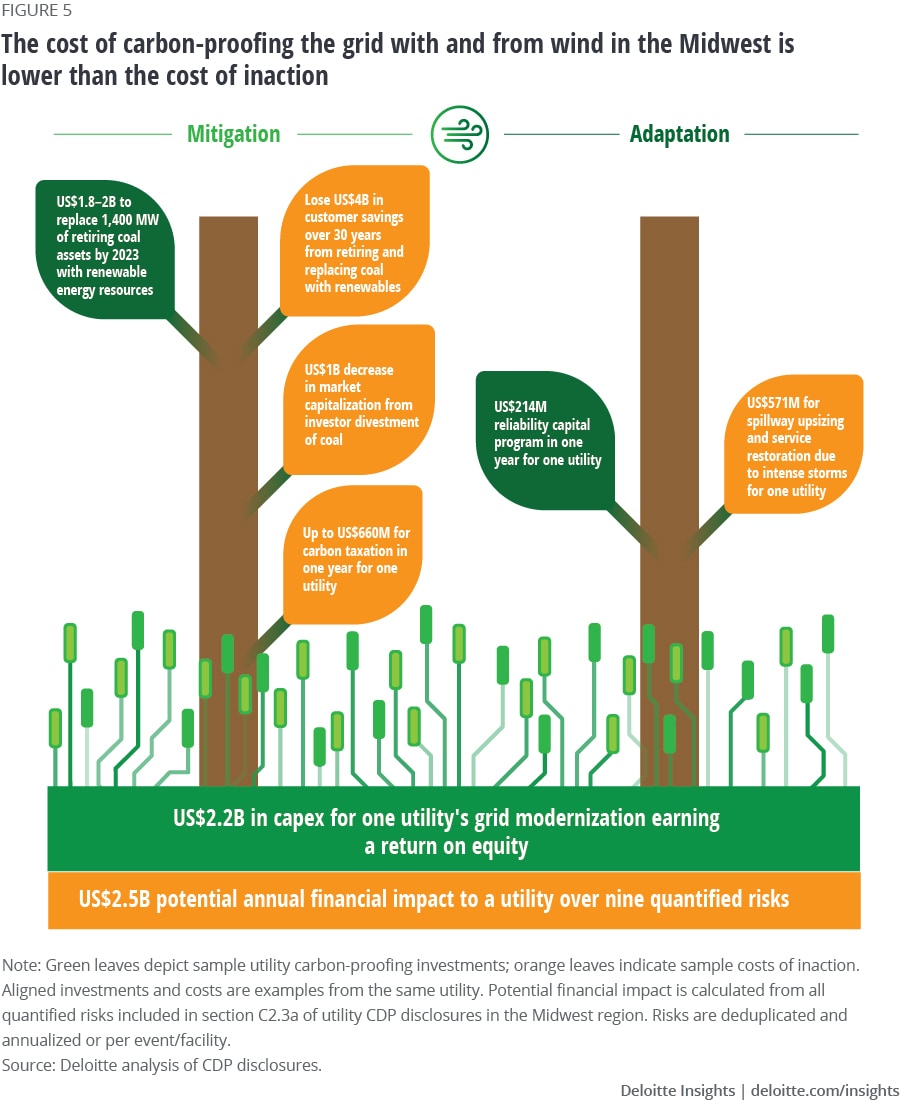

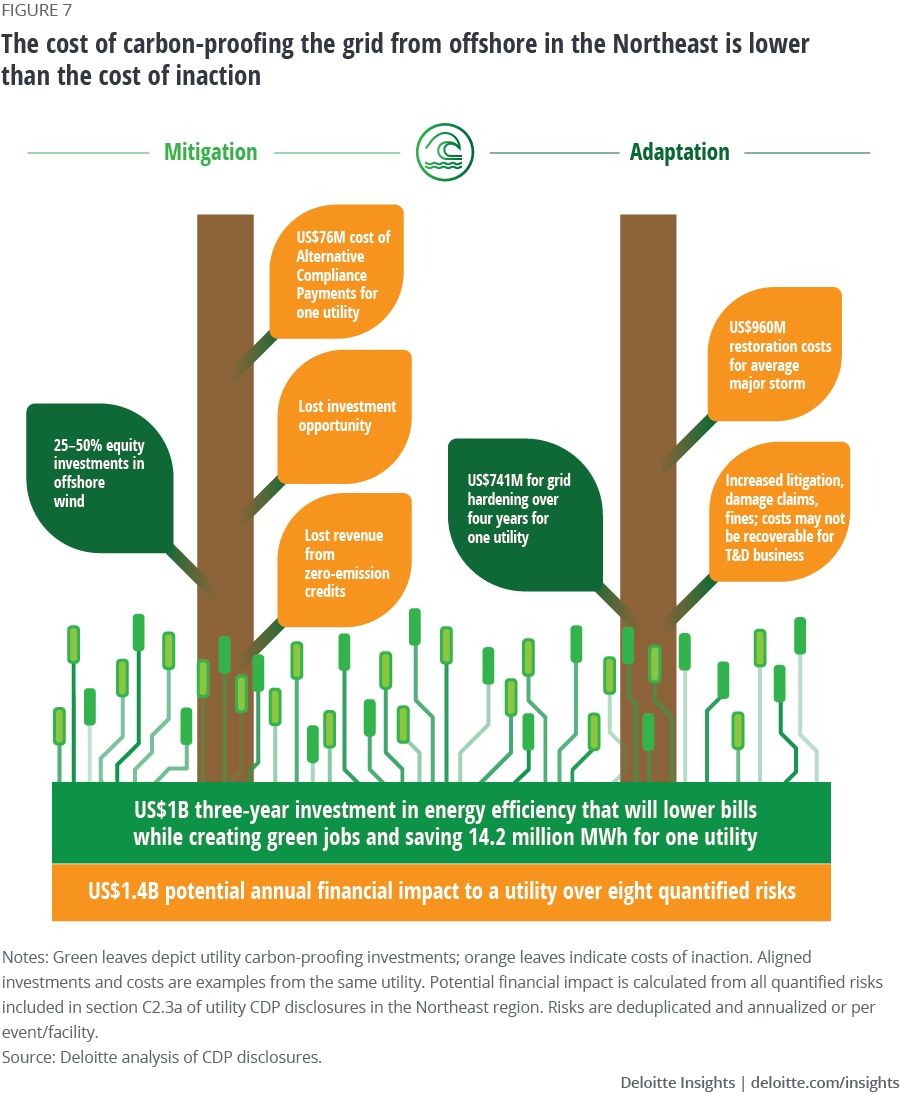

The cost of carbon-proofing the grid can be lower than the cost of doing nothing

Publicly available utility CDP disclosure calculations show that utilities have calculated the cost of action as lower than the cost of doing nothing to address climate change. Indeed, most investor-owned utilities (IOUs) now voluntarily disclose climate-related risks and opportunities to the CDP, along with estimated costs.

Our analysis considers all 29 publicly available IOU disclosures covering 2020, a year when the United States saw a record annual drop in greenhouse gas emissions amid the global pandemic.7 The year 2020 also saw record extreme weather events and damage to utility infrastructure that brought climate concerns to the fore. Climate disasters costing at least US$1 billion each reached a record-high 22 events costing over US$100 billion, wildfires burned a record acreage, and a record number of tropical cyclones made landfall.8

Utilities prepared and submitted these disclosures in 2021, the same year that the Biden administration announced a net-zero target for the United States and signed into law the Infrastructure Investment and Jobs Act funding some of the investments needed to achieve this target, while the Glasgow agreement provided a global consensus call for action on climate change. And in 2021, US$1 billion-plus climate disasters reached another record, topping over US$145 billion in cost.9

To what extent did these 2020 and 2021 events shape utility climate risk assessments?

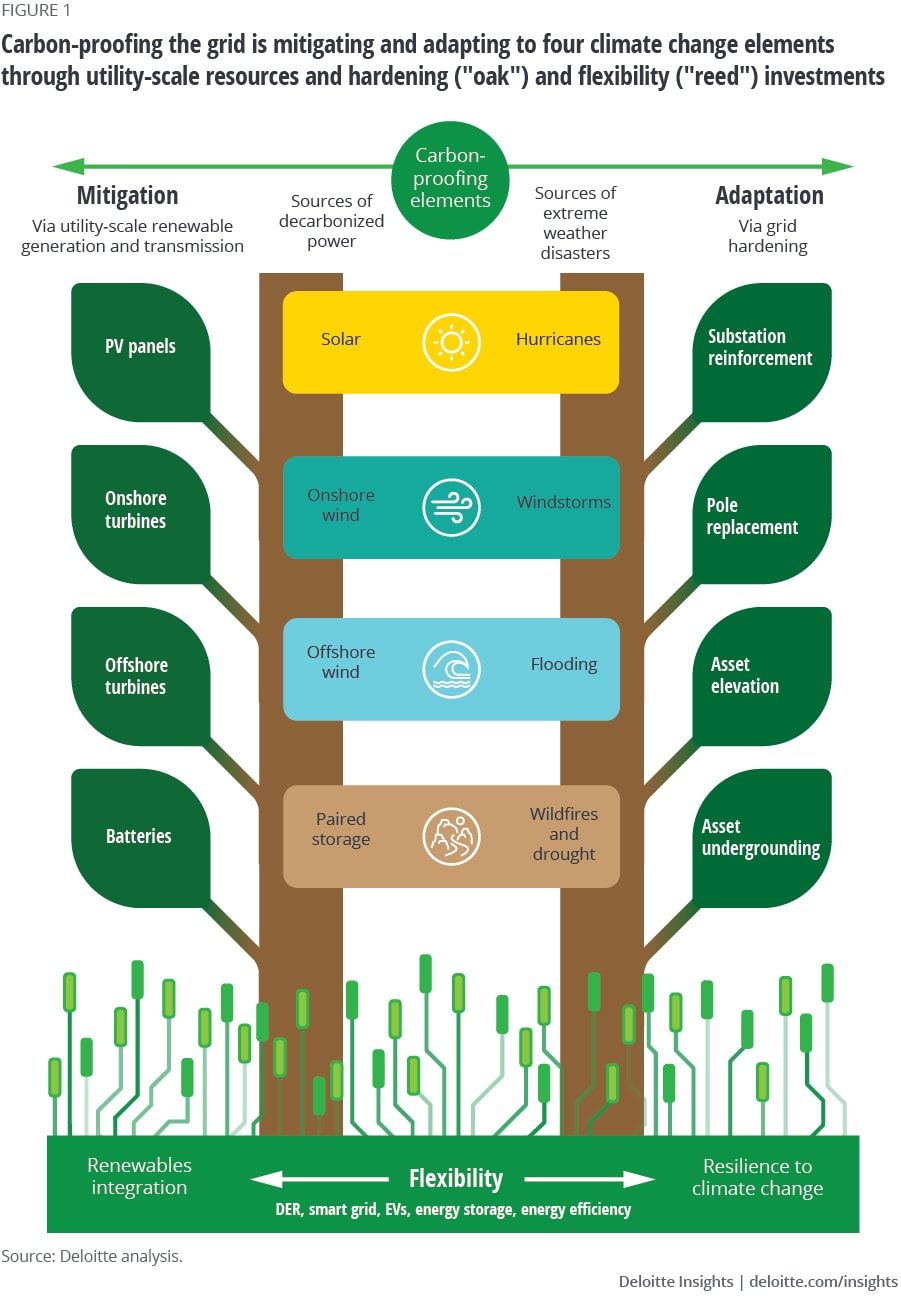

Deloitte developed a framework to help assess how the 29 IOUs that disclosed to the CDP in 2021 qualified and/or quantified climate-related risks and opportunities (figure 1). Organized around the two carbon-proofing goals, the mitigation side shows the leading technologies associated with decarbonization, while the adaptation side shows the major types of grid hardening technologies deployed to guard against the extreme weather events that have been increasing in frequency, severity, and attributability to climate change.10 Flexibility technologies that can both integrate renewables and increase resilience undergird the carbon-proofing.

The framework furthermore draws on La Fontaine’s fable about the oak and the reed to illustrate how a combination of large-scale and smaller distributed resources are needed to create a renewable and resilient grid.11 The oak is massive, but ultimately proves to be brittle during an epic storm, while the comparatively miniscule reed withstands the storm because it can bend. This is also a useful metaphor for the different types of carbon-proofing investments. Carbon-proofing the grid will require both “oak” and “reed” investments. Utility-scale grid development and hardening are the “oaks.” On the mitigation side, a record buildout of utility-scale wind and solar generation, storage, and transmission and distribution (T&D) would be needed to achieve decarbonization targets. On the other side of the carbon-proofing equation, system hardening, such as undergrounding T&D lines, enables utility infrastructure to withstand extreme weather events. But there is only so far the utility-scale investments and hardening can go; hence the need for “reeds” too. We are already running up against the grid’s ability to integrate renewables and recover from extreme weather events when damage occurs. Massive capital investments may also face resistance from regulators reluctant to pass the cost along to customers in the form of higher rates if lower-cost alternatives to grid expansion and hardening are available. Finally, decade-long implementation timelines to permit and build a transmission project could impede rapid decarbonization timelines.

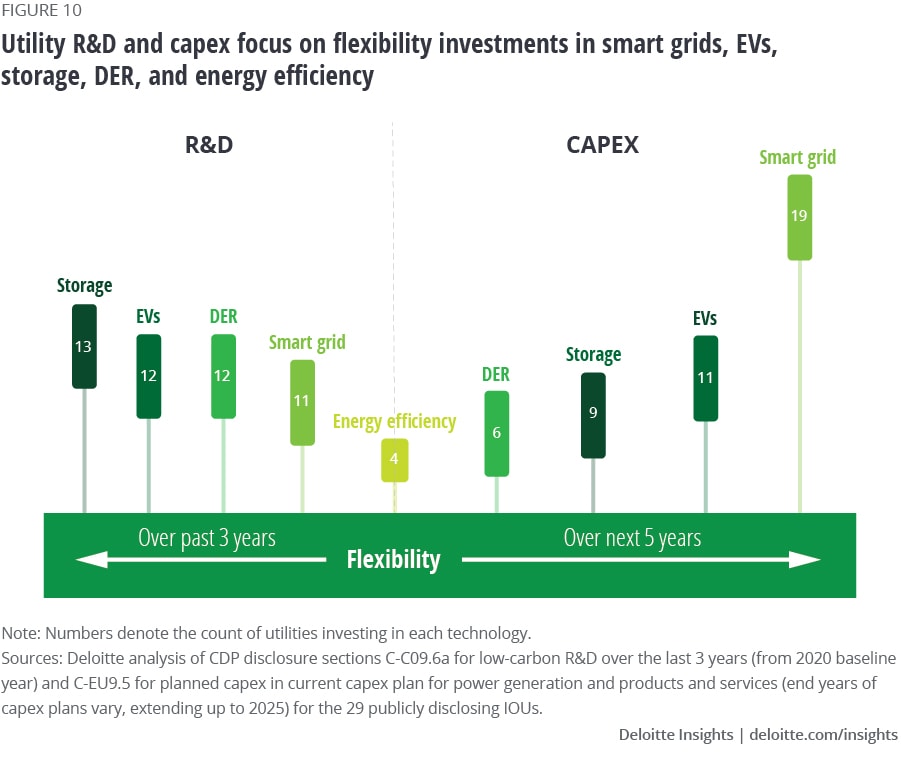

Reeds are distributed energy resources (DERs) that can follow load, and the supporting digital infrastructure, including technologies that can harness the DER in optimizing and balancing the grid via demand response, real-time flexible load programs, managed EV charging, and eventually vehicle-to-grid and transactive energy programs. These flexibility resources can be aggregated into microgrids and “bend but not break” by sectioning off from the grid in the event of an outage and continue powering critical infrastructure. They can be more rapidly deployed to help align demand to renewable supply, offer nonwire alternatives to T&D buildout, and provide ancillary services to the grid, such as frequency regulation, voltage support, and black starts.

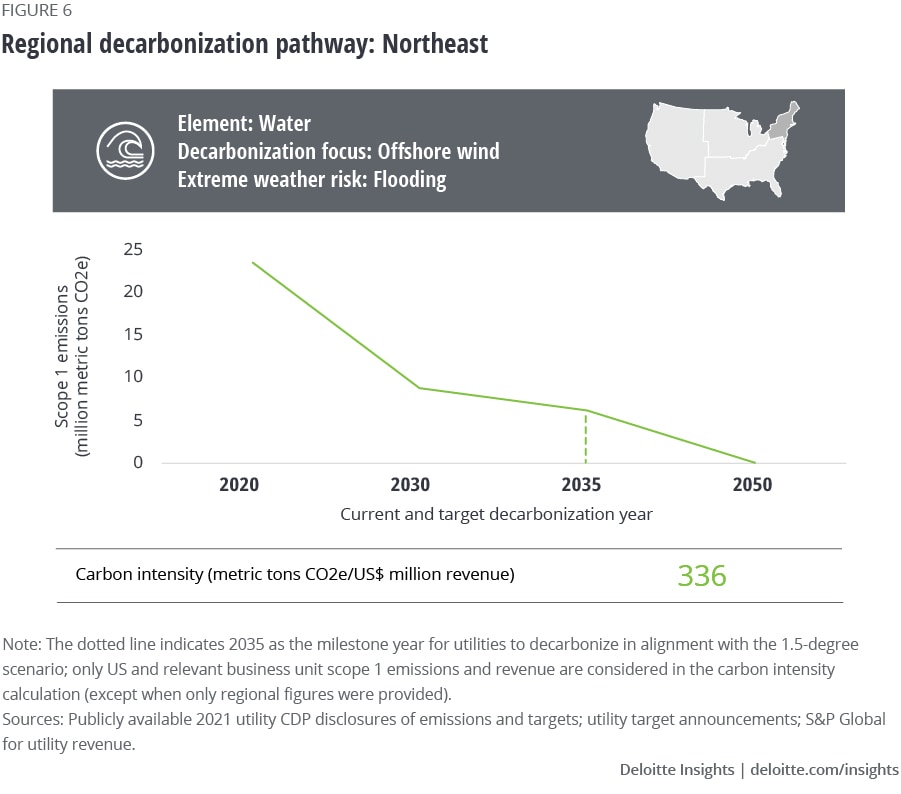

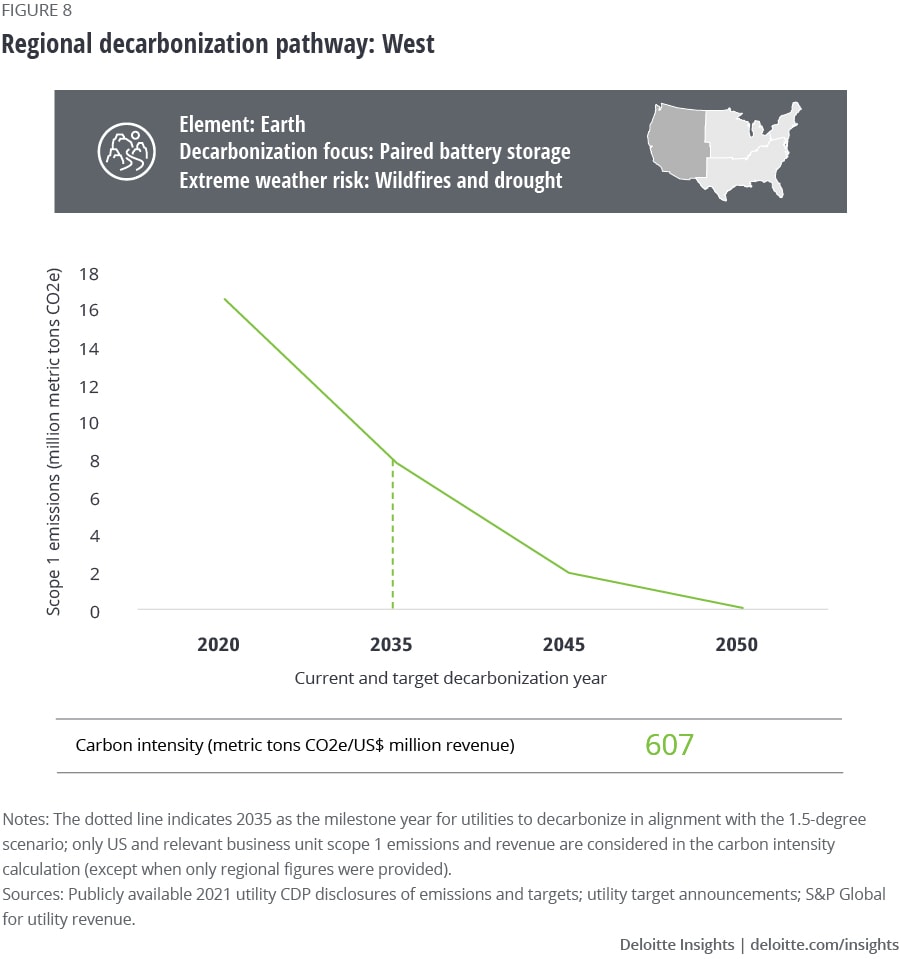

Our framework considers mitigation and adaptation costs across four elements—sun, wind, water, and earth. Sun refers to solar radiation as the source of the fastest growing decarbonization technology (solar power) and a climate risk that occurs when solar radiation peaks (hurricanes). Wind is both a source of power generation and storms. Water refers to offshore power and climate risk sources, namely offshore wind power and flooding. Finally, earth encompasses the battery storage increasingly paired with solar on the mitigation side, and drought and wildfires on the adaptation side.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}