Navigating the energy transition from disruption to growth

Energy and industrial companies are positioned for a lower-carbon future

About the study

Deloitte began work on the energy transitions study in January 2020 to garner the perspectives of key decision-makers among energy and industrials companies around low-carbon trends and strategies.

As part of this study, Deloitte and Wakefield Research surveyed 600 C-suite executives and other senior corporate leaders from around the world in March 2020. Twenty-one percent of the respondents identified themselves as C-suite executives (chairman, CEO, COO, CFO, among others); another 31 percent self-identified as senior vice president or vice president, 16 percent identified themselves as senior-level managers such as directors, and the remaining 32 percent included environmental officers, health and safety officers, regulatory compliance officers, and business unit or department heads.

About 20 percent of the surveyed executives indicated company revenues between US$100 million and US$500 million, 60 percent indicated revenues between US$500 million and US$10 billion, and the remaining 20 percent indicated revenues of more than US$10 billion. The executives represented different industry sectors, which were broadly classified as oil and gas, chemicals and specialty materials, power and utilities, and industrial manufacturing (including broader industrial manufacturing, aerospace, heavy equipment, and diversified industrials).

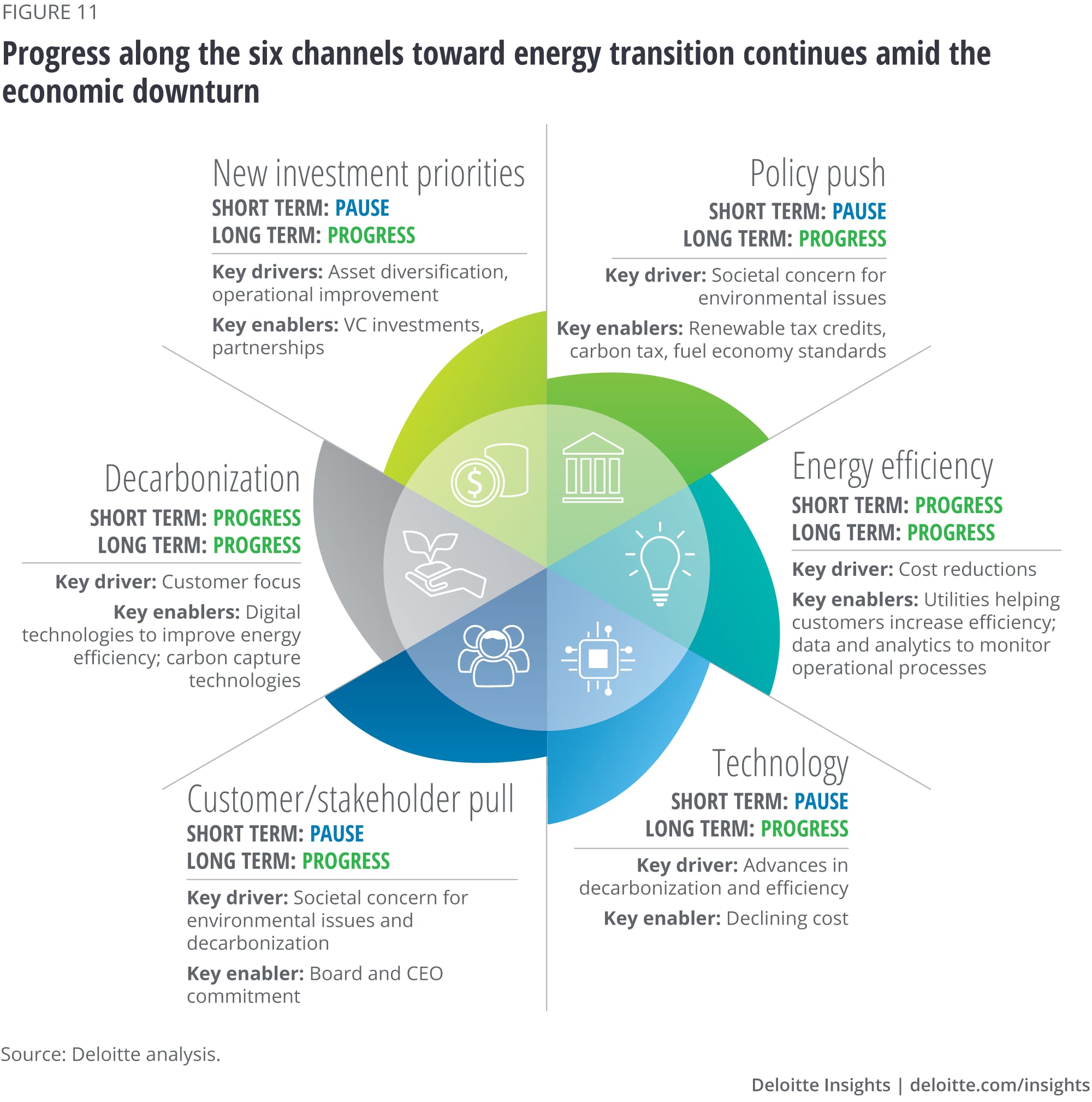

Transition progress across the six channels

Much progress has been made in the first two channels: decarbonization of energy sources and improvements in energy efficiency in energy usage and industrial processes. Advancement along these two channels is expected to continue even in the current economic downturn due to the corporate decarbonization plans already in place and the longer-term benefits expected from realizing energy efficiency gains. However, we may see a temporary pause in the other channels—notably in identifying new investment areas and deploying new technologies—due to immediate spending cuts and market disruptions.

Decarbonizing energy sources and finished products

Our survey respondents reported that their companies either already had a plan in place or were developing a strategy to reduce reliance on fossil fuels: eighty-seven percent of chemical company executives, 92 percent of power and utilities executives, and 92 percent of oil and gas industry executives responded affirmatively to these statements. Across sectors, the top drivers of decarbonization included customer focus and digital technologies supporting energy efficiency and decarbonization. Notably, 56 percent of oil and gas respondents indicated that plan metrics were tied to executive compensation. And when asked if a low-carbon future would have a positive, neutral, or negative impact on the future of their organization, more than 60 percent of oil and gas respondents answered that it would have a positive impact.

Companies are likely to continue to progress along the decarbonization channel in three key areas: increased use of low-carbon power generation, increased electrification, and reduced fossil fuel demand.

Power generation is well on its way to decarbonization

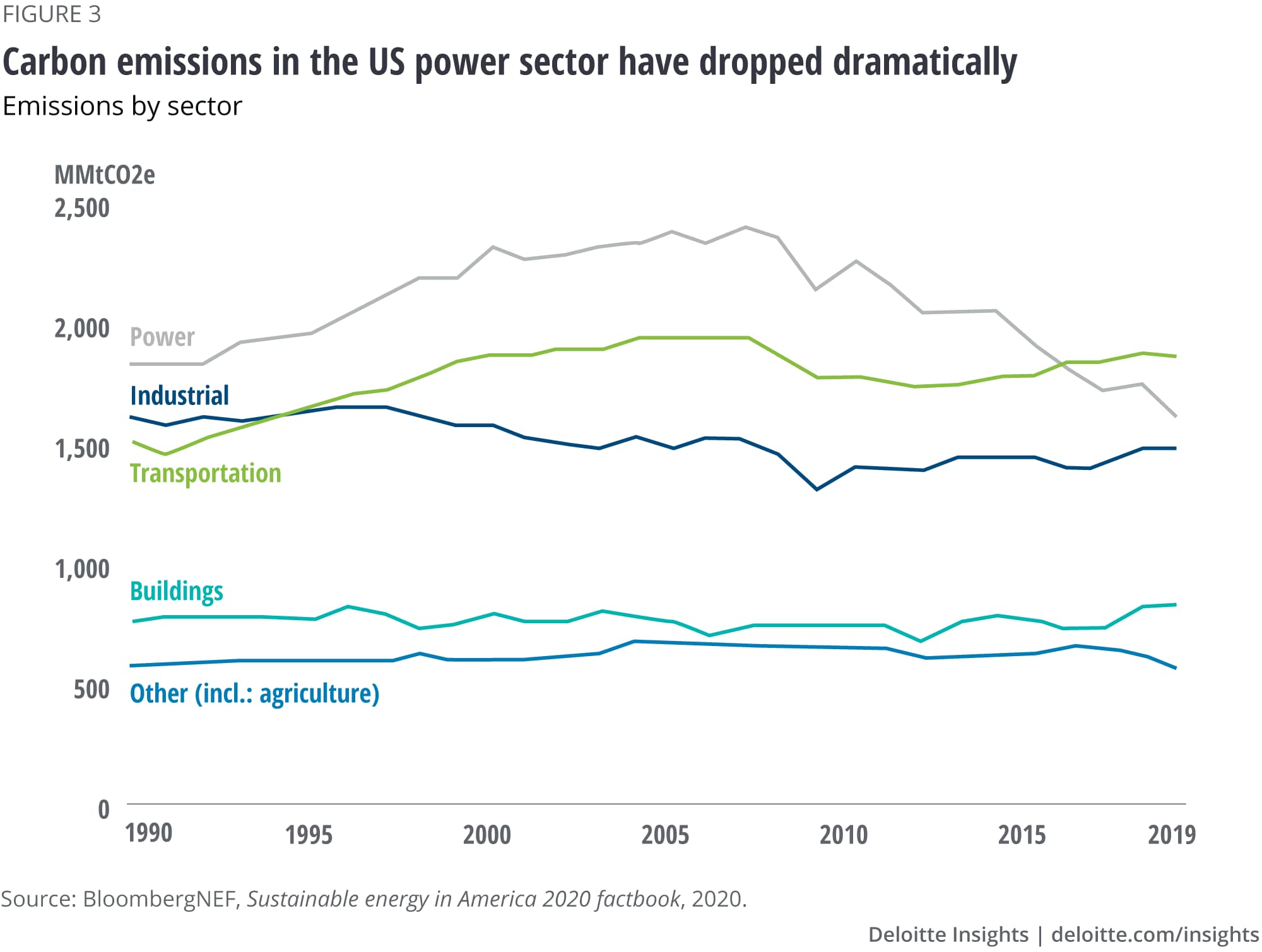

Decarbonization appears already well under way in the US power sector, where 65 percent of customer accounts are served by a utility with publicly stated carbon or emission reduction goals.3 Power and utilities executives surveyed cited three key drivers for their decarbonization strategies: customer support, digital technologies for energy efficiency, and new business models and investment areas. Progress in decarbonizing the power sector is likely also due in part to relative economics. As US shale gas production has increased, low-cost domestic natural gas has replaced coal in the generation mix in many states. Coal has declined from meeting 45 percent of US power demand in 2010 to 23 percent by 2019.4 As a result, in 2019, the United States achieved a substantial reduction in total carbon emissions—almost 3 percent—due to this displacement of coal by cheaper domestic gas in the power sector (figure 3).5

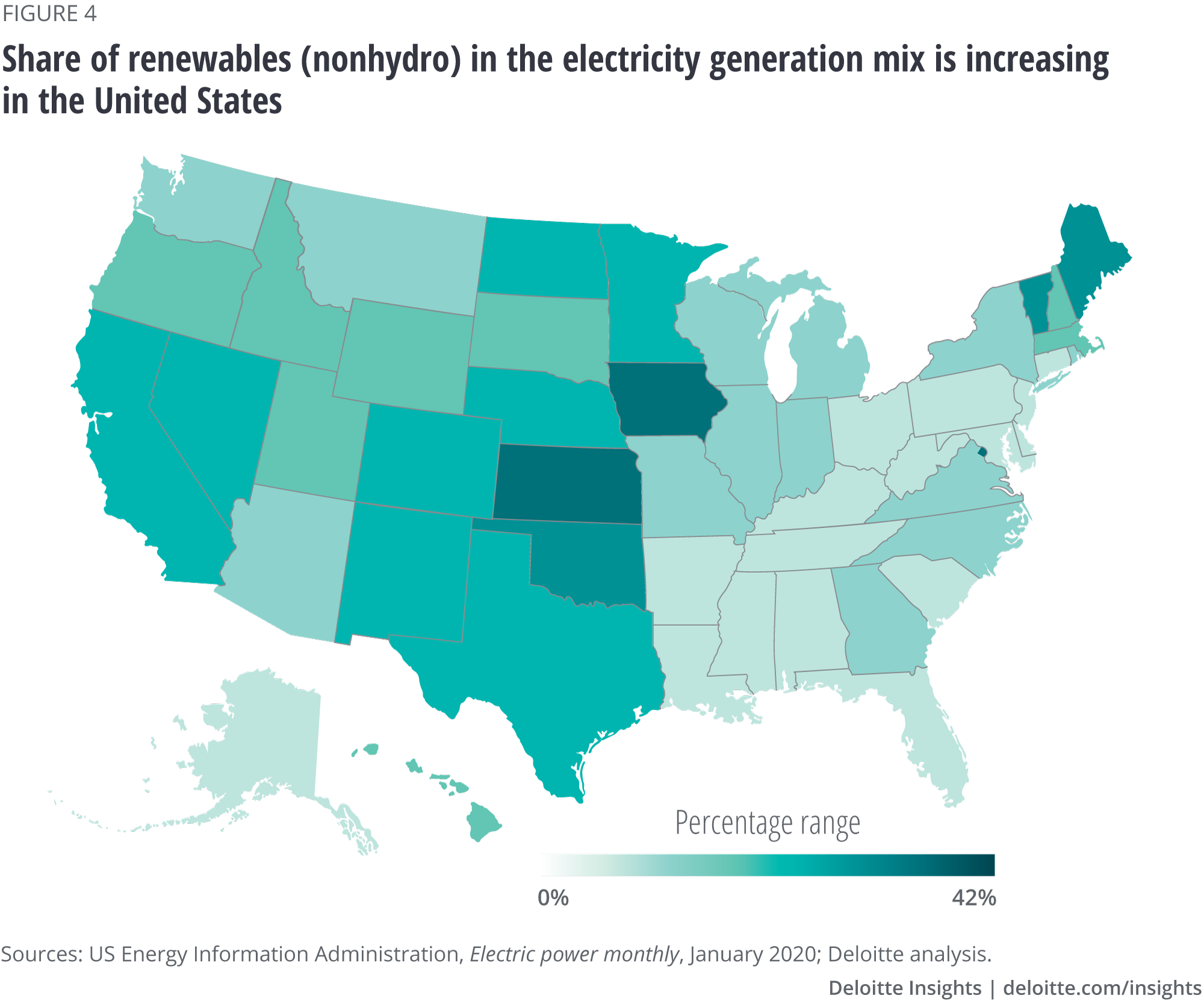

Similarly, the cost of renewable generation has fallen dramatically over the past 10 years, making renewables cost-competitive with gas in some regions. Both equipment and overall project costs have declined as the wind and solar industries have matured and scaled, with the price of the typical solar photovoltaic (PV) module dropping 77 percent and wind turbine costs falling 58 percent over the past 10 years.6 Combining energy storage with renewables is helping many renewables become more dispatchable and further improving their competitive position versus conventional power plants. This has become more feasible recently, as the cost of lithium-ion battery packs has fallen by 87 percent from 2010 to 2019. 7 Due in part to these price dynamics, US generation from renewables has grown by 77 percent over the past decade.8 In the European Union (EU), renewables currently account for 32 percent of power generation, and their share is expected to grow further as they aim to become carbon neutral by 2050.9 In the United States, renewables currently account for just under 17.5 percent of generation mix (figure 4), and are expected to rise to 38 percent by 2050.10

Electrification of additional energy end uses is speeding decarbonization

As the power sector becomes less reliant on fossil fuels, increased electrification of energy end uses throughout the economy could speed decarbonization. Seventy percent of power sector executives polled indicated that their company is working to help customers electrify, particularly with respect to electric vehicles (EVs). Other areas for electrification cited as priorities were industrial processes and buildings (air and space heating and cooling).

The electrification of transport, both light and heavy duty, could have an impact on oil demand, as the transport sector accounts for nearly 60 percent of global oil demand.11 However, the percentage of new vehicle sales involving EVs is still small, even in Europe and China, where policy has supported the move to EVs in the light vehicle sector. In 2019, approximately 2.5 percent of all new vehicles purchased globally were electric, up from under 1 percent in 2015.12 However, the March 2020 drop in global oil prices could slow adoption of EVs if lower gasoline and diesel prices delay the economic parity point with internal combustion engine (ICE) vehicles.

Electrification of fleet vehicles in the industrial sector is proceeding as well and company targets for fleet electrification are projected to rise from current targets of 20 percent of fleets to targets that are closer to 40 percent by 2035.13 Electrification of facilities and processes is happening more quickly. Deloitte’s 2019 100 Percent Renewables study showed that the majority of industrial manufacturers surveyed have electrified their processes where feasible.14 The ongoing move toward electrification in processes such as chemical treatment, cutting, metalworking, and molding seems driven by superior design, quicker startup times, and higher performance. Even though the initial equipment and installation costs may be higher, the low operating cost and increased efficiencies allow companies to achieve a return on that investment. Similarly, electrification of facilities combines electric facility heating and cooling systems with smart connected building management systems and could be a catalyst for using electricity to optimize industrial spaces, including factories, warehouses, and offices.

Decarbonization is expected to slow long-term oil demand growth

Decarbonization trends are having a mixed impact on the oil and gas sector. Increasingly, oil and gas companies are sourcing renewable energy for their needs. And while most do not have a renewables plan per se, 49 percent of respondents plan to switch to cleaner fuels or renewables in their facilities and field operations, according to our survey results. This is particularly true of the larger oil and gas companies, as 61 percent of respondents from this group noted that increasing reliance on clean fuels and renewables was core to their strategy. A similar trend has emerged in the chemical sector: fifty-seven percent of chemical executives reported that their company had invested in using renewables to reduce emissions and waste. In addition, the half of chemicals executives surveyed reported that their company had increased use of renewable energy for production, though this trend is more pronounced among larger chemical companies than at medium or small companies.

Forty-one percent of oil and gas executives surveyed cited integration downstream into refining and chemicals as another strategy for adapting to a lower-carbon future. But growth in demand for oil and refined products is expected to slow in the long term, forcing executives to focus on achieving returns in an industry with a potentially declining demand profile. The peak demand projections for oil and gas vary widely, with some analysts forecasting combined oil, gas, and coal consumption to plateau as early as 2030, while others do not see demand peaking until well after 2050.15 Factors that may reduce refined product demand growth include tightening heavy and light vehicle fuel economy standards, increased use of hydrogen and EVs after 2040, and further shifts to cleaner fuels in shipping. Given these factors, gasoline demand in the United States is projected to fall from 9 million barrels per day in 2019 to 7 million barrels per day by 2050.16 However, should the March 2020 decline in oil prices lead to a lower-for-longer oil price environment, US motorists may respond as usual with purchases of larger, less fuel-efficient vehicles. In other countries where vehicle ownership remains low, refined product demand may continue to grow as motorization levels increase and favor ICE vehicles.

The chemicals industry, which is already facing a situation of oversupply, could also be affected by decarbonization trends. There are two areas to watch closely. First, the price and availability of petrochemical feedstocks could be affected, not only by slowing crude demand growth and oil price volatility, but also by the changing demand for various refined products. Second, end markets for petrochemical companies are changing, including the automotive, consumer, and construction industries. About 11 percent of end products from the chemicals industry target the automotive sector alone.17 But as automakers increase production of EVs, some of the material inputs they need from the chemicals sector may change: Under-the-hood thermal applications are not needed in an EV, nor are antifreeze or lubricants. And with construction accounting for nearly 9 percent of end market demand, the move toward energy-efficient and lower-carbon materials in that sector could also have an impact on chemicals companies’ product slates. 18

Significant progress has been made along the decarbonization channel, as evidenced by the 89 percent of surveyed executives who reported they have a plan in action or in development to move to a lower-carbon future. When asked what steps they are taking toward the energy transition, the top answers among oil and gas executives were developing low-carbon products such as “green” gas and replacing hydrocarbons with cleaner fuels or renewables in operational processes. Several international oil companies have announced plans to reduce scope 1, 2, and 3 emissions, and are specifically targeting net-zero emissions by 2050.19 Meanwhile, in the utilities sector, the increasing economic attractiveness of and customer preference for low-carbon fuel sources suggest these longer-term low-carbon strategies will likely endure even given short-term hurdles.

Increasing operational energy efficiency

Energy efficiency is a key element of most of our survey respondents’ low-carbon transition strategies, demonstrating the progress already achieved in this channel. For example, policies geared toward energy efficiency have motivated utilities across the United States to implement energy efficiency measures and tracking. And corporations have increased monitoring of energy usage, upgraded key equipment, and installed building automation systems to control lighting and heating, ventilation, and air conditioning systems. Companies such as Carrier Corporation have reportedly focused on this area. In 2019, Carrier’s Florida headquarters became the first commercial building in the state to receive Leadership in Energy and Environmental Design (LEED) platinum v4 certification.20 In addition, Carrier has instituted regular tracking of estimated greenhouse gas emissions avoided at customer sites around the world as a result of installing high-efficiency air conditioning, heating, and refrigeration systems.21

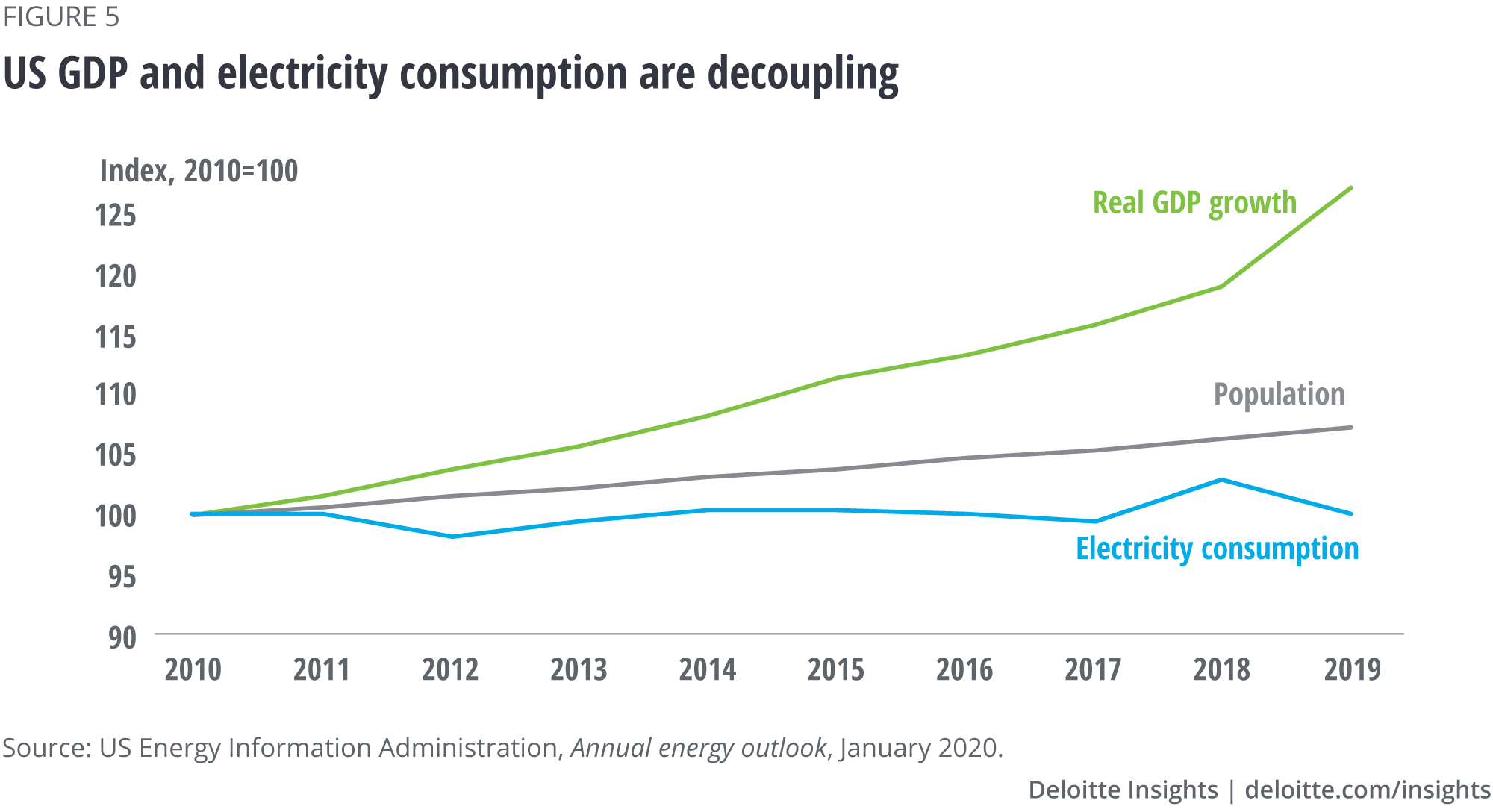

Such measures have resulted in lower energy intensity even amid economic growth. In the United States, for instance, GDP expanded by 25 percent over the past decade, while primary energy demand grew only by 6.6 percent (figure 5).22

In the oil and gas sector, many smaller US oil and gas companies have been tracking operational and efficiency targets for some time. The majority of our surveyed executives at small oil and gas companies (with revenues between US$100 million and US$500 million) indicated that leveraging data and analytics for greater predictability in operations was the key enabler to their sustainability strategies. The larger oil and gas companies in the survey also indicated that energy efficiency was a top priority (figure 6).

Efficiency gains are also apparent in the refining sector, largely due to efficient energy handling and steam generation, along with a transition toward cleaner fuels such as natural gas. Refineries have increased efficiency through debottlenecking measures such as equipment upgrades and process improvements. In addition, a shift toward large refining-chemical projects over small and energy-inefficient complexes has helped reduce refinery greenhouse gas emissions. Chemical company executives in our survey also cited energy efficiency equipment and processes as a key component in advancing decarbonization plans and reducing costs.

High-efficiency electric motors are also a key component to increasing energy efficiency. Currently, electric motors account for 45 percent of global electrical energy consumption, and industrial electric motors are expected to account for 30 percent growth in electricity demand in this segment by 2040.23 Two-thirds of this usage comes from industrial applications, such as motors on conveyor belts, pumps, elevators, HVAC systems, and machine tools. The oil and gas industry is also a significant end market for high-efficiency electric motors.24

Progress along the energy efficiency channel is expected to continue strongly even in the downturn. While some spending on retrofits and new equipment could be delayed in the short term, the larger trend toward energy efficiency is expected to continue, particularly as companies expect benefits such as cost reductions.

Identifying new investment opportunities

Over the past decade, investment in clean energy globally has risen from US$195 billion to US$363 billion.25

Over the past decade, global investment in clean energy globally has nearly doubled.

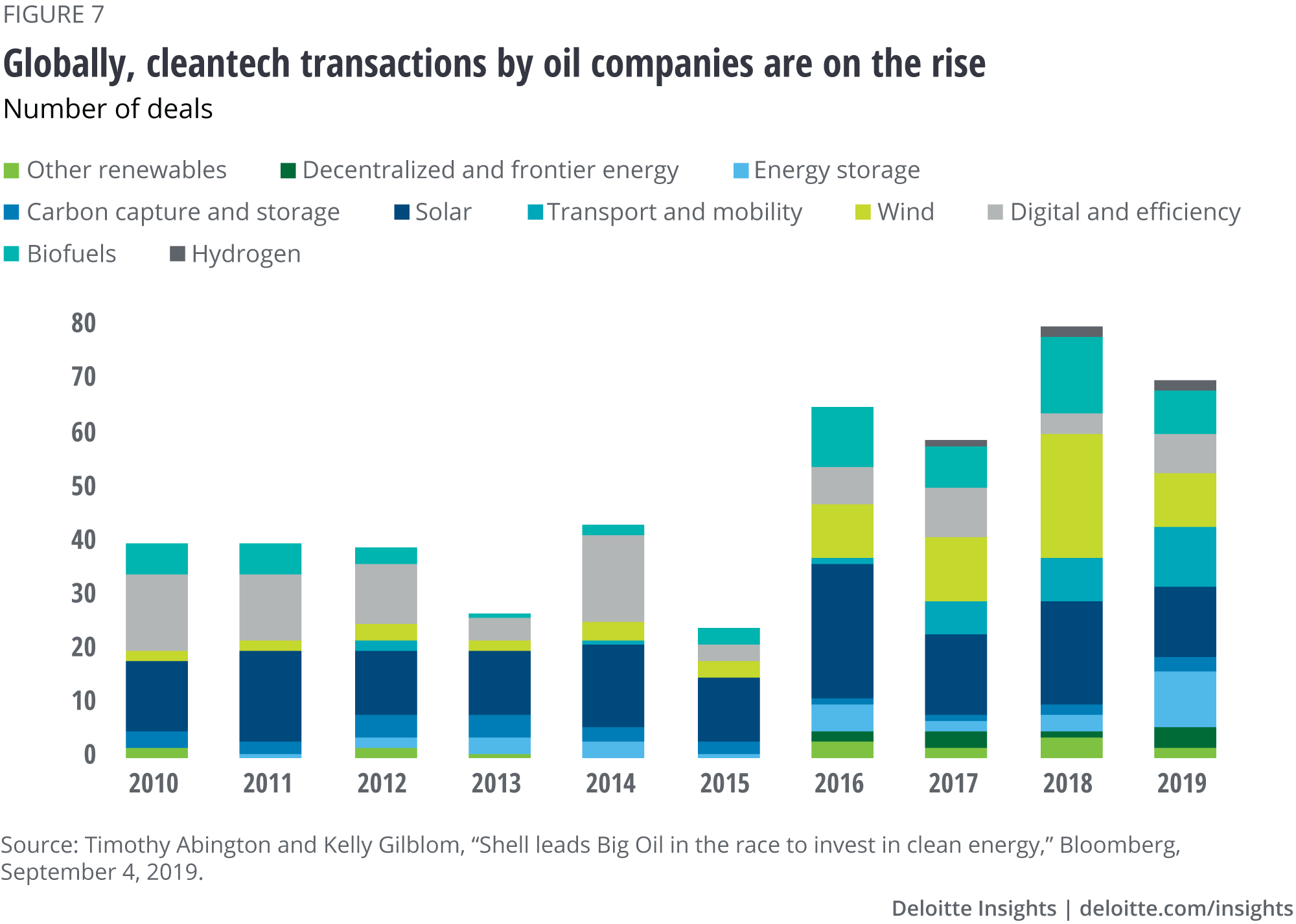

One aspect of this investment in new technology is the venture capital investments that international oil and gas companies are making in clean energy technologies. The larger companies are building their portfolios in areas such as clean energy and EV charging; many have also formed venture capital arms and pursued partnerships and acquisitions in the clean tech space. As shown in figure 7, the volume of transactions in clean energy concluded by large oil and gas companies across the globe has almost doubled over the past decade.26 While the deal volume by these companies in the solar and wind industries has begun to decline, growth in battery storage picked up sharply in 2019. Investments in EV charging have also increased from 2017, as have investments in biofuels and hydrogen.27

These investments have been important to oil and gas companies both for improving their clean tech credentials and for diversifying their portfolios. International oil and gas companies are currently investing between 1–2 percent28 of their capex on these investments, and prior to the current economic downturn, this figure was expected to rise. Forty-six percent of the oil and gas executives we surveyed said that a key step in their strategy for a low-carbon future included investment in areas outside their core business. Early indications are that during this period of low oil prices, many of the larger oil companies are staying the course with their investments, as they did in past downturns. For those companies where offshore wind or solar have already become a substantial business area, these assets are offering a welcome balance to the current oil price volatility. And some oil company executives have reiterated the importance of leadership on environmental initiatives and CO2 emission reduction even amid the immediate downturn.29

The other important type of investment in clean technologies is investments in new equipment to improve operations. The chemical company executives in our survey, for instance, cited investments in renewable energy when asked how they had achieved lower carbon emissions and lower energy use, while manufacturing executives indicated technologies that increase efficiency as a key area for investment. An example of such investments is smarter building and factory infrastructure combined with connected building management for heating, cooling, and lighting systems. Survey respondents also cited technologies to reduce landfill waste by enabling better capabilities for waste management and emissions controls. It is likely that investment in these new areas could be delayed by the necessity of short-term spending cuts to address crisis recovery efforts, but because such investments help increase operational efficiency and reduce carbon emissions, they are unlikely to be canceled completely even if there are short-term delays.

Deploying new technologies

The utility industry is driving and influencing technological advances. Utilities are increasingly deploying front-of-the-meter energy storage assets to smooth renewable energy integration and deliver additional grid services such as regulation. As of December 2019, 982.3 megawatts (MW) of large-scale battery storage capacity were in operation, and about 3616.4 MW of capacity were planned to become operational by 2023,30 although some analysts are expecting a 20 percent drop in global storage deployments in 2020 due to the pandemic and economic recession.31 In the last two years, renewables paired with large-scale batteries have become economically viable, and solar-plus-storage projects have underbid natural gas–fired plants to win power delivery contracts in certain US states.

The innovation shown in building new supply chains and altering production lines to address COVID-19–related shortages augurs well for the agility and innovation needed to decarbonize operations in the longer term

Utilities and governments are also exploring longer-duration storage technologies that meet cost and performance targets to achieve increasingly ambitious clean energy goals. The US Department of Energy directed US$30 million into research in this field in 2018, and the California Energy Commission recently solicited US$11 million for longer-duration storage projects.32 Some of these promising storage technologies are flow batteries, compressed air systems, liquefied air systems, flywheels, thermal storage, and stacked blocks.33 And storage isn’t the whole story: Utilities are deploying other technologies to add the flexibility, reliability, and resilience needed to operate grids with higher volumes of variable renewables. These include advanced analytics, artificial intelligence (AI), automation, cloud, blockchain, drones, advanced weather forecasting, and geospatial technologies.

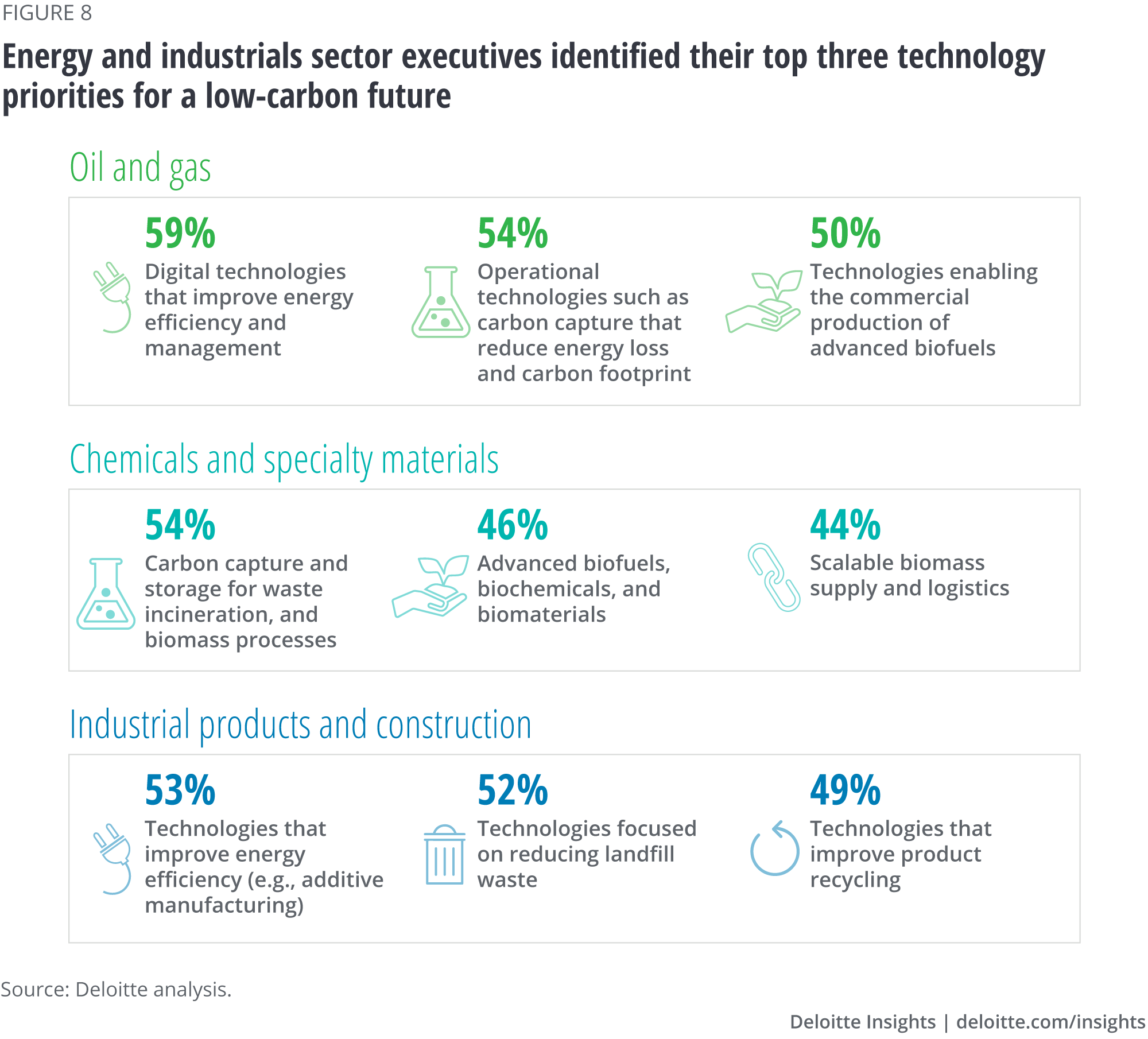

When oil and gas company executives were asked which new technologies were needed to effectively transition to a lower-carbon future, 59 percent of our respondents cited digital technology to improve energy efficiency and management as their first choice (figure 8). Other key technologies identified included carbon-capture-utilization-and-storage (CCUS) and other carbon-reducing technologies, as well as technologies enabling the production of advanced biofuels. Interestingly, hydrogen technologies for transport and other applications were the lowest-ranked. Top accelerators to achieving decarbonization goals among oil and gas respondents included partnerships (including with academia and niche tech firms), mergers and acquisitions, and organic investments.

New process technologies are also likely to change the chemical industry landscape by 2025. Among these, crude-oil-to-chemicals (COTC) technology has high potential, as it enables direct production of chemicals from crude oil with yields greater than 40 percent (compared to current refineries which convert just 5–20 percent of feedstock to petrochemicals).34 Many such COTC complexes are being built in China and the Middle East, mostly by large integrated oil and gas companies, indicating that chemical production may be expanding to the refinery scale.

Industrial manufacturing is also considered a key enabler of the energy transition, as this sector produces the technologies and products that make a lower-carbon future possible: higher-capacity wind turbines, more efficient solar panels, longer-duration batteries, EV components, and other products critical to the growth of a lower-carbon ecosystem. For example, Republic Services has partnered with a commercial vehicle manufacturer to develop a fully electric collection truck.35 The COVID-19 crisis has shown how innovative manufacturers can be in response to the current crisis. Small clothing manufacturers have retooled to produce hospital gowns and automotive manufacturers have altered their production lines to produce ventilators. Companies have quickly reoriented their supply chains away from restricted areas and have found new ways to move goods and products. This is the kind of agility that will likely be needed to accelerate the energy transition as well.

Across all sectors, immediate spending on new technologies may be deprioritized as companies reduce short-term discretionary spending and reevaluate supply chains in light of the pandemic. Many manufacturing companies are reprioritizing their short-term spending to assist in the current crisis. Moreover, the current market situation could delay commercialization of new technologies due to financing constraints and short-term hurdles. However, while a short-term decrease in spending on new technologies is expected, there are at least two reasons why progress should continue in the new technologies channel in the long term. First, the cost of these new technologies has continued to decline, making them more widely available. And second, they bring tangible benefits such as increased operational efficiency and the potential for cost reductions.

Adjusting to new policy mandates

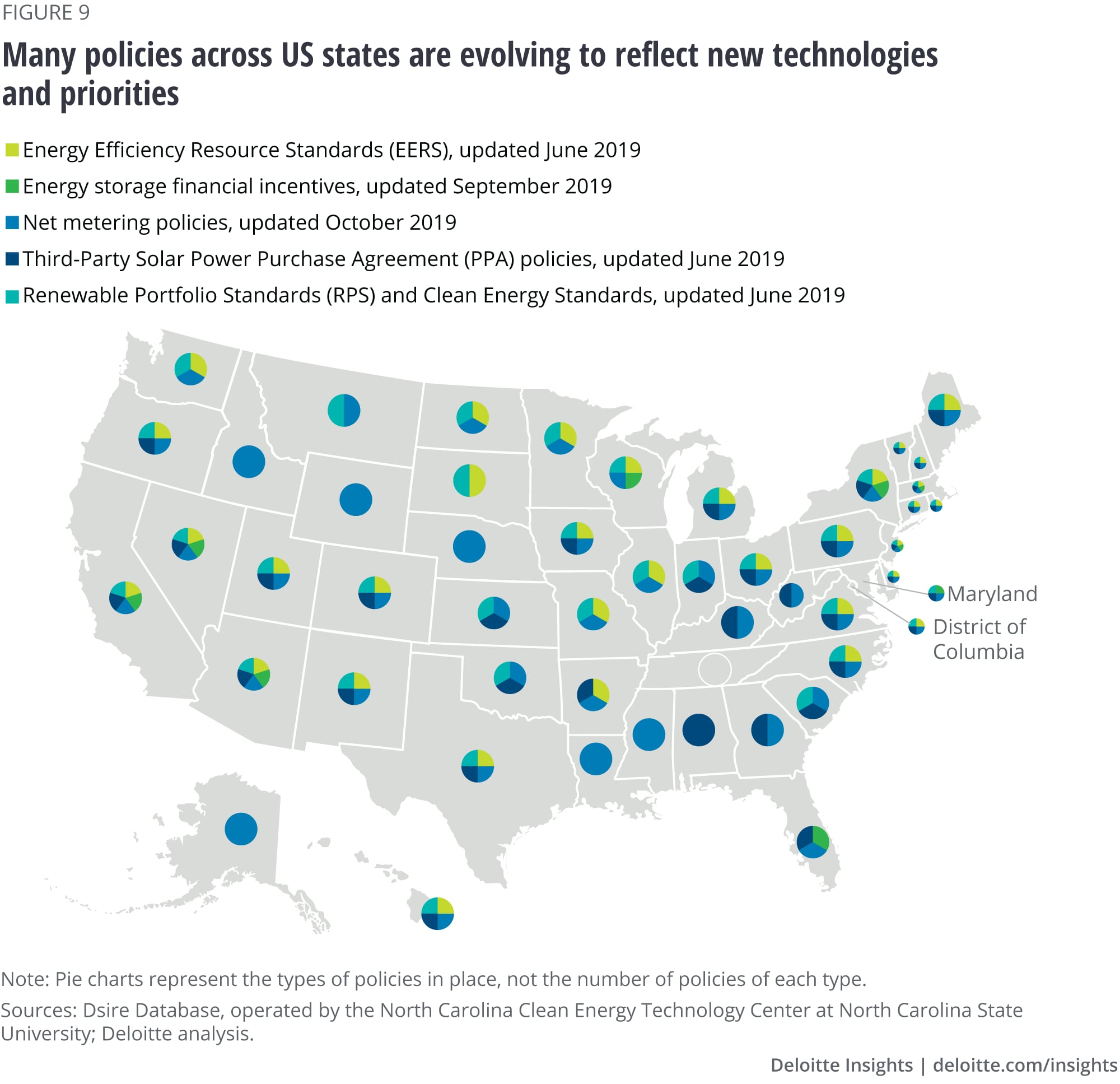

Policies at both the state and federal level have boosted the use of renewables in the US power sector. At the federal level, renewable energy and EV tax credits have played a key role, while states have introduced many policies that support renewable energy and energy efficiency (figure 9), with renewable portfolio standards (RPS) and energy efficiency resource standards (EERS) among the most effective. The phaseout of the production tax credit (PTC) for wind projects that begin construction after 2020 and the reduction in the investment tax credit (ITC) for solar projects may soften demand slightly. But rapidly falling costs and rising customer demand will likely ensure future renewables growth. More flexible regulatory initiatives that could help enable the energy transition are emerging, such as performance-based ratemaking, time-of-use pricing, green tariffs, rate recovery for EV infrastructure investment, and evolving markets for distributed energy resource owners to aggregate and sell surplus energy to peers.

Among our surveyed oil and gas executives, “regulatory mandates including policy incentives” was seen as a top driver for the energy transition. Many regulations affect the markets for oil and gas as opposed to affecting oil and gas companies themselves. For example, in many countries, incentives favoring EVs seem to have spurred EV sales since 2016, potentially softening refined product demand in the longer term. In the EU, airlines are required to monitor carbon emissions from flights, and there is discussion of adjusting a carbon pricing mechanism for aviation, both of which could eventually build demand for aviation biofuels. In parts of the United Kingdom and the United States, legislation is being passed to ban new natural gas hookups for new homes and businesses. The impact of all these policy measures could slow demand growth for oil and gas in the longer term. However, the March 2020 decision by the US Environmental Protection Agency to roll back fuel economy standards, though still in litigation, could boost gasoline demand in the United States.

Policy has proven an effective tool in curbing carbon emissions, and this policy focus is expected to continue in both the short and longer term, particularly in areas such as Europe, China, and certain US states where policy has already laid a strong foundation for the energy transition. However, there are indicators to watch as to how policy tools will be deployed during and immediately after the COVID-19 crisis. First, priority may be given to economic stimulus and social safety nets, potentially delaying decarbonization initiatives. For example, the planned November Conference of Parties (COP 26) was canceled due to lack of time for participants to prepare given their focus on near-term issues. Similarly, because emissions are declining due to the economic slowdown, this could prompt policymakers to loosen policies targeting emissions.

That said, it is possible that advances in the energy transition may be made even amid the downturn. For example, governments may use low oil prices to increase fuel taxes at the pump, which could curtail refined product demand. Similarly, European countries are discussing the use of “green” stimulus packages to help address the current economic crisis.36

Managing consumer and stakeholder expectations

Customers now perceive that not all energy molecules are the same, and many are showing a growing preference for “green” energy, in power and in oil and gas. This has led many companies across various sectors to differentiate their products and change their production processes where possible. A majority of power executives polled reported their organization has committed to providing more electricity sourced from renewables to their customers. Demand for clean energy is rising fast as corporations boost renewable procurement and carbon emission reduction targets and realize cost savings on wind and solar, even with the PTC and ITC phasedown. This is evident in the 2019 increase of power purchase agreements for renewable energy signed by corporate consumers: 14 GW of bilateral renewables PPA in 2019, up from 8.5 GW in 2018 (figure 10).37

Many shareholders and investors have begun to apply pressure on companies to focus on lower-carbon operations and curtail carbon emissions by reducing their carbon footprint and reducing reliance on fossil fuels. BlackRock’s January 2020 letter to clients emphasizing the growing impact of sustainability on investment returns and outlining initiatives to increase their focus on sustainability helped set a broader tone underlining the attractiveness of low-carbon industries and businesses.38 And a growing investor preference for sustainable companies and sustainability funds was already evident even before this announcement.

Oil and gas company executives are well aware of this market sentiment. Among the CEOs we surveyed, 68 percent indicated that the key component of their low-carbon strategy was a focus on low-carbon fuels (though that also includes natural gas). Oil and gas executives surveyed identified “consumer support for reducing carbon emissions” as one of the top drivers for the industry’s transition toward a sustainable, low-carbon future.

But if stakeholders, particularly investors, reduce their exposure to oil and gas companies, there could be two key effects. The first effect is reduction in equity and debt available for projects, leading to capital constraints for the industry. The second is concern for stranded assets, a risk that could be higher for long-lived conventional assets such as offshore oil and gas platforms. This concern has raised interest in a more asset-light strategy among some energy companies. Stranded assets are a growing concern for power utilities as well, which are grappling with decommissioning coal plants, some nuclear plants, and even gas plants too old to compete with renewables.

The long-term focus on reducing carbon emissions does not seem to have been reversed by the current economic upheaval. In fact, while environmental, social, and governance equity funds saw losses in the month from February 12 to March 12, 2020, their losses were less severe than those of conventional peers, and they were overrepresented in the top quartiles of their peer groups in terms of performance.39 In addition, the renewables market has experienced a short-term boost, as volatility in other commodity markets seems to have made renewables more attractive due to their comparatively low-risk, stable yield. So, while the economic downturn could potentially reduce funding for lower-carbon projects and investments, customer and shareholder focus on the energy transition as a way to address environmental issues may continue.

Progress continues along the six channels toward energy transition

The energy transition is expected to remain a strategic priority for energy and industrials companies in the longer term (figure 11), as is clear from our survey results detailing the scale of strategy plans in place across these sectors. From a company perspective, decarbonization efforts can deliver benefits such as reduced costs, enhanced customer loyalty, and increased competitiveness. The strong board-level support for the energy transition illustrates the commitment to these strategies: As mentioned above, more than 50 percent of the executives we surveyed reported that meeting reduction targets affects board and/or executive compensation. In addition, 71 percent of the CEOs surveyed said that the key benefit achieved from their plans for a lower-carbon future was to improve the environment. These findings suggest that company leaders are keenly aware of market sentiment toward addressing environmental issues through the energy transition.

An important question is whether company executives will be able to maintain the momentum of their low-carbon plans in the short term, given the difficult questions facing management about immediate priorities. Prior to the economic downturn, companies were generally making progress across all channels, but clearly some channels could now move more slowly than others. However, the longer-term commitment to addressing carbon emissions and expediting the energy transition is unlikely to be reversed, particularly in areas where substantial progress has already been made. For example, the power and utilities sector will likely continue to move toward decarbonization as the costs for renewable energy decline further. That means utility commercial and industrial customers could be less reliant on fossil fuels as the electricity supply is decarbonized. So, while customer and stakeholder focus on the energy transition may be overshadowed by efforts to cope with the immediate crisis, in the longer term, attention on decarbonization is not likely to diminish.

Another key question is whether the recovery could lead to a “new normal” that is less carbon-intensive and builds on lessons learned during the COVID-19 crisis. In particular, questions could be asked about whether the current crisis could even accelerate the transition in some channels:

- Will the innovation which manufacturers and energy companies demonstrated during the COVID-19 crisis become part of a new normal in which companies are able to build new supply chains and alter their manufacturing lines with remarkable agility? Will processes such as additive manufacturing that have enabled some of this change continue to grow rapidly, conferring benefits such as less energy-intensive supply chains?

- How enduring will be the boost that renewables have received during the current downturn? As overall energy demand declines in many hard-hit countries, these resources are typically accounting for a larger portion of overall generation dispatched in systems with significant access to renewables, since renewables are generally dispatched first due to their low marginal cost. This provides an unexpected opportunity to test the viability of systems running with unprecedented levels of renewables in the generation mix.40

- Will there be lingering reductions in gasoline and diesel demand? The economic crisis and physical distancing practices reduced traffic levels in affected countries by as much as 40–50 percent. 41 Will commuting rebound to previous levels as people return to work, or might we see a lower level of light vehicle traffic softening refined product demand?

Modest change in any of the above areas would have a compounding effect in all six channels of the energy transition. Many companies are already exploring the technologies and collaboration needed to move forward. First, digital technologies were cited by a majority of our surveyed executives as a key enabler of progress in the energy transition. These technologies can help forward energy efficiency goals by enabling remote working and by integrating smart devices that allow customers to moderate their electricity usage. The use of connected technologies for energy management systems in buildings is also expected to increase. A major focus could be leveraging data and analytics to enable greater predictability in operations; another might be implementing technologies for better sensing and forecasting the market environment.

Another enabler of the energy transition—which has been important in the current downturn—is increased collaboration with parties outside a company’s core business. Survey respondents highlighted collaboration with niche technology firms and academia, as well as developing partnerships and joint ventures, as important efforts in their low-carbon strategies. And as we move beyond the crisis, there may be an opportunity for partnering with large commercial customers, in the power sector in particular. As companies move to asset-light portfolios and diversify their activities, mergers and acquisitions are also expected to be important.

The COVID-19 crisis seems to have highlighted many of the attributes that could accelerate the energy transition: reevaluating supply chains, collaborating within and across sectors, and pioneering capex-light scalable solutions with digital technologies and analytics at the core. The coming months will likely show how enduring these innovations may prove.