2025 Renewable Energy Industry Outlook

Renewables race to fill resource gap as demand for clean energy is outpacing supply

Marlene Motyka

Thomas L. Keefe

Kate Hardin

Carolyn Amon

Demand growth is a rising tide that lifts all boats, and it especially lifted renewable ones in 2024. Renewables were already buoyed by record public and private investment in, and demand for, clean energy that set the stage for continued growth in 2024.1 Utility-scale solar and wind capacity additions were the largest across all primary generation sources, accounting for close to 90% of all new builds and expansions in the first nine months of 2024, versus 57% of capacity added for the same period in 2023, according to Deloitte analysis of data from the Federal Energy Regulatory Commission.2 Deployment continued to proceed at variable speeds:

- Solar was the only primary source of generation that recorded capacity growth, which jumped 88% to 18.6 gigawatts (GW). As a result, in 2024, solar surpassed hydropower and nuclear as the fourth-largest source of installed capacity, after wind.3

- Wind capacity additions fell by 14% to 2.6 GW amid continued supply chain, financing, and permitting challenges.4 Wind generation reached a new record, however, as it exceeded coal-fired generation for two months in a row for the first time.5

- Battery storage accounted for the second-largest share of total generating capacity additions, rising by 64% to 7.4 GW.6 Excess wind and solar generation is the third-largest use case that utilities report for batteries, following arbitrage and frequency regulation.7

By the end of 2024, the US Energy Information Administration (EIA) expects wind capacity to rise to 153.8 GW, up by 6.5 GW from a year earlier. Meanwhile, it expects solar to rise by a record-breaking 38.4 GW to 128.2 GW, and battery storage to rise by a record-breaking 14.9 GW to 30.9 GW.8 The storage boom is also reflected in the distributed segment, with residential solar attachment rates expected to rise from 14% in 2023 to a record 25% in 2024.9

Looking ahead to 2025, the momentum for clean energy may continue, pending new policy approaches from a new administration. The cleantech manufacturing, artificial intelligence, and carbon industries will likely continue to drive renewables deployment:

- On the demand side, many cleantech manufacturing, data center, and direct air capture (DAC) operators are seeking to meet their infrastructural load growth needs with significant shares of renewables.

- On the supply side, these three industries are helping renewable companies overcome constraints. Reshored cleantech plants are reshaping solar panel and battery storage supply chains. AI is increasingly being leveraged to optimize these supply chains, and to accelerate operational efficiencies and technological innovation in renewables. Meanwhile, the sale of attributes in carbon markets may provide an additional value stream for emerging renewable technology projects.

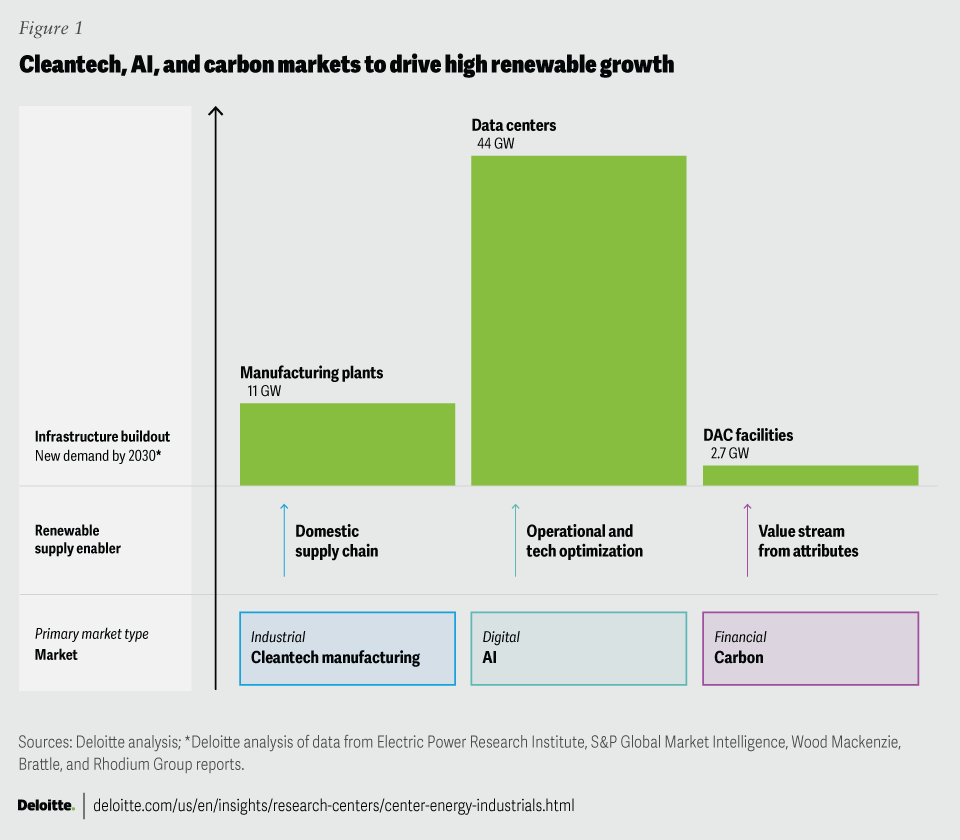

The cleantech manufacturing, AI, and carbon industries are now competing among themselves and other industrial customers to meet their infrastructural power demand at least in part with 24/7 clean energy (figure 1).10 Load growth from cleantech manufacturing plants, which could add 11 GW of demand by 2030,11 is an anticipated long-term trend resulting from supply chain reshoring to meet domestic energy needs. Less anticipated was the pace and extent of data center load growth to power generative AI model training and use. Deloitte estimates data centers will drive approximately 44 GW of additional demand by 2030. The estimate draws on a range of 26 GW to 33 GW in 2024 to 60 GW to 80 GW by 2030.12 Meanwhile, 2.7 GW in demand from DAC plants may emerge by 2030.13 This multipronged demand, totaling more than 57 GW by 2030, is currently outpacing supply. Renewables are in a race with other clean generation options to fill the resource gap. Advantages include technological maturity, low cost, and high modularity. Domestic supply chains, AI acceleration of operational and technological innovation, and carbon attribute monetization could provide additional advantages in 2025.

Deloitte’s Renewable Energy Industry Outlook draws on insights from our 2024 power and utilities survey, along with analysis of industrial policy, tech capital, new technologies, workforce development, and carbon management, to understand how the new competitive landscape may drive renewables growth amid an infrastructural buildout in the cleantech, AI, and carbon markets.

Five key trends to watch in 2025 include:

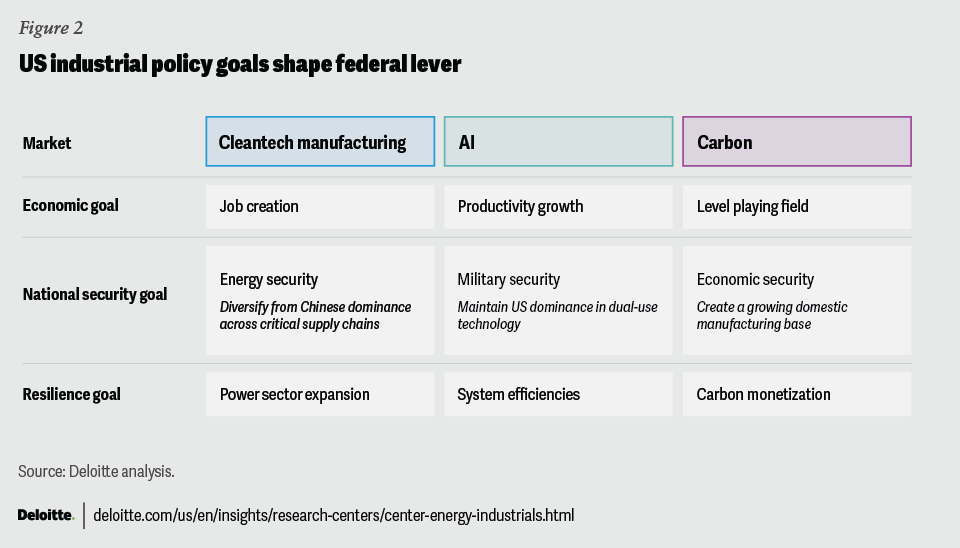

1. Federal lever: Industrial policy goals shape renewables growth

US policymakers share industrial policy goals of strengthening economic competitiveness, national security, and resilience (figure 2). The strategic cleantech manufacturing, AI, and carbon industries may continue to play a critical role in advancing these goals. Their demand for clean energy could limit the appetite for dismantling mechanisms boosting renewables.

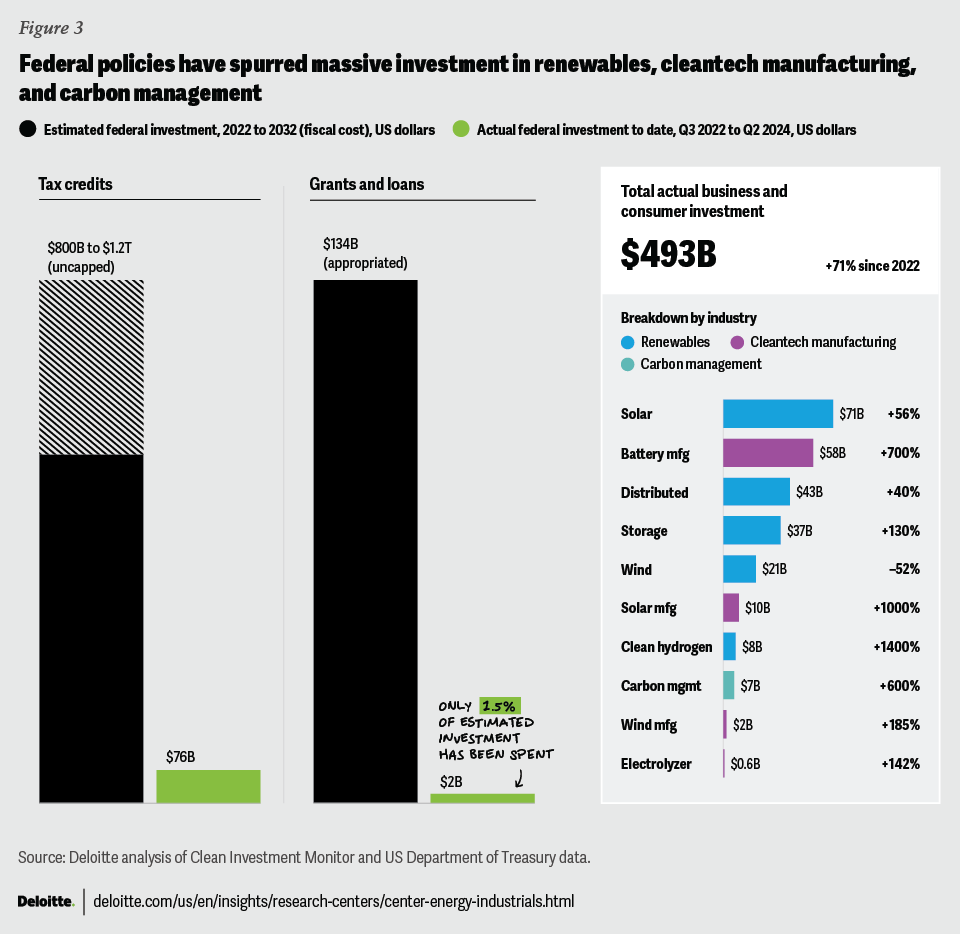

In the wake of implementation of the Inflation Reduction Act (IRA), more than two-thirds of respondents to the 2024 Deloitte power and utilities survey believe the federal government most significantly shapes policies that drive the energy transition (figure 3). As priorities may change under a new administration and the 119th Congress, state and local policy drivers impacting the pace of renewable deployment may become ascendant.

Some disbursed funding from the IRA could support sub-federal initiatives. For example, the US$27 billion Greenhouse Gas Reduction Fund has created new institutions to deploy potentially perennial sources of funding through green banks and community lenders at the state and local levels.14 Obligated funding from the fund’s Solar for All program, the US$8.3 billion Empowering Rural America program, and US$4.3 billion Climate Pollution Reduction Grants alone may spur the deployment of more than 36 GW of renewables and storage by 2030 across all fifty states.15

Meanwhile, historical data suggests market-driven growth fundamentals will continue to shape renewable deployment regardless of policy priority changes. Capital cost-sensitive renewables are poised to benefit from currently falling interest rates and subsiding inflation.16

Cleantech manufacturing: Overall investment in cleantech reached a record US$71 billion in the third quarter of 2024.17 Quarterly records in the retail and manufacturing segments drove the overall record despite tax guidance uncertainty and other factors that contributed to some project delays. Most of the announced projects have not yet broken ground and 60% are slated to begin operations during the next four years. Protection of reshored industry from unfair trade practices will likely translate into continuation of the tariffs imposed in 2024 on solar and batteries.18

AI: AI is a growing policy priority among policymakers that is expected to remain a key issue in 2025. The Biden administration has led efforts to advance US leadership in AI and the new Trump administration has also stated it will prioritize US AI leadership. Given the AI industry’s high energy needs, efforts to expedite permitting for energy projects serving data centers are likely to continue. Public-private collaboration enabling renewably powered data centers may also continue given the net-zero commitments in the tech sector.

Carbon: US industrial policy is also building on multiple Congressional initiatives to measure the carbon intensity of industrial products, including solar panels and wind turbines to leverage the US carbon edge in trade policy.19 Such measurement paved the way for carbon border adjustable tariffs in the European Union.20

Legislative and regulatory areas to watch that could impact renewable deployment for these industries in 2025:

- Legislation

Lawmakers may continue to consider permitting reform proposals—another area of bipartisan interest—to facilitate energy project development. The imperative to accelerate new generation and transmission could also help ease major bottlenecks for the existing pipeline of renewable projects to come online.

President-elect Donald Trump’s stated priorities include lifting a ban on new liquefied natural gas (LNG) exports targeting non-FTA countries as offtakers, and, as part of permitting reform, expediting LNG terminal development.21 Export capacity with existing projects is already slated to grow 86%, with projects starting to come into service by early 2025.22 The upward pressure and exposure to volatility this would place on natural gas prices could enhance the relative competitiveness of renewables vis-à-vis gas in power production.

Meanwhile, EU rules to reduce methane emissions could boost US production of lower carbon gas regardless of US regulatory requirements. US exporters of LNG seeking to serve the European market could potentially create additional demand for renewable natural gas.

- Regulation

Recent Supreme Court rulings could continue to create uncertainty about the future regulatory environment and the impacts on energy-related rules. These rulings include:

- The revocation of doctrine granting deference to agency interpretations of ambiguous statutes23

- An expanded statute of limitations to challenge rules24

- Curtailed administrative authority to enforce penalties25

- A stay of agency rules in an emergency appeal26

While the Court turned down three other emergency docket requests to stay EPA rules on reducing mercury, methane, and carbon emissions,27 these rules remain in litigation and could be impacted by changes with a new administration.

2. Data centers: AI expands renewable scale and capabilities

Scaling renewables at data center pace

Data center owners are leading the corporate shift toward renewable energy. According to Deloitte analysis of data tracked by S&P Global Market Intelligence, solar and wind capacity contracted to US data centers has grown to nearly 34 GW through 2024, representing close to half of all renewables contracted to corporations in the United States, and could reach 41 GW by 2030.28 Tech companies that own or lease data centers with a combined capacity of 9 GW, have committed to sourcing all of their power from clean energy.29

Clean energy commitments are running up against power demand growth, however. AI power demand estimates range widely given that only a couple of the major operators report on either data center electricity use or the power usage effectiveness of individual data centers, and none report both.30 Despite uncertainties over long-term growth due to efficiency gains, strong short-term growth is likely. According to Deloitte mid-range estimates, data center power load could grow from 29 GW to 75 GW by 2030.31 Spending on data center construction has increased 37%, by US$8.2 billion, over the past year ending in October, outpacing the 5% growth, by US$6.3 billion, in spending for power construction.32

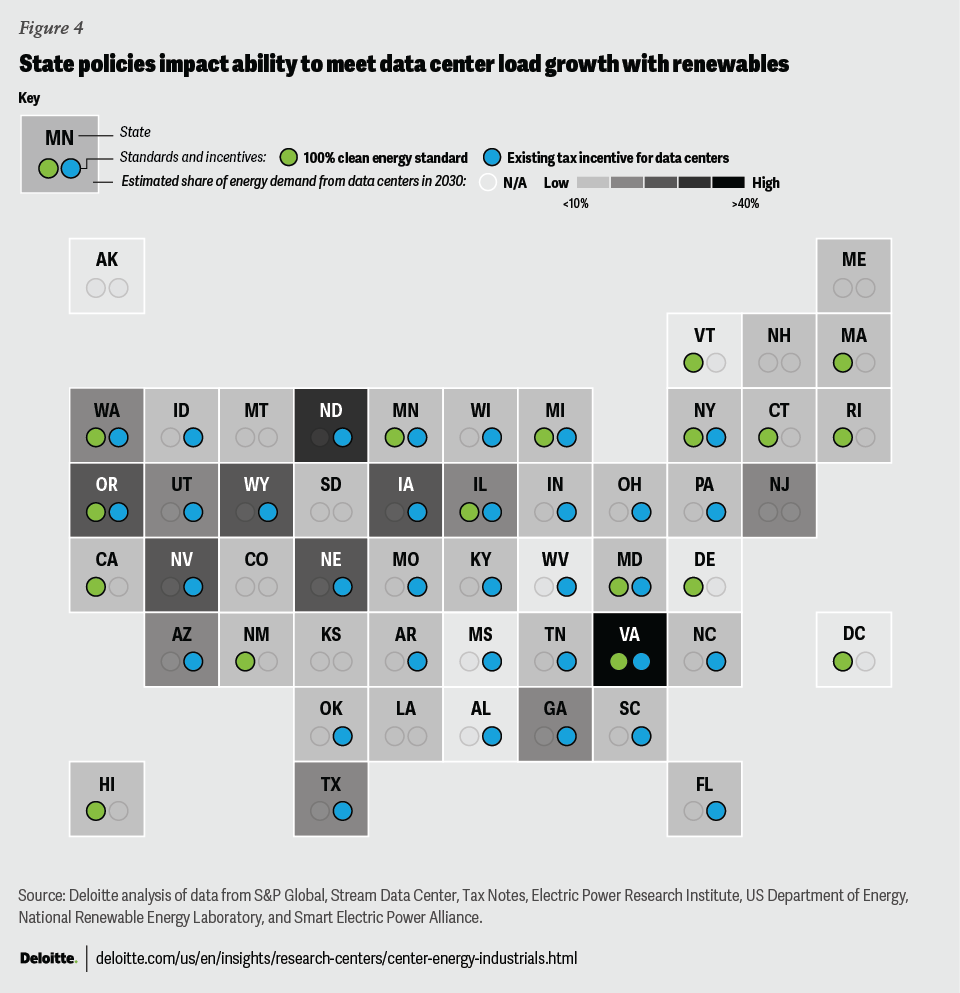

State policies are impacting both renewable and data center growth. State targets help unlock commitments as the local grid mix can constrain clean energy sourcing options. Seventeen US jurisdictions have statutory 100% clean energy requirements covering utilities, with attainment years starting in 203233 (figure 4). Most states also offer data center incentives, which are present in the seven states where data centers’ share of total electricity consumed is expected to be highest in 2030.

Over the next year, renewable configurations could change to meet the demand for clean power. At the utility-scale level, modularity and ease of permitting are expected to drive contracted solar capacity, which outpaced wind in 2024, to grow to twice the contracted wind capacity in 2025.34 Deals may scale, as reflected in the numerous largest-ever renewable power purchase agreements signed with technology companies this year for data centers globally.35 Value in scaling can also be captured at the distributed level, where there is interest in harnessing existing solar and battery storage resources and developing new ones to help meet data center needs.36

Given grid constraints, some companies and utilities are looking to onsite solutions that can help meet demand in a matter of months while awaiting a grid connection.37 In 2024, data center-as-a-service companies and utilities announced off-grid solutions such as fuel cells. Even in cases where natural gas powers them in the short term, fuel cells can bridge to a renewable natural gas or green hydrogen solution.38 New storage solutions geared toward data centers include geopressured geothermal systems and sodium-ion and thermal batteries that can lower operators’ insurance rates by offering nonflammable alternatives to lithium batteries.39

Expanding renewable capabilities with AI

AI is helping deploy and integrate the renewables that the industry is seeking to power its infrastructure buildout. Domestically manufactured smart meters incorporating AI may soon help increase grid stability as customer solar and storage systems are integrated.40 Similarly, an energy provider and tech company are deploying AI to help build a 1 GW virtual power plant of smart home thermostats and distributed energy resources, in addition to renewable generation and price modeling, and weather forecasting.41 AI-powered robots are helping install large solar deployments in the desert powering data centers.42 On the regulatory side, the Pacific Northwest National Laboratory hosts a PolicyAI project that has released a searchable database of federal environmental impact studies and public comment sorting to enable AI solutions expediting environmental and permitting reviews.43 Finally, US Department of Energy (DOE) has funded research using AI to accelerate the development of new circuit technologies for high-voltage direct current converters to help more efficiently integrate remote renewable generation.44

As utilities and tech companies deploy renewables in 2025, the following developments are expected:

- Repurposing brownfield sites: Limited grid capacity and transmission challenges can create opportunities for brownfield sites to be repurposed as clean-energy data center campuses. Projects could leverage existing power lines, water access, and a local workforce. DOE awarded a GRIP grant to build a grid-enhancing renewable microgrid on a brownfield textile site previously powered with coal to power a data center and manufacturing complex.45

- Resource planning renewables: Utility uptake of IRA provisions in resource planning is often uneven, although solar and wind are the lowest-cost resources when incentives are factored in.46 Deloitte’s 2024 power and utilities survey shows 97% of utilities prioritize clean energy to support data center growth, suggesting that tech companies with decarbonization targets could drive utilities to consider more renewable deployment as part of data center siting decisions.

- Shifting focus to real-world impact of renewable strategies: Some tech companies are seeking to reduce emissions by shifting from unbundled to bundled renewable energy credit purchases and other actions to drive new supply of renewables.

3. Technological innovation: 24/7 renewable solutions emerge

Recent federal policies have accelerated innovation in renewable technologies that can provide 24/7 clean power. Meanwhile, novel industry partnerships are forming to accelerate their commercialization. These include an initiative from a group of technology and manufacturing companies to aggregate their clean power demand to help accelerate the commercialization of advanced technologies.47 Utilities are seeking to introduce new clean transition tariffs for commercial and industrial customers that can help finance deployment of these technologies without impacting residential customer rates.48

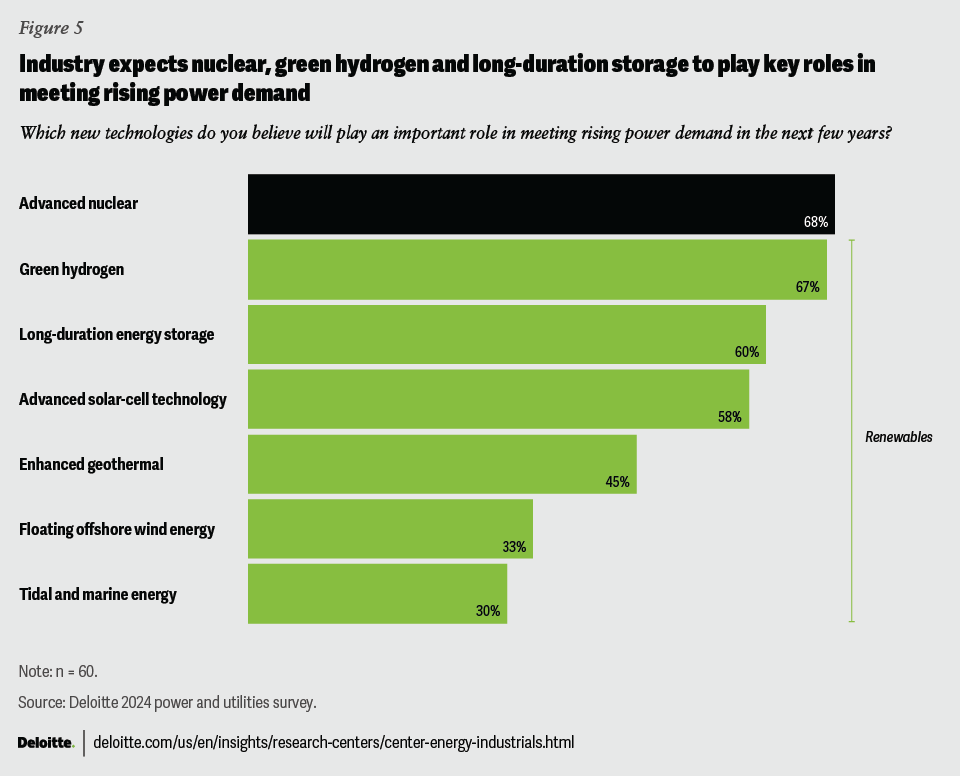

Deloitte power and utilities survey respondents believe that advanced nuclear technologies will play the most important role in meeting rising power demand in the next few years (please see 2025 Power and Utilities Industry Outlook). Among renewable technologies, most believe green hydrogen, long-duration energy storage, and advanced solar cell technology will have the greatest role (figure 5).

Green hydrogen: This 24/7 renewable gas technology powered by renewables continues to hold equal measures of promise and uncertainty. DOE has allocated US$7 billion to develop hydrogen hubs and five of seven projects have received phase 1 funding to start solidifying planning, development, and design activities around site selection and technology deployment.49 However, the US$3/kg green hydrogen tax credits have proven to be the most complex to iron out and the industry is still awaiting final guidance expected by the end of 2024.50 The incoming Trump administration could potentially revisit the proposed standards, with some industry players expecting loosened rules.51 Again, stricter European standards could boost green hydrogen production seeking to serve the largest export market opportunity. Another area to watch that could sidestep this issue altogether is the search for naturally occurring hydrogen by technology and manufacturing company-backed startups.

Long-duration energy storage (LDES): Regardless of the trajectory of these policy and technology outcomes, green hydrogen would retain its primary use case in the power sector as LDES, among other emerging storage solutions that can firm renewables into 24/7 resources. LDES technologies that received federal funding in 2024 include:

- Green hydrogen production from a Superfund site’s wastewater to provide 16 hours of storage for solar power52

- Iron-air battery deployment to store offshore wind power and discharge 85 MW of power for up to 100 hours, which would form the world’s largest battery53

Advanced solar cell technology: Innovation in silicon, perovskite, and tandem solar cells offers potential for higher efficiency rates and lower production costs.54 Advances involve 24/7 capabilities in the form of dual-use applications such as building-integrated photovoltaics, agrivoltaics colocating solar generation with agriculture, and floatovoltaics that can help address both energy and water concerns.

Enhanced geothermal systems (EGS): Rapidly maturing EGS that can provide 24/7 baseload electricity by accessing deep heat reservoirs is benefiting from federal funding and cross-sector investment in technological advances such as new drilling techniques and extreme heat operations, and bipartisan support to fast-track projects.55 Technology companies are partnering with developers to deliver geothermal power, and with utilities to support EGS deployments using a clean transition tariff to shoulder the cost and risk of deploying a new technology.56 Meanwhile, a utility signed the largest geothermal power purchase agreement, totaling 320 MW, to meet a public utility commission requirement to procure 24/7 carbon-free power.57

4. Renewable jobs: Firms address workforce development

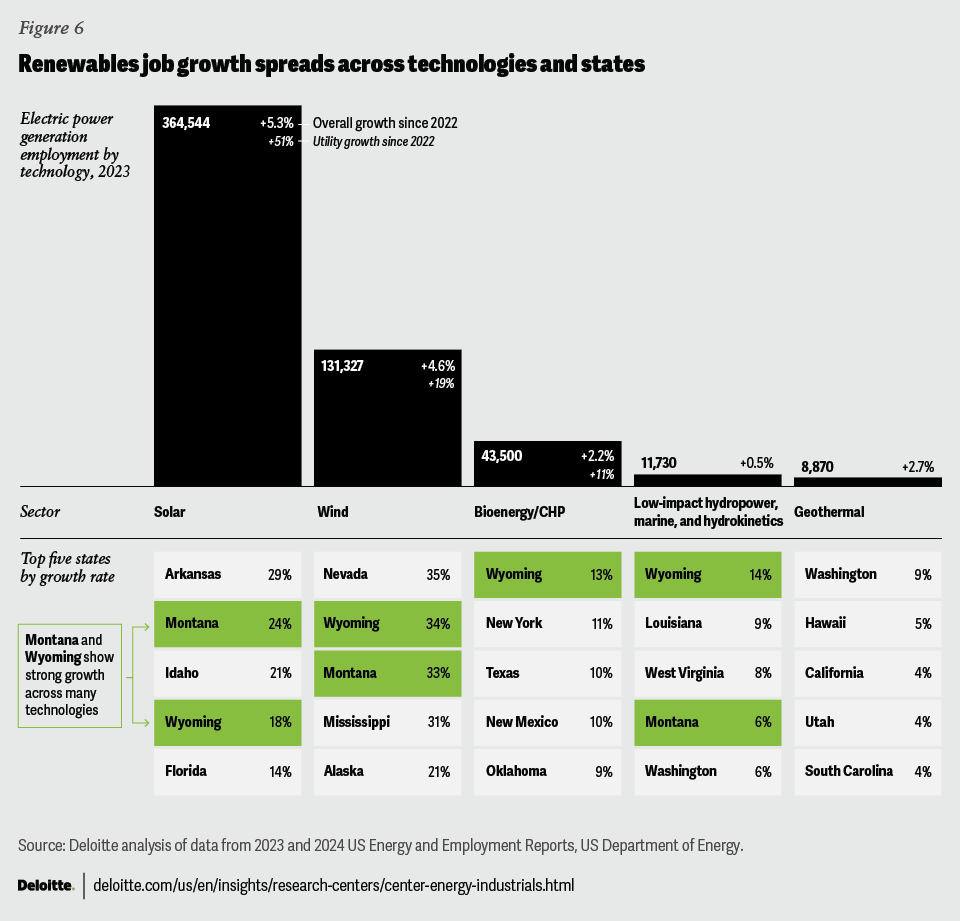

The acceleration of mature and emerging renewable infrastructure buildout is reflected in renewable employment growth. Clean energy jobs accounted for more than half of energy jobs created in 2023, and 79% of new electric power generation jobs; these jobs grew at twice the rate of jobs across the economy, while energy construction jobs grew at twice the rate of all construction jobs.58 Hiring in renewables has grown to twice the level of hiring in fossil fuels.59

Solar energy accounts for two-thirds of renewable jobs and wind accounts for a fifth (figure 6). While California and Texas continue to lead in terms of total renewable jobs and growth rates for emerging technologies, Wyoming and Montana have emerged as the fastest-growing regions, increasing renewable energy employment by 23% and 15%, respectively.60

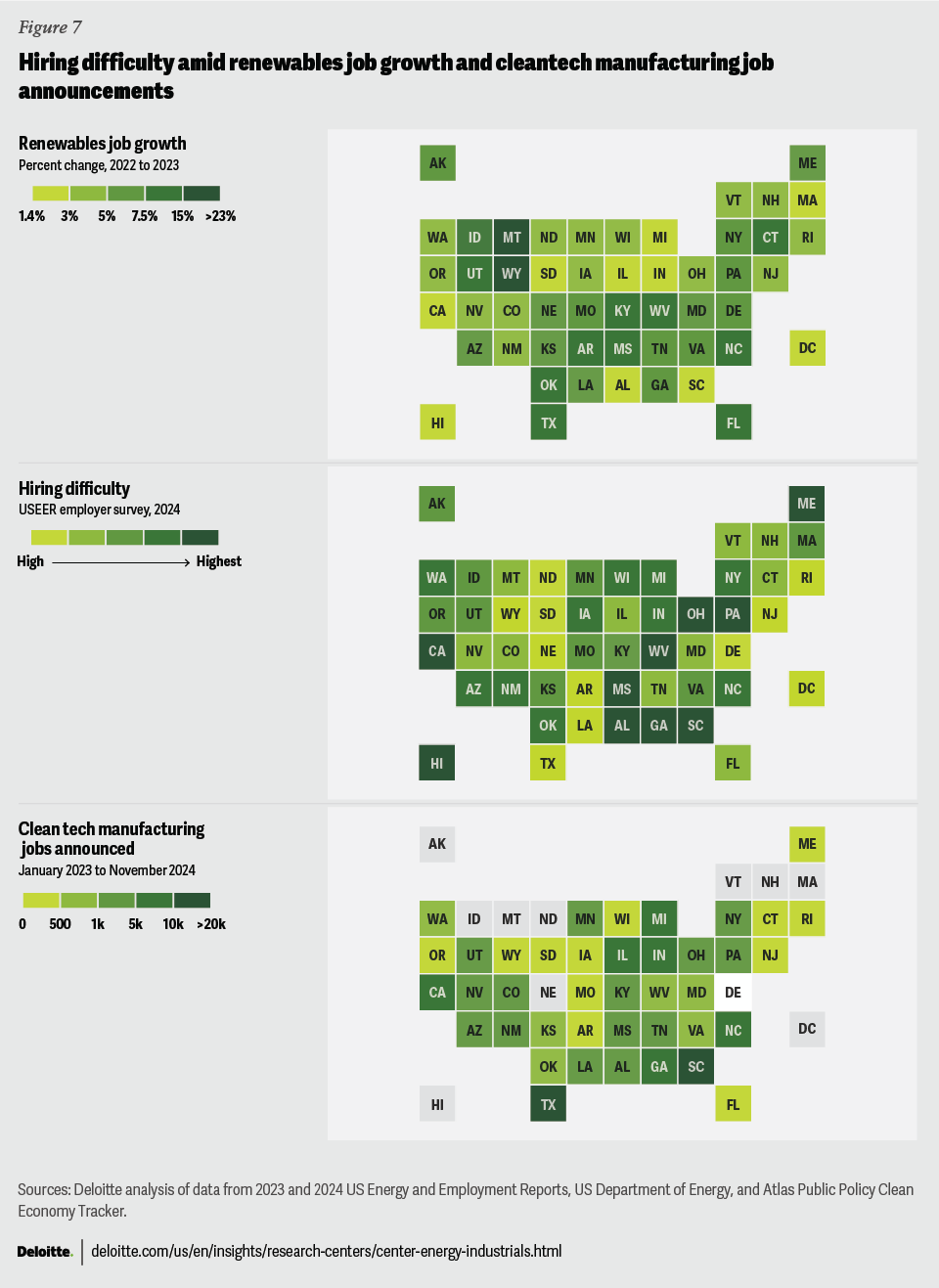

The utility industry, which has the greatest share and demand for green skills—led by renewable energy and electrification—competes with the technology industry, which has the fastest growth in green skill demand. And it competes with all other infrastructure-building industries for construction workers (please see 2025 Engineering and Construction Industry Outlook).61 Utilities and renewable developers face challenges including: securing a larger workforce, developing digital and project development skills, and hiring for completely new roles as they diversify their renewable portfolios (figure 7).62

Many organizations may not be prepared to create workforce development programs, which should proactively implement (please see the Workforce Development Maturity Model):

- Integrated workforce development strategy, structure, and governance to invest in workforce development, establish a structure to assess workforce needs, articulate organizational goals, and the partnerships to achieve progress toward those goals.

- Preparation for the changing nature of skills to identify and clearly define the future-facing skills required for the workforce, measure skills gaps, and engage the workforce to strengthen areas of weakness.

- External workforce cultivation to tap rich sources of recruitment outside an organization, building relationships and targeted messaging to attract interest, and providing inroads for recruitment and upskilling.

- Long-term external workforce development and planning to take a wider, longer-term lens to the external workforce, partnering with others in the industry and across communities to promote a continuous pipeline of candidates for recruitment.

- External skill programming and development to identify emerging career opportunities and skills in the industry, develop proficiency metrics, and engage external partners in recruitment candidate preparation.

- Policy and industry engagement to monitor legislation, engage federal agencies and workforce boards, and actively partner within the industry sector to advance workforce development priorities.

- Organizational culture and brand to align with the organization’s future-facing workforce goals and embed culture from onboarding throughout career journeys.

- Internal training and development to assess and address skill development and provide clear paths of advancement to encourage continuous learning and loyalty.

Organizations that move up the maturity curve can strengthen, diversify, and upskill their talent pipelines. They may also start reaping the results of industry ecosystem partnerships from DOE-funded workforce readiness programs to support education and training tied to apprenticeship programs with organizations that have hiring commitments. Unions, educational institutions, trade schools, and apprenticeships are expected to begin implementing some of these programs in 2025.

5. Carbon management: Renewables power high-integrity offsets

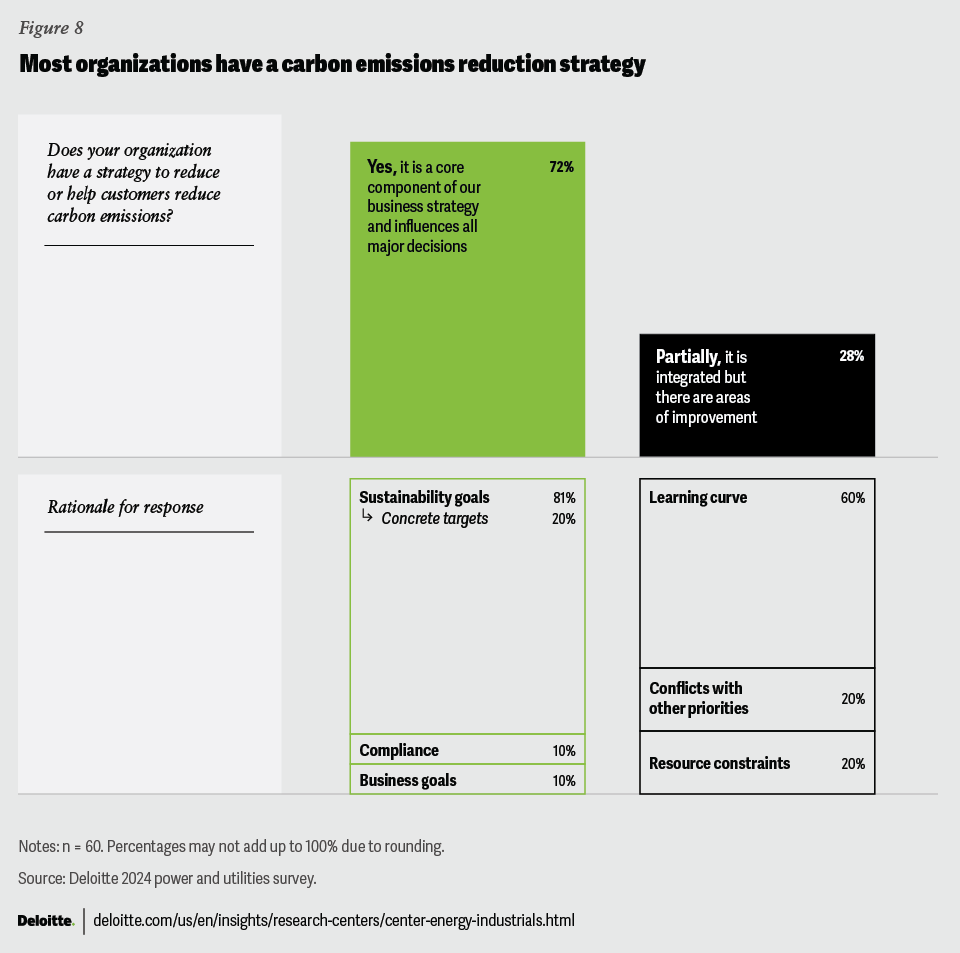

Renewables are core to carbon management taking center stage in the power industry. Seventy-two percent of respondents to the Deloitte power and utilities survey indicate their organizations have a strategy to reduce or help customers reduce carbon emissions, primarily to meet sustainability goals, while most respondents with partial integration invoked a learning curve challenge (figure 8). Renewables contribute to high-integrity carbon management solutions in two ways: by powering DAC infrastructure and providing an emerging carbon dioxide removal (CDR) approach.

Voluntary offset markets shift to CDR credits

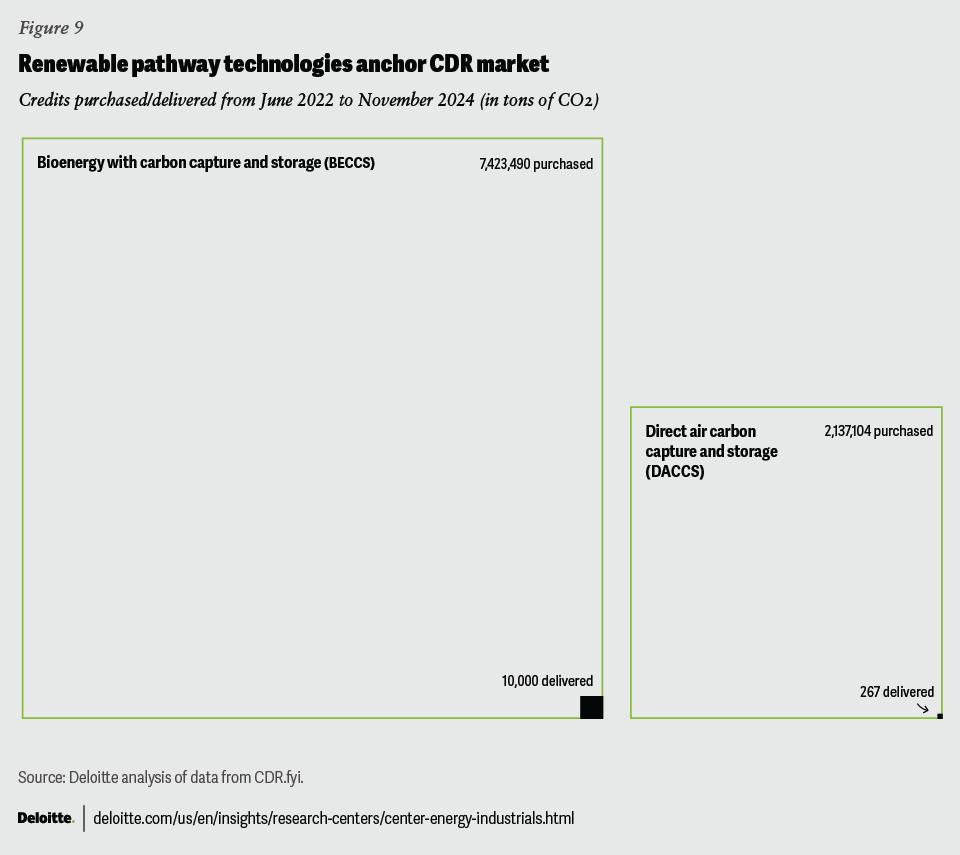

Amid recent questions of credit validity and integrity in voluntary carbon markets, organizations have pivoted from purchases of renewable energy offsets to focus on operational decarbonization and carbon removal.63 Voluntary credits tied to renewable projects peaked in 2021 with 83.7 million carbon offset purchases, dropping to 59.4 million in 2023 but still accounting for 36.6% of total offset purchases.64 At issue is that funding from carbon offsets has a negligible impact on the buildout of already low-cost solar and wind resources. Meanwhile, the emerging CDR credit market has seen a significant increase in investment, particularly from technology companies. CDR credit purchases grew from 4 million to 6.6 million tons between the first three quarters of 2023 and of 2024.65 Credits generated from renewable-powered or emerging renewable methods such as DAC and bioenergy with carbon capture, and storage, account for 84% of purchases (figure 9).66

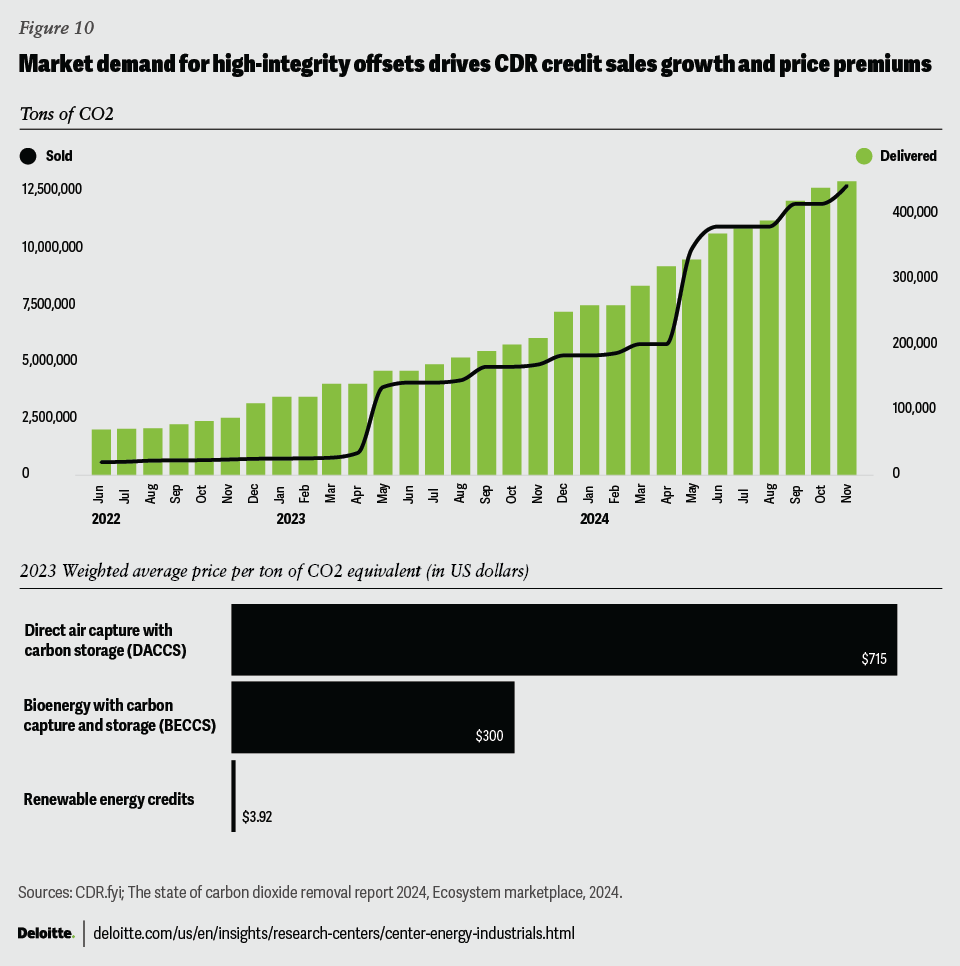

Strong CDR credit sale activity coupled with comparatively high prices is reflective of market desire for and confidence in CDR methods to drive real removals (figure 10). High price levels may provide a monetization pathway for emerging renewable energy providers to partner with CDR projects and negotiate shares of generated credits. The industry has recently called for statutory standards to improve monitoring, reporting, and verification to drive further confidence in removal schemes.67 The US federal government’s release of guiding principles for the development of high-integrity voluntary carbon markets and the emergence of a global carbon market could also help firm demand.68

DAC and data center infrastructure intersect on resource constraints and opportunities

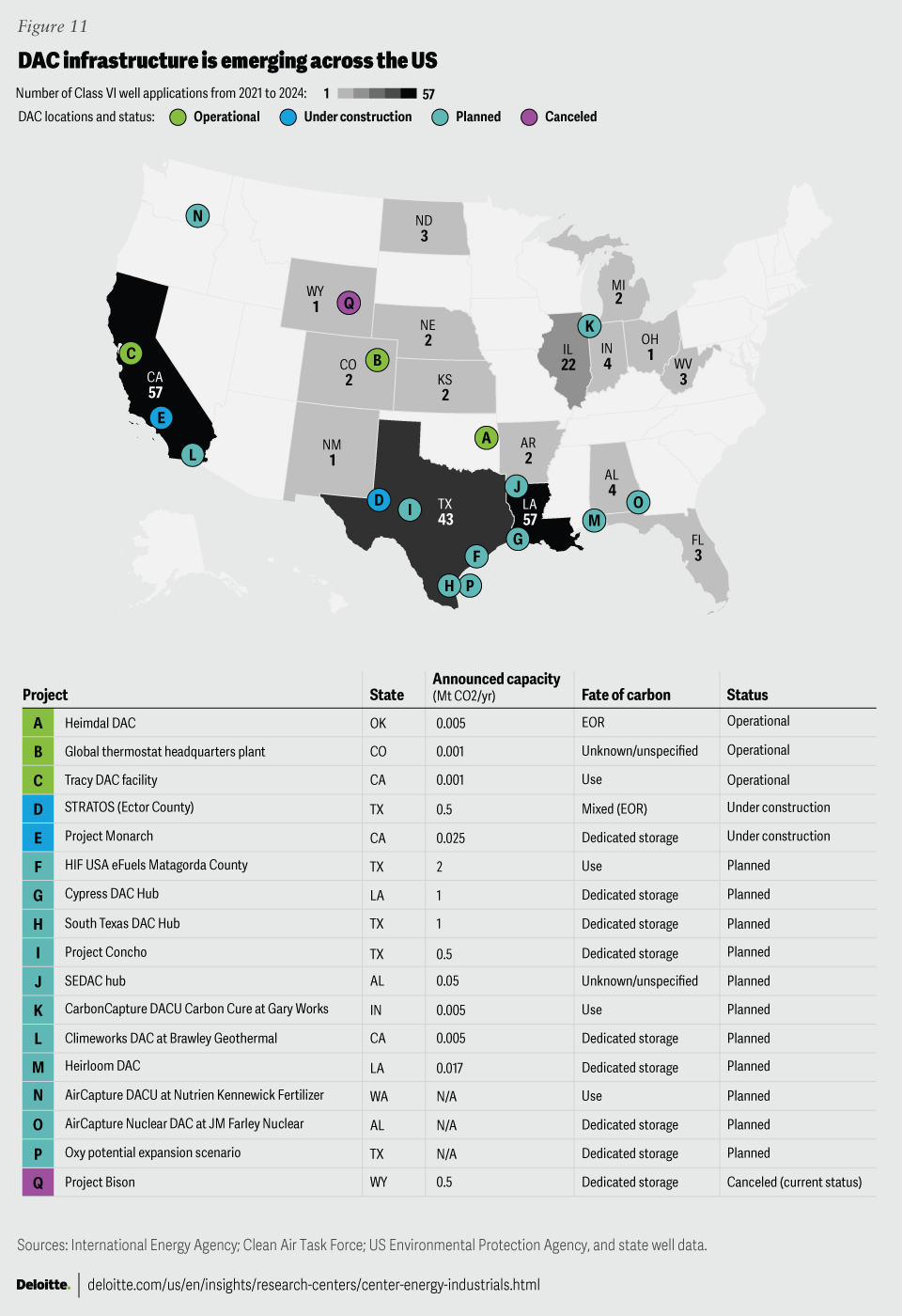

The United States has three operational DAC facilities, with 13 more in various stages of development,69 including two that have received a combined US$1.2 billion from the DOE DAC Hubs program,70 which aims to develop four hubs in total (figure 11).71 Some facilities are facing clean energy procurement challenges. A facility in Wyoming, planned to be one of the largest DAC facilities in the world, recently scrapped its plans as it claimed it could not procure enough emission-free energy, citing rising competition for renewables from data centers.72

Only two of the projects are premised on using captured carbon for enhanced oil recovery, a longstanding revenue stream for captured carbon. Most plan to utilize dedicated storage or sell captured carbon for direct use.73 An opportunity for captured carbon sale and use is in the development of lower-emission cement,74 which can support the increasing demand for green concrete driven by AI data center growth.75

In 2025, pending policy developments from the new administration, carbon management technologies are poised for growth driven by more robust carbon market guidelines, significant supplier delivery obligations, and revenue opportunities.

About the Deloitte survey

To understand the outlook and perspectives of organizations across the power and utilities industry, Deloitte fielded a survey of 60 US executives and other senior leaders in September 2024. The survey captured insights from respondents in the generation, transmission, and distribution segments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}