Wireless telecom consolidation speeds up … where regulators allow

In many markets, smaller wireless telecoms see slow growth, low profits, and have debt to repay. M&A, specifically combining assets or even entire consumer-facing companies, may help where it gets approved by regulators.

Deloitte predicts that more in-market telecom mergers will get approved in 2025 and beyond, at first led by the European Union.1 In many regions and countries, wireless telecom markets are fragmented, and some players are subscale. Historically, regulators have focused on maximizing competition by encouraging as many consumer-facing players as possible, which helps keep consumer prices lower. Increasingly, however, those who advise regulators are suggesting that future network growth, features, security, and resilience might be better maintained by permitting consolidation within markets.

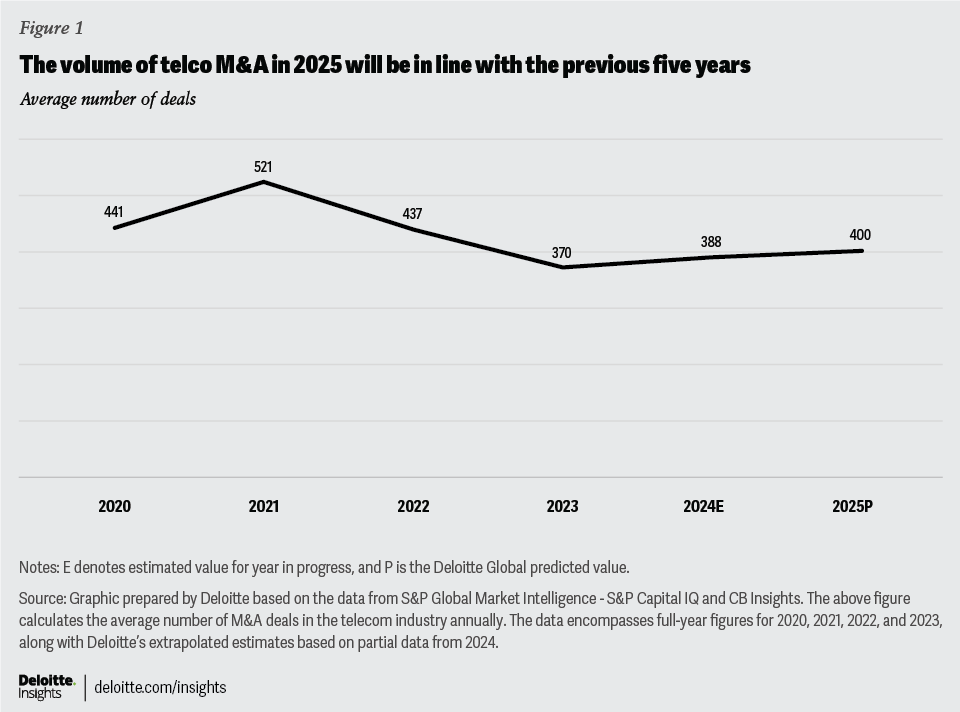

Deloitte predicts that there will be about 400 telecom mergers and acquisition deals in 2025, more or less in line with the deal volume over the last five years (figure 1).2 That may not be that interesting—what is interesting is the kind of M&A deals we predict we’ll see more of: actual operator consolidation.

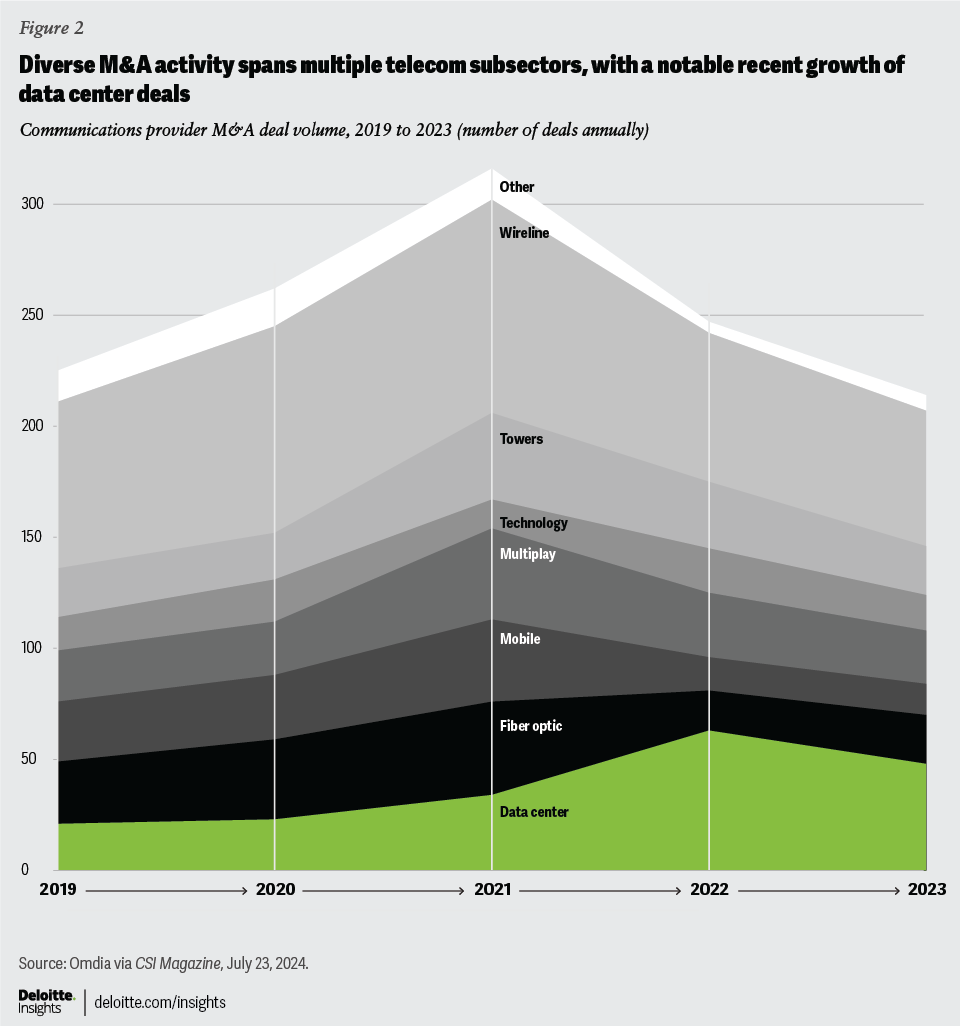

There are many kinds of telecom M&A deals, but at a high level, no single kind of M&A dominates (figure 2).3 There are both wireless and wireline deals, and as a percentage, the various deal types are fairly consistent over time, although the number of data center deals has picked up recently, likely driven by activity around AI data centers.4

Some forms of consolidation or carve-outs have been underway for years and are likely nearing the end of their growth phase: As an example, 97% of all cellphone towers in the United States and Mexico in 2023 were run by standalone tower companies rather than the telcos (up from 65% in 2016), while in Europe, tower companies nearly doubled their share in 2023 to 70%, up from 36% in 2016.5

Equally, for years, there has been consolidation and M&A activity of wireline networks (copper, fiber optic, and coaxial), and back-office software systems such as billing and operations, field service fleets, and data centers.6 Increasingly, there are wireless consolidations of various kinds.

As examples of wireless network consolidation, in Canada, two major wireless providers have shared the radio access network (RAN) since 2009.7 In Malaysia, where there used to be three separate and distinct wireless networks, the government decided to have a single national 5G network in 2021, although they have now decided to have a second network.8 In Brunei, there are three mobile companies offering services to consumers and enterprises, but all three of them use the same radio network provided by Unified National Networks Sdn Bhd.9 In 2024, two Australian operators agreed to share the 4G and 5G RANs.10

However, in these cases and others, the number of “retailcos” (companies that offer communications services to consumers and enterprises) have stayed more or less constant: For buyers of telecom services, there are still three or more (sometimes many more) companies competing with each other.11

What is relatively new and is the core of our prediction: Governments and regulators globally have been allowing mergers. Since 2020, there have been 13 telecom mergers or joint ventures that have decreased the number of customer-facing players, which have been approved or are in the process of approval by governments and regulators:

- The Americas. Six mergers (three in the United States and one each in Canada, Chile, and Colombia)12

- Asia Pacific. Five mergers (Indonesia, Malaysia, Thailand, Taiwan, and Australia)13

- Europe. Two mergers (the Netherlands and Spain)14

Observers are awaiting a final decision from the United Kingdom’s regulator on the proposed merger of Vodafone UK with Three UK.15 It may be worth noting that proposed mergers in Italy and Denmark were denied in recent years.16

Further, former Italian PM Enrico Letta submitted a report to the EU in April of 2024, explicitly calling for telecom consolidation.17 In part, he based his recommendations on an EU white paper that discussed the challenges telecoms have in getting returns on their investments in the highly fragmented European markets.18 One data point suggested why Europe may lead the way in approving consolidation: The average number of subscribers per mobile operator in Europe is 4.5 million, compared to 95 million in the United States, 300 million in India, and 400 million in China.19 Even more recently, in September of 2024, former European Central Bank president Mario Draghi (who is also a former Italian prime minister) submitted a 69-page report, in which there was a section supporting market telecom consolidation.20

In most countries, there are usually financially strong wireless telecoms in the No. 1 and No. 2 slots, as measured by revenues and subscribers. The third player is often less financially strong, but the fourth operator (or fifth or sixth, depending on the market) can be even less financially strong. These operators in the lower slots often caution that it may not be possible to continue network investments going forward. In these markets, proponents argue to regulators that three robust competitors can benefit consumers, enterprises, and the overall competitive landscape more than two dominant players and two or more weaker ones.

There appear to be a number of wireless telecom markets in Europe and elsewhere that could see customer-facing consolidation as a result.

One important factor behind the regulatory stance shifting is that connectivity choice has never been higher. As we have written about in the 2024 and 2023 Telecommunications Outlooks, consumers and enterprises have seen a surge in choice over the last few years. These choices include but are not limited to:

- Fixed wireless access competition for home broadband service. Deloitte predicts that over 30 million homes will connect via fixed wireless access in 2025, up 20% from the current year.21

- Low Earth orbit satellite competition for home broadband, especially in rural and remote areas. Over three million homes are currently connected worldwide by this approach, with multiple new networks expected to launch in 2025 and 2026.22 It should be noted that low Earth orbit satellites are less of a factor in countries with high population density and unchallenging geography such as that found in some of Europe. They’re more of a factor in less dense markets, or markets with mountains, deserts, or many small islands such as those in Asia Pacific, Africa, and the Americas.23

- 3G, 4G, and 5G still in use. In some markets, there are multiple networks in use, which provides more choice and competition for consumers.24

- Mobile virtual network operators on the verge of change. Mobile virtual network operators have been around for 25 years but have recently reached an inflection point and started taking more of a share of recent mobile subscriber additions.25 As an example, there are about 14 million US wireless customers for cable mobile virtual network operator offerings as of 2024. It’s worth noting that these are succeeding in part due to the viability of Wi-Fi. Both home Wi-Fi and Metro Wi-Fi hotspots allow US cable companies to offload 87% of all wireless data consumption.26

Bottom line

For telecoms, maintaining a robust and competitive wireless network over the next few years is likely to be less expensive than in the past few years. A costly part of the 5G network build, buying new equipment and purchasing spectrum, is now mainly over for many operators in developed world countries. RAN spending, after peaking in 2022, is now dropping at double digits for the foreseeable future.27 Most global telcos who built 5G non–stand-alone networks initially are not spending as much to upgrade to 5G stand-alone networks.28 And there are no signs that 6G is coming before 2030, if then. As a result, the annual capex intensity for the industry (which hit a 10-year peak in 2022 at 17.8%)29 is predicted by Deloitte to decline further to the 15% to 16% range from 2025 to 2029. This is positive for network operators, although may be a challenge for the RAN original equipment manufacturers.

On the other hand, telecoms often struggle to make money from 5G and other new services, except for fixed wireless access. As stated in TMT Predictions 2024, consumers have likely reached an “era of enough,” and most are unwilling to pay more for higher speeds.30 Further, potential monetization sources such as premium services to support consumer virtual reality or augmented reality glasses, private 5G networks for enterprises, self-driving cars, or telesurgery are niche at best. Some telecoms have started getting into telecom-adjacent, value-added services (healthcare, agtech, security, and more), but so far, the impact of these on most bottom lines appears to be fairly small. Some telecoms could consider getting into the gen AI data center business as a way of generating additional revenues and profits, but these are usually the larger players in the market and not an option for the usual third- and fourth-place players who are more likely to merge.31 Further, many value-added services often require scale to succeed, and as noted earlier, most European and smaller Asian telecoms lack that scale due to the fragmented market.

At a high, global level, there are often two different regulatory authorities who need to approve wireless mergers. There is an industry regulator (Ofcom in the United Kingdom, the Federal Communications Commission in the United States, and both EU-level and national-level industry regulators in the EU)32 and a competition regulator (the Competition and Markets Authority in the United Kingdom, the Federal Trade Commission in the United States, and the Directorate-General for Competition in the EU, plus national-level competition authorities). There are similar divisions of regulatory authority across much of Asia Pacific.33

Once again, at a high level, the industry regulators have generally been more open to merging wireless players within a country, while the competition regulators have been the larger challenges. We believe that may be changing in some jurisdictions, especially spurred on by recent papers and letters in Europe encouraging the merger of subscale wireless players.

That said, regulators will likely take their time and investigate closely: Multiple, recent mergers took 24 to 36 months to close.34 However, the percentage of mergers that get approved overall could increase, if our prediction is correct.

Sometimes regulators approve mergers unconditionally, but they also sometimes have conditions, such as divestitures, pricing guarantees, or commitments for future investments or providing 5G coverage, prior to approving a merger.35

{kind=link}

{kind=link}