2025 Power and Utilities Industry Outlook

Utilities are navigating a new era of growth and transformation as they address emerging challenges and rising demand

The United States is experiencing a surge in electricity demand, driven in part by a confluence of unprecedented electrification, artificial intelligence–driven data center expansion, and a resurgence in industrial reshoring or manufacturing. In September 2024, year-to-date electricity demand rebounded with a 1.8% increase, following a 1.7% decline during the same period in 2023 helped by mild weather conditions.1 However, this surge isn’t temporary; it is expected to be sustained growth after two decades of stagnant demand. This will likely fundamentally change the electricity landscape in several ways.

- Data centers, fueled by the rise of generative AI, machine learning (ML), and cryptocurrency-mining activities, are becoming major electricity consumers. Power demand estimates vary widely. According to Deloitte analysis, by 2030, electricity demand from data centers is projected to soar to approximately 515 to 720 terawatt-hour (TWh), up from about 180 to 290 TWh in 2024—a 15% to 17% compound annual growth rate.2

- Electrification continues to expand across transportation, industrial processes, and buildings and homes. Electric vehicle sales are up 8% year over year (YoY), now accounting for 9% of new car sales in the first three quarters of 2024, despite a slight decline in the first quarter of 2024.3Government incentives in at least 25 states have accelerated the adoption of heat pumps.4

- Federal policies promoting domestic content have further amplified this demand surge by relocating offshore manufacturing and expanding domestic production in strategically important sectors. Between Jan. 1, 2021, and March 1, 2023, companies announced more than 150 onshore manufacturing facilities in the United States, with an annual electricity usage exceeding 13,000 GWh, half of which is expected to be operational by 2025.5

This increase in demand has contributed to a corresponding rise in power generation. As of September 2024, utility-scale power generation reached approximately 3,287 billion kWh, marking a 3% YoY increase.6 Concurrently, renewable energy, particularly solar, experienced growth, with a 30% increase, compared to 13% in the same period in 2023.7 It is expected to be the fastest-growing energy source by year-end, potentially achieving a 34% growth rate, according to Deloitte analysis of US Energy Information Administration data.8 Natural gas, which generates about 43% of US electricity, saw a 4.1% increase this year,9 maintaining its position as the dominant power source.10 Natural gas generation is expected to rise by 3.5% by year-end,11 although its share is projected to decline to 40% in 2025 due to high fuel prices.12

Electric power utilities are responding to this dynamic landscape with record capital expenditures, which could reach US$174 billion by the end of 2024.13 Of these expenditures, 42% are expected to be allocated to transmission and distribution systems.14 Many are revising their integrated resource plans (IRPs) to accommodate higher load growth projections.15 However, amid increasing demand, utilities are also facing challenges, such as:

- Supply chain disruptions, particularly the increase in lead times for procuring transformers—from around 50 weeks in 2021 to 120 weeks (reaching up to 210 weeks for larger units) on average in 2024—are impacting grid modernization efforts.16

- The escalating costs of extreme weather events, with a record US$53 billion spent in the United States between January and August 2024—roughly double that of the entire 2023—places additional strain on grid infrastructure and finances.17

- The process for rate case approvals to recover capital investment costs may move more slowly than the dynamic market in which the utilities now find themselves as estimates for incremental demand continue to rise.18

These challenges are driving up costs. Rising wholesale prices, projected to increase by 19% on average between 2025 and 2028, combined with escalating distribution expenses, are likely to result in higher electricity bills for consumers.19As of August 2024, the year-to-date average power price across all sectors stood at 13.09 cents per kWh, reflecting a 2.7% YoY increase due to rising demand.20

In 2025 and beyond, electric power utilities can consider the following while making strategic choices as they keep a focus on reliability, affordability, and sustainability.

- Increasing data centers: Utilities are adopting a multifaceted approach to help meet increasing demand

- Greater nuclear integration: Utilities are implementing strategies to boost nuclear power use

- Distributed energy resources integration: Utilities look at sum-of-parts solutions

- Workforce 2.0: Utilities are cultivating a new generation of talent and embracing new skills

- Carbon management: Some utilities are exploring a toolkit to manage ‘last mile’ emissions

1. Increasing data centers: Utilities are adopting a multifaceted approach to help meet increasing demand

Approximately 75% of the top 35 electric power utilities in the United States have reported a rise in electricity demand from data centers.21 These energy-intensive facilities currently consume 6% to 8% of total annual electricity generation, and according to Deloitte analysis, this is expected to rise to 11% to 15% by 2030.22 This rapid growth presents a complex challenge for electric power utilities: how to meet this escalating demand while simultaneously transitioning to a cleaner energy mix.

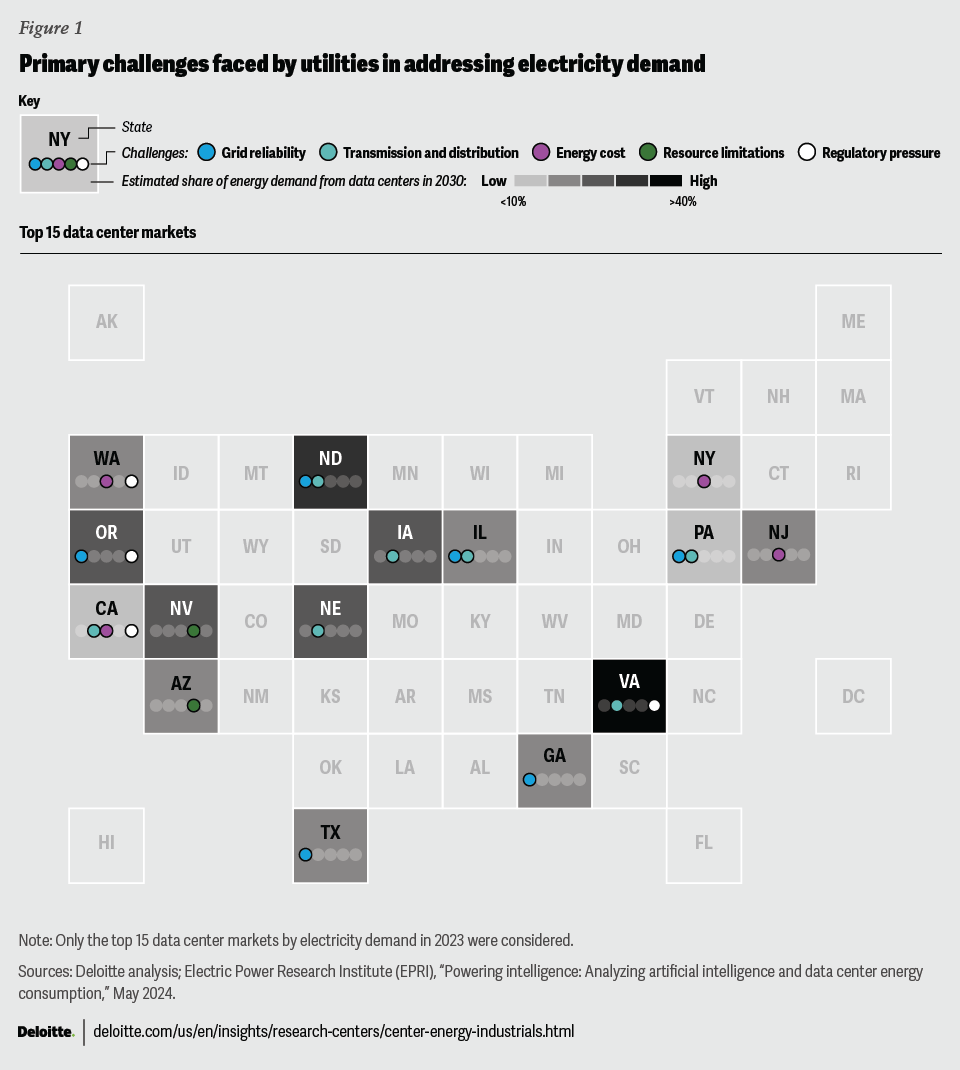

In a Deloitte survey of power and utilities executives (see “About the Deloitte survey”), grid infrastructure limitations emerged as the key challenge in providing reliable power to data centers.23 Other challenges including regulatory constraints and resource limitations vary across regions (figure 1). To help address these challenges, utilities are adopting a multipronged approach.

- Increasing efficiencies of current infrastructure by deploying advanced technologies: Utilities are deploying grid-enhancing technologies and advanced conductors to add capacity and flexibility to the existing transmission system. These technologies offer a cost-effective way to expand capacity compared to rebuilding transmission lines. Studies indicate that reconductoring US power lines with advanced conductors could help quadruple the projected transmission capacity by 2035.24 A few states have signed bills mandating utilities to consider grid-enhancing technologies as a shorter-term solution in their IRPs.25

- Ensuring reliability through multiple sources of electricity: To ensure reliable baseload power, some utilities along with state or service territory might consider extending the life of existing coal assets and proposing new gas-fired capacity, while simultaneously exploring cleaner alternatives in the regions of increased demand. The regulatory approval obtained by Georgia Power in April 2024 to build three new gas plants and extend operations of two coal plants exemplifies this trend.26 Additionally, nuclear energy’s ability to provide clean baseload power makes it an attractive option for many data centers (we explore this more in our next trend). For example, Microsoft secured a long-term power purchase agreement with Constellation Energy for power from a decommissioned nuclear plant expected to restart by 2029—although it’s pending regulatory approval.27

- Addressing cost concerns through tariff approaches: The expansion of data centers necessitates substantial investments in grid infrastructure and generation capacity, and estimates indicate that US utilities may need around US$36 billion to US$60 billion by the end of the decade.28 This significant capital requirement may raise concerns about cost recovery and potential impacts on ratepayers. To help address these challenges, some utilities are introducing new wholesale power sales rate schedules for data centers and larger loads to distribute costs more equitably. This strategy involves shifting transmission costs from residential customers to larger energy users like data centers. Various tariff approaches are being considered to achieve this, including:

a. New rate structures: AEP Ohio’s request for new rate structures was approved by the Public Utilities Commission of Ohio; however, pay share is yet to be agreed upon.29 Moreover, AEP Ohio has also requested large load tariff modifications in Indiana and West Virginia.30

b. Clean transition tariffs: Duke Energy proposed accelerating clean energy tariffs in partnership with tech companies to design new rate structures that enable large customers to directly support clean energy investments.31

- Boosting resilience and facilitating deployment with onsite generation: Some utilities and tech companies are increasingly partnering to colocate data centers with power generation facilities on the same site. This strategy offers several potential benefits, such as easing transmission constraints, reducing costs, and ensuring resiliency with onsite power.32 However, this strategy could face regulatory scrutiny and community pushback.33 Despite these obstacles, the potential for innovation and efficiency is undeniable. Yet, there is a caveat: As the volume of data centers continues to rise, the number of suitable sites for this colocation strategy could be limited. Over time, the rapid expansion of data centers may outpace the capacity of these reliable sites.

Balancing addressing demand with sustainability goals

As data centers continue to demand reliable power to meet a share of their anticipated demand, some are seeking to power their operations with clean energy by supporting the buildout of renewable energy. Solar and wind capacity contracted to US data centers has grown to nearly 34 GW through 2024, representing close to half of the total renewable contracts in the United States, and could reach 41 GW by 2030.34 As the growth in renewable power accelerates, energy storage solutions are also expected to increase penetration to address the intraday and seasonal variability.

Water scarcity is another concern. Data centers are water-intensive, and their proliferation, especially in water-stressed regions, could exacerbate existing shortages.35 As noted in our 2024 Power and Utilities Outlook, electric power companies are increasingly monitoring water stress, with some incorporating water risk into their financial disclosures, and this is expected to continue in the upcoming year.36

In 2025, utilities, policymakers, and data center operators will likely collaborate to balance priorities such as grid upgrades, renewable energy procurement, water resource management, and equitable cost allocation. Different business models will emerge, with large utilities partnering with local ones to manage data center loads. For example, Tennessee Valley Authority is collaborating with local distribution companies on demand response and energy efficiency initiatives37 and has also partnered with Origis Energy to develop a power plant for Google’s data centers in Tennessee.38

At the same time, there may be a shift of hyperscalers moving ahead without utilities as key partners, based on an October 2023 estimation that projected one-third of data centers would likely be powered by independent power producers and other business structures in 2030.39

2. Greater nuclear integration: Utilities are implementing strategies to boost nuclear power use

In 2024, utilities began rethinking the role of both existing and new nuclear, likely recognizing its potential to provide a differentiated value proposition for a decarbonized grid.40 This shift is reflected in actions and plans, in which they appear to be increasingly incorporating nuclear power into their portfolios in multiple ways.41

- Extending and enhancing existing sites: Utilities are actively extending reactor operating life, uprating existing capacity, and even restarting closed reactors.42 A report prepared for the Department of Energy (DOE) indicates that an additional 60 GW to 95 GW could be built at existing nuclear power plant sites across 31 states.43 Leading utilities are actively pursuing value from their nuclear assets. For example, Duke Energy Carolinas and Duke Energy Progress have recommended extending the lives of existing nuclear plants, recognizing their role in providing reliable and carbon-free electricity.44 Public Service Enterprise Group Inc. is pursuing thermal and efficiency upgrades at their co-owned nuclear facilities, potentially increasing output by up to 200 MW and qualifying for tax credits.45Even closed reactors are being reconsidered. In 2023, Holtec filed an application with the US Nuclear Regulatory Commission to resume operations at the Palisades nuclear plant in Michigan, which was retired in 2022.46

- Repurposing coal plant sites: Transitioning retiring coal plants to nuclear plants offers an opportunity to leverage existing infrastructure, accelerate deployment, and mitigate economic losses in coal-dependent communities. A study by the DOE estimates that 36 states have suitable coal sites that could host 128 GW to 174 GW of nuclear capacity, including advanced reactors, potentially saving up to 35% of construction costs.47 At least 11 states have publicly expressed interest in repurposing their coal sites with nuclear energy.48 This approach could also offer significant carbon reduction benefits of up to 614 million to 835 million metric tons of carbon dioxide per year.49

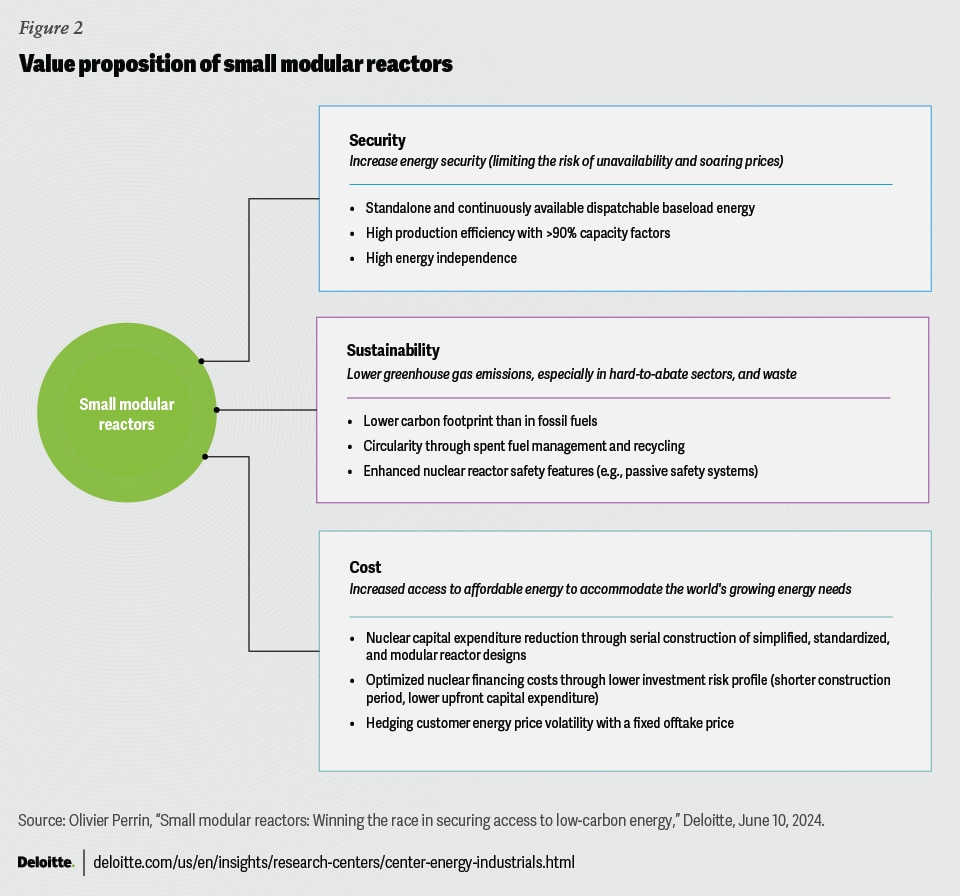

- Embracing advanced nuclear technologies: Small modular reactors (SMRs) and other advanced nuclear technologies hold potential for enhancing grid flexibility, safety, and resilience (figure 2). Their smaller size, modular design, shorter time to market, and enhanced safety features can allow for deployment in locations not suitable for traditional reactors. Some SMR designs can operate for up to 40 years without the need for refueling and can be located closer to energy consumers, overcoming grid constraints and enhancing safety.50 More utilities are likely considering advanced nuclear to boost grid capacity as they offer greater siting flexibility than traditional nuclear plants.

A confluence of factors is driving these actions.

- Nuclear as a base load resource: Despite the high construction costs, nuclear power plants can offer a compelling solution for clean and reliable energy. With a single reactor typically generating 800 MW or more, these plants can easily meet the substantial power demands of data centers, which range from 50 MW to 100 MW (and up to 1000 MW for AI-related data facilities).51 This steady generation can ensure data centers have ample, reliable electricity, aligning with sustainability goals and reducing carbon footprint.

- Supportive policy environment: Certain government incentives and research and development investments may be helping contribute to a favorable environment for nuclear energy development. This includes a significant financial incentive—for instance, the US$2.5 billion Advanced Reactor Demonstration Projects that aim to accelerate the deployment of next-generation nuclear technologies.52 Tax credits—a 30% investment tax credit for new nuclear projects and a production tax credit of US$27.5/MWh for the first 10 years of operation—are helping make nuclear energy more financially attractive.53

- Growing investor confidence: Fourteen of the world’s largest banks and financial institutions are pledging increased support for nuclear energy to meet the COP28 goal of tripling nuclear capacity by 2050.54 In 2024, Constellation Energy issued the first US corporate green bond for nuclear projects to be used for maintenance, expansion, and life extensions of nuclear energy projects.55 The share of nuclear-related bonds in the utilities sector has risen to 3% year-to-date, up from under 1% in 2021 and 2022.56 Financing has focused on refurbishing existing reactors, but sustainability-themed bonds now also support new builds.

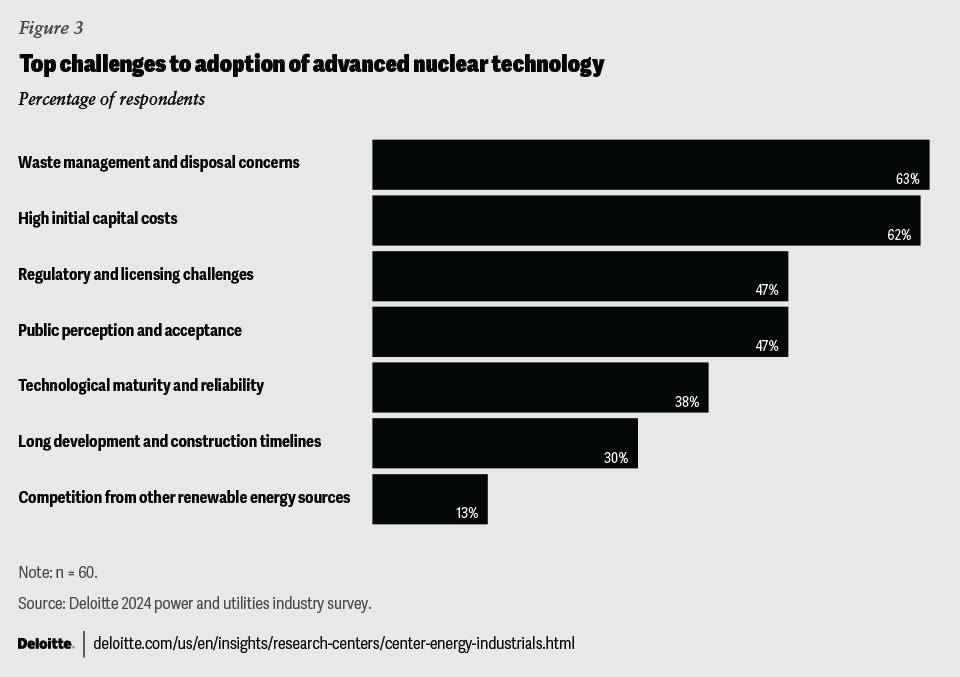

Despite this momentum, challenges remain. Deloitte 2024 power and utilities industry survey respondents recognized waste management and disposal concerns and high initial capital costs as the top challenges to adoption of advanced nuclear technology (figure 3).57

Additionally, the United States may need to strengthen its domestic uranium supply chain. The bipartisan Prohibiting Russian Uranium Imports Act, enacted in May 2024, banned the import of unirradiated low-enriched uranium from Russia and allocated nearly US$3 billion in federal funding to enhance domestic uranium production.58 This legislation aims to strengthen US energy security and stimulate the domestic uranium industry.

In 2025, utilities are expected to continue to:

- Seek partnerships to accelerate the deployment of advanced reactors to drive innovation and cost reductions.

- Find creative ways to share financial risks between public and private sectors and unlock capital.

- Engage proactively with communities and stakeholders to address concerns about safety and waste management.

3. Distributed energy resources integration: Utilities look at sum-of-parts solutions

In 2024, some states and electric utilities integrated behind-the-meter distributed energy resources (DERs) and flexible loads through compensations, rate designs, and other models. This occurred against the backdrop of rising electricity demand, on one hand, with DERs providing reliability to the grid and challenges such as permitting, and interconnection with building utility-scale resources increasing, on the other. Additionally, extreme weather events, which have been increasing due to climate change, are also impacting the electricity system and causing power failures. Between 2000 and 2023, 80% of all major power outages were due to severe storms, wildfires, and extreme heat.59

As utilities address these challenges, DERs can provide a variety of capabilities, including energy efficiency, demand response, power generation, and energy storage to the grid. By combining these capabilities, utilities can create smart systems such as non-wire alternatives, microgrids, and virtual power plants (VPPs), optimizing grid operations and enhancing resilience. For example:

- DERs used as non-wire alternatives, regardless of ownership, have the potential to reduce system operating costs and delay the need for system upgrades.60 For example, Xcel Energy recently proposed to state regulators the construction of a network of strategically located solar-powered energy storage hubs. These hubs would be linked with technology to operate in concert, designed to enhance grid efficiency and reliability.61

- The increasing availability of battery electric storage systems has strengthened the case for microgrids to enhance grid resilience and reliability. In February 2024, SDG&E introduced four advanced microgrids capable of operating independently or in conjunction with the larger regional grid, which provide a combined storage capacity of 180 MWh across four substations.62

- By combining high-capacity, low-deployment DERs like EV storage with vehicle-to-grid technology and low-capacity, ubiquitous DERs like smart thermostats, utilities can create VPPs to optimize peak load management. Deloitte’s recent analysis points out that residential electrification creates a load that could potentially serve itself by 2035.63

Combination of such capabilities can help not only strengthen the grid at its most vulnerable points supporting reliability, particularly in areas experiencing high energy demand, but also provide resiliency, mitigating the risk of disruptions.

Additionally, utilities may still have an opportunity to unlock potential from commercial and industrial customers.64 The immense energy demand of data centers, often seen as a challenge, can become an asset for the future grid. Their ability to rapidly adjust power consumption levels and location can make them candidates for participation in VPPs, enhancing grid stability and supporting the integration of renewable energy sources.65 The introduction of FERC 2222, which allows DERs to participate in the energy market, would expand the services that VPPs can provide.66 Though there have been delays in the implementation across Independent System Operators,67 in April 2024, New York launched the nation’s first program to integrate aggregations of DERs into wholesale markets.68

While these solutions may seem isolated, they are expected to continue to converge and could continue to create synergies for a more reliable and sustainable electricity infrastructure. This integration can deliver economic benefits to both the grid and customers. As the industry prepares for rising demand from data centers, VPP platforms leveraging AI and ML algorithms can aid in managing power generation assets, understanding customer behavior, and adjusting output levels based on demand and forecast consumption.

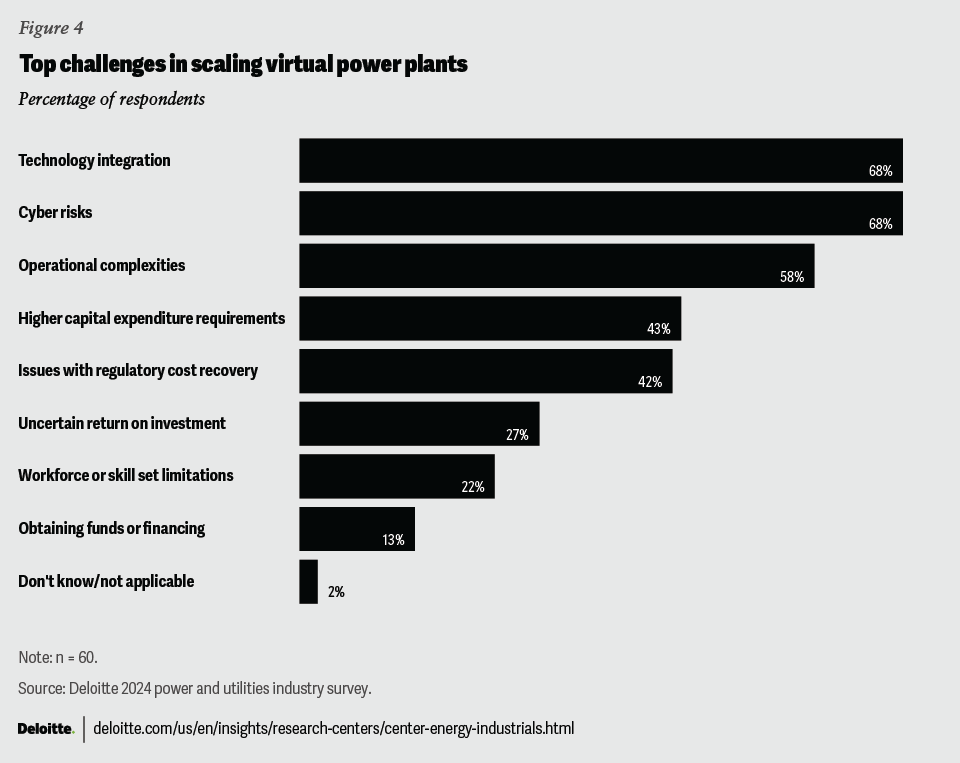

However, currently, there are hurdles that need to be overcome to facilitate greater investment in VPP infrastructure. According to Deloitte survey respondents, technology integration, cyber, and operation complexities are the top three challenges in scaling VPPs (figure 4).69

In 2025, utilities will likely continue to integrate DERs into the grid with emphasis on the following:

- Adopting advanced forecasting techniques for DERs and integrating their impacts into utility load forecasting processes

- Partnering with DER aggregators to create new business models

- Enhancing customer engagement to tap into that potential

However, the success of DER integration could also hinge on robust community engagement. This is likely important for enhancing regulatory outcomes by working to ensure that DER projects address the specific reliability needs of the community. By involving local stakeholders in the decision-making process, building trust, and fostering participation, regulators and utilities might help develop more effective and equitable energy solutions that can benefit both the community and the broader energy system.

4. Workforce 2.0: Utilities are cultivating a new generation of talent and embracing new skills

In the last two years, utilities saw the fastest employment growth compared to employment across traditional industrial sectors.70 Consolidated Edison, for example, hired more than 1,600 new employees in 2024 alone, the most since 1973.71 However, despite recent employment growth, which has helped alleviate some aging workforce concerns, a skills gap is emerging. Over half of the current utility workforce has less than 10 years of experience, indicating a need for upskilling and development.72 Competition for workforce from other sectors and the importance of retention given the pace of changes in the industry landscape are additional challenges.

To meet the challenges of the evolving energy landscape, some utilities are implementing various initiatives, including record hiring efforts73and developing integrated workforce development programs, while also balancing cost management and efficiency.74

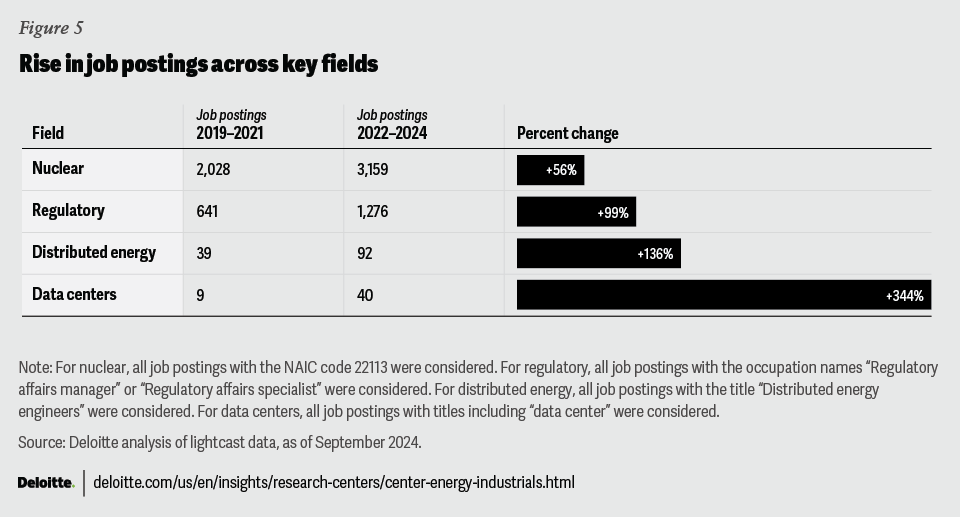

Record hiring efforts: Analysis of job posting data shows a rise in occupations, especially around the key trends identified (figure 5).

- The increase in data centers may require talent with specialized expertise for their operation, management, and energy optimization. Utilities are actively seeking engineers, analysts, technicians, and support staff to help these facilities become integrated into the grid. In fact, job postings for data center–related roles are surging in key growth markets like Arizona, New Jersey, and Texas.75

- With renewed interest in nuclear power, the demand for a skilled nuclear workforce is rising. Estimates suggest the need to grow the nuclear workforce by approximately 275% to support new reactor construction, operations, and supply chain needs.76 Seventy percent of DOE’s science, technology, engineering, math workforce programming investments target nuclear, including security priorities and programs for undergraduates, graduates, and students, as well as faculty of minority-serving institutions.77 Utilities are often competing with other sectors that are also looking at similar skills to address their power needs.

- The rise of DERs needs a workforce capable of integrating these technologies into the grid while navigating increasingly complex regulatory environments. The DOE's grid connection road map highlights the need for professionals with expertise in both engineering and policy to manage the interconnection of DERs.78 This has led to a surge in job openings for engineers, cybersecurity specialists, regulatory specialists, and attorneys specializing in this area.

Integrated workforce development programs: Some utilities are implementing a variety of workforce development programs to support the growing demand, especially demand for clean energy and energy-efficient services.

- Specialized training academies: Focused programs designed to equip employees with the skills needed for specific roles, such as DER integration, cybersecurity, and data analytics. DTE Energy, for example, is expanding its energy efficiency academy to train workers in energy-efficient home repairs, supporting both community needs and the growing demand for energy efficiency expertise.79

- Technology integration: Leveraging AI, virtual reality, and other technologies to enhance training and provide employees with the tools they need to succeed. Southern California Edison, for instance, is investing in technologies to improve their data analytics skills, enhancing decision-making and operational excellence using digital and AI capabilities.80

- Financial investments: Funding for scholarships, apprenticeships, and other programs helps support the development of a skilled workforce.

- Community partnerships: Collaboration with educational institutions and community organizations can create pathways for individuals to enter the energy industry, particularly individuals belonging to underrepresented groups. Exelon has partnered with the Cal Ripken, Sr. Foundation to open 81 science, technology, engineering, and math centers across various cities they serve, providing students with opportunities to gain hands-on knowledge and skills in areas like coding and engineering.81

As the energy transition accelerates, utilities should consider ways to further adapt their workforce strategies. Key areas of focus could include:

- Technology empowerment: Leveraging AI and advanced analytics can help optimize operations, enable flexible work arrangements, and provide employees with the tools and insights needed to manage a decarbonized grid.

- Modular skills development: Utilities can adopt a modular approach to training to allow employees to acquire targeted skills and required expertise, keeping pace with technological advancements.

- Cultivating a culture of innovation: It is important to foster a workplace that encourages continuous learning, experimentation, and collaboration to drive innovation and address the challenges of the energy transition.

5. Carbon management: Some utilities are exploring a toolkit to manage ‘last mile’ emissions

Even as utilities transition to cleaner energy sources, they face the challenge of addressing “last mile” emissions—greenhouse gas emissions that persist despite best efforts. These emissions arise from various sources including residual fossil fuel use—emissions from natural gas power plants, carbon footprint associated with manufacturing and transporting of power-generation components, methane leaks from natural gas infrastructure, and emissions from natural gas combustion in homes and businesses.

To help address these challenges, utilities are exploring a diverse toolkit of carbon management strategies. Carbon capture and storage (CCS), carbon offsets, and carbon dioxide removal (CDR) are emerging as key components of the comprehensive carbon reduction plans of utilities.82 Initiatives like the Low-Carbon Resources Initiative are considering potential offset or carbon removal strategies.83

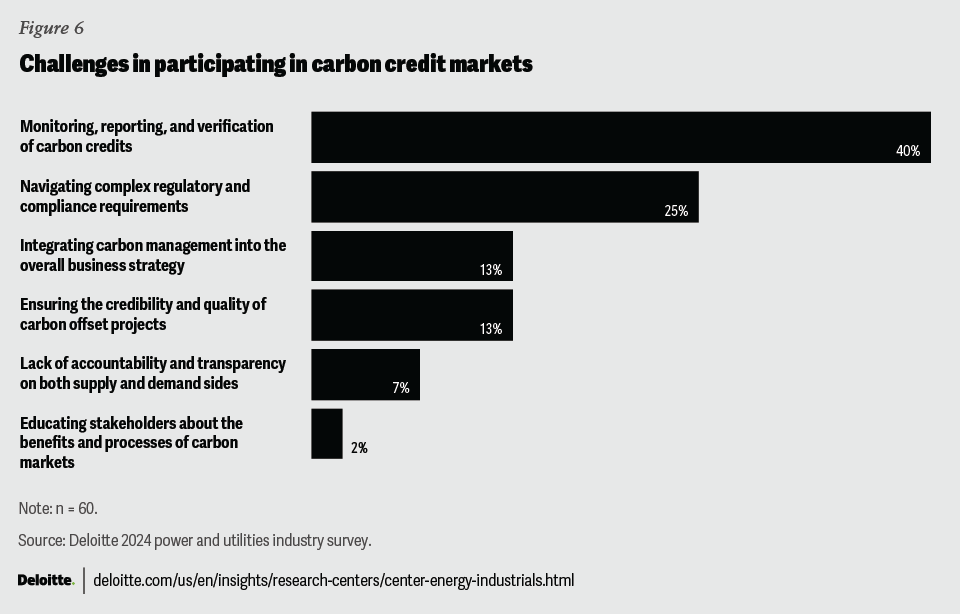

1. Some utilities may be considering carbon offset markets to compensate for residual emissions and achieve announced targets by integrating offset measures into broader emission reduction plans. This involves investing in projects that reduce or remove greenhouse gas emissions elsewhere, such as forestation, landfill gas capture, and hydrofluorocarbon refrigerant reclamation.84 Some utilities are even integrating carbon offsets into customer-facing programs, offering immediate action on emissions while longer-term infrastructure changes are implemented.85 However, challenges remain for survey respondents in ensuring project credibility and obtaining regulatory approvals (figure 6).86

2. CCS technologies can capture carbon dioxide emissions from power plants and other sources and store them underground. Utilities are increasingly investing in CCS projects, driven by technological advancements and policy incentives, including tax credits and grant programs.87 However, CCS faces challenges related to geologic suitability, pipeline infrastructure, permitting, long-term liability, water intensity, and public acceptance.

3. CDR technologies go beyond capturing emissions from specific sources and aim to remove carbon dioxide directly from the atmosphere. Some utilities are exploring investments in direct air capture technology start-ups88 and others are piloting co-location of customer load and direct air capture (DAC) of CO2.89 In fact, energy-adjacent activities can enable utilities to generate revenue with CDR opportunities.90 For example, mechanical tree thinning, as a part of vegetation management, produces millions of tons of waste biomass. Instead of wasting the wood, it can be buried, used for biochar to improve soil, or even reused in utility operations as a power generation fuel with bioenergy and carbon capture and storage.

In 2025 and beyond, utilities will likely continue to explore economically viable carbon reduction and removal technologies. However, carbon strategies may evolve with potential policy changes from a new administration. In any event, full-scale deployment is likely still several years away but progress on these first-of-a-kind projects is expected to continue.

About the Deloitte survey

To understand the outlook and perspectives of organizations across the power and utilities industry, Deloitte fielded a survey of 60 US executives and other senior leaders in September 2024. The survey captured insights from respondents in the generation, transmission, and distribution segments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}