Consumer electronics sales: During the pandemic, computer and TV sets outgrew smartphones has been saved

Thanks to Brooke Auxier, Gautham Dutt, and Shubham Oza for their support.

Cover image: Jaime Austin

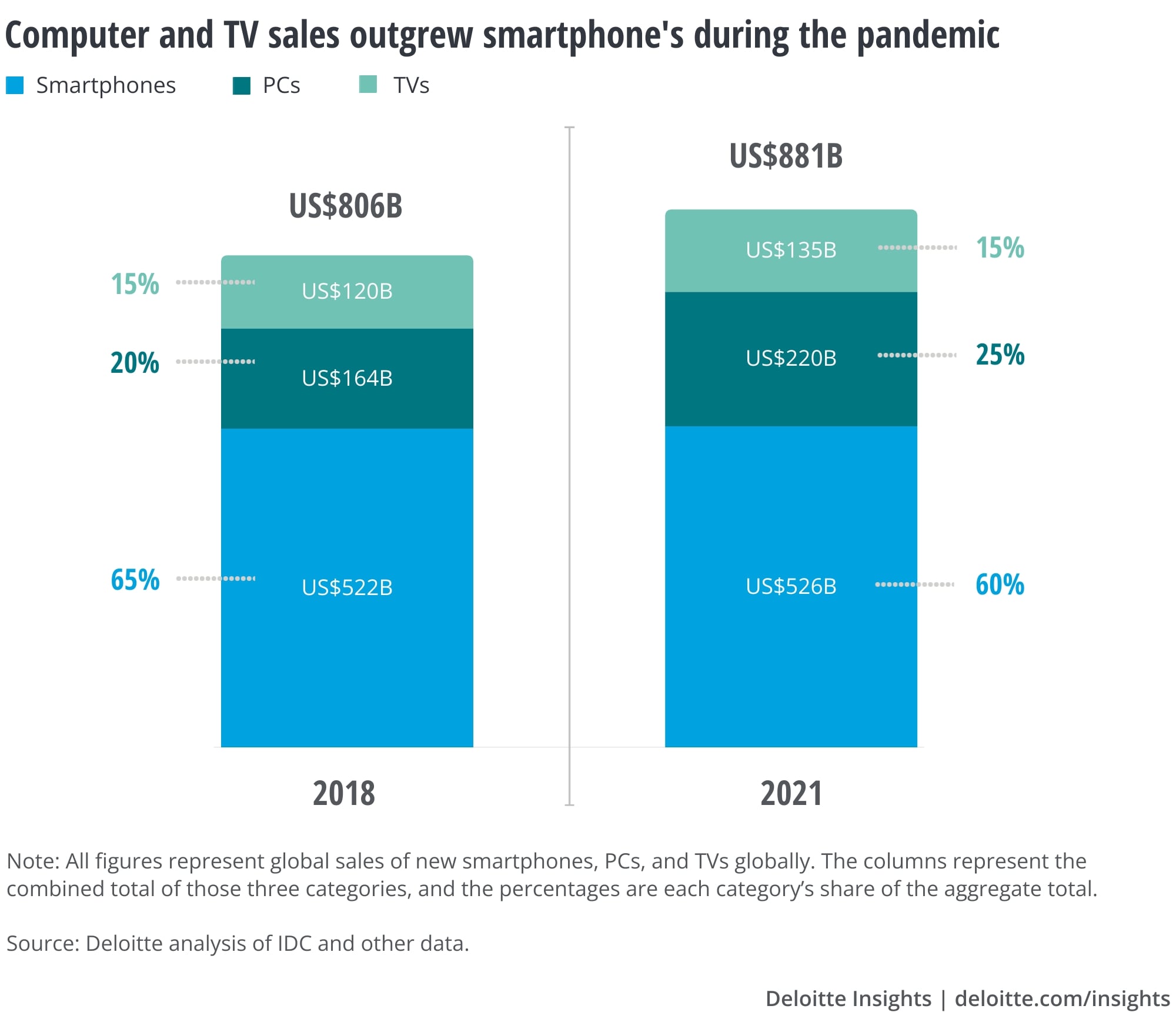

Across the consumer electronics sales categories, computers (+34%) and TV sets (+12%) have grown much faster than smartphones (+1%) in the past three years globally, likely due to COVID-19 restrictions and more time spent working and learning from home. As a result, smartphones’ share of combined sales dollars for the three device categories has fallen from 65% to 60% (see figure).

And it doesn’t look like smartphones are about to regain that share. Growth rates for units of smartphones,1 computers,2 and TV sets3 are each forecast to be 3–4% for 2022. Although PC and TV set average prices are likely to be flat, smartphone average selling prices are predicted to drop by more than 15% during the year, resulting in a likely net decline in dollar value.

These three categories were a combined US$880 billion in 2021.4 For context, the next largest consumer electronics sales category is tablet computers (both slate and detachable), at about US$60 billion in 2020.5

It’s more complicated than just sales of new devices, of course.

In 2018, a mobile-only world looked plausible—after all, smartphone grew tenfold from 2008 to 2018, while PC sales fell every year between 2012 and 2018.10 However, with smartphone sales remaining flat since 2018,11 the future looks more like a three-ring circus, with consumers continuing to support smartphones, computers, and TV sets with their wallets and their attention.

{kind=link}