to streamline permitting and expedite environmental approvals, in addition to lifting the Biden administration’s pause on new liquified natural gas export permits.67 Other potential policy changes may lead to some uncertainty about the US energy landscape and future regulatory environment.68 Meanwhile, changes in certain tax policies could also impact the industry, particularly by affecting the cash flows available to meet business and shareholder obligations.69

Europe

In Europe, energy policies are increasingly focused on clean energy adoption, with the Renewable Energy Directive III aiming to raise the share of renewable energy in total consumption from 23% in 2022 to 42.5% by 2030.70 This directive also targets advanced biofuels, biogas, and renewable fuels of non-biological origin (e.g., hydrogen) to constitute 1% by 2025 and 5.5% by 2030 of fuel consumption in the transportation sector.71 By October 2025, EU member states are expected to transpose the Energy Efficiency Directive into national legislation, and a 2% sustainable aviation fuel mandate in the aviation fuel mix will commence in 2025.72 The newly elected Labour party in the United Kingdom has announced plans to lift the ban on offshore wind development and has proposed a 78% tax rate on North Sea oil and gas producers.73

Adding to the complexity, certain EU policies, such as the proposed tariffs of up to 45% on Chinese EVs, can increase costs.74 These rising costs could face resistance from customers and contribute to increased uncertainty regarding future hydrocarbon demand. As Europe navigates these shifts, the balance between advancing clean energy initiatives and managing economic and political realities will be crucial.

Emerging economies

Despite concerns over muted hydrocarbon demand in 2024, China’s recent monetary stimulus measures are expected to boost economic growth and petroleum consumption, with Chinese liquid fuel consumption projected to grow by 0.3 million b/d in 2025.75 China’s third plenum session emphasized the supply security of strategic natural resources, likely increasing state purchases of crude oil, natural gas, and strategic metals.76 Additionally, China has doubled its EV subsidy, which could potentially lead to EVs accounting for 50% of new vehicle sales domestically by 2025.77

In India, final energy demand is projected to double between 2020 and 2070.78 The country remains committed to renewable energy, ranking fourth globally in renewable power additions.79 The incumbent government’s third term is expected to accelerate India’s energy transition, although challenges remain in phasing out coal-based power plants, with coal consumption expected to increase by 6% year on year in 2024.80

Similarly, Brazil, in addition to being one of the top oil producers in the Americas, continues to lead in renewable energy adoption, generating nearly 90% of its electricity from renewable sources.81 The country is also likely to continue increasing its blending mandates for ethanol and biodiesel, with a 15% target for the latter by 2026.82 Moreover, the New Industry Brazil policy aims to increase the share of biofuels in the transport energy mix to 50% by 2033.83

Put simply, energy policies in some economies are increasingly geared toward creating demand for new low-carbon technologies. Meanwhile, emerging economies are implementing energy policies intended to address both demand and supply to develop comprehensive energy solutions. As a result, energy regulations are increasingly looking at the whole energy basket in totality rather than favoring one energy source over another.

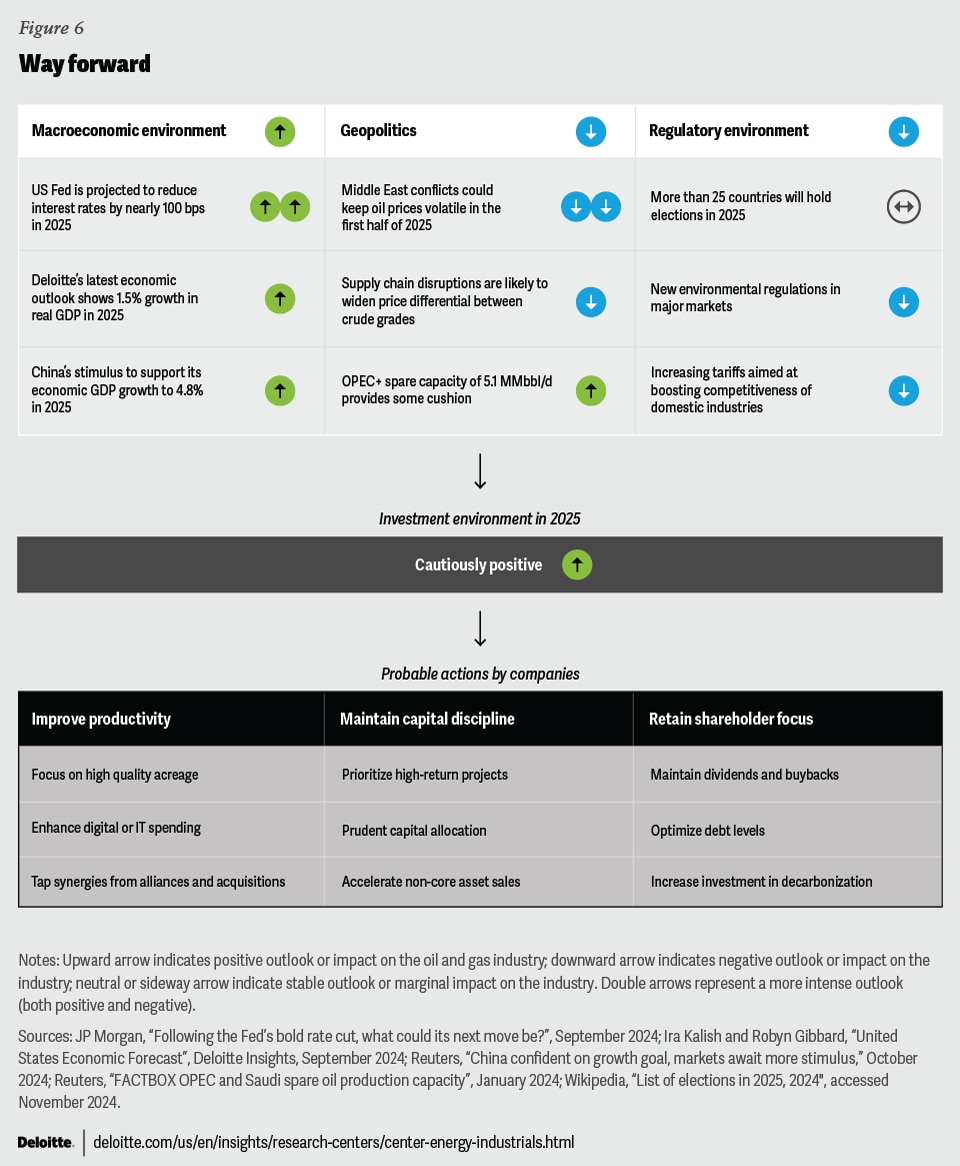

The way forward: Oil and gas companies can anticipate a balancing act ahead

As we look ahead to 2025, an interesting interplay between the global economy, industry dynamics, and corporate strategies will likely play out. Although the oil and gas industry is no stranger to disruption—and recent history suggests it has emerged stronger from such challenges—the coming year could be pivotal due to easing monetary policies, geopolitical tensions, and postelection energy policies. With oil prices projected to remain range-bound amid a cautiously optimistic investment environment, oil and gas companies are expected to focus on strategic capital allocation, technological innovation, and maintaining capital discipline.

- State of the global economy: The confluence of easing monetary policies amid global slowdown fears, rising geopolitical tensions impacting financial markets and energy trade flows, and the shaping of energy policies following the 2024 elections in more than 70 nations could make 2025 a pivotal year for the global economy and energy markets. Analysts project oil prices to hover between US$70/bbl and US$80/bbl in 2025, with a potential uplift of US$10/bbl if geopolitical tensions escalate.84

- Investment environment: This projected state of the economy is expected to create a cautiously optimistic investment environment for the industry in 2025. Companies will likely embrace strategic capital allocation to high-return projects and technological innovation as their strategy. Analysts project a modest 0.5% yearly increase in the industry’s capital investment in 2025.85

- Probable actions by companies: Oil and gas companies are likely to stick to their existing playbook of maintaining capital discipline and shareholder payouts, focusing on technology-driven productivity and cost savings, attaining synergies from their recently completed acquisitions, and managing risk through diversification and integration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}