Bitcoin has been saved

Bitcoin Fact. Fiction. Future.

27 June 2014

- Tiffany Wan, Max Hoblitzell

Virtual currencies such as Bitcoin could be the natural next stage in the evolution of money.

Introduction

Despite an explosion in media coverage, virtual currencies such as Bitcoin are misunderstood. Every day, news articles describe exchange meltdowns, price volatility, and government crackdowns. This focus on Bitcoin as a volatile and even renegade currency may be distracting governments and businesses from its potential long-term significance as a disruptive new money technology.

Bitcoin is more than just a new way to make purchases. It is a protocol for exchanging value over the Internet without an intermediary. Much has been written about the payment applications of Bitcoin, including remittances, micropayments, and donations. However, Bitcoin could soon disrupt other systems that rely on intermediaries, including transfer of property, execution of contracts, and identity management.

As the Bitcoin ecosystem evolves and use cases emerge, the public and private sectors will face new challenges, opportunities, and responsibilities. Government may discover new methods for executing its mission as a regulator and law enforcer, while corporations may build upon Bitcoin technology to create innovative products and services. In the future, Bitcoin may even revolutionize the way we conduct business and think about work. The sooner the public and private sectors understand the potential of this new technology, the better prepared they will be to mitigate its challenges and realize the benefits of Bitcoin and other similar virtual currencies.

This report explains the technology underlying Bitcoin and other virtual currencies, identifies new applications, and explores the impact of potential future scenarios. If Bitcoin’s short history is an indicator, the future of this technology will be an exciting ride.

Bitcoin overview

Bitcoin is best thought of as a natural next step in the evolution of money. Throughout history, many items have been used as a store of value and medium of exchange, such as cowrie shells, clay tablets, coins, and now paper money. Starting in the 18th century, nation-states increasingly used precious metals such as gold and silver to back their paper money, creating a monetary system called the gold standard. The gold standard required governments to hold enough precious metal reserves to support their currency. As the global economy became more complex in the second half of the 20th century, most nations eventually moved away from the gold standard, creating fiat currencies built on laws and trust in government.

As our understanding of money as a store of value, medium of exchange, and unit of account has matured, so have the methods and modes for exchanging it. In this sense, the exchange of money has always been a function of the technology available. We moved from precious metal coins to paper money before inventing checks, then credit cards. Yet credit cards weren’t created for the Internet era. They’ve simply been adapted to meet the needs of consumers operating in a networked and digital world. With the consumer-accessible Internet now 20 years old, the question is not why a currency specifically designed for the Internet has emerged, but what took it so long.

Bitcoin is one of the first currencies born on the Internet to be used in the real economy. It can be used to make purchases of goods like smartphones, hotel stays, pizza, and coffee. Other virtual currencies have since been created from the same open source code as Bitcoin, including Litecoin and Dogecoin, the virtual currency based on the Doge meme.1 More are popping up every day. Some of these currencies aim to improve upon Bitcoin’s technical or operational difficulties, such as transaction speed and security. However, Bitcoin so far has sustained its first-mover advantage. It is the most popular and has the highest value in circulation. As of June 4, 2014, there are 12.85 million bitcoins in circulation with a total market capitalization of $8.3 billion.2

How does Bitcoin work?

Bitcoin is a protocol for exchanging value over the Internet without an intermediary (figure 1). It’s based on a public ledger system, known as the block chain, that uses cryptography to validate transactions. Bitcoin users gain access to their balance through a password known as a private key. Transactions are validated by a network of users called miners, who donate their computer power in exchange for the chance to gain additional bitcoins. There is a fixed supply of 21 million bitcoins that will be gradually released over time at a publicly known rate. There is no monetary authority that creates bitcoins. The capped supply of 21 million is known to all, and the rate of supply diminishes over time in a predictable way. As a store of value, this means that bitcoins are inherently deflationary. It also means that there is no government or central entity to make discretionary decisions about how much currency to create or attempt to defend it through monetary policy actions.3

In order to process a bitcoin-denominated transaction, Bitcoin verifies two facts addressed by current payment systems like PayPal or Visa. The first is that when user A transfers a bitcoin to user B, user A has a bitcoin to spend (that is, prevention of counterfeiting). The second is that when user A transfers a bitcoin to user B, user A is not trying to transfer the same bitcoin to another user, user C, simultaneously (that is, prevention of double spending).

As Bitcoin matures, an ecosystem of companies is emerging to support consumers and retailers in storing, exchanging, and accepting bitcoins for goods and services:

- Banks and wallets store bitcoins for users either online or on storage devices not connected to the Internet, known as “cold storage.”

- Exchanges provide access to the Bitcoin protocol by exchanging traditional currencies for bitcoins and vice versa.

- Payment processers support merchants in accepting bitcoins for goods and services.

- Financial service providers support Bitcoin through insurance or Bitcoin-inspired financial instruments.

What are the qualities of Bitcoin as a technology system?

Bitcoin has three qualities that differentiate it from other currencies and payment systems.

First, Bitcoin is peer to peer, transferring value directly over the Internet through a decentralized network without an intermediary. Current payment systems, like credit cards and PayPal, require an intermediary to validate transactions; Bitcoin does not. As a result, Bitcoin has been referred to as “Internet cash,” as it can be exchanged from person to person much like paper currency today.

Second, Bitcoin is open, yet securely authenticated. Traditional payment systems rely on the privacy of transaction information to maintain security. For example, the compromise of a credit card transaction can result in the release of valuable information that can be used to conduct future transactions. In comparison, Bitcoin relies on cryptography. As every transaction is validated with cryptography by the network of miners, Bitcoin functions because of its openness, not despite it.

Third, Bitcoin is self-propelling. Bitcoin uses its own product, bitcoins, to reward or “pay” miners who are providing the computing power that serves as the engine of the transaction verification system. As a result, the system does not require the same type of overhead that traditional payment systems might require. In this sense, Bitcoin functions because of those participating in the system.

These three aspects are part of what drives Bitcoin’s success, enabling a nearly frictionless global payment system. However, these same factors have also created challenges.

Miners are individuals that provide the computing power for Bitcoin’s validation process in exchange for the opportunity to gain new bitcoins. Together, miners make up Bitcoin’s distributed network. Miners use their computing power to validate transactions by solving a cryptographic problem, called a hash function. By using their computing power for this work, miners are rewarded with bitcoins. This is how new bitcoins enter the money supply. Because the money supply is capped and the rate of supply diminishes over time, the difficulty of creating a block increases and the actual amount rewarded for each new block created decreases.

Mining has been the subject of significant media coverage, as an arms race has grown around hardware designed to perform highly specialized computations to mine bitcoins. In the early days of Bitcoin, miners were mainly hobbyists using personal computers to solve relatively simple cryptographic problems. Now, miners are raising investor dollars to construct server farms optimized for bitcoin mining.

Bitcoin caveats: Speculation, regulation, and whatever

In order to achieve wider adoption as a currency, Bitcoin needs to address significant questions around volatility, regulatory uncertainty, exchange security, ease of use, and transaction volume.

Bitcoin speculators have driven significant price volatility, reducing Bitcoin’s utility as a medium of exchange. People may be reluctant to use Bitcoin to make large future commitments of value, or even buy a cup of coffee, when the price can change by 30 percent overnight. Unless Bitcoin’s volatility settles, it will be used less as a currency and more as a vehicle for speculation and “get rich quick” schemes, much like a penny stock.

The global regulatory environment around Bitcoin remains uncertain. Any news of new government scrutiny or rumors of a policy change can significantly affect Bitcoin prices, reducing its stability as a currency. At the same time, businesses are unwilling to engage in the Bitcoin economy, while governments treat it as a fringe movement that is the purview of black-market operators and drug dealers, such as Silk Road. As governments begin to issue consistent guidance on Bitcoin, businesses may become more willing to accept it as a form of payment.

Security problems, punctuated by highly publicized exchange meltdowns, may prevent mainstream usage of bitcoins as a currency. Many exchanges that have suffered—including Mt. Gox, which experienced the most notorious exchange collapse—were built on unstable platforms with little security, due to their having been created when bitcoin trading was small and nascent. Mt. Gox was like a bank storing valuables in the lobby entrance. To mature, exchange security needs to be as strong as at traditional banks.

The requirements necessary to safely store bitcoins have created ease-of-use problems. Though digital wallets have worked to solve some of these problems, best practices for storing bitcoins include locking flash drives in a bank vault. Really? Mainstream consumers are unlikely to use Bitcoin until wallet services develop more user-friendly and secure storage techniques.

One of the first major online retailers to accept bitcoins, Overstock.com, made more than $124,000 in bitcoin sales on January 10, 2014, its first day of accepting the currency.

Validating transactions requires significant electricity, bandwidth, and data storage. The resources required to support Bitcoin’s relatively small volume of transactions are already being pushed to their limits. Currently, Bitcoin averages about 60,000 transactions per day.4 VisaNet, the electronic payment processing network used by Visa, handles more than 150 million transactions daily from 2.1 billion Visa cards and over 2 million ATMs.5 It can do this because it charges fees for the resources required to operate its servers. In order to support mainstream transaction volumes, the Bitcoin system for validating transactions will likely have to change how it uses electricity, bandwidth, and data storage.

Despite these obstacles, mainstream merchants are beginning to explore Bitcoin. One of the first major online retailers to accept bitcoins, Overstock.com, made more than $124,000 in bitcoin sales on January 10, 2014, its first day of accepting the currency. By March 2014, Overstock.com had topped $1 million in bitcoin purchases. The company has revised its bitcoin revenue projection for 2014 from an initial $3 to 5 million to $20 million.6 According to Overstock.com, Bitcoin’s popularity and its low fee structure drove new consumers to its marketplace. More large-scale merchants and mainstream actors in the global economy are following suit. SecondMarket, an online marketplace for buying and selling illiquid assets such as venture-backed private-company stock, is opening a Bitcoin trading platform for institutional investors.

Bitcoin: Beyond money

Bitcoin is more than a new currency. Bitcoin and other virtual currencies are creating a new architecture for exchanging information over the Internet that is peer to peer, open yet secure, and nearly frictionless. Imagine how other systems that rely on intermediaries, such as property transfer, contract execution, and identity management, could be disrupted by a similarly open peer-to-peer system.

System of payment

Bitcoin reduces friction in payments. Currently, when an individual transfers funds, he or she must work with a third party. This intermediary, such as a credit card or payments company, often exacts high fees. For example, for remittances, there is an average fee of 9 percent, with some banks charging an additional fee of up to 5 percent for turning the remittance into cash.7

Bitcoin allows for a direct payment to anyone, anywhere in the world, at any time (figure 2). With Bitcoin, an individual could transfer value to his or her cousin in India without paying a fee to a global money transmitter or a bank for the wire transfer. Though most uses of Bitcoin to make payments will rely on third parties, like Coinbase, Bitcoin may allow these companies to charge lower fees than they do today. This could disrupt the global remittance market, valued at $514 billion in 2012, by providing a less expensive method for direct transfers globally.8 Current providers may be forced to lower fees or be replaced by entrants like BitPesa, a mobile payment application for Bitcoin in the developing world.

In the same way that Bitcoin lowers transaction costs for remittances, it could also lower transaction costs for everyday purchases of low-margin items. Today, if someone buys a donut with a credit card, the merchant pays an interchange fee to the credit card issuer. This interchange fee is usually a small flat amount (10-20 cents) plus a percentage of 1-3 percent.9 For a low-margin good like a donut, a 10- to 20-cent flat fee can approach 100 percent of the cost of goods. This interchange fee is often passed on to the customer. Using Bitcoin, the transaction fee could be lowered to as little as 1 percent.10 This could ultimately evolve into a new payment system for credit card companies and banks.

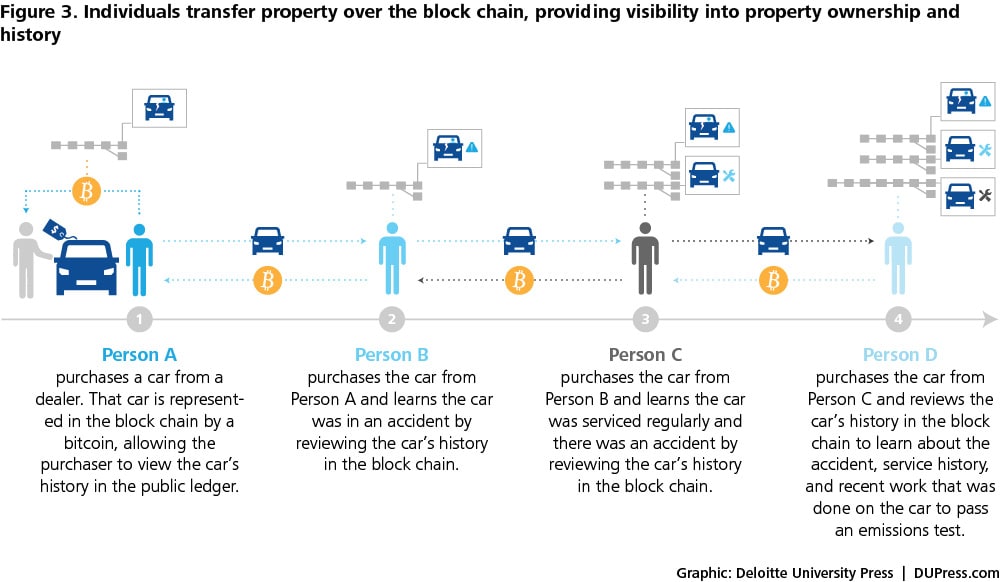

Transfer of property

The Bitcoin protocol could simplify complex asset transfers, revolutionizing the services that support this industry (figure 3). Currently, the transfer of large assets requires significant time and resources. For example, in order to purchase a car from an individual seller, one has to engage a third party to transfer the title. Additionally, one has to use services to learn about the car’s accident and inspection history. And who doesn’t like to spend a Saturday at the Department of Motor Vehicles updating a car registration?

The block chain, Bitcoin’s public ledger, could change all of this. Bitcoins can be qualified in such a way that they represent real-world assets. Bitcoin entrepreneurs at companies like Colored Coin are already working on ways to use small portions of Bitcoin to denote physical property. A fraction of a Bitcoin would publicly identify who currently owns that property, and could include a record of both past ownership and other history about the property. When purchasing a car, one would be able to verify all accidents and inspections over the block chain and transfer the title on site. Similarly, real estate and financial instrument transactions could all be executed over Bitcoin or a similar protocol.

This could soon create efficiencies and reduce friction by allowing individuals to directly transfer property without the use of a broker, lawyer, or notary to sign off on the transfer.

Execution of contracts

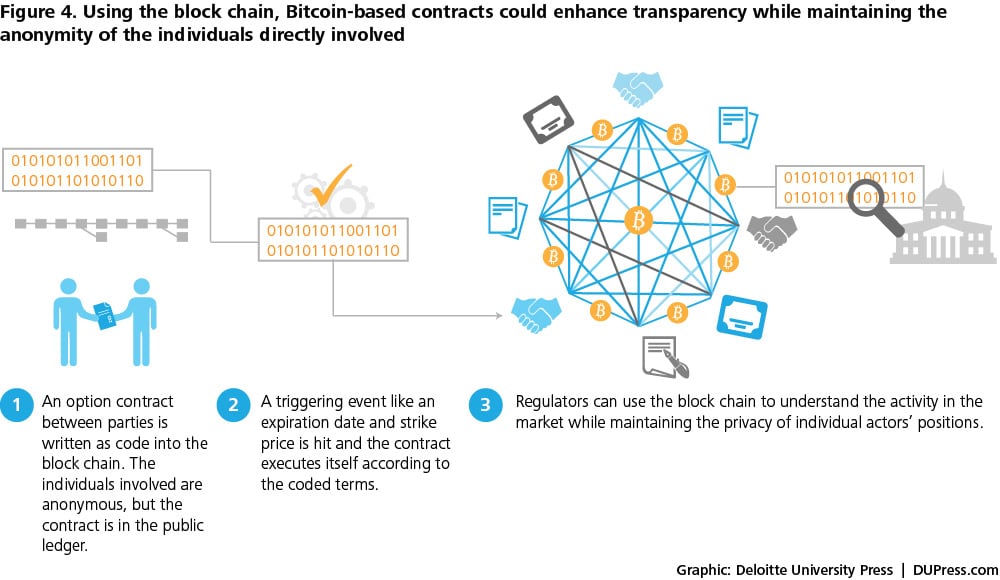

Bitcoin could similarly be used to structure contracts, bringing new efficiency and transparency to the process (figure 4). Contracts are typically developed by lawyers on a case-by-case basis, with significant time and resources devoted to negotiation, development, and enforcement. Additionally, markets based on contracts, including certain financial derivatives markets, lack transparency, which complicates regulation.

Traditional contracts could be replaced by code that self-executes when a triggering event occurs. In a simple example, a financial instrument, like an option, could be developed and executed over the block chain. In addition to reducing legal fees, this could bring new transparency to financial markets, as regulators could use the public ledger to understand the market without forcing individual actors to reveal their specific positions. It is possible that new crypto-currencies will emerge to serve these niche purposes.

New ventures, like Ethereum, are creating these capabilities today. Ethereum is developing a network to serve as both the registry and escrow to execute the conditions of a contract automatically through rules that can be checked by others.

Identity management

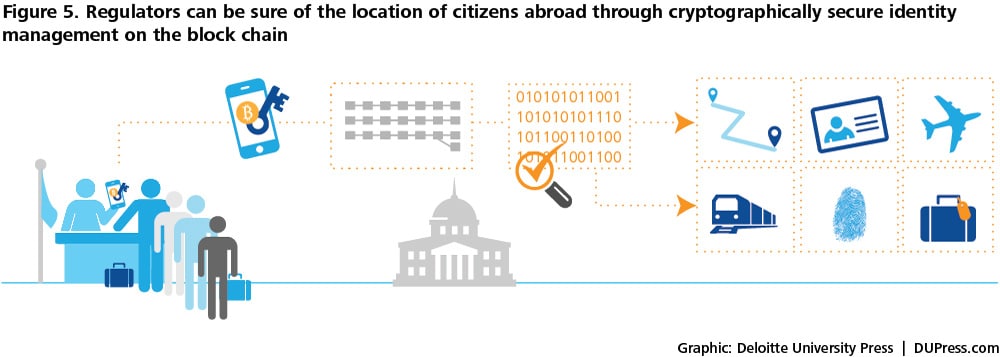

Bitcoin’s cryptography and block chain could also transform identity management. Much of identity management, including passports, still operates on a paper-based system. These documents are frequently forged and stolen. Interpol’s database currently lists 39 million stolen travel documents. But what if there was a way to create a unique, verifiable key that was impossible to forge?

A cryptographic network similar to but separate from Bitcoin could be used to verify individuals’ identities and monitor movement across borders (figure 5). When a person travels through a checkpoint at a border crossing, instead of showing and scanning a paper passport, he or she could present his or her Bitcoin key. A network privately maintained by the government, a contractor, or other entity could verify the key and register the entry into the ledger. This system, based on cryptography instead of paper documents, would simultaneously increase mobility and security. If Bitcoin can be used for travel documents, it could also be used for other forms of identity management like social security numbers, tax identification numbers, or even driver’s licenses.

Property, contracts, and identity management are only a few examples of how a peer-to-peer, open, and frictionless system could change business in the future. In order to achieve this wider adoption, Bitcoin will need to address significant questions around trust, ease of use, and operability. To date, the Bitcoin community has shown remarkable adaptability and it is already working to mitigate these problems. In the next decade, we can expect significant innovation around the Bitcoin network. Though much of that will revolve around payments, particularly early on, the evolution of Bitcoin could take several diverging paths.

Additional use cases for Bitcoin in the payment space include:

Banking services in developing countries

Developing countries with appropriate mobile phone infrastructure may be able to leapfrog the developed world in the maturation of mobile finance. As a form of electronic banking, Bitcoin could be an avenue for financial inclusion in emerging markets.

Micropayments

A micropayment is a very small financial transaction that occurs online. Practical systems to allow for the transfer of $1 or less online with a credit card do not exist. Bitcoin could facilitate the direct payment to musicians for individual songs or the ability to “tip” individuals on Twitter, Reddit, or other social media platforms. It could also be used for newspapers and other content producers looking for new revenue models.

Future of Bitcoin

Many factors will influence Bitcoin’s evolution, including regulation, technological innovation, and economic conditions. Predicting the future of Bitcoin today resembles what it must have been like to try to comprehend the significance of the Internet in the 1990s. Some experts, such as Ray Kurzweil in his book The Age of Intelligent Machines, first published in the late 1980s, got it spectacularly right. But others, like Paul Krugman, who in 1998 predicted that the Internet’s impact on the economy would be no greater than the fax machine’s, were dead wrong, though for understandable reasons.11 Timelines for the adoption and extension of new technologies are inherently unpredictable, primarily because their ultimate impact will be a result of how humans interact with them.

Bitcoin’s future can best be understood by considering four scenarios that represent a range of possible outcomes.

“Life on the fringe”

“Investors flee Bitcoin as another exchange collapse sends bitcoin prices plummeting”

Bitcoin, the currency, never solves its trust and security problems, reinforcing price volatility and skepticism. It remains an arena for illegal activity and speculation. As a result, companies in the Bitcoin ecosystem are unable to enter into mainstream commerce. Exchange collapses and sales of illicit goods and services continue to occur. The majority of bitcoins are held by speculators, crowding out users who want to use the protocol to make legitimate purchases. Bitcoin and its imitators resemble penny stocks instead of a payment system. In short, the focus on bitcoin’s obstacles as a currency prevent the benefits of the technology from being fully realized.

How you can tell if this scenario is happening:

- Another exchange meltdown, security breach, or operational failure occurs

- Volatility continues to be 10 to 15 times higher than traditional assets such as gold 12

- Bitcoin suffers a flash crash

Why this scenario might not happen:

- The Bitcoin community solves the trust and security problems related to bitcoin as currency

- Bitcoin as technology overwhelms the reservations about bitcoin as currency by creating new offerings and markets

What government’s role could be:

- Issue guidance and regulations on Bitcoin as a currency and as a technology, signaling that both aspects can be taken seriously

- Focus on enforcement for illicit activity, like money laundering

- Create safeguards to protect mainstream consumers from being victimized by Bitcoin wallet and exchange scams

“CorporateCoin”

“Payment card companies compete to offer low-fee Bitcoin-based payment options”

Payment and technology companies incorporate the Bitcoin protocol into their payment systems. These companies build proprietary payment platforms using cryptography for security and the block chain for transaction validation. Bitcoin moves to the back office and becomes invisible to the consumer in the same way that different Internet protocols are invisible to most web users. As a result, payments occur across the Bitcoin protocol, but consumers are not required to hold bitcoins. This drives down fees for payment cards and eliminates exchange risk. In short, the Bitcoin protocol grows as a money technology, is adopted by mainstream institutions, and begins to serve as the backbone of many Internet transactions.

How you can tell if this scenario is happening:

- Services offered by traditional payment solutions, like credit and fraud protection, are provided around Bitcoin

- A new wallet technology is introduced in the form of a Bitcoin payment card

Why this scenario might not happen:

- Large payment companies lower fees to match Bitcoin without adopting its protocol

- Corporations continue to distrust open-source technology

What government’s role could be:

- Enable companies to use Bitcoin as a payment mechanism through tax and financial crimes enforcement guidance

- Encourage payment companies to use the Bitcoin protocol to offer low-fee solutions for underbanked populations

“Satoshi for all”

“Regulators rescue Wall Street after block chain exposes new market risk”

Bitcoin becomes the protocol for all transfers of value, creating new visibility into financial markets and transforming the services around these functions. Exchanges of value and information, such as property transfer, contract execution, and identity management, are all performed on the block chain. As a result, the services that support these functions are revolutionized. Professionals like traders and lawyers focus on writing code and maintaining the block chain. The process of regulation is changed as well. Regulators download the ledger for a market, such as commodities, every day. Bitcoin’s pseudonymity allows regulators to understand the risk of entire markets, while still maintaining the privacy of individual actors. The government creates the Block Chain Administration to oversee cryptographic exchanges and provide consumer protection. In short, all transfers of value are executed in a peer-to-peer and open, yet secure way, reducing fees and increasing transparency.

How you can tell if this scenario is happening:

- A piece of physical property is exchanged over the block chain

- Financial instruments, such as options, are created and traded over the block chain

- A Bitcoin-based central clearinghouse is launched

Why this scenario might not happen:

- Economic path dependence on current systems prevents such significant disruption

- Stakeholder interests challenge adoption

- A Bitcoin programming skills gap expands as the demand for programmers increases

What government’s role could be:

- Provide consumer protection and education

- Regulate block chain-based transfers, providing standardization, security, and enforcement

“New networks”

“Number of individuals working 15 or more jobs reaches 10 percent of US population”

Two key attributes of Bitcoin enable a transition to a new model of work and employment. First, Bitcoin’s utility in facilitating micropayments allows people to more easily receive compensation for the many tasks they perform as part of a digital network. Second, and perhaps even more important, is that Bitcoin is a self-propelling, decentralized, peer-to-peer network that allows its members to derive both income and utility from their participation. Today’s technology services, like email and social media networks, provide utility to users free of charge and generate income for owners. But as the saying goes, if you’re getting something for free, you aren’t the customer, you’re the product. In a Bitcoin world, users are both the customer and the product, because individuals participate in the Bitcoin network by both exchanging the currency and validating the transactions. Currently, at the average day job, a person may spend eight hours at her desk and be paid an income for that one role. In addition, he or she is tweeting, reading news articles, and checking out blogs, generating valuable data throughout the entire day. In the future, we could engage in these same activities and get paid for all of them as Bitcoin enables payment for the myriad activities individuals perform as part of a networked economy.

How you can tell if this scenario is happening:

- Mainstream online media sites reward commenters for input

- A public technology company accounts for user income on its 10-K

Why this scenario might not happen:

- This is a major departure from our current employment model

- Achieving this scenario requires technological savvy on a larger scale than exists today

What government’s role could be:

- Adjust definition of employment to include this new type of work

- Refocus taxation and other policies to stimulate this new type of work

- Tap into the new labor pool created by this employment model

These scenarios lie within the realm of the possible. Though the first scenario is closest to the status quo, current trends may indicate that the second scenario is possible in the near term, which may lay the groundwork for the seemingly more distant scenarios. Certainly, some skeptics argue that Bitcoin will be the Esperanto of finance.13 But, others are intrigued by Bitcoin’s potentially more revolutionary impact. As Kevin Kelly, co-founder of Wired, writes in his latest book New Rules for the New Economy, “The great benefits reaped by the new economy in the coming decades will be due in large part to exploring and exploiting the power of decentralized and autonomous networks.”14 Bitcoin is an early example of this future.

Given the spectrum of possible scenarios, the range of actions available to governments and businesses is broad. Some foreign governments have tried to ban Bitcoin by making the exchange of cash for bitcoins illegal. Others have taken a “wait and see” approach, allowing the ecosystem around Bitcoin to develop while closely monitoring it. In the United States, government agencies have begun to issue taxation and other guidance, paving the way for entrepreneurs to create a new wave of Bitcoin-related companies and large corporations to engage in the Bitcoin economy.

Bitcoin is yet another example of how new technologies and trends can pop up seemingly out of nowhere, creating problems and opportunities for government as it sorts out how to respond. Most governments chose a hands-off approach to the Internet when it emerged in the 1980s. But the lessons of the Internet should be fair warning that these new technologies can come out of nowhere and change everything. Bitcoin’s direct relevance to traditional government domains, such as currency and taxes, merits specific consideration. Given its broad potential impact on activities from contracts to identity management, agencies tasked with diverse operations, from financial markets oversight to border patrol, need to monitor Bitcoin’s evolution. Governments need to understand how Bitcoin will evolve in the short term. But even more importantly, they need to explore how the concepts underlying this new technology could intersect with their mission in the future.15

© 2021. See Terms of Use for more information.