{kind=link}

{kind=link}

{kind=link}

Japan economic outlook, July 2023 has been saved

Cover image by: Jaime Austin

Japan’s economy continues to post economic gains, though the pace of growth remains relatively slow. Real GDP is still below 2019 levels and was up by just 1.8% from a year earlier in Q1.1 Higher-frequency indicators, such as the purchasing managers’ indices, show a manufacturing sector that has either plateaued or gone down over Q2, while the services sector continues to recover from pandemic-related weaknesses.2 Pent-up demand and a highly accommodative central bank should keep the economy moving in the right direction. However, the pace of growth will likely be restrained by relatively high inflation and weak economy across the rest of the world.

The Bank of Japan (BoJ) has continued to maintain its accommodative monetary policy stance despite high inflation. This has meant leaving its policy rate at –0.1% and holding the yield for the 10-year government bond near zero percent.3 We expected the latter—called yield curve control—to be abandoned before the end of this summer. However, recent comments from Governor Ueda suggest that any softening of its yield curve control will be put off until fall at the earliest. The governor indicated that he wanted to be more confident that underlying inflation will not come down on its own before tightening the policy.4

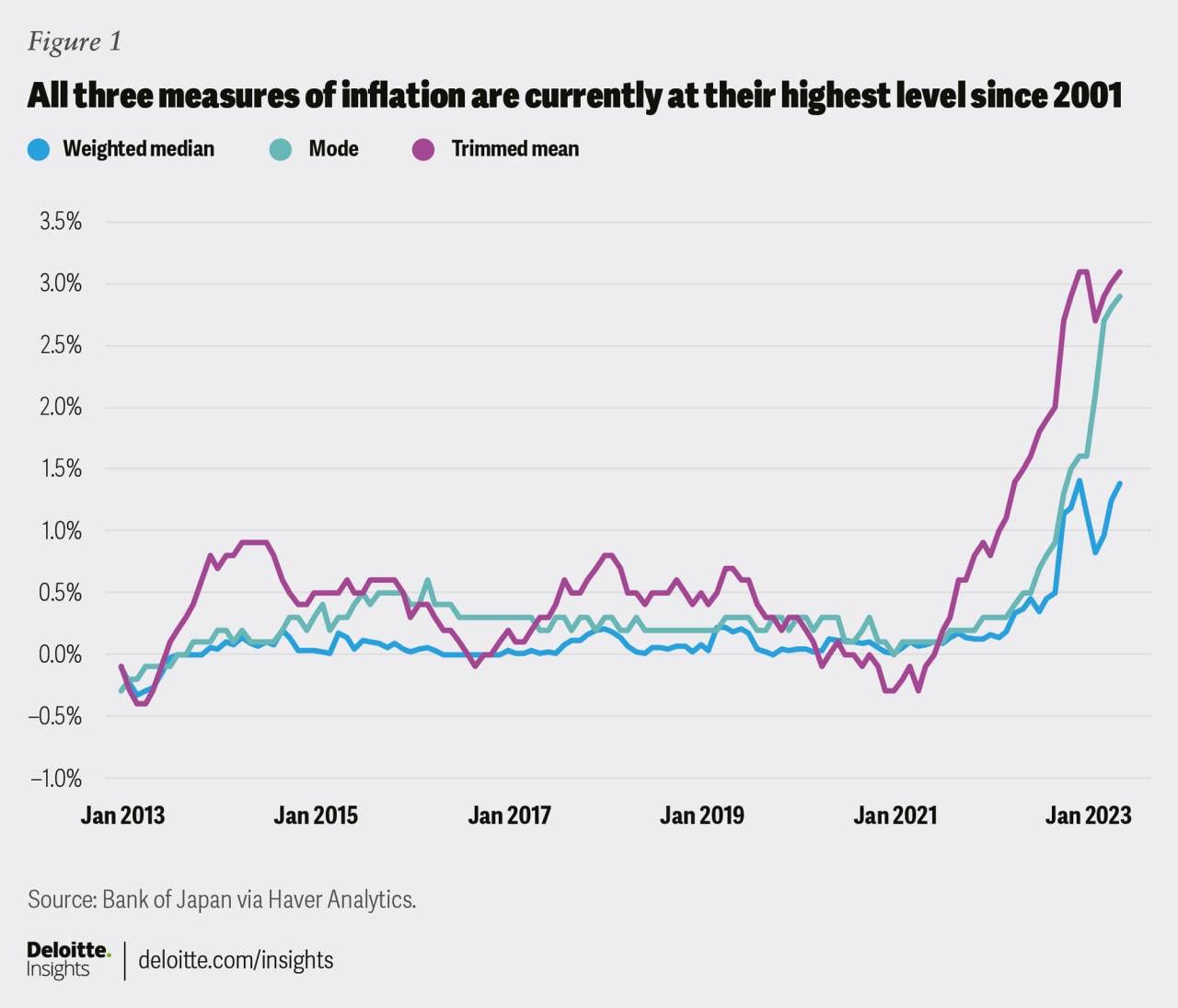

The BoJ generally uses three measures of underlying inflation: weighted median, trimmed mean, and mode. Weighted median inflation was up just 1.4% in May from a year earlier, which has allowed the governor to claim that underlying inflation is still running below the central bank’s 2% target.5 However, trimmed mean and modal inflation were 3.1% and 2.9%, respectively. When rounded to the tenths place, all three measures are at their highest levels since data became available in 2001 (figure 1).

So far, there is scant evidence that inflation is turning around on its own. Using the Western core price index, which excludes food, nonalcoholic beverages, and energy, we can see that prices are up 2.7% from a year ago.6 Year-ago measures can be misleading as the economy was considerably weaker last year, while pandemic restrictions were still periodically in effect. However, on an annualized month-to-month basis, Western core prices have exceeded 2% for the last four months. None of this suggests that inflation is on the cusp of going down.

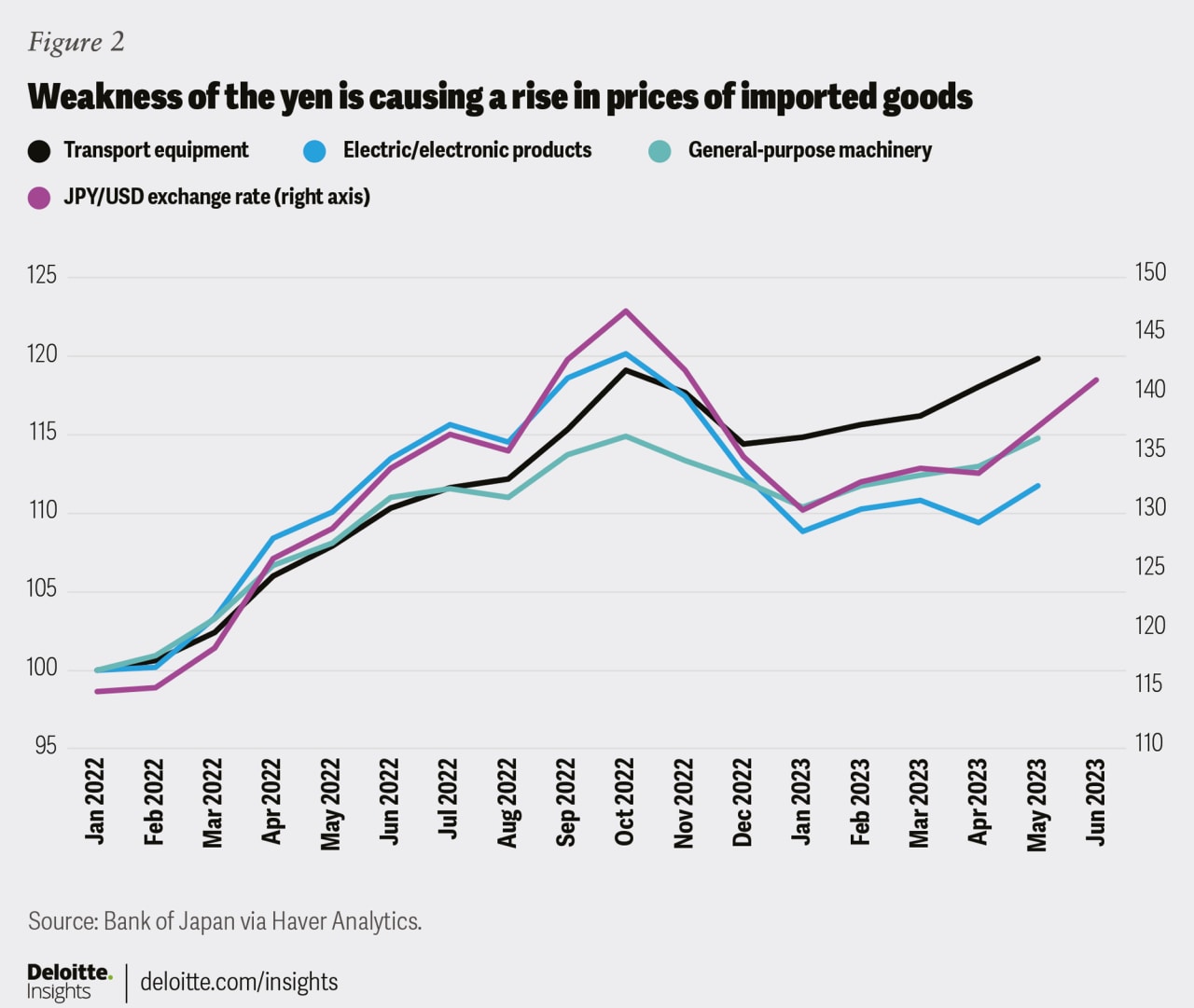

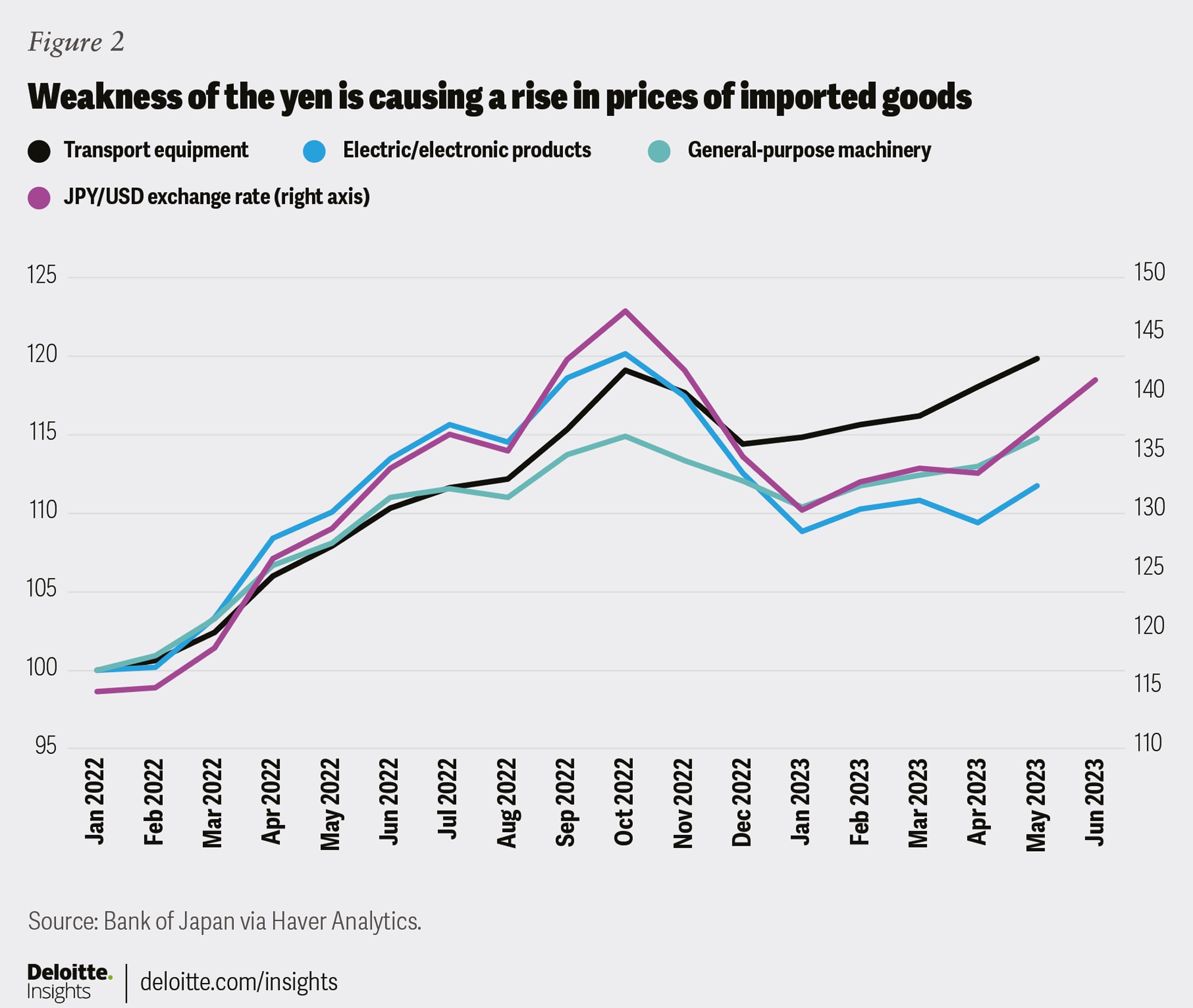

Inflation drivers do not appear to be waning either. Although energy prices have declined, other commodity prices continue to grow relatively quickly. Producer prices for manufactured goods were still up 4.5% from a year earlier in March.7 Plus, the yen has been depreciating again this year, as foreign central banks become more hawkish while the Bank of Japan remains dovish. Import prices were down 5.4% from a year ago in May, but they have clearly jumped higher this year once energy has been excluded.8 For example, the prices of imported transportation equipment, general-purpose machinery, and electronic products fell between October 2022 and January 2023—but these have started to rise since then. This import-price pattern closely tracks the value of the yen, and any additional weakness in the currency will keep upward pressure on prices, especially in the goods sector (figure 2).

The outlook for underlying consumer demand remains mixed, which buys the BoJ some time to keep its monetary policy stance. Some of the data on consumers looks weak. For example, spending per household was down 0.5% in April from a year earlier. However, the consumption activity index from the BoJ was up 6.9% over the same period. Plus, retail sales were up 5.9% year over year in May.9 Even after removing inflation from the equation, the latter two measures of consumer spending are rising relatively strongly.

It is also possible that consumer spending will strengthen from here. Wages for numerous Japanese workers are determined every April during the annual shunto. This year’s wage negotiations yielded a lofty 3.7% increase for workers at large firms.10 However, contractual wage growth for all workers in May was just 1.7% from a year ago. It may take a few more months for the announced wage gains to materialize in the data. But the relatively slow growth in May raises concerns that actual wage gains are well below those announced.

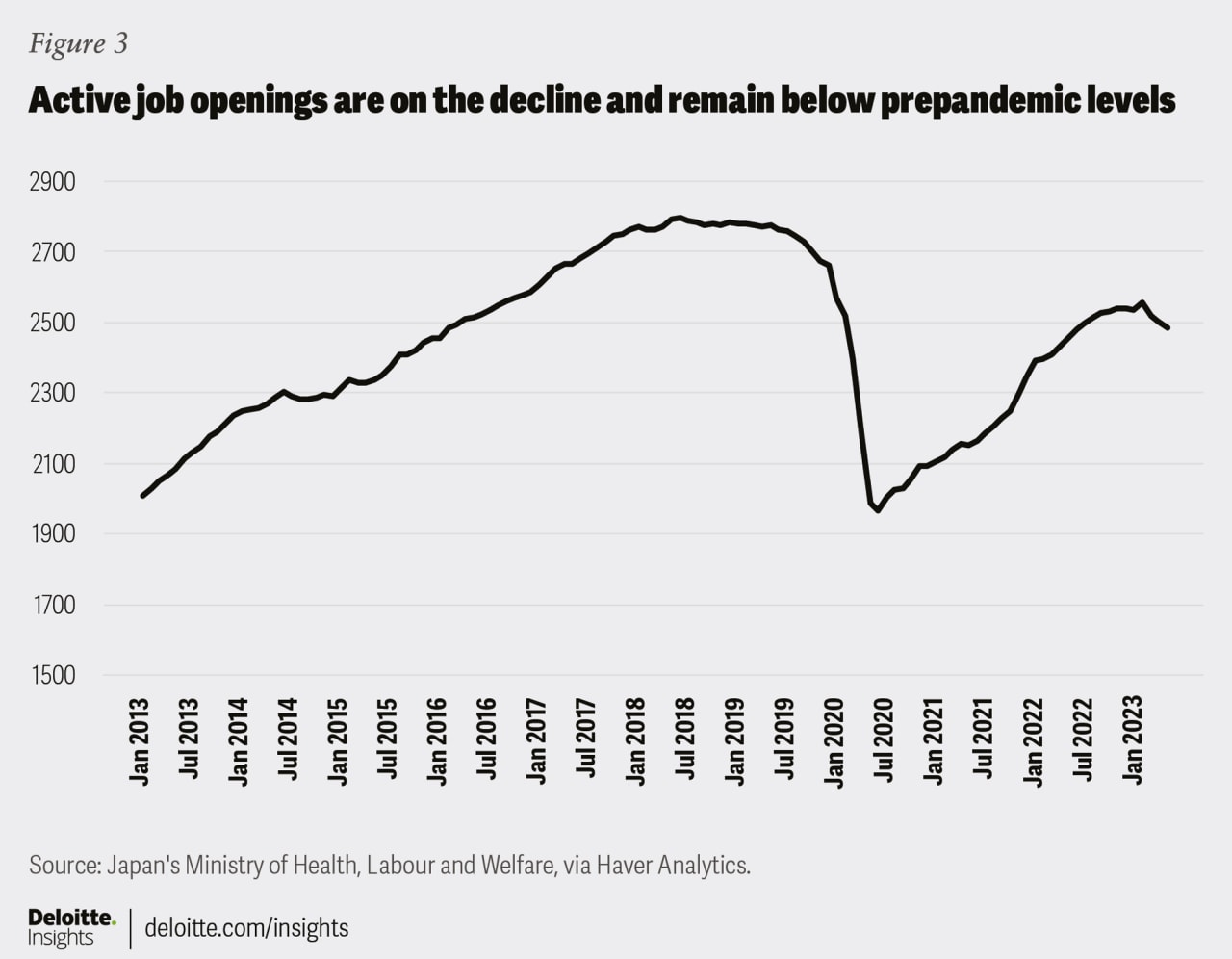

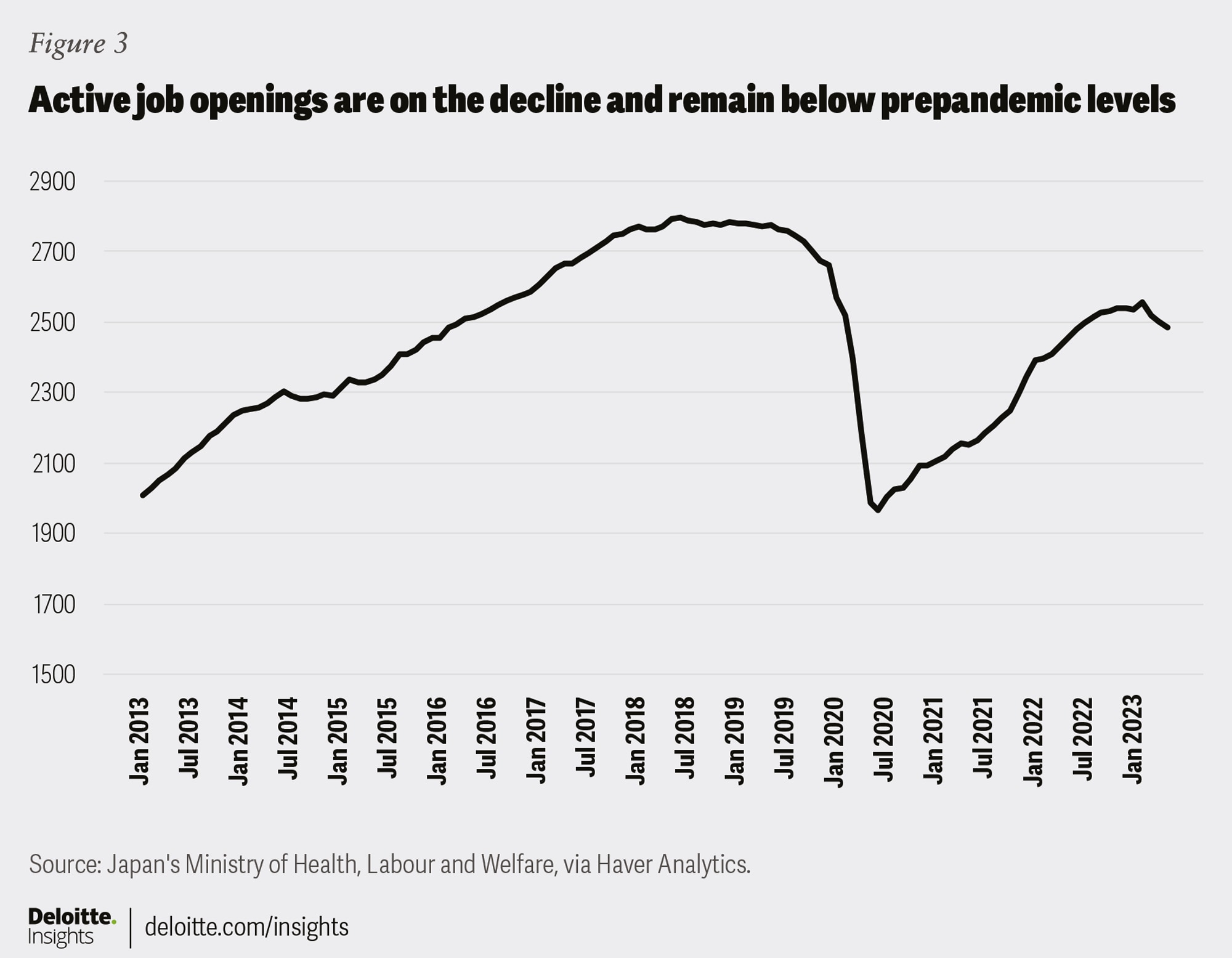

In addition, any spike in wage growth may ultimately prove to be short-lived. For one, the number of active job openings is declining and remains well below prepandemic levels (figure 3). Although the unemployment rate—at 2.6%—is low by international standards, it remains higher than at any point in 2018 or 2019. The higher unemployment rate is largely due to an increase in labor-force participation rather than a decrease in employment. Female participation in the labor force continues to grow, and older-age cohorts have mostly remained in the workforce, unlike what has been seen in other developed economies. In addition, the number of foreign workers in Japan reached a record high in 2022.11 If such gains in the labor force ultimately dampen wage growth, the BoJ would have little incentive to tighten its monetary policy.

Japan’s manufacturing sector has largely benefitted from a weak yen, which has made exports more competitive. In October 2022, goods exports were more than 25% higher than a year earlier.12 Since then, the value of exports came down as the yen appreciated and the global economy weakened. Although goods exports were lower in May than a year before, they have grown 1.8% since January. This gain coincides with renewed weakness in the exchange rate. As the BoJ maintains its dovish policy stance when other major central banks continue to tighten, the yen will likely remain weak and could even depreciate further, which will support export growth.

Some of the more recent strength in exports is due to pent-up demand for automobiles globally. After years of supply chain issues, the auto sector is renormalizing, which is boosting demand for cars and trucks. As a result, motor vehicle exports were up 66.3% from a year earlier in May.13 Other parts of the factory sector are facing headwinds. The first headwind is the general drop in demand for goods. Much of the world is experiencing slower economic growth, which is weighing on demand. Plus, spending growth has been largely concentrated in the services sector rather than tradeable goods.

The semiconductor industry will also act as a headwind. Japan plays a crucial role in the semiconductor supply chain. Semiconductor exports were down 12.1% from a year earlier, while semiconductor machinery exports had fallen 20.2%.14 The outlook is not exactly promising either. According to World Semiconductor Trade Statistics, global semiconductor revenue is expected to fall by double digits this year.15 Although a rebound is expected in 2024, geopolitical tensions and overcapacity in the industry could prevent Japan’s related exports from benefitting.

While Japan’s economy is expected to grow relatively slowly for the rest of the year, there seems to be little risk of a recession. Pent-up consumer demand will keep growth positive. A sizable wage bump from this year’s annual negotiations should give consumers additional purchasing power. The central bank’s accommodative monetary stance remains for now, but it will likely tighten before the end of the year. From there, higher rates, a stronger yen, and weakness abroad will likely restrain the manufacturing and export sectors and keep a lid on GDP growth.

Japan Cabinet Office via Haver Analytics.

View in ArticleS&P Global via Haver Analytics.

View in ArticleBank of Japan via Haver Analytics.

View in ArticleToru Fujioka and Craig Stirling, “Ueda says more confidence in 2024 prices needed for BOJ shift,” Bloomberg, June 28, 2023.

View in ArticleBank of Japan via Haver Analytics.

View in ArticleMinistry of Internal Affairs and Communications via Haver Analytics.

View in ArticleBank of Japan via Haver Analytics.

View in ArticleIbid.

View in ArticleMinistry of Internal Affairs and Communications via Haver Analytics.

View in ArticleKantaro Komiya and Kaori Kaneko, “Japan wages rise after labor talks but weak consumption drags on economy,” Reuters, June 6, 2023.

View in ArticleMinistry of Internal Affairs and Communications via Haver Analytics.

View in ArticleMinistry of Finance via Haver Analytics.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleWorld Semiconductor Trade Statistics (WSTS), “The WSTS has recently published its latest forecast for the semiconductor market, generated in May 2023,” press release, June 6, 2023.

View in ArticleCover image by: Jaime Austin