Gen Zs and millennials find reasons for optimism despite difficult realities

Deloitte Global’s latest Gen Z and millennial survey reveals how they’re finding balance between uncertainty and optimism and how organizations can create positive momentum

The past few years have been difficult for even the most die-hard optimists, and Gen Zs and millennials, in particular, have faced a battery of challenges. Navigating the COVID-19 pandemic took a toll on their education, career opportunities, and mental health. They’re uncertain about what their futures will look like, and if they’ll even be able to afford it when it comes, given the rising cost of living. Global instability, climate change, and the unpredictable impact of artificial intelligence/technologies all loom large for them.

But Deloitte’s 2024 Gen Z and Millennial Survey, which surveyed more than 22,800 respondents in 44 countries, shows growing optimism among Gen Zs and millennials, despite their concerns about what their futures might look like. This year’s survey identified five key areas where Gen Zs and millennials are becoming more adept at managing the tension between reality and optimism as they look to the future.

They’re uncertain about what will happen at the polls but optimistic about their ability to drive change on social issues

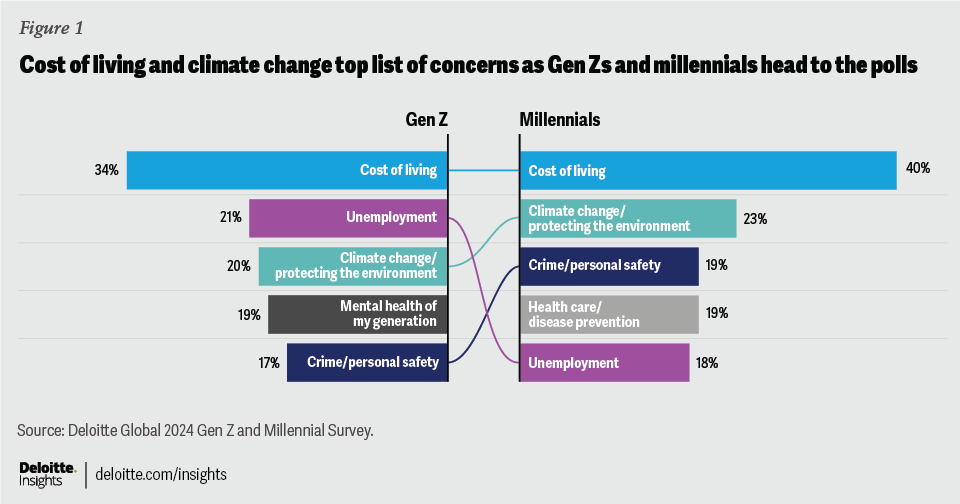

As nearly half of the world’s population heads to the polls this year1—including in 23 of the 44 markets covered in this survey—the year seems to represent one of global choice and opportunity. While the role and significance of upcoming elections this year vary across countries, for many markets, the results of their elections promise to have significant impacts on the issues that matter most to Gen Zs and millennials around the world (figure 1).

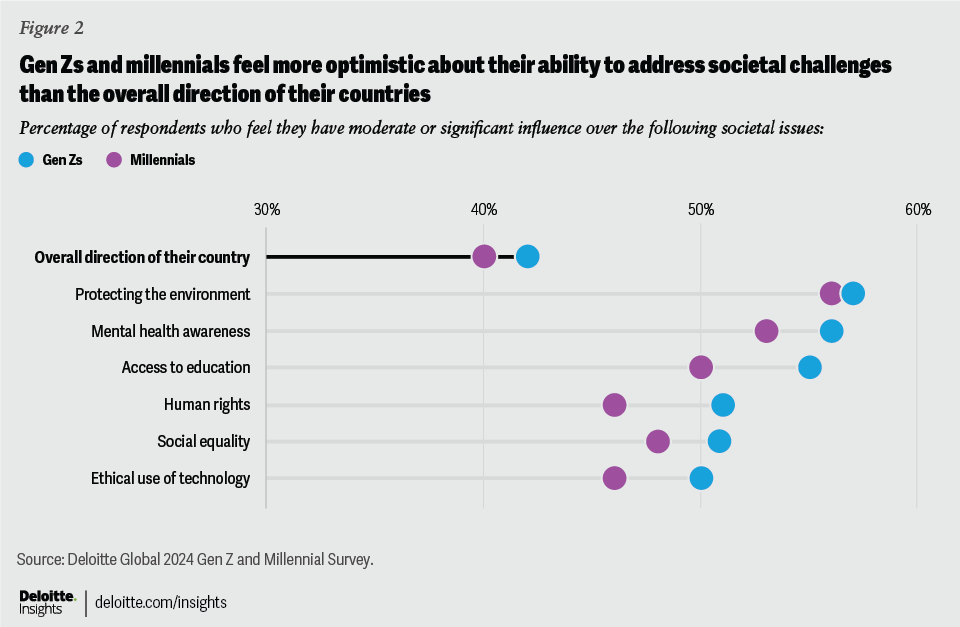

Roughly a quarter of Gen Zs (28%) and millennials (26%) believe that the social and political situations in their countries will improve over the next year—a one-point increase for both generations since last year. But fewer than half of respondents (42% of Gen Zs and 40% of millennials) believe they have an influence on the overall direction of their countries. Both generations are likely to believe they have the agency to drive change on major societal challenges, such as protecting the environment, raising awareness for mental health, increasing access to education, and addressing social inequality (figure 2).

They’re struggling financially but are optimistic about their economic futures

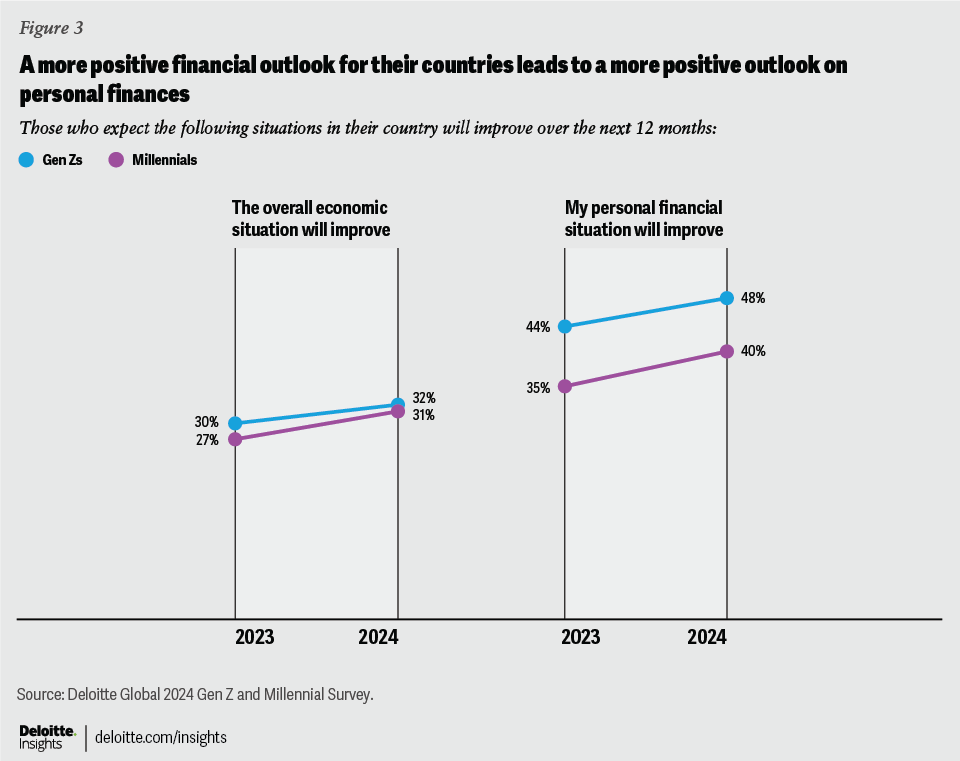

Financial insecurity continues to plague Gen Zs and millennials. Three in 10 (30% of Gen Zs and 32% of millennials) say they do not feel financially secure. And roughly six in 10 (56% of Gen Zs and 55% of millennials) live paycheck to paycheck. The cost of living remains their top concern by a wide margin compared to their other top concerns, which include climate change, unemployment, mental health, and crime or personal safety.

But despite these statistics, Gen Zs and millennials are hanging on to hope. Three in 10 (32% of Gen Zs and 31% of millennials) are optimistic that the economies in their countries will improve within the next year, a sentiment that has trended up since last year and is at its highest since the 2020 survey conducted prior to the pandemic. This optimism also extends to their personal finances, with more than four in 10 Gen Zs (48%) and millennials (40%) expecting their financial circumstances to improve as well over the next year (figure 3).

They’re uncertain about generative AI’s impact on their careers but are optimistic about its potential to make their work lives better

The past year marked a huge leap in the advancement of gen AI. And as new tools and use cases emerge, organizations are racing to harness the opportunities.

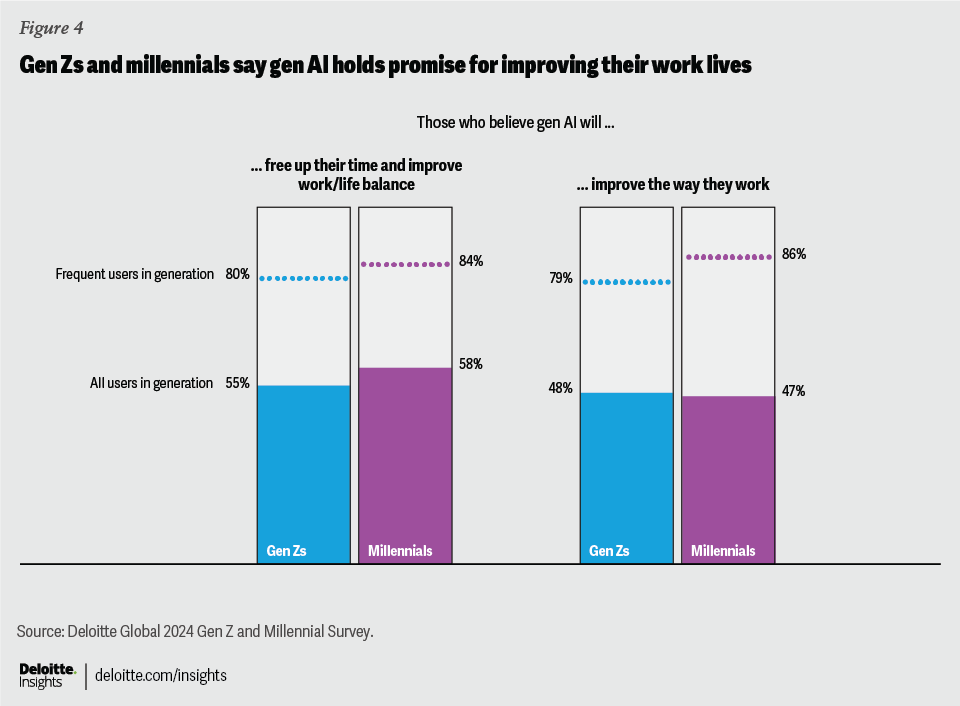

While the top emotion Gen Zs and millennials report feeling when they think about gen AI is uncertainty (24% of Gen Zs and 26% of millennials), excitement and fascination are close behind. Positive perceptions of the technology increase with more hands-on experience. Roughly a quarter of Gen Zs (26%) and millennials (22%) use gen AI at work all or most of the time, and those who do experience excitement and trust at higher levels than the total respondent base. In terms of practical benefits, the overwhelming majority of Gen Zs and millennials who frequently use gen AI believe it will free up their time, improve the way they work, and improve their work/life balance (figure 4).

But frequent use of gen AI appears to have a downside as well: It contributes to increased anxiety around its impact on their careers. Seven in 10 Gen Zs (71%) and millennials (73%) who use gen AI all or most of the time believe gen AI–driven automation will eliminate jobs. Frequent users of gen AI are also more likely to believe that they will need to look for job opportunities that are less vulnerable to automation and that younger generations will find it harder to enter the workforce because of gen AI, potentially because the technology will automate many of the more manual tasks that entry-level workers typically do. In response to these types of concerns, both generations are starting to think about how to adapt. Nearly six in 10 Gen Zs (59%) and millennials (57%) say that the prevalence of gen AI will require them to reskill and will impact their career decisions.

They don’t believe business is living up to its responsibility to make the world better but are optimistic about their collective influence

Roughly six in 10 Gen Zs and millennials believe that business has the opportunity to influence a range of societal challenges. Protecting the environment (65% of Gen Zs and 68% of millennials) and ensuring the ethical use of technologies such as gen AI (65% of Gen Zs and millennials) are at the top of that list. And nearly two-thirds of Gen Zs and millennials (63%) believe business has the ability to influence social equality.

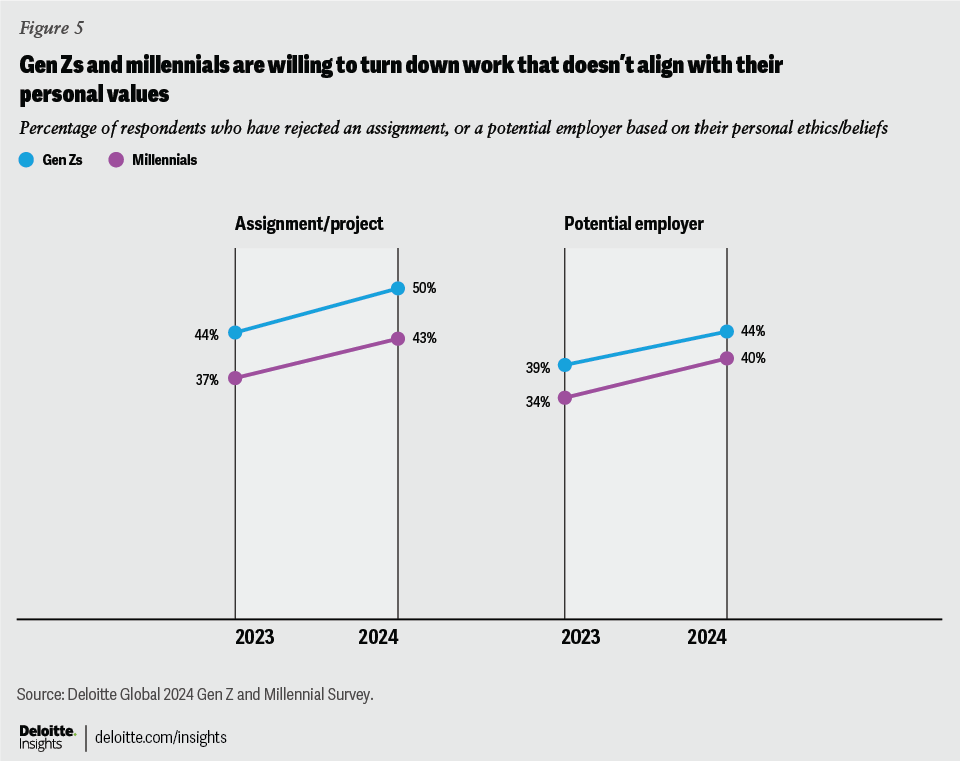

While respondents feel largely positive about their individual employers’ societal impacts, they are less certain about the impact of business more broadly. Less than half believe business is actually having a positive impact on society. But they are optimistic about the impact of their collective power. Six in 10 Gen Zs (61%) and millennials (58%) believe they have the power to drive change within their organizations, particularly when it comes to workload, the services offered to clients, learning and development, diversity, equity, and inclusion, wellness, social impact, and environmental efforts. Three-quarters of respondents say that an organization’s societal impact is an important factor when considering an employer, and Gen Zs and millennials are pushing businesses to take action through their career decisions and consumer behaviors (figure 5).

For example, protecting the environment is the top societal challenge on which respondents feel businesses have the opportunity and necessary influence to drive change, and they are willing to reject assignments or employers who don’t align with their environmental values. Two in 10 Gen Zs and millennials have already changed jobs or industries to align with their environmental values, with another quarter of both cohorts planning to do so in the future. They also actively research the environmental practices of companies they purchase from and are willing to pay more for sustainable products.

They’re still struggling with stress and mental health but are optimistic about the progress their organizations are making

While there has been a slight decline since last year’s survey, stress levels continue to be very high among Gen Zs and millennials, with 40% of Gen Zs and 35% of millennials saying they feel stressed all or most of the time. About a third of respondents say that their jobs (36% of Gen Zs and 33% of millennials) and their work/life balance (34% of Gen Zs and 30% of millennials) contribute a lot to their stress levels. In addition, transparency about mental health in the workplace continues to carry a stigma, with nearly three in 10 from both generations being worried that their managers would discriminate against them if they were to raise concerns about mental health.

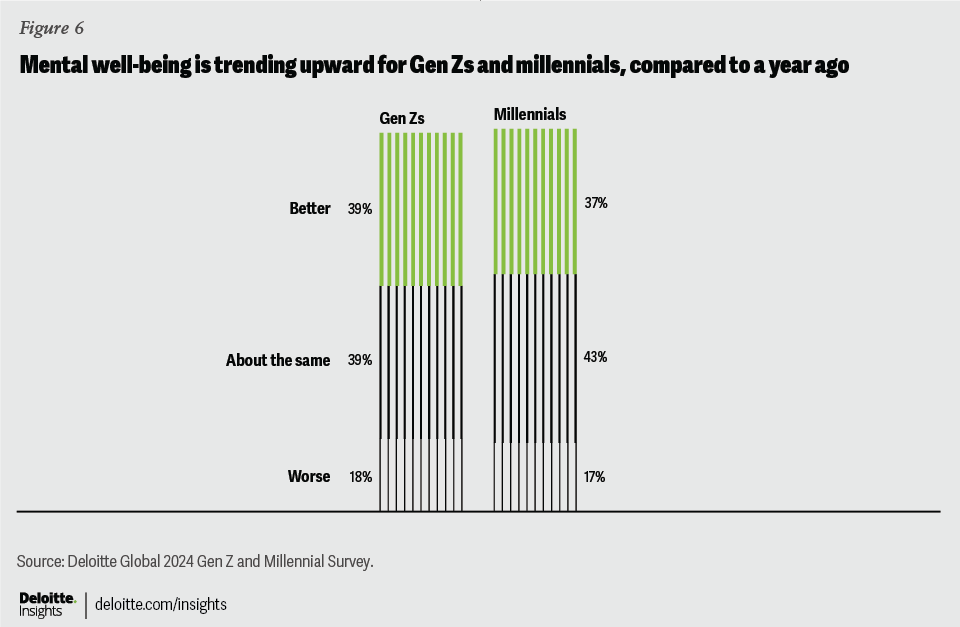

But Gen Zs and millennials seem to be optimistic about the progress their organizations are making. Just over half of Gen Zs (54%) and millennials (55%) agree their employers take the mental health of their employees seriously, and about half of respondents have seen positive changes within their workplaces over the last year when it comes to mental health (51% of Gen Zs and 50% of millennials). As a result, overall mental health seems to be trending in a positive direction: Thirty-nine percent of Gen Zs and 37% of millennials say their mental health improved over the last year, and only 18% of Gen Zs and 17% of millennials report that their mental health worsened over the same period (figure 6).

Maintaining momentum

How can organizations tap into the Gen Z and millennial optimism of this moment, and continue to encourage it? Leaders can empower Gen Zs and millennials to drive change within their organizations and demonstrate their commitment to positive work/life balance, addressing mental health in the workplace, and to the social and environmental values that these generations are passionate about. Consider these opportunities to engage your Gen Z and millennial colleagues:

- Communicate your organization’s societal commitments, especially during the talent recruiting process. Three-quarters of Gen Zs and millennials (75%) say that an organization’s community engagement and societal impact are important factors when considering a potential employer. Since Gen Zs and millennials are using career decisions to create an impact on the topics that matter to them, strive to make your social commitments visible and discuss them when recruiting new talent.

- Make environmental sustainability a priority for your organization. Environmental sustainability continues to be among the top priorities of Gen Zs and millennials, and the top societal challenge on which respondents feel businesses have the opportunity and necessary influence to drive change. Workers are looking to their organizations to support this value through actions like providing organizationwide sustainability education, subsidies for sustainable choices, and green office renovations. If Gen Zs and millennials feel their organizations don’t share their environmental values, they may be more likely to leave: Two in 10 Gen Zs and millennials have already changed jobs or industries to align their work with their environmental values, with another quarter of both cohorts planning to do so in the future.

- Ease career anxieties with skill development, particularly around gen AI. Nearly 60% of Gen Zs and millennials are anticipating that gen AI will impact their career trajectories and require them to learn new skills. But they say their organizations haven’t stepped up to provide the kind of training they believe they need to be successful in an AI-fueled environment. Only around half (51% of Gen Zs and 45% of millennials) say their employers are training employees on the capabilities, benefits, and value of gen AI. In addition, as the cost of living continues to climb, a third of Gen Zs and millennials in this year’s study say they are forgoing higher education. This highlights a trend toward respondents seeking out alternatives to traditional education. Organizations should consider plans to supplement higher education with learning and development opportunities, particularly as emerging technologies make lifelong learning even more essential for career success.

- Encourage managers and senior leaders to create more transparency about mental health. Managers and senior leaders can play a critical, front-line role in reducing the stigma associated with mental health in the workplace. But around three in 10 survey respondents (27% of Gen Zs and 34% of millennials) say their senior leaders do not share their own mental health experiences. And a similar percentage (26% of Gen Zs and 32% of millennials) say their senior leaders do not speak about prioritizing mental health in their organizations, leading them to feel that these topics are not appropriate for discussion in a professional context. For many people, their relationship with their manager has a significant impact on their mental health—on par with the impact of their partner, and even greater than the impact of their relationship with their doctor or therapist.2 Encouraging managers and senior leaders to be transparent about mental health at work can create greater mental health transparency across the organization.

The findings in our survey reinforce the idea that when organizations drive progress on the workplace issues that matter most to Gen Zs and millennials, it commonly results in employees who are more engaged and more likely to act as brand ambassadors for their organizations. It’s not easy to get all these things right. It requires employers to engage, listen, and adjust their strategies. But those who do get it right can expect to have a more satisfied, productive, future-fit, and agile workforce that’s better prepared to adapt to a transforming world.

Methodology

Deloitte’s 2024 Gen Z and Millennial Survey reflects the responses of 14,468 Gen Zs and 8,373 millennials (22,841 respondents in total), from 44 countries across North America, Latin America, Western Europe, Eastern Europe, the Middle East, Africa, and Asia Pacific. The survey was conducted using an online, self-complete-style interview. Fieldwork was completed between November 24, 2023 and March 11, 2024.

The report includes quotes from respondents who provided feedback to open-ended questions in the main survey. These quotes are attributed to respondents by age, gender, and location.

The report represents a broad range of respondents, from those with executive positions in large organizations to others who are participating in the gig economy, doing unpaid work, or are unemployed. Additionally, respondents include students who have completed or are pursuing degrees, those who have completed or plan to complete vocational studies, and others who are in secondary school and may or may not pursue higher education.

As defined in the study, Gen Z respondents were born between January 1995 and December 2005, and millennial respondents were born between January 1983 and December 1994.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}