A fresh (food) take on grocery convenience

Call it ‘fresh convenience.’ Combining two traditional strengths may help grocery retailers compete in new ways.

Daniel Edsall

Adam Almond

Brian Baker

Justin Cook

Siddharth Mishra

Grocers are navigating a new wave of change. They spent the past five years managing radical disruption in the economy and their industry—spanning COVID-19 shutdowns, digital acceleration, supply chain challenges, and inflation spikes. Now, they may need to pivot again as they adapt to a world that looks like a return to normal in some ways and like science fiction in others. And both views seem to reflect stressors for the traditional grocery business.

In the return-to-normal category, food-away-from-home resumed its long-running trend of eating into grocers’ share of wallet.1 Additionally, with inflation falling and consumers resistant to further price increases, grocers may have to rely on unit volume sales growth to boost revenues—a need both familiar and urgent.2 Yet, they may find themselves in a pinch. Volume growth should also be profitable to power the earnings that keep investors happy and the flywheel of reinvestment turning. So, grocers should also avoid overreliance on expensive discounts and promotions in pursuit of boosting sales.

Other challenges may seem more futuristic. Consumers today often expect grocers to be omnipresent and available in-store as well as across channels such as the web, apps, and social media. Some consumers may be less willing to shop from stores’ physical shelves, requiring grocers to take on more pick and pack labor cost. And some consumers would like their groceries delivered to their door and seem content to use a third-party service or even supplied by that third-party's own warehouse (a.k.a. “ghost store”) if necessary. Investing to accommodate and provide last-mile delivery in-house stresses the profitability of the grocery business model. Meanwhile, the race against competitors to incorporate artificial intelligence could disrupt all aspects of the grocery business, from logistics to customer service.

Learn more

And even as grocers fend off internet and AI-enabled competitors, consumers may elect to buy fresh food from dollar store formats—something that was hard to imagine at scale just a few years ago, reminiscent of consumers’ surprise embrace of buying groceries from big box stores decades prior.

Yet certain fundamentals remain constant through this industry swirl. One is grocers’ strength in the realm of fresh food—fresh fruit, vegetables, meat, and seafood which both consumers and retailers continue to value highly. Another is consumers’ desire for convenience in multiple forms. Convenience is one of the few purchase drivers that has sustained its high value under inflation pressures, according to Deloitte research over the last six years.

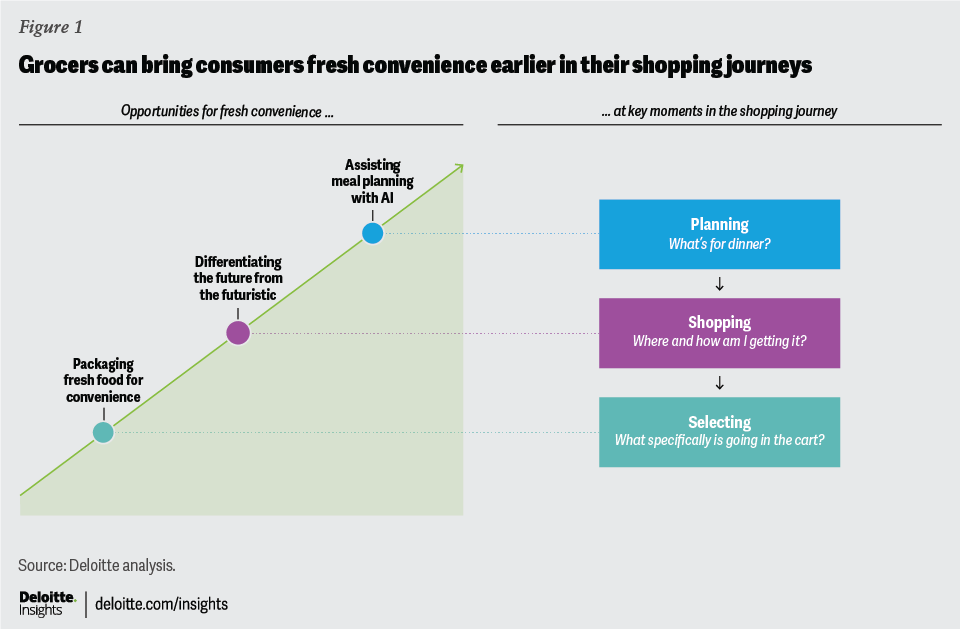

Our research findings indicate that the nexus of these two perennials—fresh food and convenience—could serve as a foothold for progress (see “Methodology” for details about the survey). Both have long played a major role in consumers’ experience with grocery. Today, new frontiers are developing at distinct moments in customers’ grocery journey, giving grocers opportunities to marry fresh food with convenience profitably. Here, we are calling it “fresh convenience.” The earlier in the journey grocers can help consumers, the greater the opportunity to create value (figure 1).

Methodology

This research marks Deloitte’s sixth annual assessment of the state of fresh food. This year, Deloitte surveyed 100 US-based grocery retail executives from organizations with at least US$1 billion in annual revenue and 2,000 US consumers, using an approach designed to approximate US census demographics.

It’s not expected to be easy. On the way, grocers may encounter sustainability issues, significant investments, and consumer concerns about using generative AI. And winning on fresh convenience isn’t the only lever to pull. Strong “future of consumer” forces are affecting the markets, models, and mechanics of the industry that should also be addressed.3 However, those grocers that can successfully bring fresh convenience to consumers at key moments in their journey could stand to capture the profitable volume growth and share of stomach they seek.

Customers want food that is both fresh and convenient

It may come as no surprise that fresh food ranks high in importance for both consumers and grocery stores. Consumers love it: Nine in 10 respondents said fresh food makes them happy. They equate fresh food with nutrition and want to buy healthy food (even if they don’t always do so).4 Fresh food is critical from the grocer’s perspective as well. This year, more than half (52%) of executives surveyed report that fresh food will be their most strategically important department over the next one to three years, with produce, deli, and meat leading the charge.

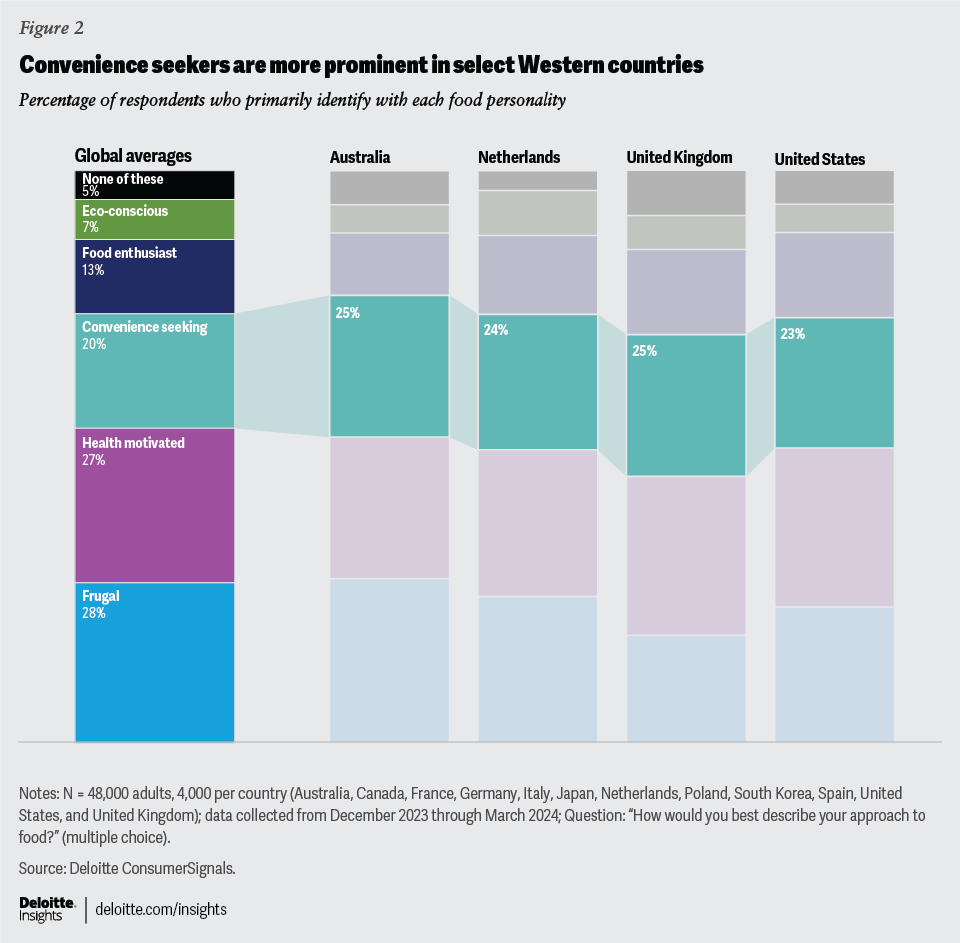

While consumers like the idea of fresh food, they also crave convenience in multiple forms throughout their shopping and buying experiences. Convenience is not only a resilient driver of food purchases, but it also seems to be growing in importance, with more than half of surveyed customers (52%) saying they value convenience now more than they did in the past. Millennials (57%) and Gen Zs (61%), in particular, are growing keener on it, suggesting the trend may be here to stay.5 For some customers, convenience is their North Star—23% of surveyed US consumers are primarily convenience seekers when it comes to their overall approach to food (see “The five food personalities”).

The five food personalities

Food marketing will become hyper-personalized in the coming years, say nearly 9 in 10 grocery executives (88%) surveyed. For that future to come to pass, grocery companies may need to take intermediate steps to more approximately understand individuals’ priorities around food.

In a global survey spanning 12 countries and including more than 48,000 consumer responses, Deloitte found that 95% of people recognize they have a specific approach to food—identifying primarily with one of five distinct food personalities.6 Convenience seeking is a top three approach to food in all countries, but it plays an outsized role with consumers in Australia, the Netherlands, the United Kingdom, and the United States (figure 2).

Using regression analysis and controlling for major structural factors like age, income, and family size, models show these personality types independently help to predict what consumers might put in their grocery carts and how much they budget to spend. This can help make them a jumping-off point for grocers as they work to deliver more precisely tailored communications and assistance.

Grocers also understand the value of convenience. When asked what they would most like their store to be known for to maximize its competitive advantage, surveyed grocers ranked convenience second, behind only quality and ahead of low prices and value.

Grocery executives’ answers to other questions show them understanding and prioritizing convenience. More than three-quarters of surveyed executives “agree” or “strongly agree” that:

- They are making significant investments to increase convenience (85%).

- Successfully competing on convenience is essential to increasing unit sales volume (84%).

- Convenience is a major purchase driver for consumers (83%).

- Consumers value convenience now more than they did in the past (81%).

- Competing on convenience is a major part of their overall strategy (77%).

As grocers plan their futures, they can consider how they can use their strengths in fresh food and convenience to capture the new frontier’s high ground at key points in consumers’ grocery journeys.

Adding fresh convenience at key moments

Once customers are already in a grocery store (physical or virtual), they can find convenience in the products they select. These more convenient products can be easier to prepare, eat, dispose of, or even get through the self-checkout without trying to spell “jalapeno” so that the computer recognizes their purchase. But before that, consumers may choose the most convenient channel for their circumstances in which to shop. It could be shopping at a traditional grocery store, using a third-party internet app, or going to a quick-service restaurant. And, going back to the beginning, life could be a lot more convenient if consumers could more easily figure out what to have for dinner in the first place.

Ideally, all this convenience should come to consumers without compromising away from the healthy, fresh food they wish to eat. And, moving earlier through key moments in the consumer journey, backward from selecting to shopping to planning, there may be greater opportunity for grocers to create value.

Key moment: Selecting

Grocery executives surveyed estimate that 50% of their consumers would pay a premium for more convenient fresh food and peg the average price premium willing to be paid above traditional fresh food alternatives at 41% more. That projection may be overly optimistic, considering the surveyed consumers say they would pay an extra 17% on average. Still, even a 17% premium could add meaningfully to revenues and profits and help offset consumer price sensitivity elsewhere.

The idea of making fresh food more convenient isn’t new. Grocers have tried to make fresh food more convenient across various dimensions—making it easier to prepare, consume, and clean up—by providing precut produce, grab-and-go meals, in-store dining, and a variety of other offerings.

These offerings have their place. Yet, grocers may not fully be meeting the need. Although consumers seem to love the idea of fresh food, convenience can still trump the fresh food options provided today. More than two-thirds of consumers surveyed say that, on busy days, they buy more convenient food items even if they’re not healthy (that is, not fresh food), the fourth straight year with that survey result.

Consider: Packaging with care can help make fresh food a convenient choice

Our research suggests that focusing on smartly packaging fresh food may be more effective. Half (50%) of consumers say packaged fresh food is an attractive way to provide greater convenience, making this the No. 1 response at the selecting phase of their journeys. Why? Consumers surveyed say:

- Packaging is a way to prevent contamination (70%).

- They value packaging with labels because labels help them understand their fresh food purchase (61%).

- Packaging helps fresh food stay fresh longer than unpackaged fresh food (57%).

Packaging fresh food also has operational benefits for grocers. For instance, packaging can help grocers better track and trace fresh foods, manage inventory with relative ease, offer higher consistency for online shopping, lower labor costs, and reduce shrinkage.

Yet, increasing fresh food packaging could collide with another imperative: sustainability. On its face, greater use of packaging on food items, some of which previously went without packaging, is problematic. In practice, however, the relationship between packaging and sustainability is complex and full of tradeoffs.

Over one-third of food is wasted, along with all the resources that went into producing and bringing it to market. Additionally, wasted food makes up 24% of the composition of landfills. It decomposes there, producing methane, a greenhouse gas 28 times as potent as carbon dioxide. And fresh fruits and vegetables rank at the top of the most wasted types of food.7

So, while the additional material used is a tradeoff, packaging fresh food can help reduce food waste by extending fresh food’s shelf life and reducing spoilage.8 The packaging label can provide a place for educating consumers about waste. Then there are the potential health benefits of consumers buying and eating more conveniently packaged fresh food and the potential of more of it feeding food-insecure consumers, instead of ending up in landfills.9 And for consumers, there is a cost component. The No. 1 strategy for consumers trying to save money on groceries is being cautious about the food they buy to avoid at-home food waste.10

Whether for convenience, sustainability, health, or cost—consumers want to cut food waste more than many grocery executives may appreciate: Nearly three-quarters (73%) of consumers say it’s important to them, but less than half (48%) of grocery executives think consumers make it a priority.

Grocers that use packaging on fresh food should consider communicating the benefits while taking steps to mitigate packaging’s drawbacks, including following models of European grocers that make use of packaged fresh food. They can pursue more sustainable packaging solutions by developing relationships with packaging providers and food companies that help them capitalize on ongoing breakthroughs in materials sciences, technology, and automation. They can review existing data and conduct their own experiments to identify where packaging makes a difference in food waste and overall carbon impact.11 They can advocate for and invest in reclamation and recycling programs, and there may be an opportunity to remove “best buy” dates where it isn’t proven to improve food safety. This approach could align with the desires of consumers, about half (49%) of whom want packaging to be more responsible or sustainable. These advances in packaging materials and technology ultimately may be an interim step until technologies such as machine vision and AI are ready to monitor food freshness, ripeness, origin, and inventories.

Key moment: Shopping

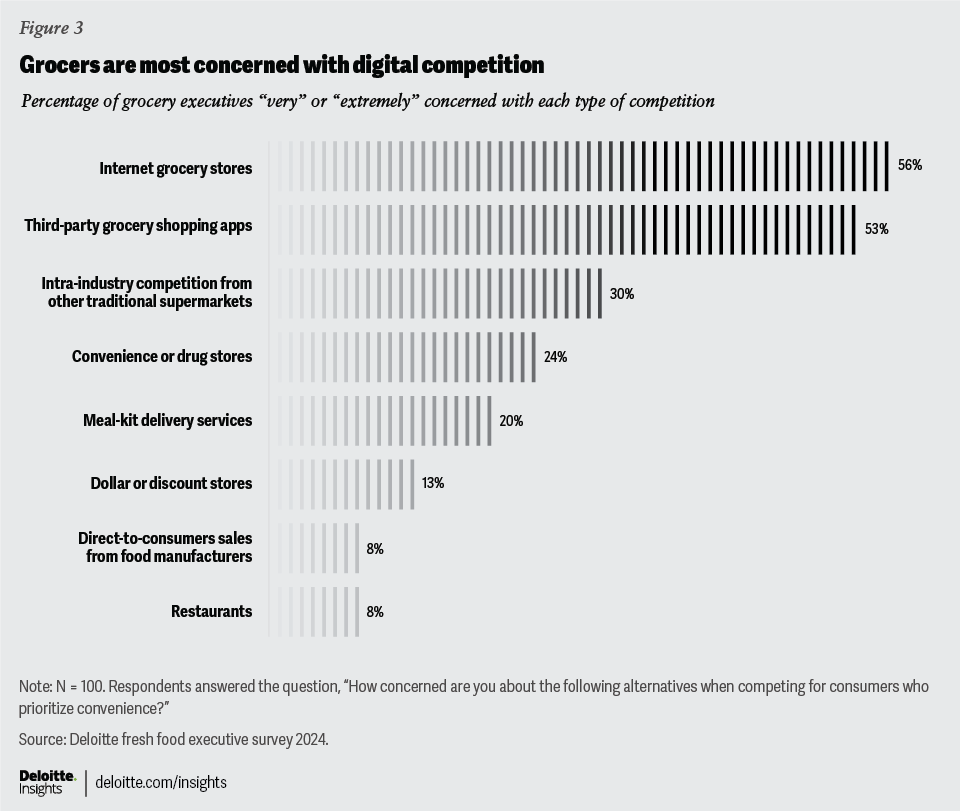

Convenience for shopping has traditionally played out like real estate—location, location, location. The laws of physics are not suspended. Today, how close a store is to a consumer’s home is often still a factor in their choice of grocer.12 But it isn’t everything. The technological and social disruptions of the last several years have likely accelerated the proliferation of new business models and consumer options. Internet-only retailers, third-party delivery apps, dollar stores, meal-kit providers, and direct-to-consumer sales by food manufacturers have joined grocers’ traditional convenience store and restaurant competitors to vie for convenience-seeker spending.

While many competitors may struggle to match grocers on fresh food, some new entrants seem well positioned to cater to customers’ growing desire for convenience. Internet grocery stores and third-party shopping apps especially seem to be keeping grocery store executives up at night (figure 3).

Consider: Differentiating the future from the futuristic

It may now be a business school cliché, but it isn’t always followed. In The Art of War, Sun Tzŭ famously advised that, to succeed in battle, you must “know the enemy.”13 In the case of grocery retail, executives may be looking past their true competition by focusing on the more futuristic and digitally enabled competitors.

For one, consumers seem to view their options differently than grocery executives do. When we surveyed consumers on where they turn for food when they want convenience, 47% said traditional grocery stores, far ahead of third-party shopping apps (9%), meal-kit delivery services (3%), internet grocers (3%), and food producers’ direct-sales websites (2%). Additionally, many of these newer business models seem to be struggling to figure out how to generate sustainable profits and scale their business models, calling into question whether they will genuinely prove to be existential threats.14

Other potential threats may be flying under the radar. For instance, restaurants may be a more formidable convenience rival than executives appreciate. One-quarter of consumers surveyed say they turn to restaurants when they need convenient food. A sizable minority say that fast food is often cheaper than groceries for a meal, and that perception is especially prevalent among the younger generations surveyed. Yet, while grocery executives appear wary of restaurants, they do not seem especially alarmed: Only 8% say they are “very” or “extremely” concerned.

Grocery executives appear only slightly more worried about dollar stores, with 13% showing strong concern about competing with them for convenience-seeking customers. This lack of urgency may reflect more limited fresh selection at dollar stores or perhaps that their consumers have relatively low spending per transaction—around US$20 at dollar store formats, on average,15 compared to more than double that at the largest grocery retailers.16

However, what dollar stores lack in spending per transaction may be made up with volume. As of year-end 2023, the top two dollar stores had almost twice as many locations as the top 10 US grocery stores combined.17 Grocery executives surveyed seem dubious about dollar stores’ ability to replicate their fresh food supply chains, with only 1 in 5 saying they think dollar store efforts will be successful. But dollar stores are making a run at it, doubling their investment in providing fresh food.18

Sun Tzŭ also claimed that, in battle, in addition to your enemy, you must “know yourself.”19 A key to beating competitors for convenience-motivated consumers—and doing so profitably—may be leaning into grocery’s traditional strengths. Fresh food is a strength, and as noted above, traditional grocery is still the top consumer choice for convenience among respondents. What consumers say they really want is more convenience in stores. Just-walk-out-style frictionless or not, customers’ No. 1 in-store priority for convenience is speedier checkouts, cited by almost three-quarters (73%) of respondents and agreed to by more than 8 in 10 executives (86%). Most consumers also seek more convenient store layouts (59%) and easier returns (51%). They also want services like having associates bag groceries, with 41% of them saying it is “attractive” or “very attractive.”

Grocers should have options for consumers who want to shop digitally and have purchases delivered. However, such efforts could contribute to business success only if they are undertaken with measured, prudent investments. They should also be executed to both provide and receive more value from digitally engaged consumers, steering them to more profitable fulfillment models and expanded service offerings.20

Key moment: Planning

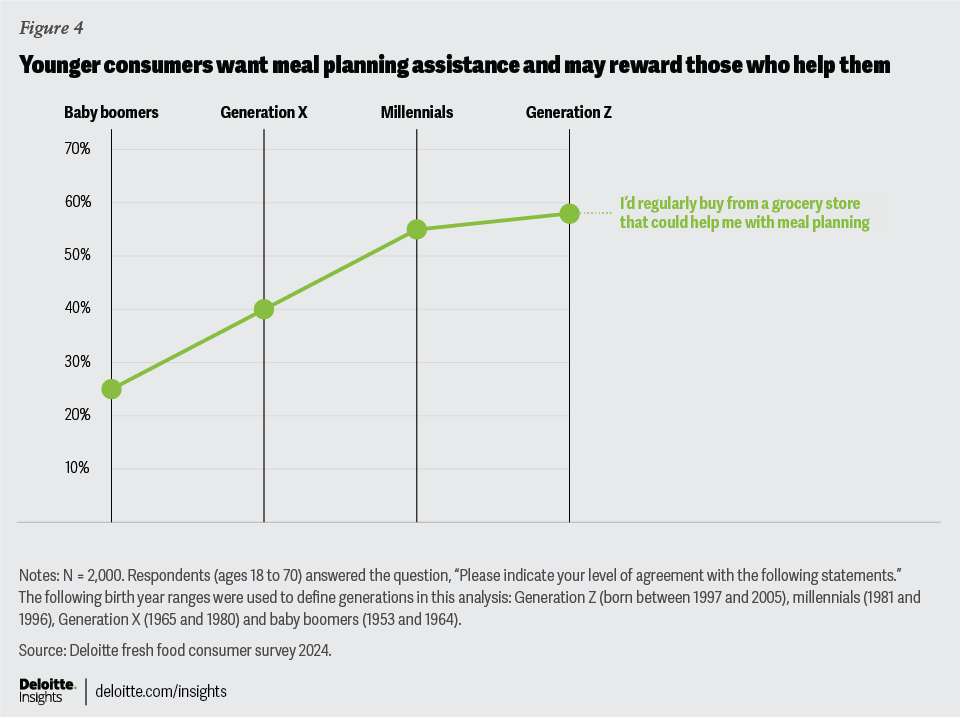

Consumers are asking for help deciding on dinner. More than half (53%) surveyed say that figuring out what’s for dinner is one of their major pain points. Their need echoes a meme that went viral in recent years expressing surprise that the hardest part of adulting was the mundane drudgery of figuring out what to cook for dinner night after endless night.

Younger consumers (66% of Gen Zs and 60% of millennials) were especially likely to call figuring out dinner a primary pain point. Households with children, across all generations, also struggle to plan their families’ evening meals (62%).

Grocers have long offered circulars, recipes, and in-store demonstrations and layouts that emphasize special-occasion meal ideas, such as barbequing kits around summer holidays. But with today’s proliferation of other options, grocers likely need to capture consumers earlier in the planning stage or risk losing them. Think about it: The later in the evening consumers go without deciding what to have for dinner, the more likely they will default to quick-service restaurants or other cheap and convenient eats rather than shopping at a grocery store for ingredients. And that comes with a greater chance of missing out on the healthiest fresh food.21

Grocers could look to get ahead of this pattern if they can figure out how to offer more meaningful meal planning help further upstream. Many consumers surveyed say they want the help and would regularly buy from the grocers that help them (figure 4). And over half—including more than 6 in 10 Gen Zs—say they would buy a store’s private label goods if they were part of an easy meal plan.

Consider: Using generative AI to help consumers plan meals

Grocery retailers could consider deploying gen AI planning assistants that have the potential to help consumers solve their “what’s for dinner” problem. As they develop these assistants, grocery professionals may want to revisit their childhoods and emulate the grown-up caregivers who devoted care and attention to providing the healthy food they liked. (For more on this topic, see “Gen AI goes grocery shopping.”)

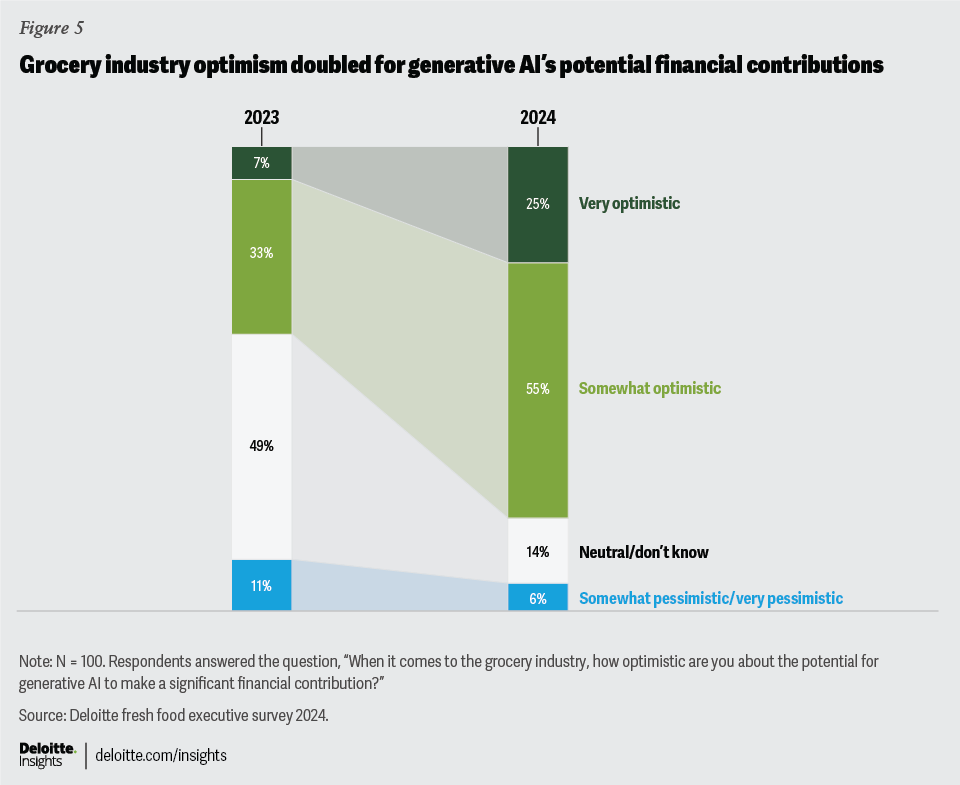

The industry appears to recognize the potential opportunity AI presents. Grocery executives’ appreciation of generative AI’s potential doubled from 2023 to 2024, with 8 in 10 now saying they are “optimistic” or “very optimistic” about its potential to create a financial impact in the industry (figure 5).

And they think the time is now. About two-thirds (65%) of executives say their companies are increasing investments in gen AI, while nearly three-quarters (73%) say their companies will have a major application in place within the next six months. When asked what the first killer app would be, executives surveyed ranked consumer assistant first, ahead of back office functions like inventory management and supply chain management.

Although gen AI presents unprecedented potential to understand and cater to individual consumers, it also introduces a risk that misuse of the technology could alienate or even anger them. For these applications to fulfill their promise, consumers often need to share their preferences, aversions, allergies and other health-related dietary needs, religious dietary restrictions, and other personal information. Yet less than a third (27%) of consumers agree they want to use a gen-AI-powered assistant; more than half (53%) say they don’t want to receive AI-generated messages from their grocery stores; and just one-third say they trust that their primary grocer would use gen AI responsibly—a drop of five percentage points from 2023. Grocers should plan and execute any gen AI initiatives with great care to help grow consumer trust (see “Grocers score high on trust, low on transparency”).

Grocers score high on trust, low on transparency

Grocery retailers have typically been rated by surveyed consumers as highest on trust relative to all other retail store types,22 and 2024 was no exception: Overall, trust in grocers improved slightly in 2024 from already-high levels (Deloitte TrustID score rose from 40 to 42) as consumers increased their ratings of grocery companies’ capability, humanity, and reliability.23

Not all the news was positive for grocers, however. Their ratings on transparency, already their weakest dimension of trust in 2023, fell in 2024. One consequence: Only 30% of consumers surveyed are willing to share their medical or health-related data with their grocer (a drop of eight percentage points from the prior year). A lack of satisfaction with grocery stores’ transparency also may help explain customers’ concerns about grocers’ use of AI. Addressing those concerns could be key as grocery companies look to roll out technology-enabled personal shopping assistants.

Thoughtful information-sharing can help grocery executives improve customers’ faith in their companies’ transparency. Based on the survey results, they might consider improving disclosures around:

- The ways they make money from retail interactions (such as with retail media business models)

- How and why they use consumers’ data

- Sustainability and community impact

Grocers should be transparent about their use of gen AI as it pertains to consumer data. However, they may want to consider using it to drive recommendations rather than making the technology itself a selling point. Grocers may wish to engage customers with friendly, easy-to-use apps, smart speakers, and other interfaces. They can draw on AI to enhance the things customers already do, and then look to expand use cases for it over time as customers become comfortable with an AI-powered experience.

The road to profitable growth likely goes through new frontiers

Overall, grocer executives surveyed feel good about their prospects. Seven in 10 are optimistic about the grocery industry in the year ahead, while 8 in 10 are optimistic about their company’s strategy (80%), performance (80%), and the underlying demand for their offerings (82%).

However, fewer have faith in the strength of consumers’ finances (31%). They seem to understand that prices can’t keep going up so significantly, and 89% agree that increasing unit volume sold will be essential to meeting their business performance goals. They may need to find ways to generate significant, profitable volume growth to produce the performance that allows them to reinvest in their businesses and satisfy investors.

Our research suggests that new frontiers at key moments of the customer journey offer opportunities to combine fresh food and convenience to help grocers meet their goals. Consider:

- Selecting: Deploy packaging smartly to make fresh food a convenient choice and seek to provide grocers with more consistent execution and improved operations.

- Shopping: Play to their traditional strengths to beat competitive alternatives, including those currently flying below the radar.

- Planning: Help consumers plan meals in new ways enabled by generative AI, and potentially benefit from additional sales and loyalty consumers say they would reward in turn.

Navigating these frontiers will likely push grocers to make the most of their legacy advantages, including their customer relationships and strengths in fresh food, while developing new, cutting-edge practices. With these efforts, grocers and customers can have their fresh fruits, vegetables, meat, and seafood—and eat them, too.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}