How the pandemic is changing the future of automotive has been saved

How the pandemic is changing the future of automotive Restarting the global automotive engine

8 minute read

13 July 2020

Significant challenges lie ahead for companies trying to rev up the global automotive engine.

It’s the question every backyard mechanic asks themselves just before they turn the key after rebuilding the engine on their favorite old car—will it start? In most cases, getting the engine to turn over is just the beginning. Dialing in a rough idle while making sure it doesn’t stall is equally important to getting the car back on the road. It’s an apt analogy for the moment in time currently facing the global automotive industry.

Learn more

Learn more about connecting for a resilient world

Explore the Deloitte State of the Consumer Tracker

Read more from the automotive collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

Companies up and down the value chain are feeling the pressure of supply and demand disruption, and public concern for health and financial well-being has slowed global economies. Even as some jurisdictions are laying the groundwork to fully reopen, gaping questions remain around the steps automotive companies should take in order to prepare themselves for the realities of a heavily disrupted sector. For example, much more can be done in terms of tapping into technology to create frictionless customer engagement and maximize transparency. Cost-cutting and operational fitness programs that began well before the pandemic remain key, but manufacturers also should protect the critical investments that can yield significant benefits down the road (powertrain electrification, smart factory, etc.). Even tactical priorities, such as worker safety, are paramount to enable a return to vehicle manufacturing.1

Automotive manufacturers are taking a hard look at the resiliency of a globally integrated supply chain brought to its knees by parts production disruptions in China even before the coronavirus spread around the world. Now they have to entice consumers back into the new vehicle market despite strong evidence to suggest that vehicle demand was already headed for a downturn.2 The magnitude of this challenge is clear as industry forecasters are now expecting global new vehicle sales to total just more than 70 million units in 2020, a downgrade of 18.5 million light vehicles from January’s estimates. To put that in context, the drop in global demand this year alone is roughly equivalent to light vehicle sales expectations in the United Kingdom, Japan, and the United States combined.3

Financial pressures set the stage for lasting sector impact

In the face of a possible lengthy recession, many consumers around the world are worried about their financial well-being. According to the Deloitte State of the Consumer Tracker data, 37% of US consumers are delaying large purchases and 21% are concerned about making upcoming payments.4 As many as 30% of those still employed in the United States are fearful they will lose their jobs. While this number is high, it is still below the study’s global average of 41%. It has, however, remained worryingly consistent since mid-April, suggesting that consumer concerns regarding near- and long-term financial well-being have not improved despite recent attempts to reopen the market.

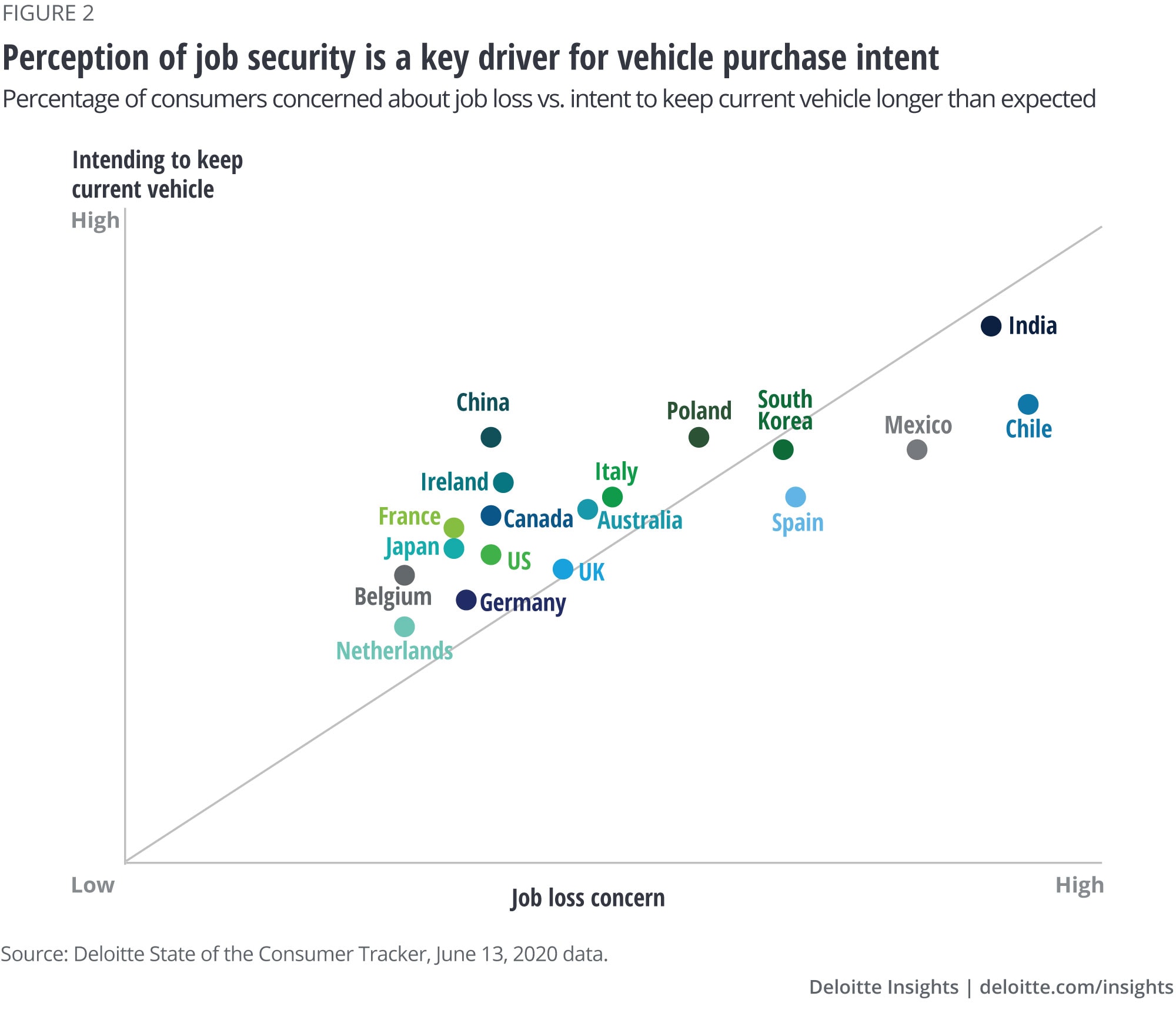

What does this mean for automotive sales? Is the pandemic creating pent-up demand that will propel the automotive industry to a robust recovery? May auto sales figures were encouraging in a few global markets, but our study results reveal that nearly half of US consumers (47%) are planning to keep their current vehicle longer than they originally expected. This level of apprehension is echoed in other large automotive markets around the world, including China (65%), South Korea (63%), and Japan (48%). It also represents an obvious challenge for manufacturers looking to kick-start new vehicle sales and casts a shadow over expectations for the shape of the demand curve moving forward.

Consumers in several countries are also rethinking more near-term expenditures focused on regular vehicle maintenance. Nearly 80% of consumers in India are actively redeploying funds originally slated for vehicle maintenance. So are consumers in Chile (45%), China (43%), and Mexico (41%). However, in the Netherlands and Japan, which exhibit the lowest levels of overall financial anxiety, relatively few people are planning to put off required vehicle maintenance.

A full demand recovery may take years.5 An immediate, V-shaped recovery is looking increasingly far-fetched, as various government assistance initiatives start to dissipate in the coming months, leaving consumers to face the full reality of a diminished financial capacity. Coupled with the sheer caution being applied by companies in their reopening efforts, and the specter of a second wave of COVID-19 hitting later this year, sustained financial strain could result in a consumer retrenchment, truncating economic growth for the foreseeable future.6

How would people want to reengage with the automotive industry?

Assuming demand will eventually return, manufacturers are still faced with the task of meeting an evolving set of expectations when it comes to the way in which consumers will engage with the sector. Living through various levels of lockdown and stay-at-home orders, many consumers have ramped up their use of digital tools to consume an increasingly diverse set of goods and services, from groceries and apparel to entertainment and even medical consultations. A natural expectation might be that this behavior is not only becoming more commonplace for consumers but may also extend to large purchases, such as vehicles. In fact, as economies across the globe began to shut down for an extended period, in a bid to stay relevant, many vehicle retailers installed third-party solutions to facilitate a fully digital vehicle sales process.7

This ride, however, may not be without a few bumps. Our study results suggest that most consumers are not looking to buy their next vehicle online—other than India (71%) and China (45%), interest in a fully online purchase process is limited to one in four consumers or fewer in other markets around the world. The reason for this may be a long-standing acknowledgment that certain aspects of the vehicle sales process, such as the test drive, remain very difficult to digitize. Therefore, it will be very important for original equipment manufacturers (OEMs) and retailers to continue deploying digital tools that address key consumer pain points, such as the overall length of time taken to complete a purchase, and the excessive amount of paperwork involved.8

Are consumers changing the way they view mobility?

The COVID-19 pandemic is also influencing the way many people think about mobility. The need to maintain physical distancing is leading many to a conclusion that the idea of vehicle ownership is valuable to them—79% of consumers in France, 74% in the United States, 69% in the United Kingdom, and 63% in South Korea. Owners can also feel more confident in the level of hygiene in their own vehicles as compared to shared transportation options. In fact, 56% of people surveyed in the United States indicated they are planning to limit their use of public transit over the next three months. Similar sentiment prevails in Italy (63%), Spain (60%), Australia (53%), and Japan (48%), among others. Consumers in many countries are questioning their use of ride-hailing services too. All this is having a significant effect on shared mobility business models and presents a critical challenge for both incumbent players and startups operating in that space going forward.9

However, translating this consumer sentiment into actual vehicle sales may prove challenging as growing affordability concerns may remove people from the market. It may also result in a situation where people who were intending to purchase a new vehicle need to refocus on the preowned market. The average transaction price for a new car in the United States reached US$37,308 in 2019, representing a gap of nearly US$15,000 when compared to the price of an average three-year old vehicle (US$22,459).10 Given this significant difference, used vehicles may be assuming the role of the entry-level car, giving cash-strapped consumers an interesting option to consider. Moreover, consumers intent on acquiring a new vehicle may either downgrade to a more affordable vehicle segment and/or reduce the number of features included on the vehicle. In any case, financial institutions including the captive lenders will likely play a pivotal role in determining whether consumers will be able to maintain access to credit and stay in the market.

Better prepared than last time, but still vulnerable

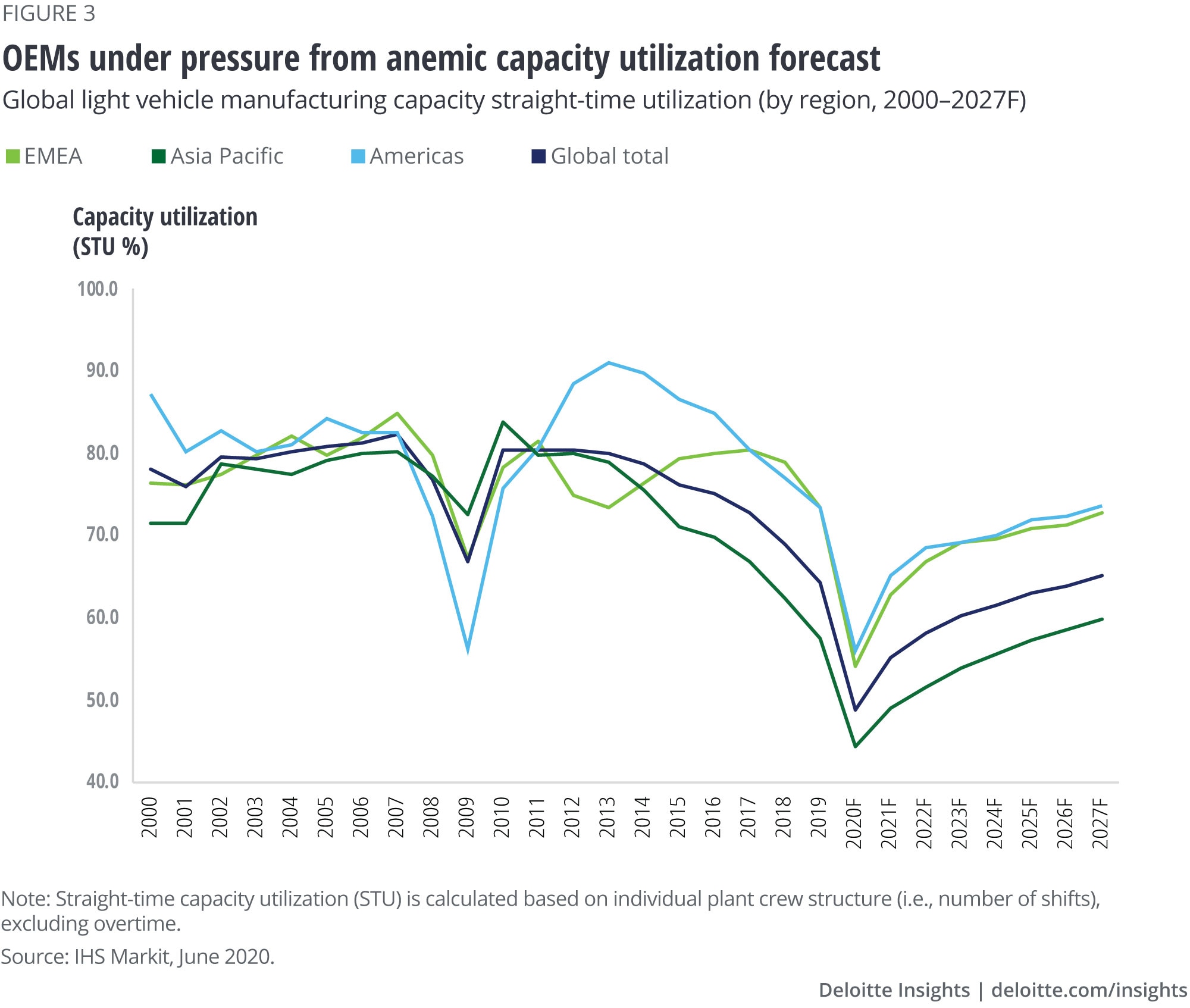

Some automotive companies entered the current crisis in a much better financial position11 as compared to the recession a decade ago, but debilitating liquidity issues loom ever larger given the current economic uncertainty. Some fast-acting companies were successful in drawing down credit lines and making hard decisions regarding operational cost structures to shore up their balance sheets. However, light vehicle manufacturing capacity utilization in the Americas alone is expected to remain below 75% through 2027,12 placing additional, longer-term profitability pressure on OEMs. It may also lead to an increasing number of distressed assets across the industry, resulting in a significant number of mergers and acquisitions as financial and strategic buyers look for opportunities to consolidate vulnerable parts of the value chain.

The stress on the ecosystem may also mean an upturn in corporate bankruptcies, as companies heading into the pandemic in a relatively weaker financial state may not have the cash reserves or the ability to refinance that they need to weather this storm. The knock-on effect could be devastating, as a relatively small disruption in the supplier base could have a disproportionately damaging downstream effect on a surprisingly brittle global value chain. It is also highly unlikely that many global governments will have the ability to step in and offer targeted bailouts considering the massive amount of stimulus pouring into the global economy to prop up a wide array of sectors under massive financial strain.

Five things manufacturers should consider to dial-in their recovery effort

- Increase collaboration with dealer networks to accelerate the adoption of digital tools designed to create frictionless engagement and meet customers where they want to do business. Even though the jury may still be out as to whether consumers will migrate en masse to buying cars fully online, there are still many areas where integrated digital tools can have a transformational impact on the vehicle purchase process and overall brand engagement. At the same time, manufacturers can accelerate the deployment of digital tools back through the supply chain to maximize transparency and to detect potentially crippling issues early on. Establishing digital supply networks and deploying artificial intelligence can enable smarter planning decisions and improve overall agility through a deeper and broader understanding of the system as a whole.13

- Maintain the manufacturing discipline gained through the last upcycle, focusing on producing vehicles that consumers actually want to buy. In fact, companies that are trying to restart assembly operations under a prepandemic strategy may need to be much more agile in order to respond to shifts in the vehicle mix caused by a growing consumer affordability issue.

- Deploy technology transformation tools to identify and prioritize further cost-cutting opportunities while protecting critical investments that can yield significant forward benefits (powertrain electrification, smart factory, etc.). Cost cutting in a downturn is certainly not revolutionary, but knowing which investments in innovation to protect given longer-term macro trends can be a critical success factor for automotive companies moving forward. For example, driving forward with smart factory implementation strategies could yield significant competitive advantages related to throughput, quality, safety, and revenue growth.14

- Isolate areas of the business that represent a cash drain and make the hard decisions required to rehabilitate, sunset, or divest underperforming assets. Continuing to prop up unprofitable assets will be increasingly difficult moving forward, particularly manufacturing operations that struggle to meet a minimum capacity-utilization threshold.

- Ramp up the exploration of strategic partnerships to maintain a focus on innovation while sharing investments and minimizing risk. Traditional notions of competitive exclusivity between OEMs may be giving way to the realities of emerging market conditions. Finding ways to collaborate on innovation may become a strategic imperative for automotive companies.

The pandemic started just as the global automotive industry was headed into a cyclical slowdown with a potential for a more permanent, structural downshifting in demand. It is also playing out against a backdrop of global automakers already under intense pressure to maintain massive research and development spending with no guarantee of a return on investment, and a critical need to develop new business models. The full impact of the pandemic will likely remain unclear for at least several more months. What is becoming very clear, however, is the need for industry stakeholders—including manufacturers, suppliers, retailers, financial institutions, and governments—to come together in a focused dialogue to understand exactly what actions are needed in order to tackle these incredibly complex issues and get the global automotive engine running smoothly again.

Please check out our interactive dashboard to explore additional data by country and age.

Customer & Marketing Offering portfolio

The US Customer & Marketing Portfolio integrates our most differentiated, globally recognized customer and marketing businesses. It focuses on owning the commercial agenda through growth strategy, enhanced user experiences, and engagement through the entire customer lifecycle. From our core strengths in creative design, to strategy, platforms and solutions, as well as our continued growth through acquisitions, we are uniquely positioned to bring fully integrated solutions to our clients.

Learn more

Get in touch

- Joe Vitale

- Principal, Global Automotive sector leader

- Deloitte Consulting LLP

- jvitale@deloitte.com

- +1 313 324 1120

Explore the automotive industry

-

The futures of mobility after COVID-19 Article4 years ago

The futures of mobility after COVID-19 Article4 years ago -

Cyber everywhere: Building cybersecurity, one vehicle at a time Article5 years ago

Cyber everywhere: Building cybersecurity, one vehicle at a time Article5 years ago -

Driving differentiated value with additive manufacturing Article5 years ago

Driving differentiated value with additive manufacturing Article5 years ago -

-

Automotive Collection

Automotive Collection