Grocery shopping with personality

Most consumers identify with one of five food personalities, influencing what they buy and how much they spend

Randy Jagt

Adgild Hop

Evan Sheehan

Justin Cook

Siddharth Mishra

The price of groceries can’t go up forever, or at least not as fast as it has these past few years.1 Food companies and grocers alike are pivoting, and the essential thinking seems to boil down to this: If you can’t charge a higher price for it, you better sell more of it. Of course, this increased volume should also be profitable to help keep investors happy and the flywheel of reinvestment turning.2

As one of many approaches to boosting volume, the industry is pivoting “from mass to micro.” Grocers want to get closer to their consumers and engage them as individuals.3 The idea is that both parties could benefit from messages and entire systems explicitly geared toward individual needs. For grocers, this may mean understanding each individual’s most profound connection to food.

What should a company know about its consumers to help facilitate personalization? There are demographic basics like income, age, and household size—structural factors that heavily influence what and how much gets in the shopping cart on the weekly trip to the grocery store. But people’s relationships with food often matter, too. And those relationships can be diverse, from the person who uses food primarily to live a healthy life to the shopper hoping to save as much of their paycheck as possible.

Call it an approach to food or food personality. This research—based on survey responses collected monthly since September 2022 from 228,000 adults across 12 countries—shows that independent of demographics, personality has predictive power for what people buy and how much they spend.

Probing for personality

Attempting to identify food personalities is not new. In the 19th century, French author André Borel d’Hauterive developed a taxonomy that spanned gastronomes to gluttons.4 But it may be time for an update appropriate for the modern grocery shopper—one that works globally yet highlights key differences. After all, the world has changed:

- Social media, cooking shows, travel, restaurant experiences, and more have created a global foodie culture. For some, food is a passion and a way to embrace one of life’s great pleasures.

- Modern life is hectic. Some consumers may seek convenience from food to save time and hassles.

- High food inflation is causing shoppers to be more careful with grocery spending,5 but some consumers, even regardless of income level, may have always leaned toward frugality. These consumers would likely be fine with affordable, basic meals if they minimize their expenses.

- With medical breakthroughs, greater longevity, and a better appreciation of the connection between food and health, others may now primarily see food as fuel for building healthy bodies and minds.

- Climate change concerns have made some people more sustainability-focused. For them, food can often express their values, and their choices around food are a means to live them.

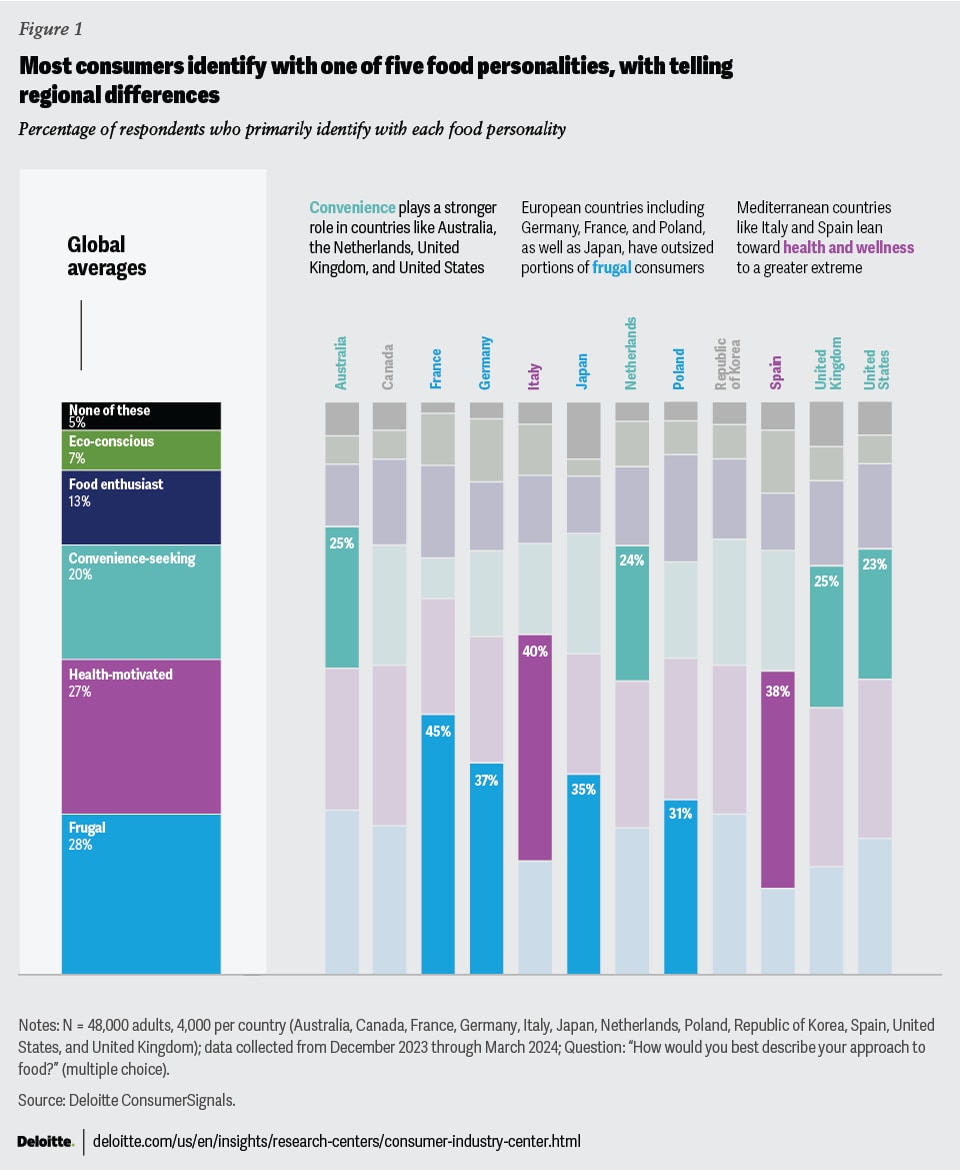

Inspired by these changes, the survey tested for the prominence of a corresponding set of food personalities—the food enthusiast, convenience-seeking, frugal, health-motivated, and eco-conscious. Much like the concluding insight from the movie The Breakfast Club, each one of us can inhabit many of these different personalities from time to time. However, we found that most people surveyed (95%) recognize that they have a primary personality when it comes to food (figure 1).

The top two personalities, frugal and health-motivated, are found in essentially equal proportions globally and represent over half of all consumers. However, there are important global patterns in these profiles. For instance, Mediterranean countries, including Italy and Spain, tend to have more consumers who let health be their primary guide. In contrast, other European countries, including Germany, France, and Poland, have more consumers with frugal personalities dominant.

While third most prominent globally, the convenience-seeking personality is more prevalent in the stereotypically overworked and harried West. The United States and Australia have disproportionately high numbers of convenience-seeking personalities, and in the United Kingdom, it is the second most common, outstripping frugal.

The last two personalities are rarer, but, as the research shows, they are incredibly passionate about food in their different ways and are willing to spend what they need at the grocery store. The food enthusiast personality, aka “foodies,” hits double digits at 13% of the population. A smaller 7% of consumers have personalities that prioritize sustainability, although they come in somewhat higher numbers in France, Germany, and Spain. These personalities may represent smaller numbers, but they also may be poised to grow over time as they skew toward younger consumers. Meanwhile, frugal and health-motivated personalities have disproportionately older consumers.

Playing out the patterns

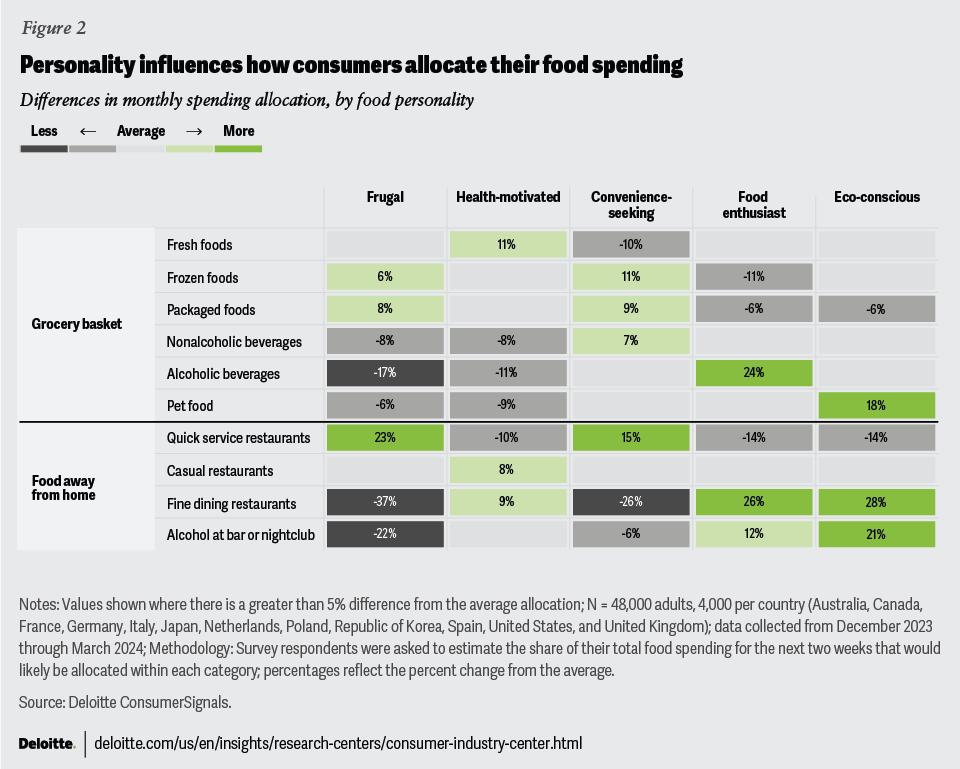

Personality partly shapes what is put in the grocery basket. Like the differences by country and cultural affinity described above, several almost stereotypical shopping behaviors shine through (figure 2).

Running down the categories at the grocery store, the health-motivated personality allocates more of their budget to fresh food among respondents. The convenience-seeking personality allocates the least to fresh food and instead spends more on frozen and packed foods, as does the frugal personality. The health-motivated and frugal personalities surveyed both seem to relatively avoid soft drinks and similar beverages, perhaps preferring to drink more water, with different motivations. Soda is not at the top of the list for the foodies, either. Instead, foodies spend a disproportionate amount on alcoholic beverages, which the frugal and health-motivated proportionally shun. And eco-conscious personalities surveyed may have more furry friends at home as they allocate more to pet food.

Food personality appears helpful outside of the grocery store. The food-away-from-home options suggest quick-service restaurants are favored by both the frugal and the convenience-seeking personalities surveyed. The health-motivated personality favors casual restaurants and fine dining. The foodies are doubling down on fine dining and enjoying bars and the nightclub scene. Frugal personalities surveyed are unlikely to be in those locations, but perhaps surprisingly, the sustainability-focused personality enjoys fine dining as much and nightclubs even more than the foodies.

Personality meets price pressure

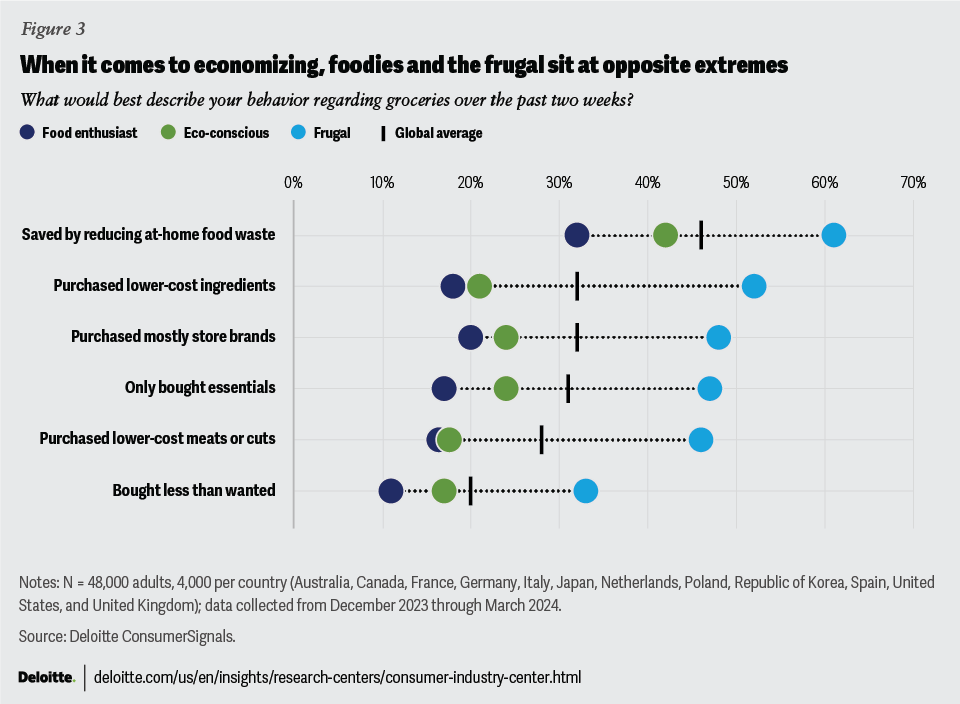

Over the past two years of high inflation, all food personalities climbed Deloitte’s Food Frugality Index, a measure that captures the percentage of global consumers engaging in six distinct cost-saving behaviors at the grocery store.6 This trend of all personalities becoming more frugal in practice is a reminder that price still matters to everyone, regardless of personality.

But the extent to which people engage in frugal behaviors varies across personalities (figure 3). As expected, the frugal personality is most likely to engage in all six frugal behaviors, and the food enthusiasts are least likely. The rest of the personalities fall somewhere in between, but with the eco-conscious looking a lot like foodies (more on this below). Consistent with all personalities, the most frequently used strategy is to be careful about purchases to reduce at-home food waste from spoilage. The last resort appears to be simply going without.

These frugal to foodie bookends also quantify these behaviors’ higher and lower limits, at least in the current economic context. And there are limits. Frugal individuals aren’t maximally frugal in all behaviors. Only in two of the six behaviors do over half of people with frugal personalities deploy the cost-saving strategy. Similarly, the foodies have some limits in their pursuit of passions. At least 10% of those with a food enthusiast personality are deploying each of these economizing behaviors.

The eco-conscious respondents may behave with similar liberal spending patterns to foodies, but they likely have different motivations. Both generally don’t seem to hold back on their spending. But the foodies are likely paying more for superior taste, while the eco-conscious spend on typically more expensive sustainable food offerings.

Personality in the pocketbook

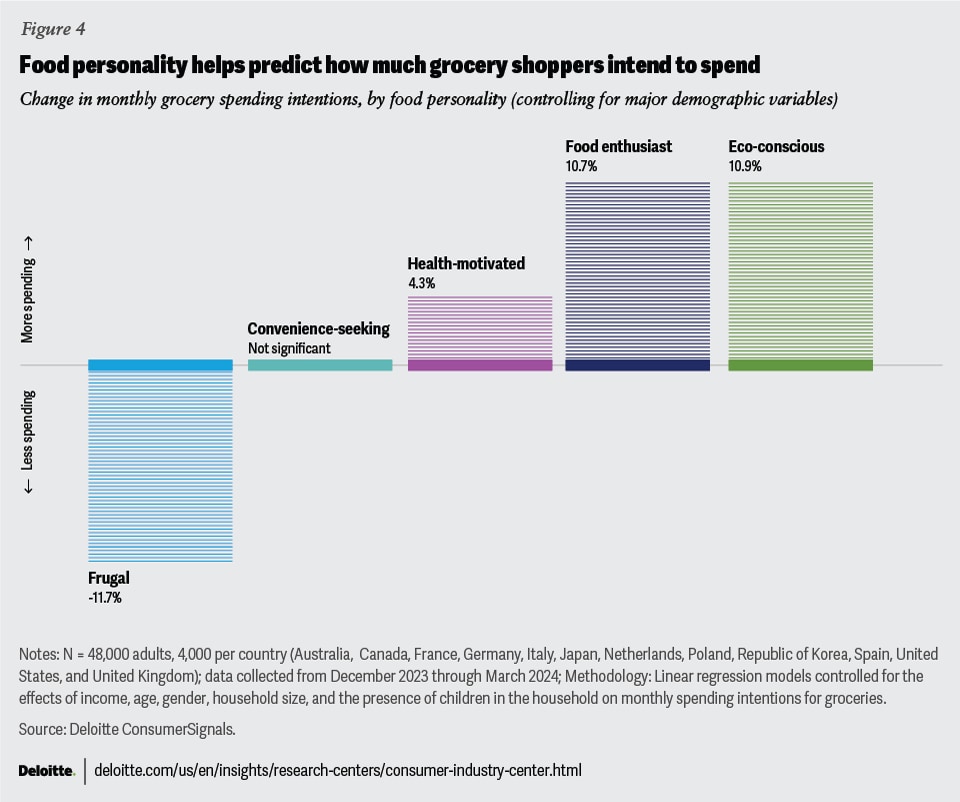

Food personality helps shape what people buy and how they buy it. But at some point, it likely comes down to dollars spent for food producers and grocers alike. Income, household size, and whether you have children at home are immensely predictive of grocery budgets.7 However, the modeling results show that food personality is also predictive of spending, although to an understandably lesser extent.

Food personality was not only statistically significant in predicting grocery spending, but the differences in dollar terms are material for all except the convenience-seeking personality (figure 4). The frugal personality spends the least, while the foodies and eco-conscious spend the most. Convenience food and channels have attributes that simultaneously make them more expensive (for example, pre-chopped vegetables or paying extra for delivery) and less expensive (for example, packaged and frozen meals or fast food). Those competing factors could explain the lack of a strong spending intent influence in either direction for the convenience-seeking personality.

Personalizing with personality

In the years ahead, increasing unit sales volume may be an essential component of the revenue growth strategies pursued by food retailers. To this end, grocery retailers may consider personalizing their marketing, merchandizing, and fulfillment strategies for each food personality as part of their industry’s shift from mass to micro. Consider the following actions:

- Identify: Personalizing on personality starts with discovering each customer’s dominant food identity. Adding a simple multiple-choice question to a loyalty program asking, “How would you best describe your approach to food?” could be a good starting point.

- Target: Knowing what each personality spends and prefers to put in their cart relative to others and what might be competing for spending away from home provides a starting point for more successful engagement.

- Mix: All else held equal, actions that get more food enthusiasts and eco-conscious consumers in the door should translate into bigger baskets. Both personalities skew toward younger consumers, so they may also be poised to become more prominent in the population over time.

- Mode: Consider using a multichannel marketing strategy to engage customers where they are—be that on social media channels for those seeking new recipes and wine pairings, sites where consumers swap economizing tips with others while also looking for coupons for those seeking deals, or third-party shopping apps to engage those seeking the convenience of delivery.

- Message: Craft messages for personality effectiveness. For example, in the survey, both foodies and health-motivated consumers disproportionately buy more premium-quality meat. A grocer might be tempted to market this meat to everyone based on foodie qualities like marbling and specialty aging. But if they know their consumer is health-motivated (and there are many more such consumers), that messaging could be a miss. If they instead emphasized growing conditions, organic certification, lack of antibiotics, or lean protein, it might result in more sales.

- Maintenance: Deloitte’s forthcoming fresh food survey suggests that three in four consumers belong to a grocery loyalty program. But retaining consumers isn’t all that easy.8 Different loyalty and reward system tracks geared toward specific food personalities may also help. Think of one track where store apps offer more health data and nudges, another that centers on calculating the carbon footprint, and another with quick-fix meal highlights and frequent delivery benefits.

- Learn and adapt: Grocers have their own data sets and feedback loops. With the scaffolding of personality in place, they have the potential to discover additional attributes and behavioral relationships connected to personality to further improve their systems on their journey from mass to micro.

The food personality conversation will continue in our annual fresh food study publishing this summer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}