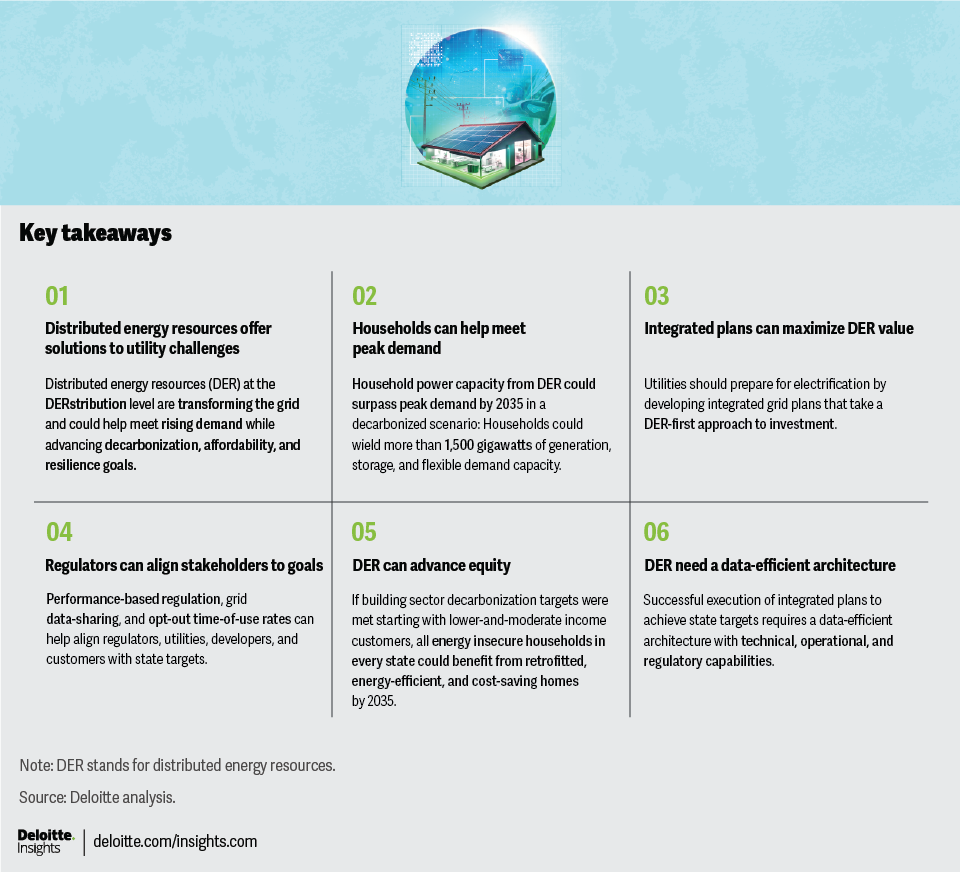

Households transforming the grid: Distributed energy resources are key to affordable clean power

Distributed energy resources like solar panels, EVs, and smart thermostats can help utilities meet rising peak demand and decarbonization goals to achieve net-zero electricity

Christian Grant

Craig Rizzo

Kate Hardin

Carolyn Amon

Household energy use is transforming, placing utilities at the center of two important trends—decarbonization and customer affordability. Individual purchases of smart home appliances, solar and storage systems, and electric vehicles (EV) are exponentially increasing the number of distributed energy resources (DER), which can generate, store, or flexibly draw energy from the grid. This partial decentralization of production and storage is changing the historical unidirectional power flow from utility power plants to customers as bidirectional DER networks multiply at the distribution grid edge, or “DERstribution.” Commercial, industrial, and other customers are part of this DERstribution, but households form the most distributed and versatile customer segment, with the greatest capacity and equity potential.

Using DER, households can now pursue their own financial, operational, and environmental priorities, while utilities still have an obligation to serve them. However, if unmanaged, these resources could complicate utilities’ efforts to balance decarbonization with affordability. But if utilities successfully engage customers, they could harness DER to help meet peak demand with clean energy and provide essential grid services, while equitably sharing revenue and resilience benefits with households and placing downward pressure on rates. This is the case utilities should make to regulators to secure backing for DER integration plans.

The potential role of quickly deployable DER is likely to become even more important as permitting and interconnection queues for utility-scale resources lengthen, compounding cost and resource pressures that have intensified over the past year due to:

- Growing load: Grid planners who had assumed flat demand for decades increased projections in early 2023 and ended the year doubling their five-year load forecast to 4.7%.1 Estimates have continued rising since, as utilities reassess demand from domestic manufacturers, artificial intelligence data centers, cryptocurrency miners, and green hydrogen producers, in addition to demand from transportation and building electrification.

- Growing climate impacts: In 2023, the warmest year documented,2 a record US$28 billion were spent on weather and climate disasters in the United States.3 Wildfire risk areas grew and spread to new states,4 exposing more utilities to billion-dollar litigation risk.

- Growing mission: In addition to its core mission to deliver safe, affordable, and reliable power, the electric utility is expected to play an increasingly important role in helping achieve state decarbonization, resilience, and equity goals.

- Growing regulatory pushback: Some regulators have challenged utility capital expenditure plans to meet new goals and lowered return on equity, as they remain laser-focused on limiting rate increases that would disproportionately impact low-income customers.

Enabling households to help address the pressures arising from these challenges requires utility investment in equitable deployment of DER and the digital technologies to harness them. Utilities should understand residential DER trends over the next decade while considering state decarbonization targets, and how grid planning, the regulatory compact, and data architecture must change to optimize the DERstribution system transforming the grid.

The challenges of matching variable energy supply to variable—and growing—demand

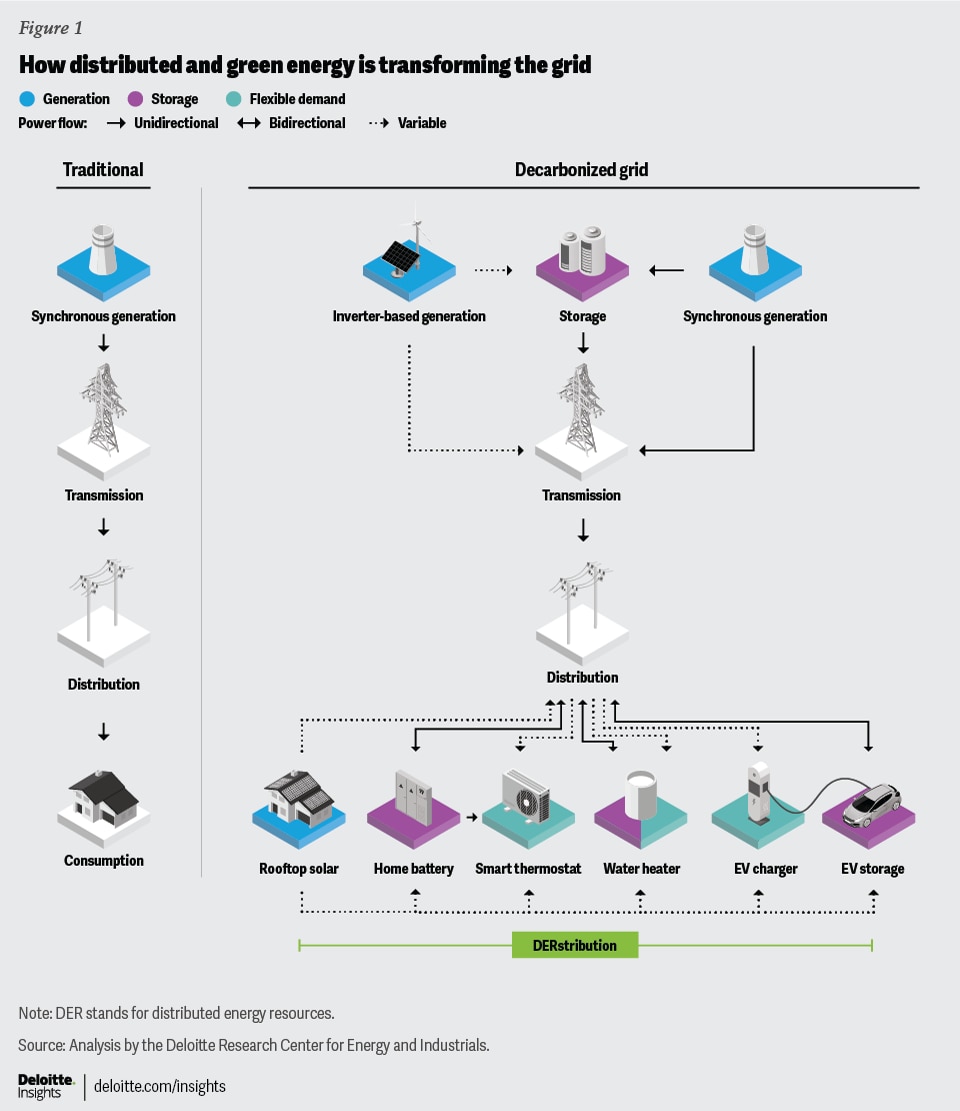

Decarbonization and decentralization are increasing grid complexity, often making it harder for utilities to match supply and demand. What was once a predictable flow from large, synchronous generators (such as coal, gas, nuclear, and hydroelectric plants), today includes inverter-based technologies that intermittently generate (namely solar and wind) and store electricity (figure 1). At the DERstribution level, these technologies are reflected in rooftop solar and home batteries, few of which are utility-owned. At the intersection of the power, building, and transportation sectors, DER-equipped households also include major home appliances with smart controls, such as home heating, ventilation, and air conditioning (HVAC) systems and water heaters, and mobile DER such as EVs that owners intermittently plug into their homes. Because DER can generate, store, or flexibly draw or discharge power to the grid, the demand from households is becoming increasingly variable.

At the same time, decarbonization is increasing and shifting peak demand. Achieving the Biden administration’s target for a fully decarbonized grid by 2035 with renewables could double peak demand to 1.4 terawatts by 2035.5 Demand now typically peaks on hot summer afternoons due to air conditioning use across the United States.6 But as households switch from gas to electric heating, it will likely peak on winter mornings and evenings. Depending on their current generation mix and climate, most states are expected to become winter or dual peaking systems by 2035.7

Meeting higher peak demand is costly, often requiring the deployment of fossil-fueled peaker plants that are idle most of the time but built to ensure utilities have enough capacity to quickly start up when electricity demand spikes.8 If utilities meet demand using variable renewables, generation and storage build-outs should be much larger because only a fraction of intermittent capacity counts toward resource adequacy requirements, and solar generation does not match the load profile of winter peaking systems.

The bulk power system is constrained due to fossil fuel plant retirements and lengthy project timelines for new power plants to connect to limited transmission infrastructure, now stretching to five years. In 2023, the backlog of mostly utility-scale renewables and storage awaiting grid interconnection grew to 2.6 terawatts9—more than twice the current installed capacity. Though not all of that will be built, the delays complicate project deadlines and financing arrangements.

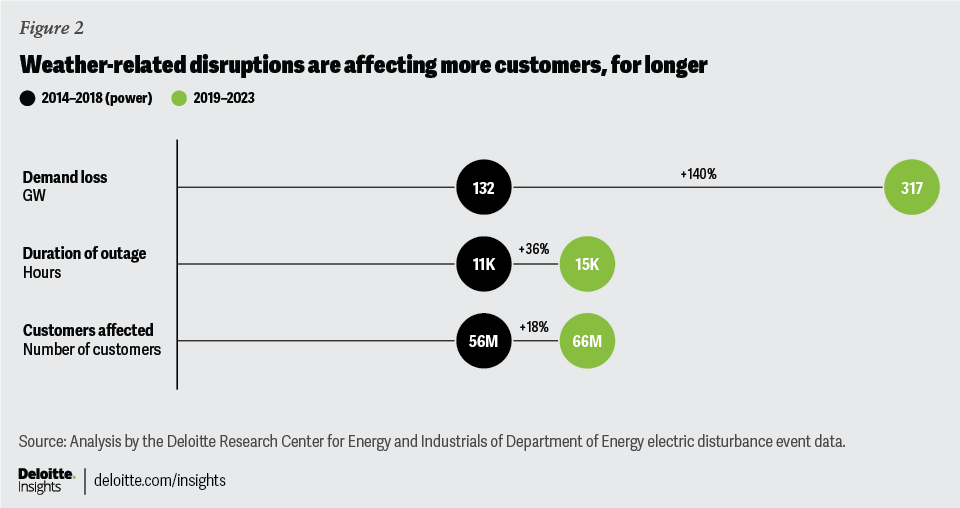

Climate impacts compound these challenges. The impact of electric disturbances due to weather events has significantly increased over the past few years, and they mostly hit the distribution grid, where 90% of outages originate.10 Demand losses have more than doubled between 2014 and 2018, and over the past five years, the disruption of 317 gigawatts of electricity impacted 66 million customers for longer durations (figure 2).11

The grid imperative to always match supply and demand is a much taller order in this context. Meeting it requires hardware, software, and integration controls to prevent reliability issues.

The opportunity of harnessing DER to meet flexible and peak demand needs

Utilities can harness DER to help address these grid flexibility and peak demand challenges. DERstribution can enable responsiveness to supply and grid conditions, making demand coequal to supply as a flexible resource. For example, grid operators sometimes curtail renewable generation that exceeds demand, thereby wasting this clean energy. But DER with storage capacity, such as home batteries, EVs, and water heaters, can soak up excess renewables by charging and heating up when renewable generation is abundant, and using the stored energy when the sun sets or the wind subsides. Conversely, in the event of a generation shortfall during extreme weather, grid-interactive households can adjust their thermostats and delay hot water heating or EV charging for a short period of time to help prevent a blackout.

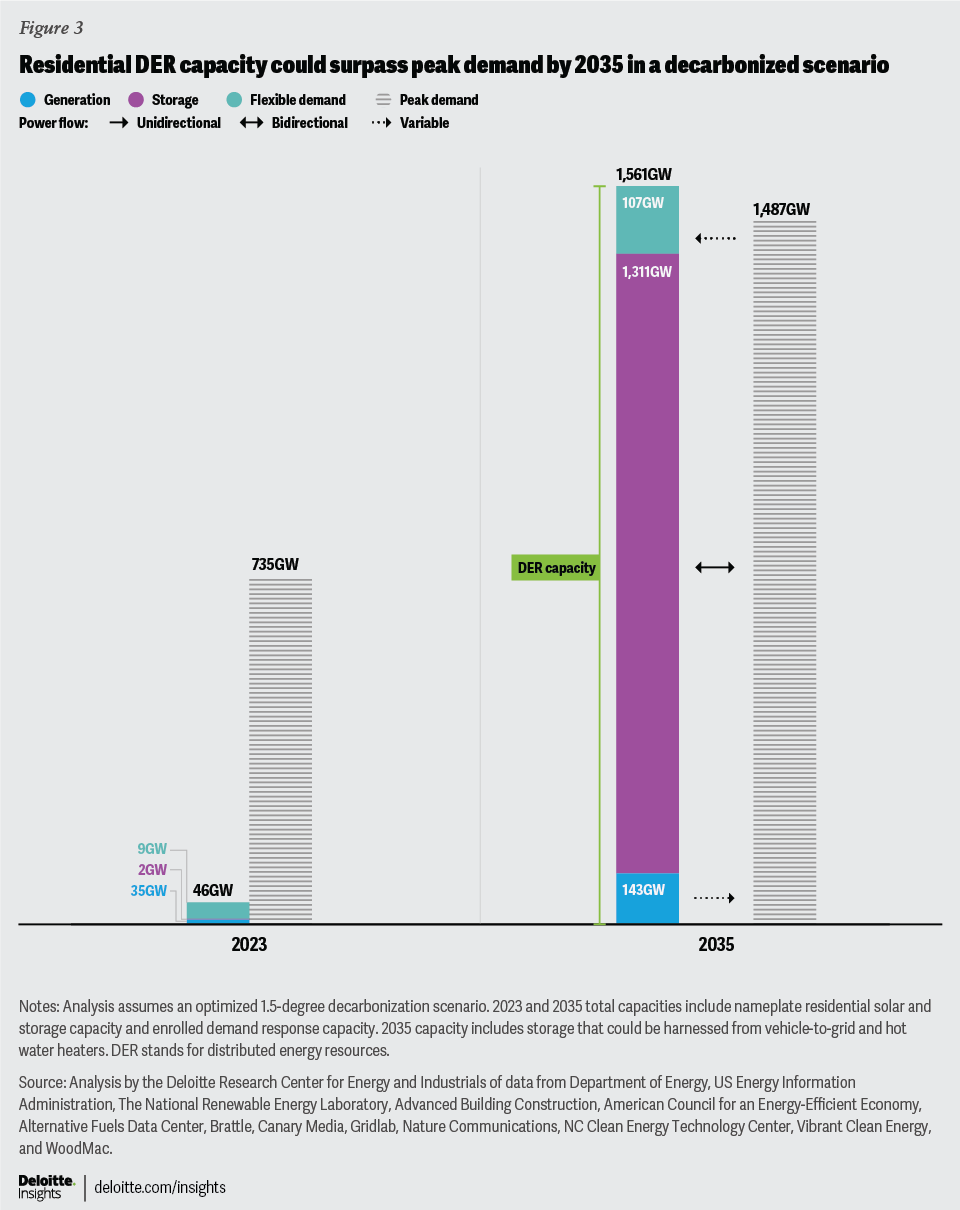

Rapid DER deployment could outpace utility-scale capacity by 2035 and help meet higher peak demand. Unlike inflexible loads that are driving up peak demand and grid expansion, residential electrification creates a load that could potentially serve itself by 2035 (figure 3). For example, load growth from buildings can be offset by energy efficiency upgrades to envelopes and appliances, as well as solar-plus-storage deployments. This can be especially true for households shifting from electric resistance space and water heaters to their highly efficient heat pump counterparts. Zero and positive energy homes are so efficient that they can generate as much or more renewable energy as they consume.12

At one end of the spectrum are DER with low deployment but high capacity, such as EV storage harnessed via bidirectional vehicle-to-grid (V2G) charging technology. EV capacity potential alone could meet peak demand in 2035, but only if the fledgling V2G tech achieves widespread adoption.13 EVs could also serve as backup power sources for homes to ride through grid outages, especially when rooftop solar is not generating.14 The automotive industry’s recent adoption of a new V2G standard may unlock the capability for EVs to digitally send utilities all the data needed to enable controlled bidirectional power flows and payments to EV owners.15

On the other end are DER with high availability but limited capacity, such as thermostat-controlled HVAC systems. Almost nine out of 10 households have thermostats, most of which are programmable; a fifth are Wi-Fi-enabled “smart” thermostats that can automatically optimize temperature settings.16 When aggregated, thermostats can deliver the same capacity reduction that a peaker plant would supply.17 Since DER have different penetrations, capabilities, and load profiles, combinations of different types of DER could help better adapt to changing seasonal and intraday peak profiles.

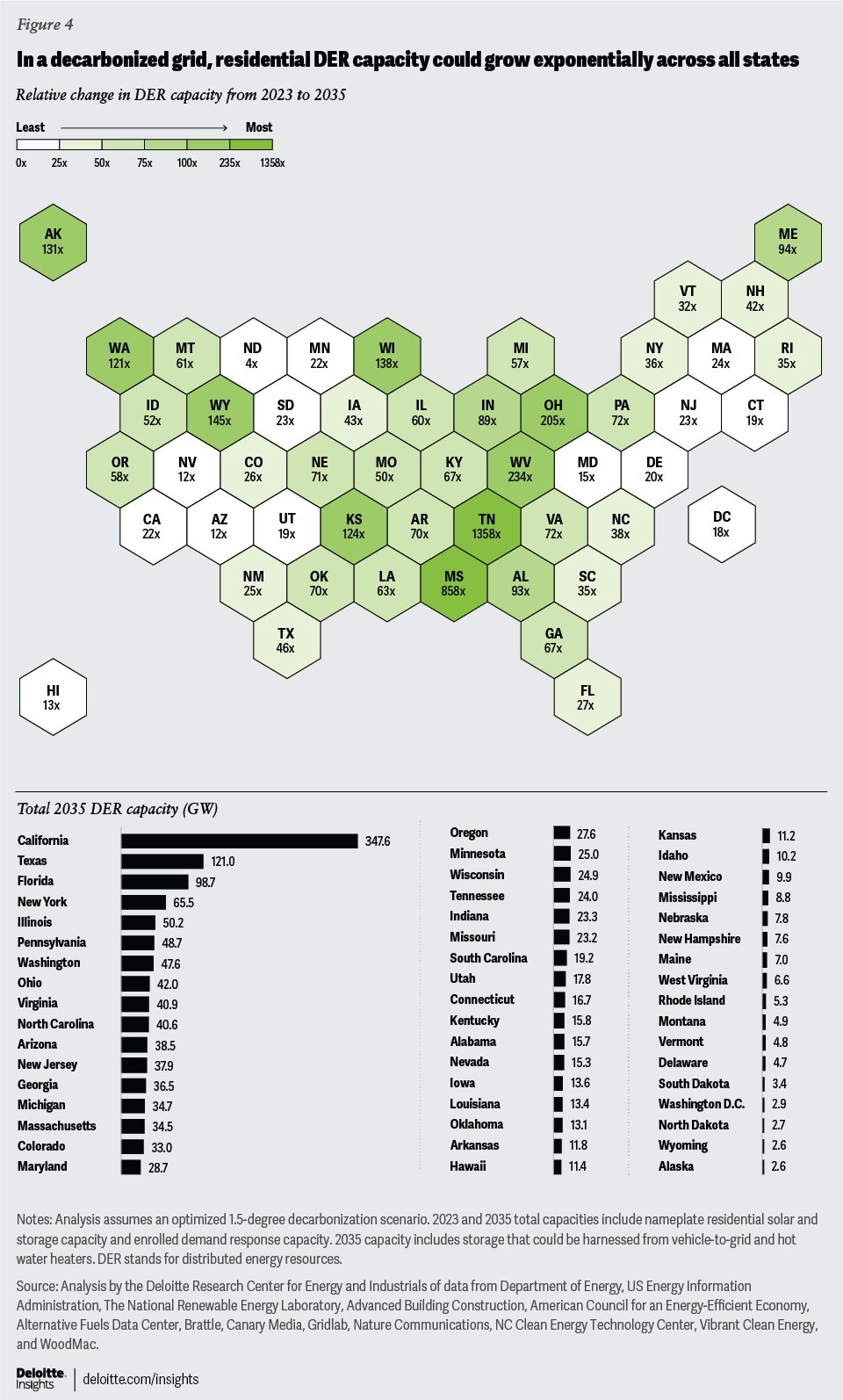

Unlocking this potential requires advanced digital technologies to enable active management but could deliver cost savings to utilities and customers. While controls to manage DER in real time require significant utility investment, DER management includes least-cost mechanisms such as time-of-use (TOU) rates and demand response for programmable thermostats that have been operating for decades with simple controls. Studies commissioned by the states of California and New York show that managed electrification could lower the cost of distribution upgrades needed through 2035 by more than US$30 billion in each of these states.18 That’s because building efficiency measures and smart devices to manage energy usage and smooth EV charging could reduce capital spending on new substations, transformers, feeders, and other distribution equipment (figure 4).

Ways to plan for DERstribution

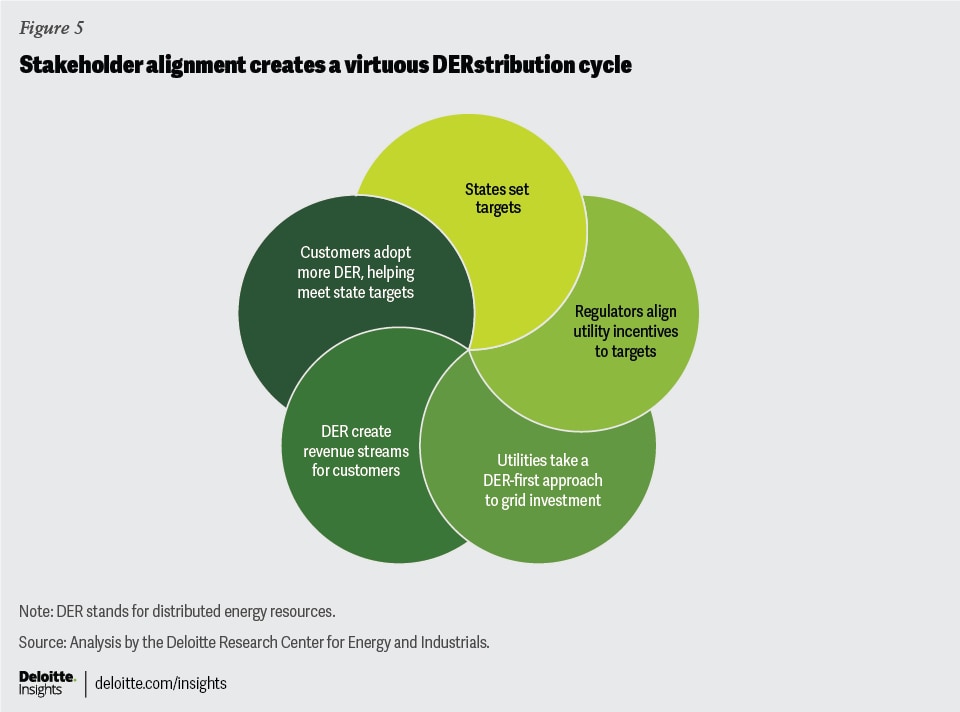

To help manage electrification, utilities should prepare for it with integrated DER plans developed in close collaboration with stakeholders across the DERstribution network (figure 5). This process can begin with states setting sector-level decarbonization targets that provide a road map for utility DER forecasts. Next, regulators can align utility incentives to meet these targets at the lowest system cost. Utilities can then take a DER-first approach to grid investment while compensating customers at a rate that reflects their DER value to the grid. Customer engagement might begin with automatic DER enrollment in a utility or aggregator program upon purchase, such as TOU rates, automated management, or demand response. Customers could also participate in virtual power plants (VPP) that aggregate DER to reduce demand or provide energy and other services to the grid. A virtuous circle can form as customers are incentivized to purchase revenue-generating DER that can also help meet state targets, and low- or middle-income customers receive accommodations accordingly.

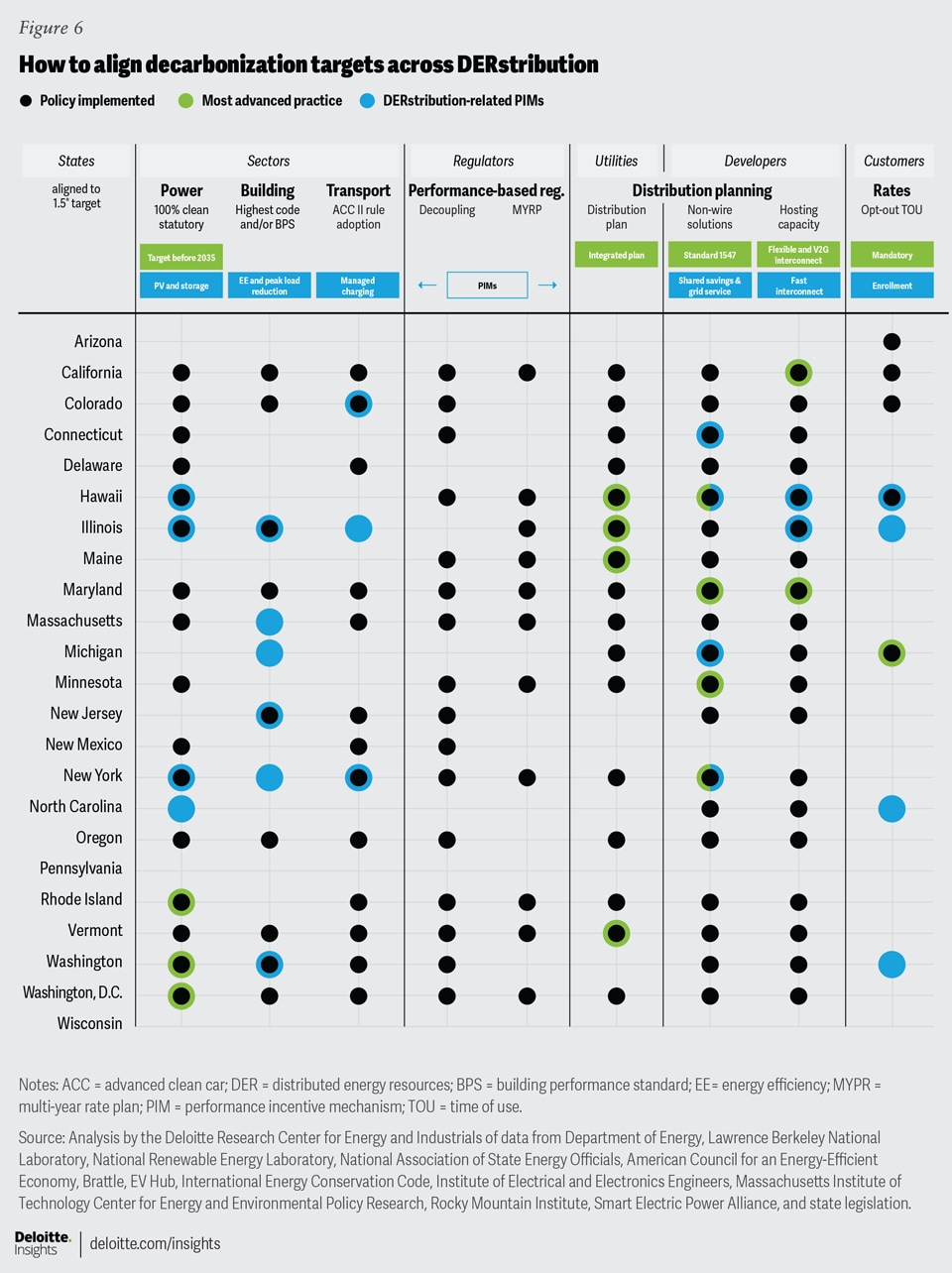

1. States could start with targets. Twenty-two jurisdictions currently require electric utilities to file distribution plans, including ones that focus on transmission and distribution improvement, DER, or grid modernization (figure 6).19 All of the states that require utilities to file either a distribution system or integrated grid plan are also members of the United States Climate Alliance, a bipartisan coalition of governors aligned with the US commitment under the Paris Agreement to limit global warming to 1.5 degrees Celsius compared to preindustrial levels.20 Some states have related energy and electrification plans that utilities can use to inform their DER forecasting. States also administer federal grants that require state engagement in planning to access funds for distribution projects.21 Finally, many states have targets reflecting federal ones across the power, transportation, and building sectors: Sixteen have binding full decarbonization requirements for utilities,22 14 have adopted California’s Advanced Clean Cars II regulation mandating 100% zero-emission vehicle sales by 2035,23 and nine have adopted the most stringent code for new residential buildings and/or building performance standard for existing buildings.24 The targets these states have set are expected to require the greatest level of DERstribution transformation to meet them.

2. Regulators could use performance-based regulation to align utilities with state targets. Most states have implemented some elements of performance-based regulation to help address legacy biases that slow DERstribution progress, and a few, led by Hawaii, are even moving toward comprehensive performance-based regulation (figure 6). This approach introduces flexibility to level the playing field for DERstribution investments that may otherwise remain unvalued or in conflict with the traditional cost-of-service regulatory model. It does so by addressing the following three biases:

- Sales bias: Businesses typically earn revenue by selling their product. Electrification can bring in more revenue from sales, but DERstribution investments also provide needed flexibility to the grid by decreasing demand. A foundational performance-based regulation component is the full decoupling of utility revenue from electricity sales, as is the case in 18 states.25 Decoupling recasts investments in energy efficiency and demand reduction as a grid resource.

- Business-as-usual bias: In a stable, flat-demand context, utilities might go for extended periods of time between rate cases. But because business is no longer usual, they may need to take a more agile approach. Nine states have adopted multiyear rate plans that dynamically adjust prices and revenues based on external indices, including inflation, in between regularly scheduled rate reviews that take place every few years.26 Multiyear rate plans allow utility investments to more closely track with the pace of electrification and technological innovation at the DERstribution level.

- Capital expenditure bias: Utilities earn a rate of return on capital expenditures, but operating expenses are automatic pass-throughs. Some states allow for certain types of intangible assets, such as volt/VAR optimization, to be capitalized.27 But accounting principles and guidance provide limited leeway to do so, and “regulators are loath to stray from these to carve out their own rules,” in the words of a former chairperson of a public utility commission.28 Lack of ownership of DER assets often further complicates their capitalization. Alternatively, performance incentive mechanisms (PIMs) provide rewards and penalties for utilities to support state targets and related customer flexibility and developer needs. So far, 11 states have adopted emergent PIMs pertaining to DERstribution that level the playing field for DER non-wire solutions vis-à-vis poles and wires investments. These provide fixed sums, percentage adders, return on equity basis points, bonuses, penalties, or shared savings between utilities and customers for leveraging DER grid services; more rapidly interconnecting DER; enrolling more customers in time-varying rates; and achieving peak demand reductions from energy efficiency, demand flexibility, and managed EV charging.29

3. Utilities can analyze and share grid data to direct DER development. Advanced planning can speed consideration of DER as inputs and solutions to grid constraints. Although many utilities do not perform detailed hosting capacity analyses (HCAs) of their distribution grids, all the utility standard or integrated distribution plans require HCAs and consideration of non-wire solutions (figure 6). HCAs identify locations and times when the grid is congested, down to the feeder level. They can help inform grid upgrade planning and inverter functionality needed to interconnect additional DER to the grid. And the latest Institute of Electrical and Electronics Engineers standard 1547-2018 requires that DER inverters provide advanced grid support functions that were either absent in the previous standard, such as startup ramp rates and inverter communications, or prohibited, such as voltage support, but are now key to enabling more DER deployment.30 Four of the 1.5 degrees Celsius–-aligned states have completed orders to implement the current standard, and a dozen are planning to do so.31

HCA maps are publicly shared,32 which allows developers to deploy DER and propose non-wire solutions in areas of greatest value to the grid. The California Public Utilities Commission, for example, recently released a pioneering set of flexible interconnection rules that show how HCA data can enable more and faster DER interconnections. Traditional rules assume constant maximal output from generating DER when assessing the grid’s ability to integrate it. Under flexible rules, the commission allows developers to choose an HCA-derived scheduling option to time grid injections for when they would be most beneficial to the grid, and to lower them when the grid is congested. Inverters, storage, and power control technologies that are currently undergoing certification would unlock these capabilities.33 Similarly, the state of Maryland recently passed legislation requiring utilities to expedite V2G interconnections and facilitate payments to DER owners and aggregators for providing grid services.34 These DERstribution forecasts, investments, and expansions can impact the bulk power system, and vice versa. The most advanced distribution planning therefore holistically integrates with bulk power system planning, as is the case in four of the states (figure 6).

4. Customer engagement through opt-out TOU rates can align households with state targets and grid needs. The technological foundation is largely in place to align households to climate targets through opt-out time-varying rates. Advanced metering infrastructure (AMI) deployment already enables such rates for three-quarters of residential connections.35 In all 1.5 degrees Celsius–aligned states, utilities offer TOU rates that vary between two or three periods on a set schedule reflecting typical daily system costs (figure 6). This means that rates are higher at times of the day when demand peaks, and lower when demand falls and when renewable generation is plentiful. All customers could save, especially if they stack TOU rates with utility incentives to participate in demand response programs. Enabling home technologies such as smart thermostats can further boost peak demand reductions per participant to 30% at the highest peak to off-peak price ratios.36

Despite its potential, time-varying rates remain a largely untapped opportunity: Only 8.7% of customers are currently enrolled in TOU rates.37 Enrollment is a level of magnitude higher when customers must opt-out rather than into the rates,38 as is the case in five of the states (figure 6).

Some states go beyond TOU to offer dynamic rates that more closely reflect wholesale prices and grid congestion via peak-time, critical peak, and real-time pricing that varies daily or hourly. Given customer preferences for bill stability and the importance of market-based rates to lowering system costs, a combination of TOU and peak pricing could optimize residential flexibility to respond to both routine and emergency grid needs.39

5. Equity imperatives matter at all levels of planning. More than half of distribution plans have explicit equity goals, as do many PIMs, reflecting the importance of planning to address DER inequities from the outset. Market-driven adoption has resulted in a concentration of DER in higher-income households, except for heat pumps.40 And expensive utility programs benefiting these households, namely net metering, undermined the equity argument for DER.41 Yet low- and moderate-income (LMI)42 households would likely most benefit from these technologies. Housing and transportation are, respectively, the first and second largest household expenditures.43 A third of households are housing cost burdened, a fifth are transportation burdened, and over a quarter are energy-insecure.44 Utility participation in energy efficiency and smart home technology deployment is key to achieving more equitable outcomes. And proposals to direct utility funding to low-income multifamily buildings could be especially effective with regulators.45

- First, utilities can directly deploy DER. While some jurisdictions bar utility investment in potentially competitive DERstribution segments, restrictions may be waived for projects benefiting underserved LMI households.

- Second, utilities can provide tariffed on-bill financing for DER and energy efficiency projects. By providing interest-free capital, utilities remove the upfront cost and credit barriers for LMI households to efficiently electrify. And customers can immediately recoup savings that outweigh the tariff added to their monthly bill.46

- Third, advanced application piloting in LMI areas could engage these communities in understanding how reliability, air quality, and other factors that utilities can control or influence, affect them daily.

DER deployments using these approaches could start with energy-insecure homes in areas of locational value to the grid. Utilities can further leverage new federal and state incentives to minimize cost while maximizing the reward to first-mover LMI customers. The energy efficiency retrofits needed to achieve a zero-carbon-aligned building sector by 2050 could yield utility savings ranging from US $181 to US$1,539 per dwelling per year across states.47 Deloitte analysis found that if this target was achieved by focusing on LMI customers first, all energy-insecure households in every state would be energy-efficient by 2035.48 More broadly, LMI-first DER deployment could address equity by lowering whole system costs while building resilience.

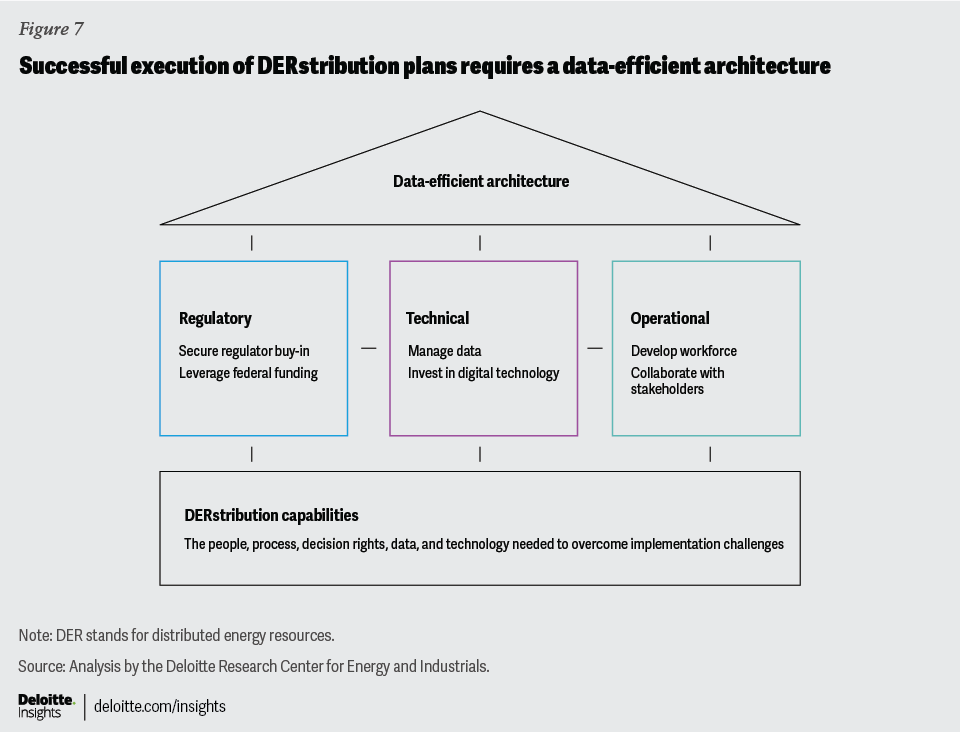

A data-efficient architecture to overcome implementation and resiliency challenges

Successful execution of integrated plans to achieve state targets should include a data-efficient architecture. That is, the technical, operational, and regulatory capabilities should be in place for DERstribution. These encompass the full capability blueprint of people, process, decision rights, data, and technology needed to overcome implementation and resiliency challenges (figure 7).

Regulatory capabilities

Make the case for DERstribution

To achieve regulatory backing for DERstribution, utilities should make a clear case to regulators for DER-related investments. In an interview, Brien Sheahan, former chairperson and chief executive officer of the Illinois Commerce Commission, explained how utilities can do so.

- Reliability is a key to making the case for DER investments. As penetration levels rise, DER visibility and management become necessary to help ensure continued reliability. Integration costs are often underappreciated. Regulators, and politicians, will likely want to clearly see the benefit to customers if the utility is earning on the investment and raising rates.

- In states with climate goals, the carbon impact is one piece of making the case. DER investments can lower carbon emissions by helping to integrate renewables. Illinois’ Future Energy Jobs Act helped support this case by considering the social cost of carbon—a potentially controversial approach.49 In states without climate targets, the case may be more difficult to make. Many regulators could espouse a least-cost approach, complicating any cases that rely on unrecognized societal benefits.

- Another challenge is that the case for investing in foundational technologies has not yielded all the promised benefits. For example, smart meter deployment is costly. Illinois has achieved close to universal coverage, but value is limited to a few use cases, namely automatic shut-offs.50 So a state that has not yet deployed advanced metering infrastructure may not see a compelling case to invest in it, let alone other technologies that build on this infrastructure.

- Finally, the rate impact remains paramount. When rates get too high, pushback overtakes climate concerns. Ratemaking is often a political and legislative function delegated to commissions. A different way to socialize costs could be to revisit cost allocation across customer classes to minimize the impact of the increased costs on residential customer rates.

Leverage federal funding for DERstribution

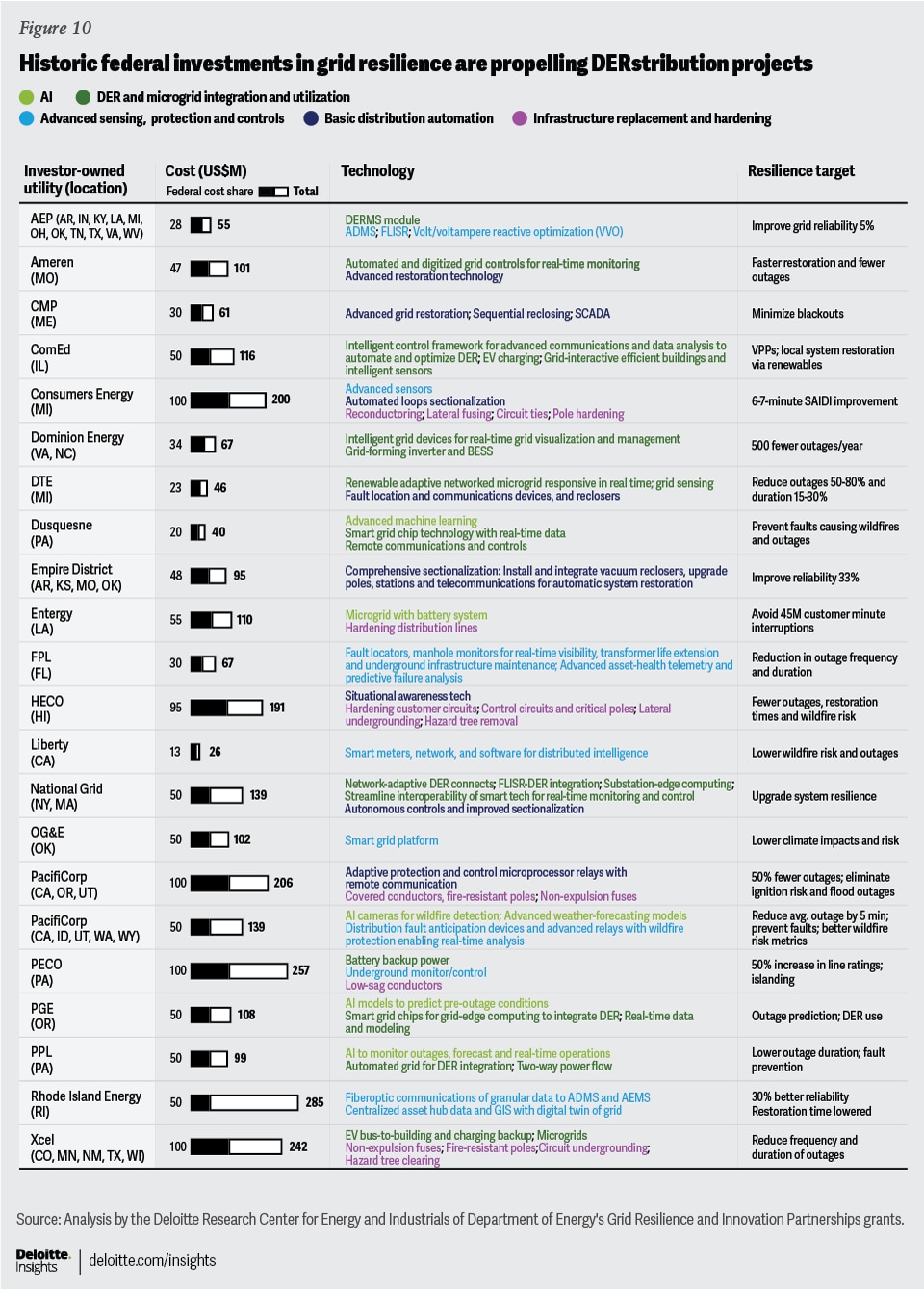

Regulators are also important to helping unlock the financial resources utilities need for implementation. They will likely want to see that utilities are leveraging unprecedented federal funding to build resilient DERstribution capabilities. In October 2023, the United States Department of Energy awarded US$3.5 billion of US$10.5 billion in Grid Resilience and Innovation Partnerships (GRIP) matching grants to utilities, representing the largest single direct investment in the grid.51

The department has also released grid security and resilience funding from separate programs focusing on innovative AI research and cybersecurity solutions. In addition, all but a few states have submitted priority climate action plans to the Environmental Protection Agency, providing access to US$5 billion in direct funding for climate projects.52 The bulk of proposed projects are in the transportation, building, and electricity sectors. Many of the 116 projects in the electricity sector focus on distribution investments.53

Finally, all states are planning to launch Home Energy Rebates programs backed by US$8.8 billion in funding from the Department of Energy: Seventeen applications have been submitted with rebates available in one state.54 These provide point-of-sale customer rebates to LMI customers, with 50% to 100% of costs covered up to US$14,000 for heat pump HVACs, water heaters and dryers, electric stoves, breaker boxes, electric wiring, and weatherization.

Technical capabilities

Manage data for operational decentralization

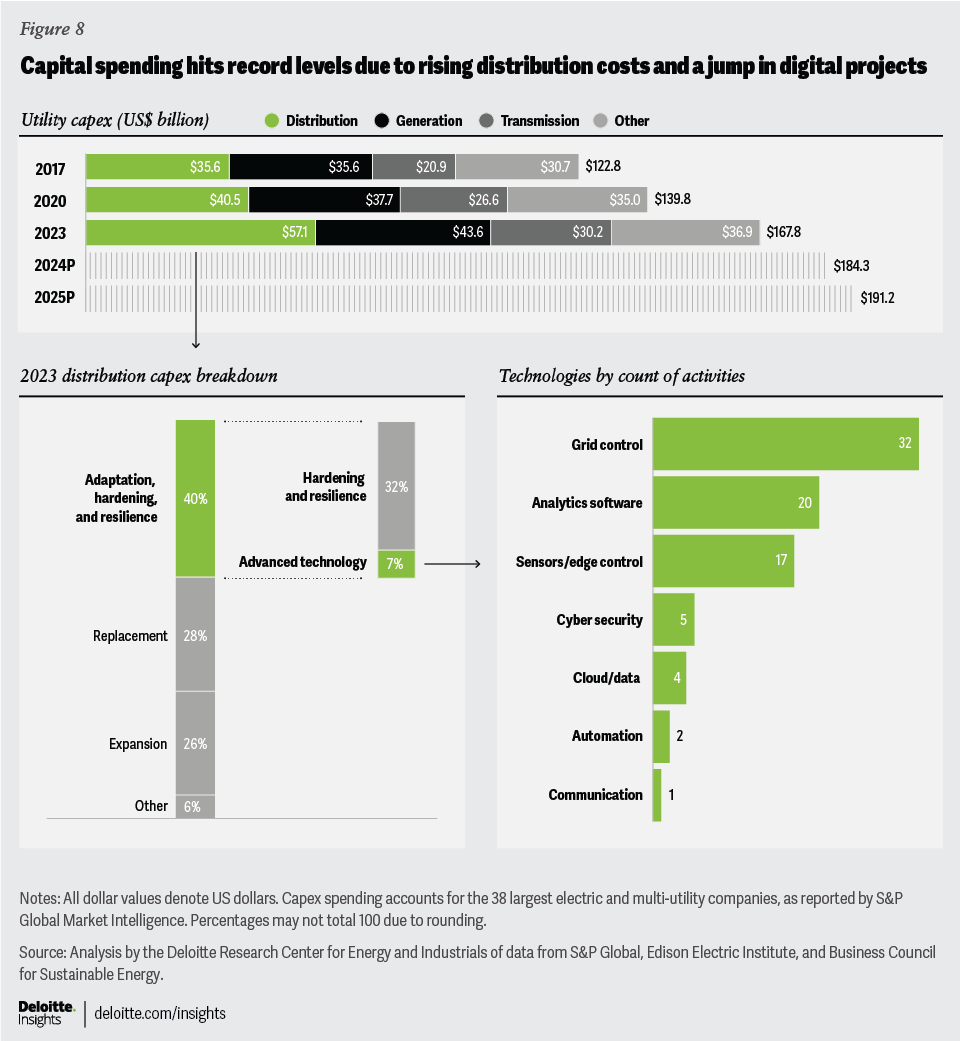

DERstribution resilience builds on a digital foundation and utilities are realizing that real-time control within and at the edge of the grid—also known as operational decentralization—can help maximize DER value and decarbonize. Chief among the distribution grid needs that drove record utility capital expenditures in 2023 are adaptation, hardening, and resilience investments (figure 8),55 which increasingly involve advanced digital technologies. The United States has taken the lead globally as digital projects and partnerships in its power sector have quadrupled since 2021, starting with a boom in control technologies to manage distributed energy resources, followed by analytics software that can help with forecasting.56 The amount of data needed to accommodate DER growth is expected to exponentially increase the amount of data utilities must process and analyze, as well as the cycle time. The complexity of optimizing aggregations of DERs from individual households with different usage, comfort, risk profiles, TOU rates, and options to self-generate or participate in retail or wholesale markets is pushing DERstribution competition into a race for the best AI-powered algorithms. Robust data management is a prerequisite to unlocking AI capabilities. Utilities are looking to either develop these internally, lease third-party platforms, or do both.57

Invest in digital grid technology

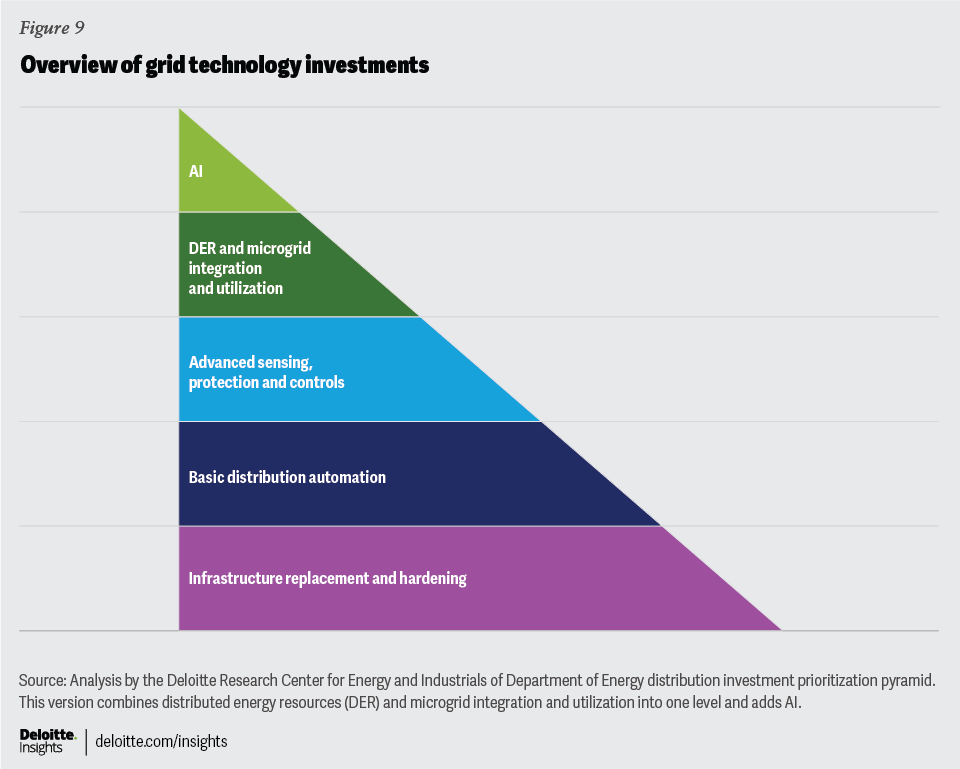

GRIP awards provide a window into the needed technical capabilities. The first round of GRIP provided funding to 24 investor-owned utilities (IOUs).58 All but two of the awarded projects cover distribution.59 The projects range from infrastructure replacement and hardening to AI deployments. Figures 9 and 10 show all IOUs awarded GRIP grid resilience and smart grid grants, with projects categorized according to a distribution investment prioritization pyramid, where each level builds on the preceding one.60

- Infrastructure replacement and hardening grants mostly cover pole and wire hardening and undergrounding projects for the six IOUs awarded GRIP grid resilience grants.61

- Basic distribution automation projects among IOU awardees involve sectionalization, or dividing feeders into sections so that utilities can isolate a fault on one feeder to a small area while restoring power to adjoining areas from a second feeder. More advanced applications the technology enables include creating dynamic DER microgrids to minimize the impact of outages.62 Other basic distribution automation projects include fault locators and reclosers to detect and interrupt faults, and supervisory control and data acquisition (SCADA) systems to remotely monitor and control the grid.63

- Advanced sensing protection and controls build on the foundational advanced metering infrastructure and advanced distribution management systems (ADMS), which enable maximization of use cases from complementary technologies such as fault location, isolation, and service restoration.64

- DER and microgrid integration and utilization can develop as ADMS modules or interconnected systems. Bidirectional charging, grid-forming inverters, and smart grid chips communicating real-time data further enable integration.

- Finally, utilities are starting to deploy AI for resilience. Use cases include pre-outage and outage prediction and monitoring and enhanced real-time grid operations.65

Project resiliency targets often revolve around shorter outage duration and faster restoration.

Operational capabilities

Prepare the DERstribution workforce

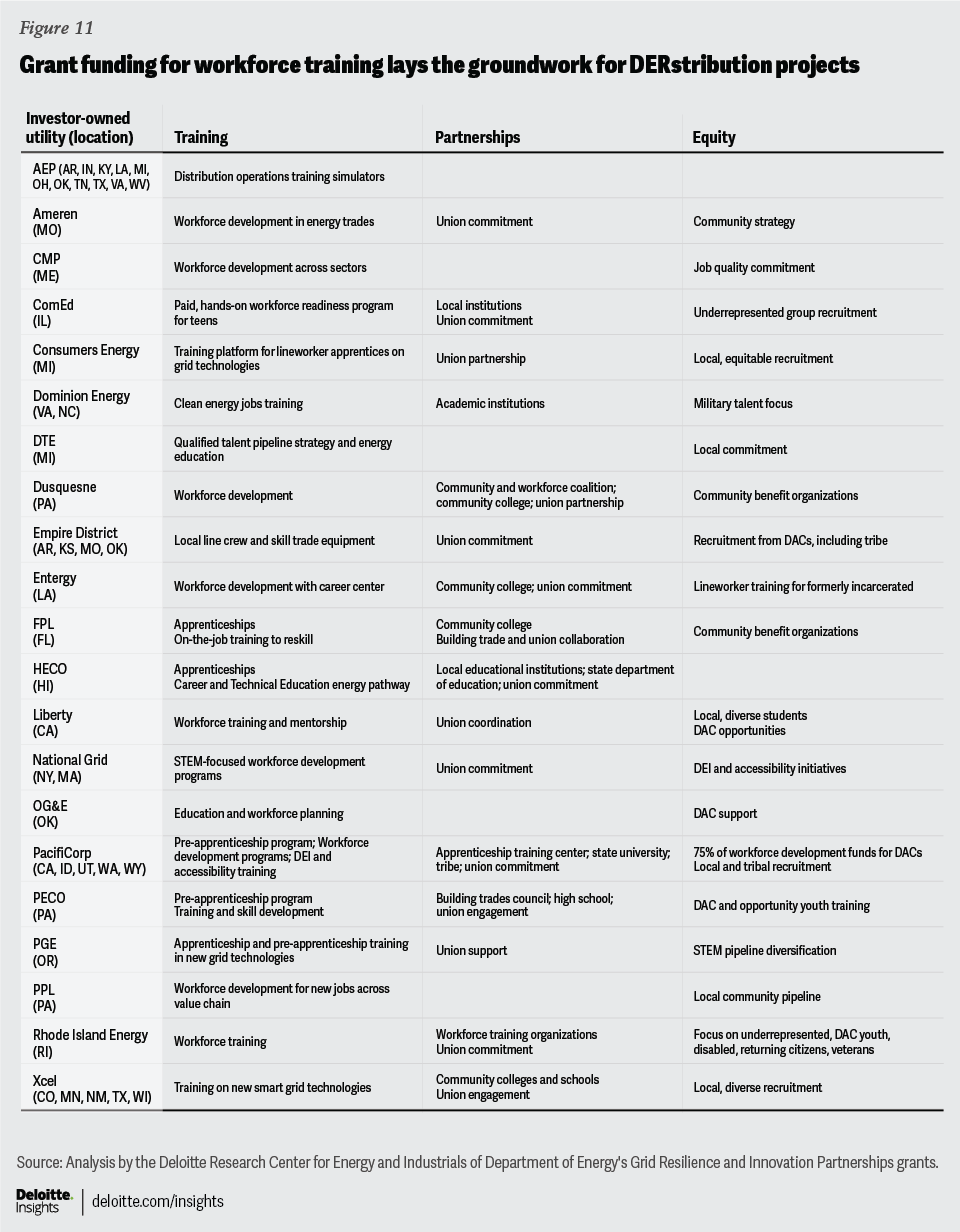

GRIP grant requirements include equitable deployment and workforce training for the new workers and new skills that are expected to be needed to operate a more digital and distributed grid. Indeed, only 3% of utility workers are currently employed in smart grid operations, but investments stemming from GRIP funding alone could create 178,000 more of these jobs.66 Many utilities plan to collaborate with unions, in addition to community colleges and apprenticeship programs, and career centers (figure 11).

DERstribution registered apprenticeships in LMI communities could create talent pipelines to highly skilled jobs locally with credentials recognized nationally. These paid apprenticeships would provide additional support to help LMI communities overcome job barriers, with a combination of training and mentorship.67

Collaborate more closely with more stakeholders

Integrated grid planning is expected to require improving communication and collaboration between:

- Resource planning groups within the utility such as bulk power and distribution planning teams to help increase coordination at the transmission/distribution interface.

- Utilities, states, and federal agencies to incorporate in distribution planning their respective incentives, grants, and tax credits for distribution investment, rooftop solar and storage, EV chargers, heat pump HVACs and water heaters, electric panels, and weatherization.

- Utilities and independent system operators or regional transmission organizations staff to coordinate DER management when bulk and distribution system needs conflict.

- Utilities and customers to facilitate DER interconnection and program enrollment.

- Utilities and underrepresented communities who should be included throughout the planning process to promote procedural, distributional, and structural equity.

- Utilities, unions, regulators, states, federal agencies, and industry organizations such as the Center for Energy Workforce Development to help align on workforce development objectives, timelines, and implementation through registered apprenticeships and other training programs.

- Utilities and regulators with limited resources to transition to performance-based regulation amid record-high rate case activity in 2023.68

- Utilities, DER manufacturers, software vendors, automakers, homebuilders, aggregators, and industry standard setting groups like Institute of Electrical and Electronics Engineers, on communication and control protocols to help ensure interoperability for data exchange.

The data-efficient architecture in action: TOU and VPP case studies

Case study 1: Opt-out TOU rates

Once implemented, opt-out TOU rates foundational to demand management are among the least-cost solutions to peak demand reduction, with no marginal cost to customer participation. Yet technical, operational, and regulatory barriers impede widespread adoption, highlighting the importance of developing the capabilities to overcome them. Some of these include:

- Regulatory: It can take longer for states to pilot and implement TOU rates than it takes to roll out the advanced metering infrastructure foundation: five years from stakeholder engagement to rate implementation, and three years to transition from opt-in to opt-out rates.69 In some states, TOU default rates may be difficult to implement politically.

- Technical: TOU rates require advanced metering infrastructure, but 17 states have penetration levels at or below 50%, limiting the potential uptake in these states to a minority of households.70 Similarly, the smart thermostats that can maximize reductions are only available in over a tenth of households nationwide.71 Utilities in 32 states provide incentives, mostly in the form of rebates, to promote smart thermostats to customers.72 Finally, in the event of successful widespread adoption, TOU rates alone can create secondary peaks. At high DER penetration levels, technology to automate staggered demand, especially from EV charging, could become necessary to help protect the distribution grid.

- Operational: Transitioning to TOU rates is a nine-step path for many utilities, from selecting the rate design, computing the changes across customers multiple times, identifying adversely impacted customers and remedies, conducting focus groups, running a pilot, rolling out and marketing the rates, and tracking and tweaking the rates.73

Case study 2: VPPs

- Regulatory: Utility or third-party aggregations of DERs have traditionally been tapped in response to emergencies. In the aftermath of grid emergencies, over the past year, California implemented an Emergency Load Reduction Program and Demand Side Grid Support Program funded from taxpayer revenue rather than ratepayer revenue.74 Meanwhile Texas launched and then expanded an Aggregate Distributed Energy Resource Program.75 Regulators may regard VPP with some skepticism because customers have opted out during emergency demand response events. Utilities could argue that large aggregations mitigate risk, but regulators will need proof that this is the case, and that no cheaper alternative exists. Pilots could help make the case.76 Yet on average, DER management project costs are 100 times lower than physical infrastructure costs.77

- Technical: VPP consisting of EVs and other DERs could play a broader resilience role. There are still technical concerns related to battery cycling in EVs, and some customers may not be comfortable granting utilities access to their charging car batteries. Even with recent moves by the automotive industry to facilitate V2G, there may be a distance to go yet for residential EV-based VPP to work at scale.

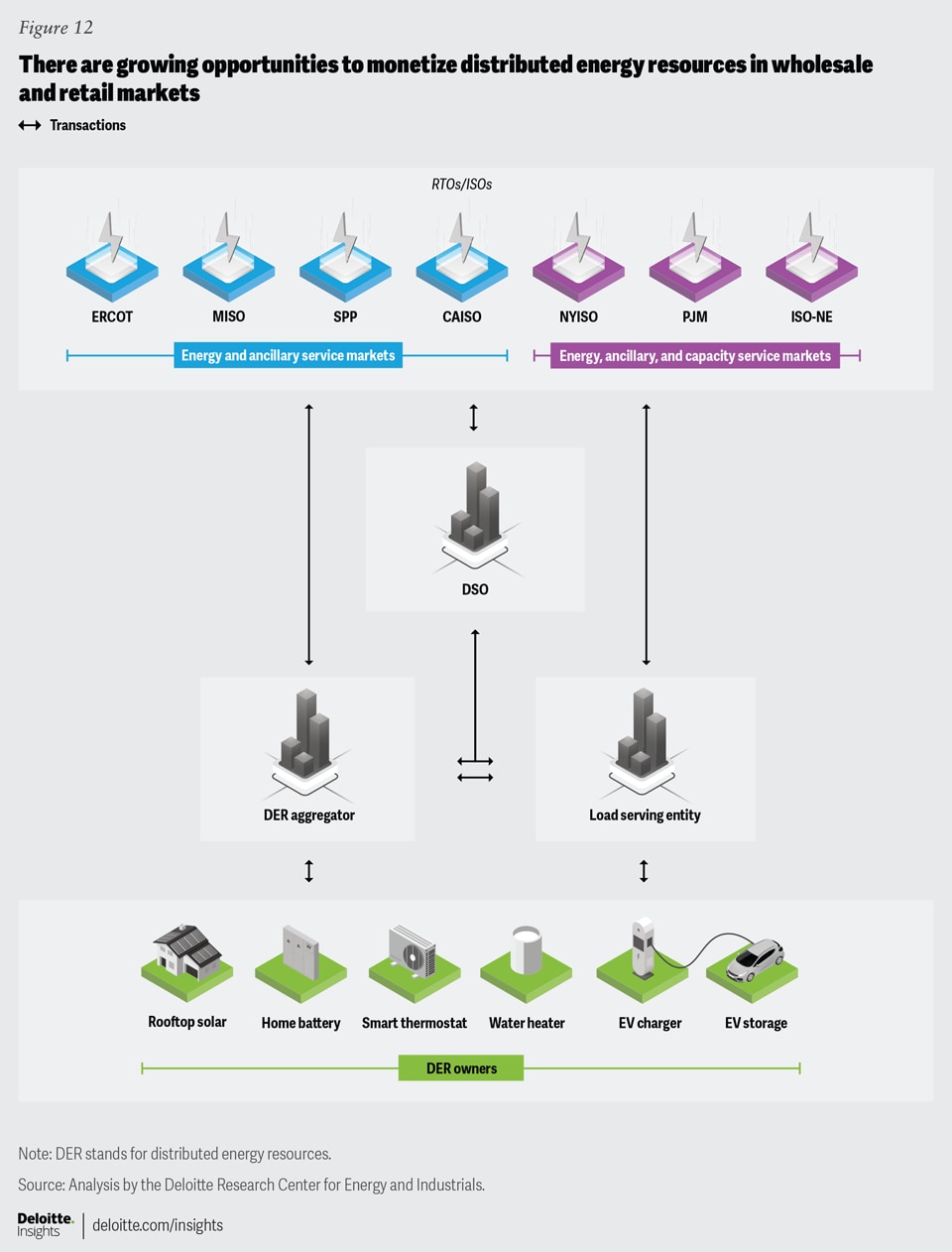

- Operational: VPPs are designed to monetize value streams from providing energy, capacity, and ancillary grid services in the retail and wholesale markets (figure 12). Additional value streams include avoided distribution and transmission upgrade costs, as well as currently unmonetized societal benefits such as resilience, comfort, clean air, and carbon reduction.

Bringing home decarbonization and resilience with DER

Residential resources could be key to meeting the electric utility’s core mission to deliver safe, affordable, and reliable power and more expansive remit to advance societal decarbonization, resilience, affordability, and equity goals. Through improved efficiency, self-generation, demand flexibility, and home and vehicle storage use, households can offer highly distributed and diversified resources that can be orchestrated to meet peak demand while providing grid services.

Moreover, residential electrification can help increase utility revenue, creating headroom for the DER grid integration investment needed without raising rates. Unlike alternative solutions, DER aggregations can lower system costs by leveraging customer capital expenditures and federal funds and relieving pressure on the transmission and distribution grid to deliver power. DER aggregations are also inherently modular and can be fine-tuned to correct deviations from grid planning load forecasts. Finally, DER can also provide revenue, resilience, comfort, and clean air benefits that can redress inequities disproportionately impacting LMI customers.

While the opportunities for DERstribution seem clear, execution can be highly complex. The current planning tools are likely insufficient for a high-DER penetration world. Moreover, the planning processes should be expansive and accelerated to help accommodate an increased number of internal and external stakeholders. Many utilities have yet to put the data-efficient architecture in place to understand, identify, and manage DER on their system, and how to best aggregate and orchestrate them to meet all their goals. To take effective action, utilities can:

- Assess current data foundation: Leveraging DER effectively will likely require decentralization and digitization, which can be done gradually. But utilities can start by assessing the current state of their data efficiency, data quality, and data security. Utilities can work with their customers, third parties, and local communities to manage expectations about the type and speed of change.

- Focus on affordability first: Start with the least costly way to achieve decarbonization with demand response and TOU rates as examples. Using these available tools can free up capacity and allow utilities to spread investment costs over more time.

- Set priorities through scenario planning: Focus on planning and high probability use cases to prioritize the data quality work that is expected to be required. Engage stakeholders to increase communication and collaboration in the planning process.

- Strengthen important relationships: Expand outreach and engagement now so that the grid of the future and its planning includes the breadth of perspectives from the start.

Building the needed technical, operational, and regulatory capabilities will likely require breaking silos within the utility, deploying new technologies, and engaging more deeply with regulators, developers, and households. Aligned utilities could make real progress toward decarbonization goals through DERstribution by 2035.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}