-q1-2021/figures/7133_Figure1.jpg){kind=link}

-q1-2021/figures/7133_Figure2.jpg){kind=link}

-q1-2021/figures/7133_Figure3.jpg){kind=link}

-q1-2021/figures/7133_Figure4.jpg){kind=link}

-q1-2021/figures/7133_Figure5.jpg){kind=link}

-q1-2021/figures/7133_Figure6.jpg){kind=link}

-q1-2021/figures/7133_Figure7.jpg){kind=link}

-q1-2021/figures/7133_Figure8.jpg){kind=link}

-q1-2021/figures/7133_Figure9.jpg){kind=link}

-q1-2021/figures/7133_Figure10.jpg){kind=link}

-q1-2021/figures/7133_Figure11.jpg){kind=link}

-q1-2021/figures/7133_Figure12.jpg){kind=link}

-q1-2021/figures/7133_Figure13.jpg){kind=link}

-q1-2021/figures/7133_Figure14.jpg){kind=link}

-q1-2021/figures/7133_Figure15.jpg){kind=link}

-q1-2021/figures/7133_Figure16.jpg){kind=link}

-q1-2021/figures/7133_Figure17.jpg){kind=link}

-q1-2021/figures/7133_Figure18.jpg){kind=link}

-q1-2021/figures/7133_Figure19.jpg){kind=link}

-q1-2021/figures/7133_Figure20.jpg){kind=link}

United States Economic Forecast has been saved

Thanks to Lester Gunnion, who played a key role in developing and producing this forecast.

Cover image by: Russell Benfanti

-q1-2021/primary/7133_Banner.jpg/jcr:content/renditions/cq5dam.web.1920.400.jpeg)

Granted, after a grueling year of lockdowns, the light at the end of the tunnel metaphor may be overused. But the accelerating rate of vaccination in the United States suggests that the end of the pandemic—or, at least, of the immediate economic impact of the pandemic—may really be in sight. This raises two questions for our economic forecast. The first is just how fast and how strong the economic recovery will be; the second is what the new normal will look like—and whether the pandemic has done permanent damage to the economy.

The last few months of the pandemic have been the most difficult. One reason is that the weather has kept much of the country from using the outdoors to mitigate the impact of social distancing. That’s psychologically difficult, and it has a direct impact on some economic activity, such as restaurants were forced to curtail their outside operations. On top of that, the early winter saw COVID-19 cases ramp up around the country. And, worse, we learned of the existence of new variants of the SARS-CoV-2 virus that are more contagious than the original. All of this weighed on people—and on economic activity.

However, the vaccination program accelerated as the winter went on. Daily vaccinations averaged about 350,000 doses in early January,1 and the shaky rollout created tremendous frustrations. But by mid-February, the daily rate was up to 1.6 million doses and has since accelerated as vaccine supply has increased and as providers have learned and adjusted their systems to allow for greater transparency and easier use. Bottom line: The immediate goal of resuming economic activity seems to be within reach. Notwithstanding ongoing distribution glitches and frustrations,2 the United States is, in fact, a global leader in the speed of vaccination.3

The rate of vaccinations is consistent with our previous forecasts. Since last spring, we have assumed that vaccine rollout in the United States would be widespread by summer 2021, allowing most normal economic activity to resume at that time. The current acceleration of vaccination suggests that that schedule still holds.

Could the vaccination program be derailed? The most likely stumbling block is a new variant that requires a reformulated vaccine. Imagine having to restart the global vaccine program from the ground up! That’s extremely unlikely.4 But even the need for a revaccination with a “tweaked” serum could delay the economic recovery. Our long slog scenario explores the worst-case possibility—the need for restarting vaccination programs for new variants several times, creating a start-and-stop world in which conditions for a real economic recovery are never fully in place during the five-year forecast horizon.

But that’s not our baseline. Our baseline assumes—without undue optimism, we believe—that enough Americans will be vaccinated by the summer to allow most normal activity to resume.

What happens when things are mostly back to normal? There is a short-term question and a long-term question.

The short-term question involves the pool of savings available to consumers. Households put aside over US$5 trillion in the first three quarters of 2020;5 that’s a huge amount of money that households that have remained employed during the pandemic are likely to want to spend. Pent-up demand for travel, leisure consumption, and recreation services might explode this summer, leading to spot shortages and spikes in prices. Or people might elect to be cautious: Spending could ramp up more slowly as it gradually becomes evident that people can travel, eat at restaurants, and go to theaters without risking illness.

The long-term question is how much permanent economic damage the pandemic has caused. Two key factors will determine the size of this impact:

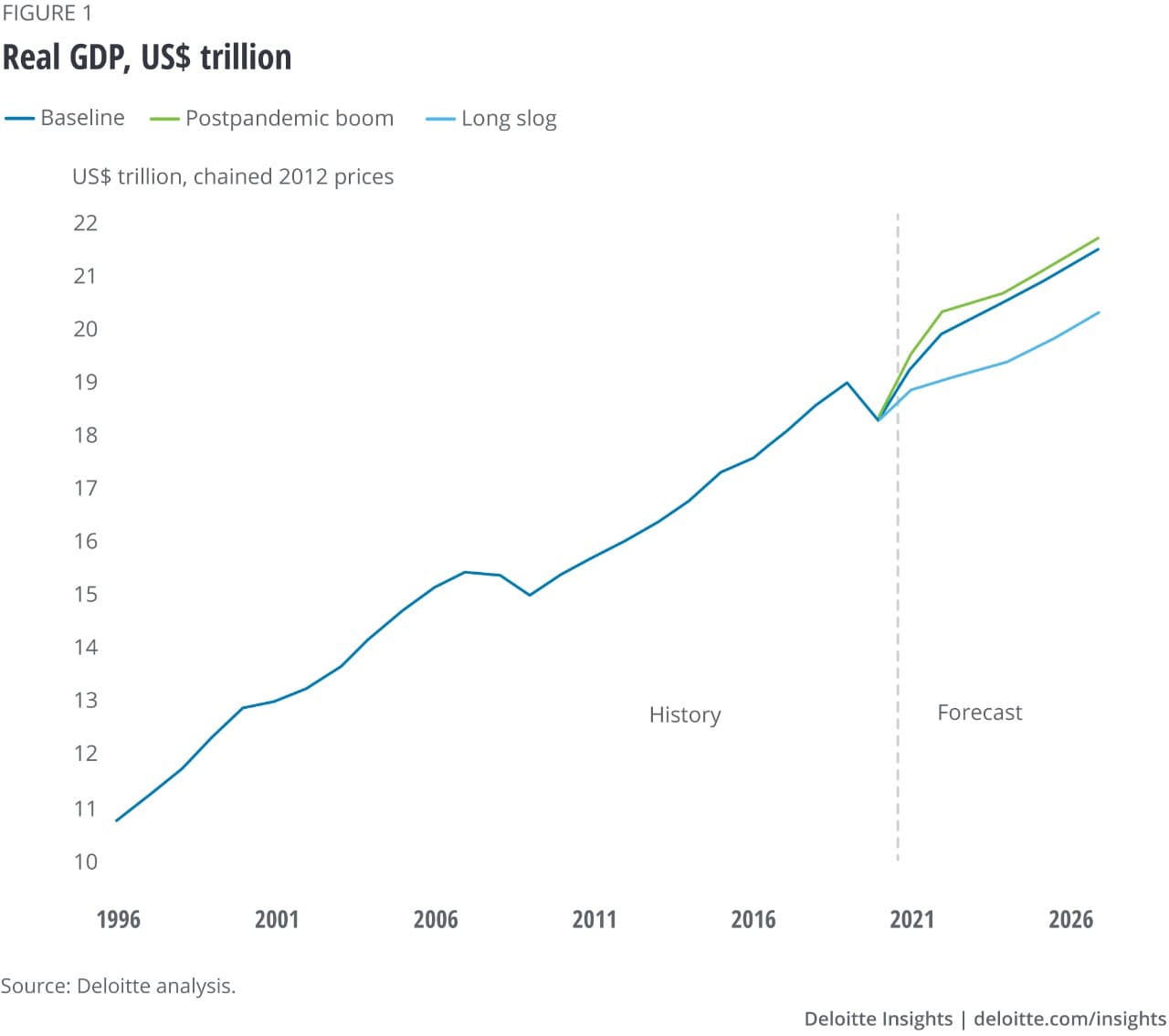

Our baseline scenario assumes some permanent damage, with GDP remaining below the level it would have reached had COVID-19 never materialized. The postpandemic boom scenario anticipates a spike in consumer spending in the summer and fall, boosting GDP and creating inflationary pressures and higher interest rates—which, then, constrain GDP and create a period of slower growth as the economy moves back toward equilibrium that is lower than it would have been had the pandemic not occurred. However, the permanent damage is less in the boom scenario, and by the end of the forecast horizon, the economy is back to where it would have been had the pandemic not happened.

The light at the end of the tunnel is visible even if the metaphor has been too often misused But we must wait to see the actual shape of the economy when we finally emerge from that tunnel.

Baseline (55%): The late-December federal relief package helped to keep the economy together in early 2021. We assume that Congress will pass another aid package by March that will include an extension of the unemployment insurance expansion through September, as well as aid to state and local governments. We therefore see moderate growth in the first half of 2021. While vaccine deployment has been chaotic, people are getting vaccinated, and the federal government is pushing hard to improve distribution and supply more vaccine. We continue to expect vaccinations to reach a significant portion of the public by spring, allowing activity in affected industries to resume. GDP growth is very fast in the second half of 2021, then settles to something closer to the long-term annual trend of 1.5% to 2.0% after that. Employment growth lags GDP growth. Despite this, productivity growth and profits grow more slowly than nominal GDP after 2021, because of the need to write down capital (such as office buildings) that new working conditions have made less productive. Potential GDP remains about 1.4% below the prepandemic trend in 2026.

Postpandemic boom (25%): The relief bills are more effective than expected, allowing GDP growth to pick up early in 2021. Then, as the vaccine rollout reaches a large portion of the population, huge pent-up demand for travel and recreation services pushes GDP above trend. Employment growth is strong, with these sectors mobilizing their low-skilled workforces more quickly than observers expect. Incipient inflation pressures appear, the CPI briefly pushes over 3.0%, and the Fed reacts cautiously, unwinding quantitative easing and raising interest rates faster than in the baseline. GDP returns to the long-run trend by 2023 after a short period of slower growth. And damage to the economy’s long-run capacity proves small, so in 2025 GDP is close to the prepandemic trend.

Long slog (20%): New COVID-19 variants cause cases to spike in the spring even as the vaccine rollout ramps up. States are forced to attempt to again limit economic activity. Schools again go entirely virtual, and some parents leave the labor force to manage their children’s schooling. The cycle of restart attempts and subsequent reclosing continues, limiting the possibility of recovery and eroding trust in institutions. Even later, as treatment improves and businesses again reopen, consumers prefer to stay at home in safety rather than take what they have come to believe are unwarranted risks. Household savings remain high, keeping a lid on aggregate demand. The economic recovery is hesitant, and GDP growth remains relatively slow. As far out as 2026, unemployment remains high, with the level of GDP about 7% below the level it would have reached had the pandemic not occurred.

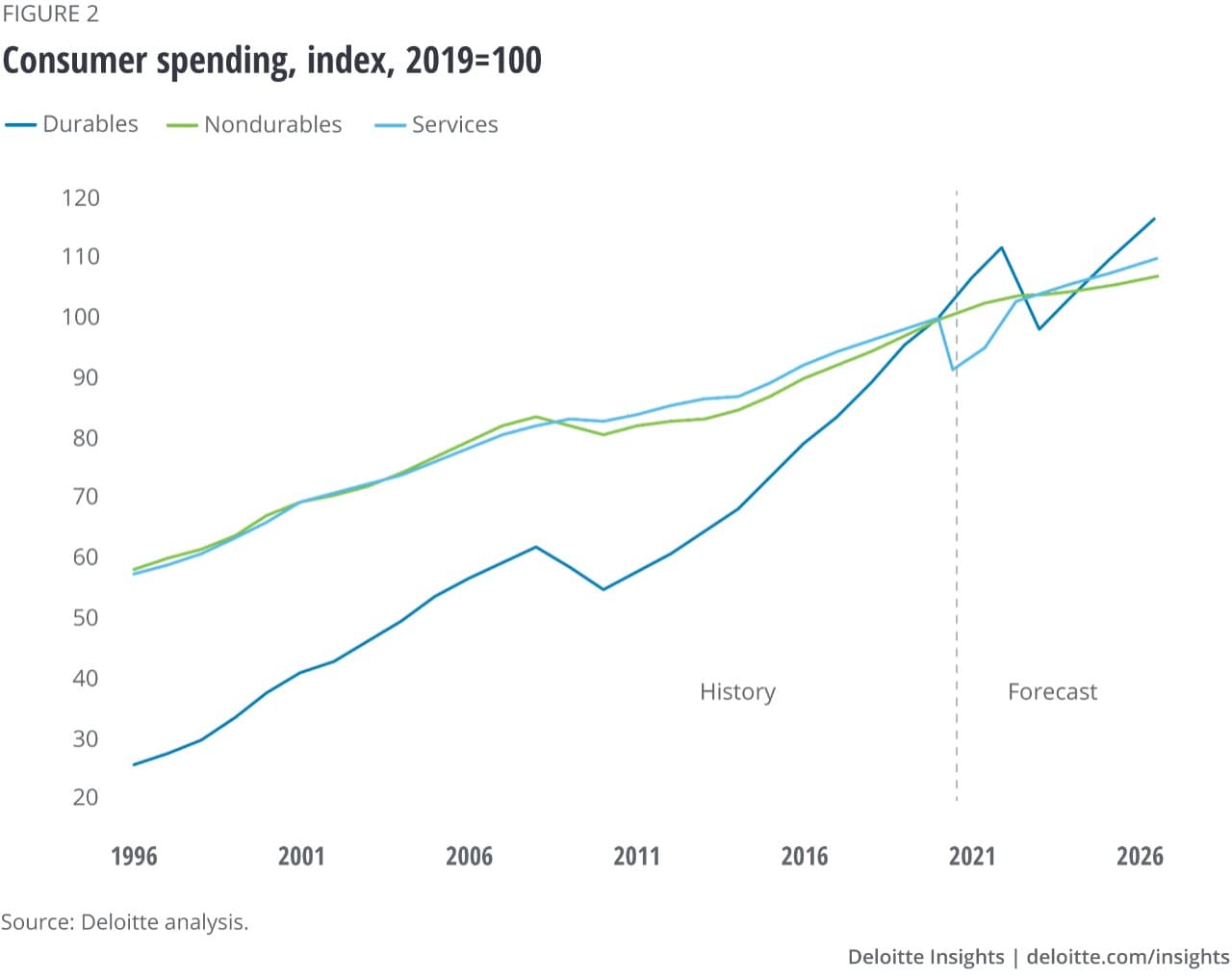

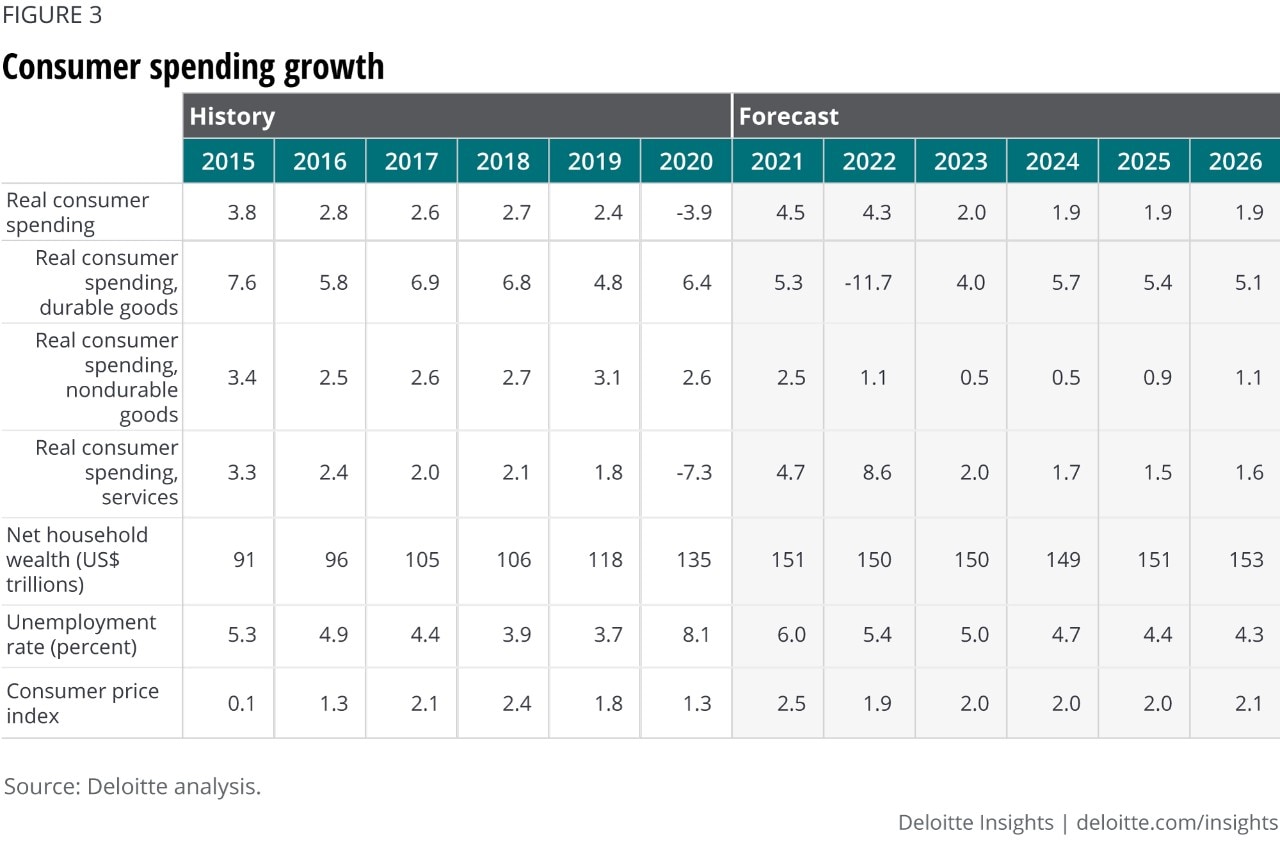

Consumer spending weakened at the start of the winter, reflecting the slowing job market. Distribution of the US$600 stimulus payment may have helped support spending in January, and suggested that more expansive fiscal policy may help support consumer spending through the spring. What was surprising was less the recent weakness than the fact that spending held up so well in the spring and summer. Despite the withdrawal of the US$600 weekly supplement to unemployment insurance at the end of July, and notwithstanding rising cases of COVID-19 across the country, people continued to be willing to spend until November. This is partially because of the massive savings that occurred early in the pandemic, when even the unemployed shifted from spending to saving.7

The pandemic dramatically changed patterns of spending, however. During 2020, real spending on goods grew 3.9%, while real spending on services fell 7.3%. Until medical interventions render COVID-19 considerations moot, consumers are likely to continue to direct spending away from activities perceived as risky—entertainment, food service, accommodation—and toward consumption that can take place in a socially distanced way.

The rollout of vaccinations raises the question of how consumers will behave once the coronavirus is no longer a threat. One possibility, consistent with our baseline, is that consumers will remain wary for some time. This suggests that households will maintain a higher level of savings, and that consumer services spending will recover slowly. Another possibility, shown in our fast-return scenario, sees consumers rapidly resuming their previous spending patterns.

Spending on durable goods has been particularly strong, rising 6.4% in 2020. This poses another problem: Even before a vaccine is widely deployed, consumers may exhaust their demand for durable goods that substitute for services spending. After spending their mostly unused restaurant budget of six months on a home gym, what does a household do with the money ordinarily spent during the next six months? Some suppliers, such as automobile manufacturers, are used to boom-bust cycles in consumer demand; others may experience this for the first time.

In the longer term, we expect the pandemic to exacerbate existing consumer problems. The pandemic has thrown the problem of inequality into sharp relief, straining the budgets and living situations of millions of lower-income households. These are the very people who are less likely to have health insurance—especially after layoffs—and more likely to have health conditions that complicate recovery from infection. And retirement remains a significant issue: Even before the crisis, fewer than four in 10 nonretired adults thought their retirement was on track, with one-quarter of nonretired adults saying they have no retirement savings.8 Low interest rates will worsen Americans’ preparation for retirement, while the stock market boom will have little impact on the balance sheets of most Americans.9

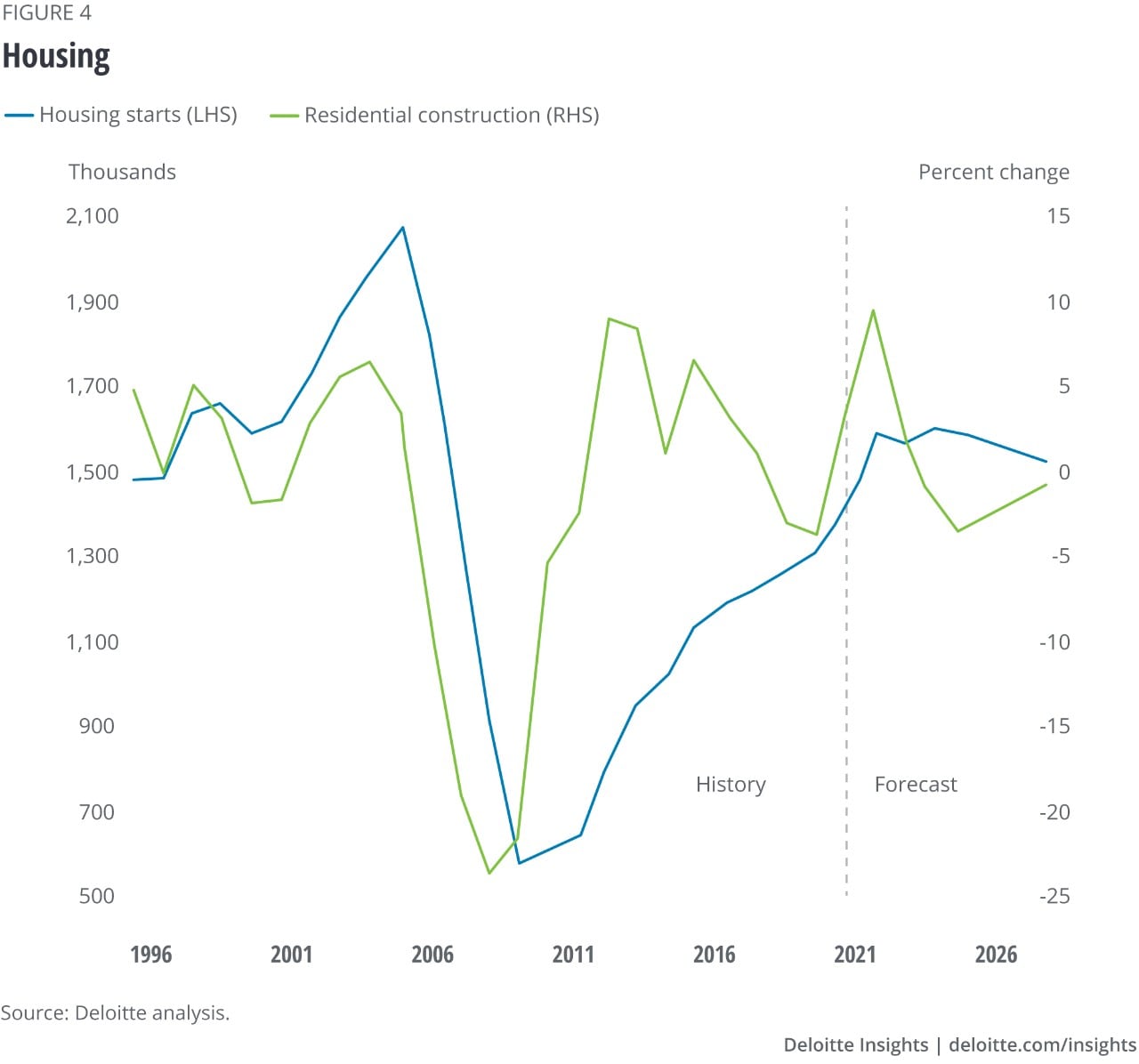

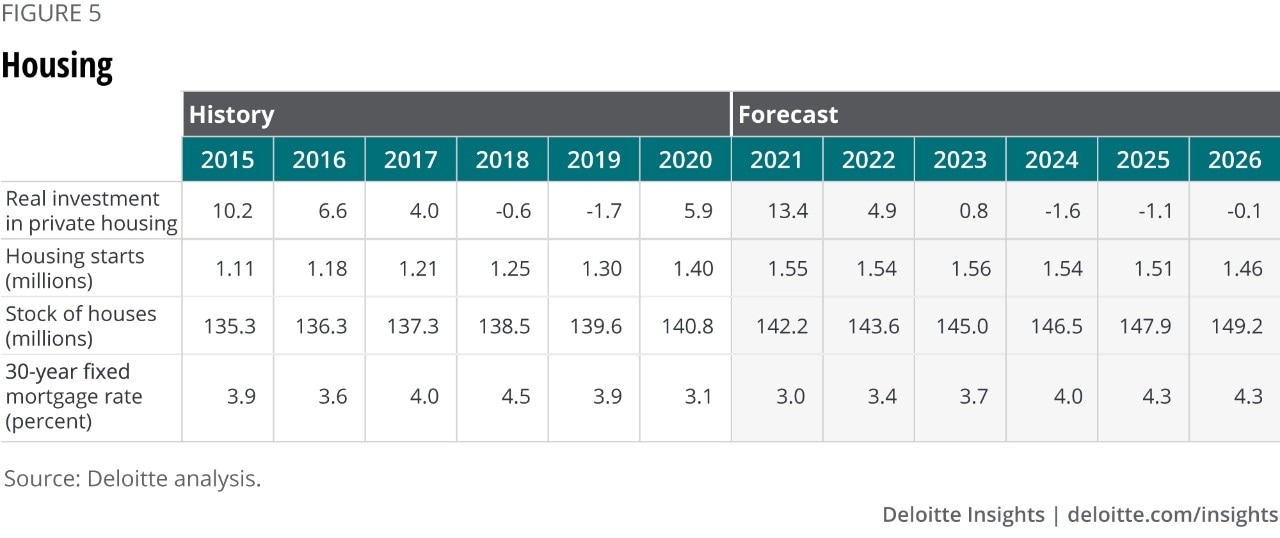

The housing sector has outperformed the broader economy in the wake of the pandemic. Buyers and sellers have found ways to navigate the pandemic’s restrictions. But other factors have combined to boost housing demand.10 These include the continued strong economic positions of high-wage remote workers, growing expectations that remote work will persist after the pandemic, historically low mortgage rates, and more millennials moving into prime home-buying age. This has lifted homebuilder confidence above pre–COVID-19 levels.

High-wage, remote-working homeowners have benefited from rising home equity. And real interest rates will continue to remain attractive to prospective buyers even as the 30-year fixed-rate mortgage rises. But strong demand coupled with suppressed housing supply will likely boost house prices further in 2021. Despite rising home prices, particularly for first-time buyers, risk is weighted to the upside. Overall housing activity is likely to stay elevated through at least the first half of the forecast period. A further spurt in activity is possible once the labor market recovery is clearly underway.

However, long-run fundamentals ensure that housing does not become a key driver of economic growth in our forecast. Slowing population growth means that the demand for housing will grow relatively slowly after the current boom in housing construction. Housing activity might also decline in the out years of the forecast because a considerable chunk of demand has been pulled forward. Moreover, an aging demographic means that more than a quarter of the nation’s existing owner-occupied homes are likely to become available over the next 20 years as the current owners either pass away or vacate their homes.11

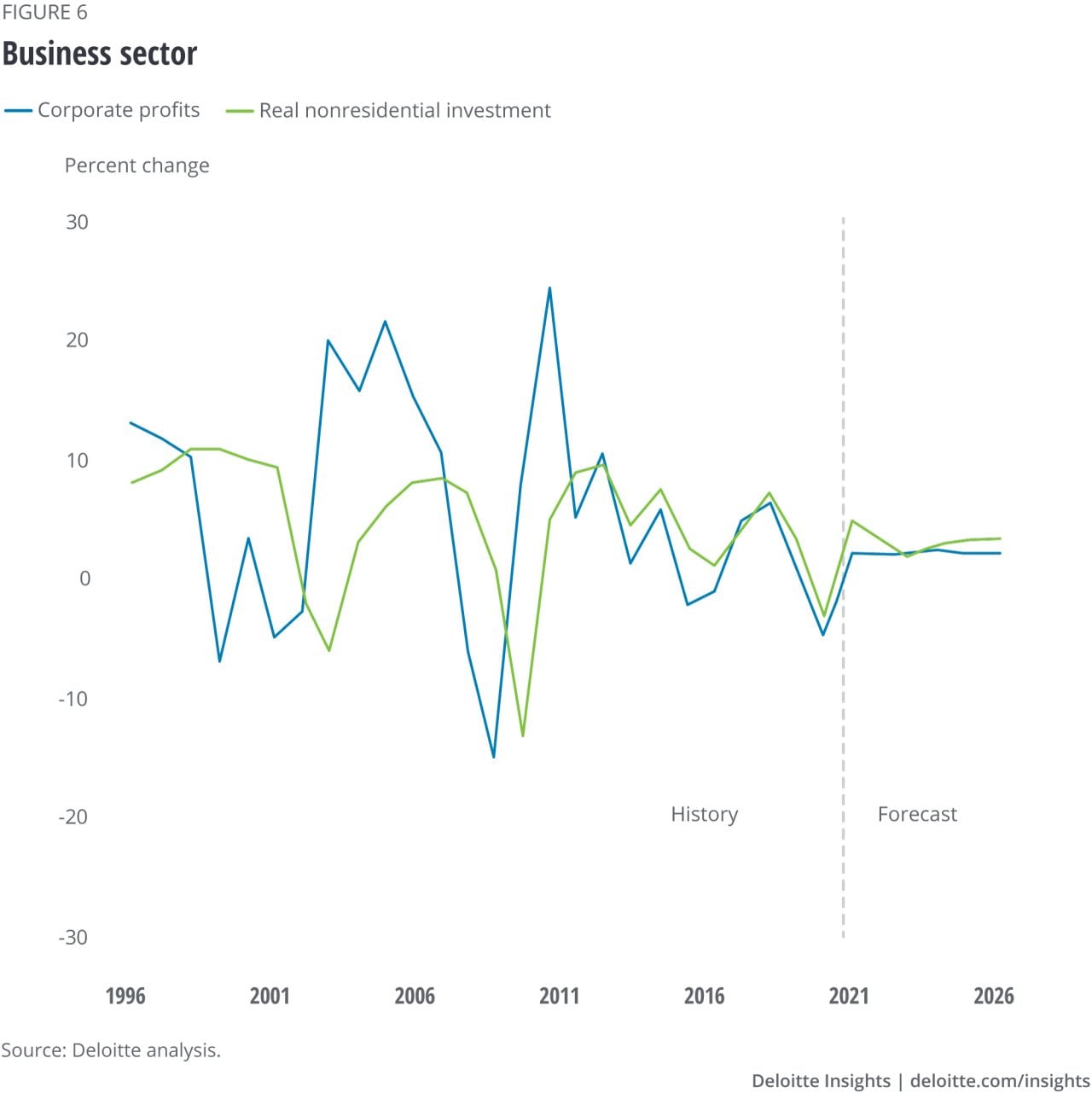

Much of business investment was interrupted, like everything else, by the closing of the economy to slow the pandemic’s spread. Investing in certain specific areas that supported virtual operations registered an impressive gain—business purchases of information processing equipment, for instance, rose 5% even as GDP fell in the second quarter. But this was insufficient to keep overall investment from dropping in 2020.

Businesses now face uncertainty in several dimensions. There is uncertainty about the disease itself, raising difficult-to-answer questions for any business—questions about operations, customers, and costs. There are questions about the financial system and the ability to fund new investments. And there are questions about the recovery—how quickly the unemployed will be able to find new jobs once the crisis is passed, and whether the government response will help the recovery.

On the other hand, businesses are sitting on a pile of cash. Nonfinancial businesses in the United States increased their holdings of bank deposits and similar instruments by over US$1.1 trillion in the first three quarters of 2020. Like consumers, many businesses decided to save rather than spend their cash inflow. And like consumers, businesses could decide to go on a spending spree when the pandemic ends. There is some question about what business would buy: Some traditional expensive capital projects, such as trophy headquarters buildings, may seem less compelling in a post–COVID-19 world. And the spending impetus is likely to vary quite a bit by industry, with those dependent on office workers or business travel perhaps a bit more reluctant to expand operations than those dependent on medical products or consumer durables.

These considerations may cause business investment to remain muted for some time. The baseline forecast assumes that business spending will remain relatively soft until the overall economy begins to steadily recover in mid-2021.

At that point, there may be reasons for businesses to begin increasing investment. Some of those reasons, unfortunately, may actually reduce productivity. First, many businesses will need to spend on safety equipment—air filters, for example—that will neither improve productivity nor add to profits. Second, government policy may encourage reshoring in “strategic” industries, especially medically related industries such as instruments and pharmaceuticals, arguing that it’s worth some inefficiency to obtain better national control over these areas in a future crisis. Third, businesses are likely to consider investing in ways to make their supply chains more robust, including reshoring, diversifying suppliers, and/or increasing inventories of critical products. All of these will likely help prevent extreme events from shutting down production but reduce efficiency and add to costs in normal operation.

The United States may, therefore, see relatively high levels of investment in this recovery. But it may not achieve the higher productivity we would normally expect that investment to generate.

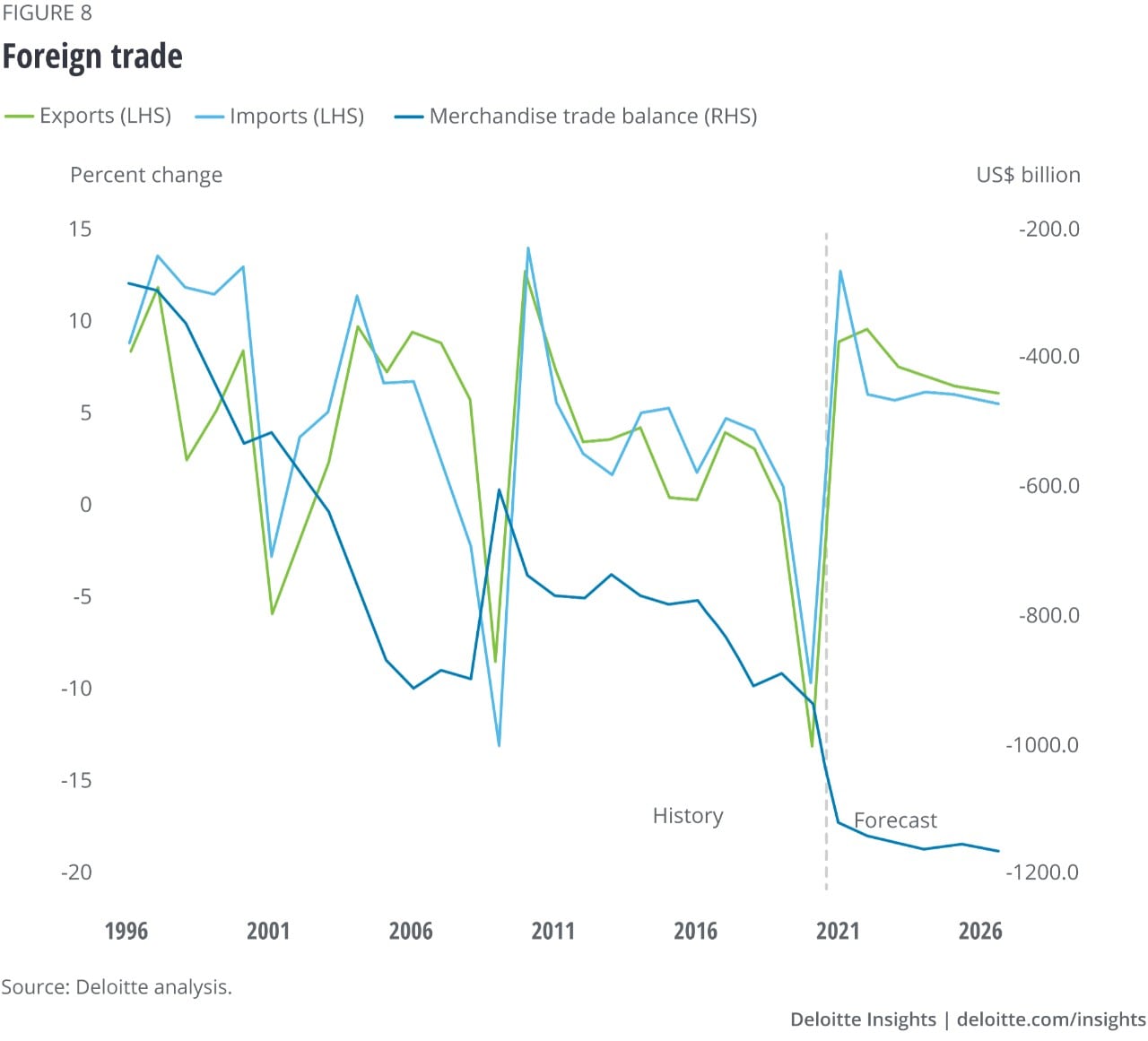

Over the past few years, analysts have begun to face the possibility of deglobalization. Global exports grew from 13% of global GDP in 1970 to 34% in 2012, but the share of exports in global GDP started to fall, globalization then began to stall, and opponents of freer trade took power in some key countries—most notably, the United States and the United Kingdom. All of this suggested that the policies that fostered globalization may change in the future.

COVID-19 may have accelerated this trend. Although the pandemic is a global phenomenon, leaders have made major decisions about how to fight it—in both health and economic policy—on a country-by-country basis. The most striking examples of this are the US withdrawal from cooperation in the World Health Organization—a move that President Biden rescinded on his first day in office—and the unilateral decisions of both China and Russia to deploy their own vaccines before completing testing.12 As the pandemic surged, the US-China trade war showed no sign of abating. And almost immediately after the adoption of the USMCA trade treaty for North America, the United States imposed tariffs on Canadian aluminum—not a good sign for the future of international cooperation and continued open borders.

Although President Biden signed a flurry of executive orders in his first weeks, the new administration has been cautious about overhauling his predecessor’s tariff-heavy trade policy.13 However, the White House has made clear that the United States intends to return to supporting a multilateral approach to trade by supporting Ngozi Okonjo-Iweala for director-general of the World Trade Organization (WTO). That ended a standoff over WTO leadership and suggests that the United States will once again support solving trade disputes through the WTO.

Businesses are likely to respond to the ongoing trade policy volatility. One important question is whether businesses will rebuild their supply chains to create more resilience in the face of unexpected events such as the pandemic and the change in US trade policy from the Obama administration to the Trump administration to the Biden administration. It’s impossible, of course, to simply and quickly refashion supply chains to reduce foreign dependence. American companies will continue to source from China in the coming years. But companies will likely begin to reduce their dependence on foreign suppliers or, at least, attempt to use a portfolio of suppliers rather than a single source, even if the single source is the cheapest.

Reengineering supply chains will inevitably mean a rise in overall costs. Just as the “China price” held inflation in check for years, an attempt to avoid dependency on China might create inflation pressures in the later years of our forecast horizon. And if markets won’t accept inflation, companies will have to accept lower profits in order to diversify supply chains. Globalization has offered a comparatively painless way to improve most people’s standard of living; deglobalization will involve painful costs and may limit real income growth during the recovery.

One of President Biden’s first initiatives—actually announced before he was sworn in—was proposing a comprehensive COVID-19 relief bill. Complicated parliamentary rules, combined with the increasing hardening of political party lines in the United States, explains the “Christmas tree” aspects of the COVID-19 relief bill, as Democrats know that they have only a few chances to pass preferred legislation. (An example is the funding of multiemployer pension plans in the House legislation passed at the end of February.)

Any relief proposal should be judged on two areas.

First, does it extend unemployment insurance benefits? These benefits have been the primary way in which the federal government has addressed the pandemic’s economic damage to individual workers. Unfortunately, the normal unemployment insurance system is inadequate when the economy goes into a recession, and Congress has always, in the past, extended the length of time that workers could receive benefits during economic downturns. This time, Congress also extended the reach of benefits to gig workers and others who are not normally eligible and initially supplemented benefits by US$600 per week.

The current relief bill extends benefits past the current March 14 final date to September. Our forecast suggests this will be sufficient, as the economy and labor markets should be in much better shape then. It also adds a US$400 weekly supplement (up from US$300), necessary because of the relatively low replacement rate of unemployment insurance using the usual formals in many states.

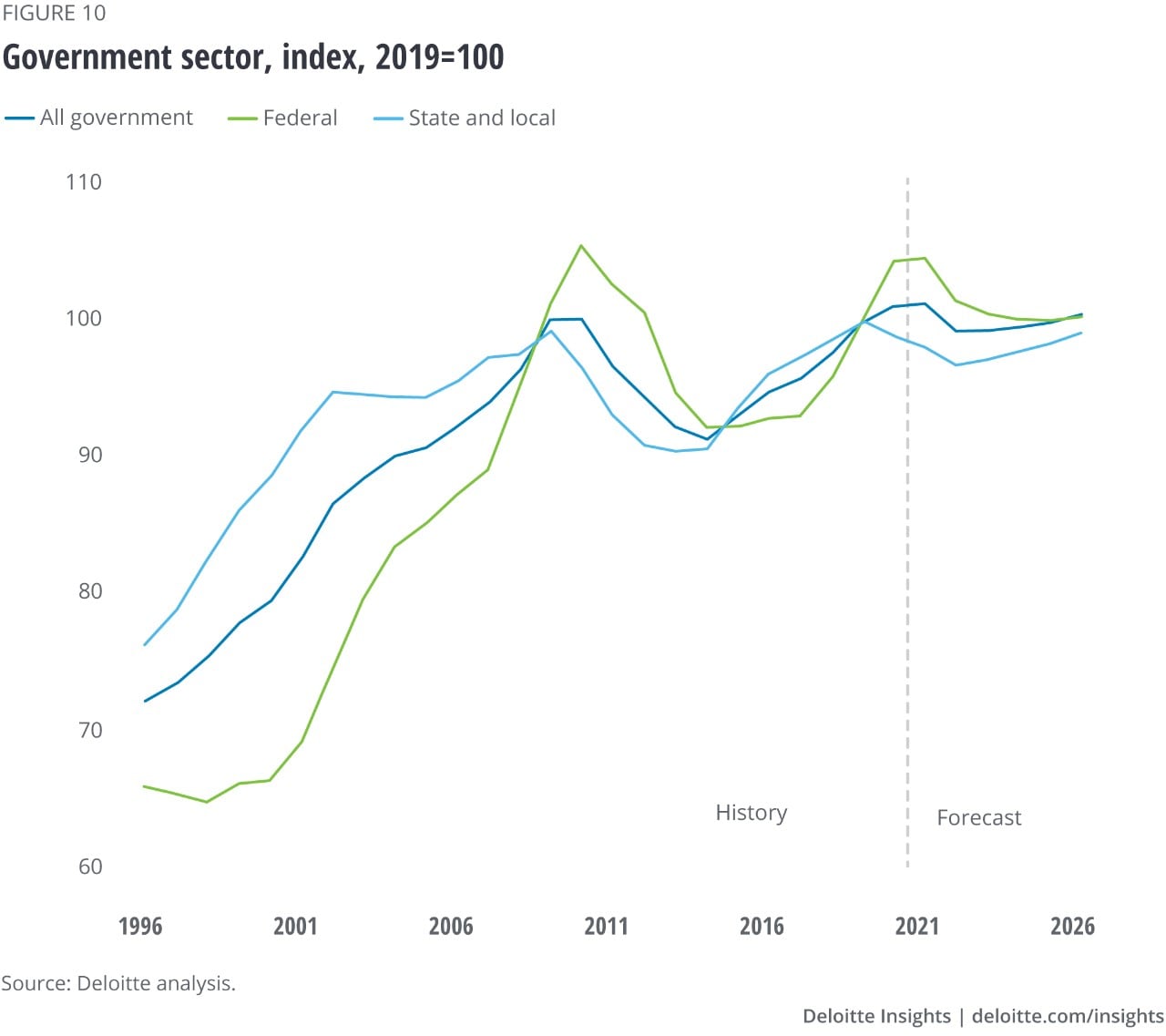

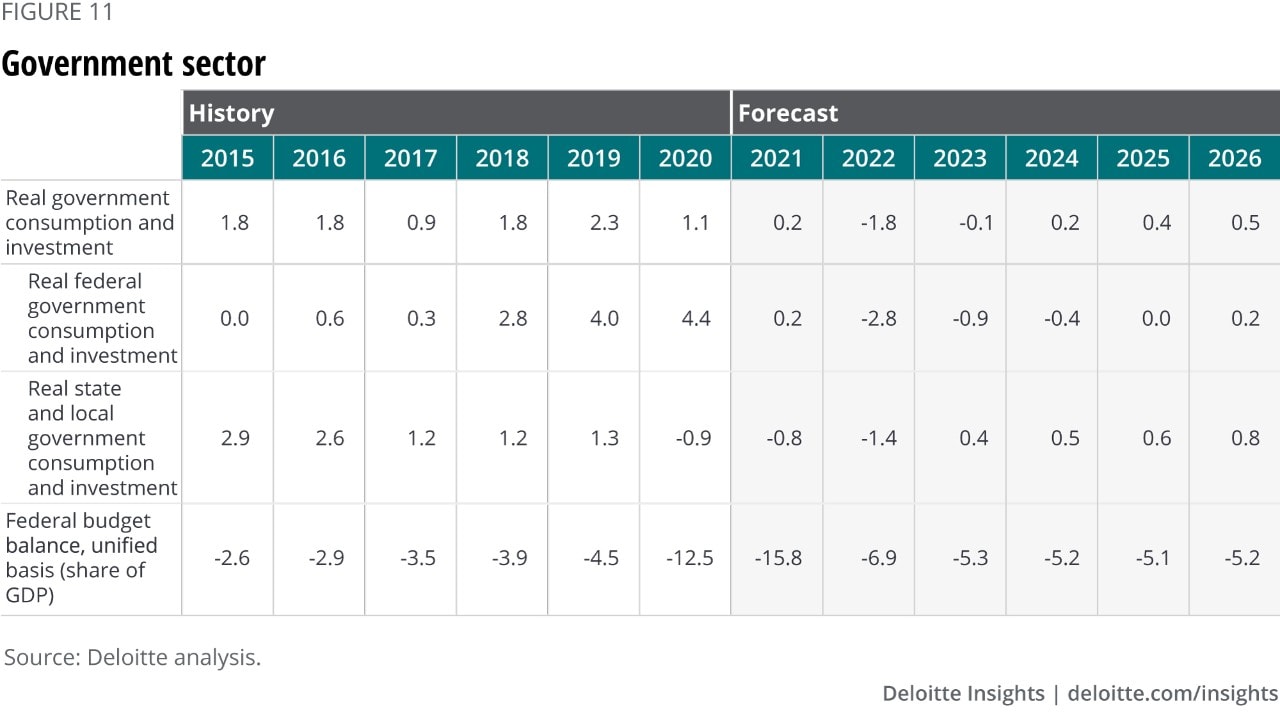

Second, does the bill provide help to state and local governments and to schools? Some analysts are questioning the need for intergovernmental aid because state and local tax revenues don’t appear to be hit as hard as many economists had expected.14 The picture is complicated by the rise in the stock market, which has buoyed the tax receipts of states that depend on progressive income taxes and delayed filing deadlines that make it difficult to compare year-over-year tax receipts. Two things are clear, however: State and local expenses are higher, and state and local governments have shed 1.3 million jobs over the past year. That’s 6.5% of the prepandemic payroll. Taking the chance that such layoffs won’t continue seems to be a bet.

The current relief bill provides quite a bit of money for state and local governments (including separate money for schools and for transit agencies). This may be too much: but at least it addresses the problem.

Former Treasury Secretary Larry Summers, among other analysts, has raised the possibility that the bill’s total spending is too large and could create inflationary pressures.15 This misunderstands the purpose of the bill: Its main goal is to keep deeply affected economic actors solvent until the pandemic is over; it’s not a traditional stimulus bill, should not be evaluated as one, and is unlikely to create sustained inflation (see below for more on inflation).

It’s true that relief spending thus far has ballooned the budget deficit. The CBO expects federal debt held by the public to equal over 100% of GDP by the end of FY2021. The Deloitte baseline shows the annual federal deficit remaining at over US$1.2 trillion through 2025, the end of our forecast horizon; this is just a little smaller than the largest deficit run during the global financial crisis.

This inevitably raises the question of whether the US government can continue to borrow at such a pace. The answer is that it can—until investors lose confidence. At this point, most investors show no sign of concern about US debt. In fact, very low interest rates on US government debt indicate that the world wants more, not less, American debt. We anticipate no problem over the forecast horizon. But the government will face a crisis if it does not eventually find ways to reduce the deficit and consequent borrowing. That crisis may be many years away, and current conditions argue for waiting. It would be a bad idea to wait too long once those conditions lift.

The current relief bill provides quite a bit of money for state and local governments (including separate money for schools and for transit agencies). This may be too much: but at least it addresses the problem.

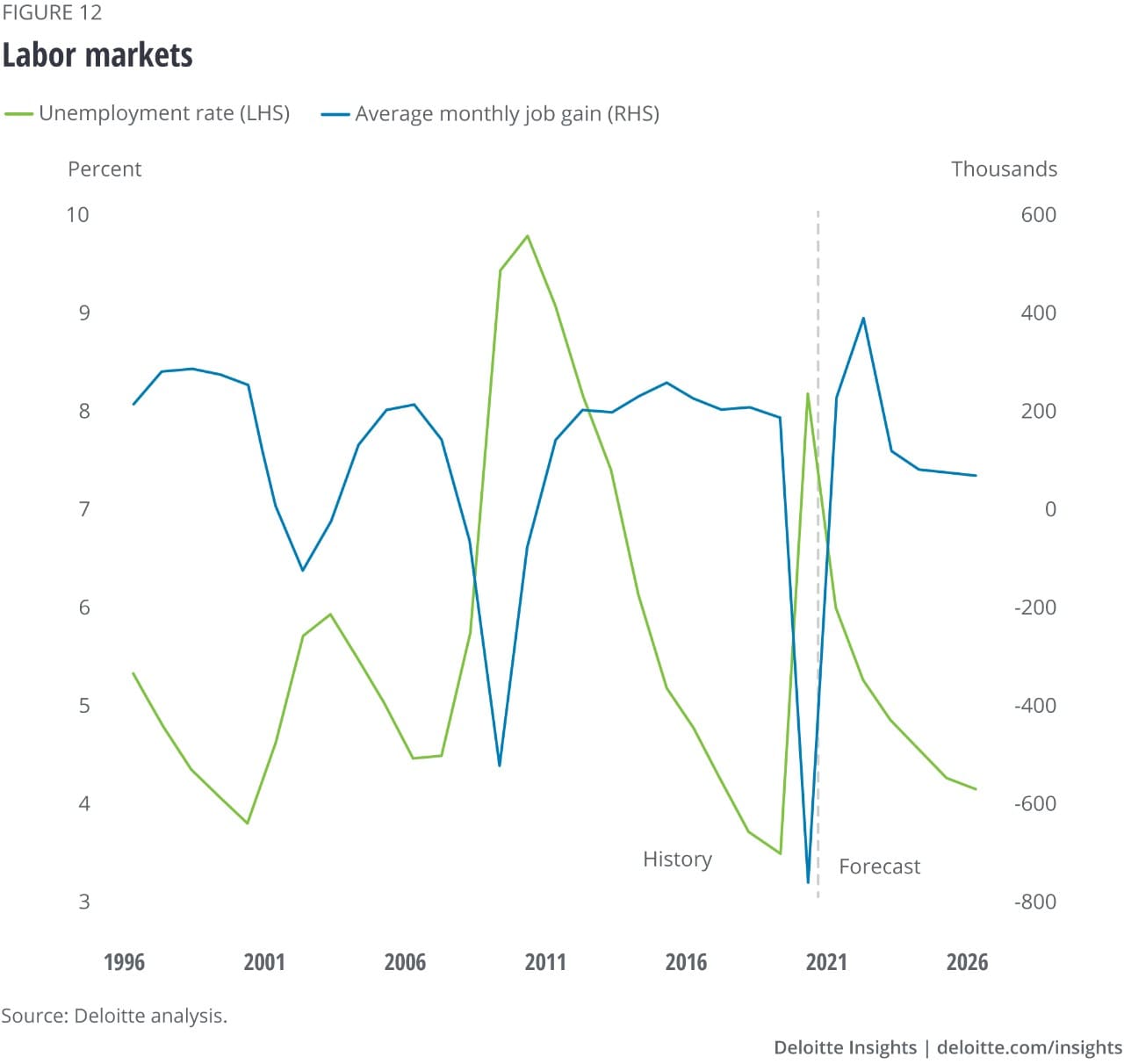

The great layoff of April 2020 saw employment plunge by more than 20 million, with most industries suffering a decline of more than 10%. Employers laid off half of everyone working in arts, entertainment, and recreation and in food services and accommodation. That’s a massive hole. About half of those jobs have returned, but employment remains about 10 million below the prepandemic level.

As long as COVID-19 remains a significant issue, demand in the most affected industries will continue to lag. But as the vaccination program begins to allow resumption of activity, we can expect to see demand for workers spike. That raises the question of whether those workers can return to the job quickly. Some, who have left the labor force or found jobs in other industries, may not return immediately. Spot labor shortages could well pop up in industries—such as food service and accommodation—unaccustomed to having to offer significant employment incentives. Businesses will eventually find those workers, and we will reach equilibrium. But the road there may be rocky.

In the longer term, businesses will still be looking for people—but perhaps in different industries and occupations. Efforts to reshore parts of the supply chain, and to build more robust manufacturing systems, will likely mean that jobs will become available in manufacturing and related industries. How to entice people to switch to manufacturing from, say, food service, and accommodation? The lack of opportunities in the old areas will help, but many businesses in manufacturing may need to invest substantial effort—and perhaps higher wages—to attract workers, even as unemployment remains high.

Such labor market adjustments are usually slow to occur, one reason why we expect the overall economic recovery in the baseline to be relatively slow. Promoting more efficient labor markets might help to speed the recovery—but it would mean admitting that the prepandemic economy will never return. That might be a hard pill for workers, businesses, and policymakers to swallow.

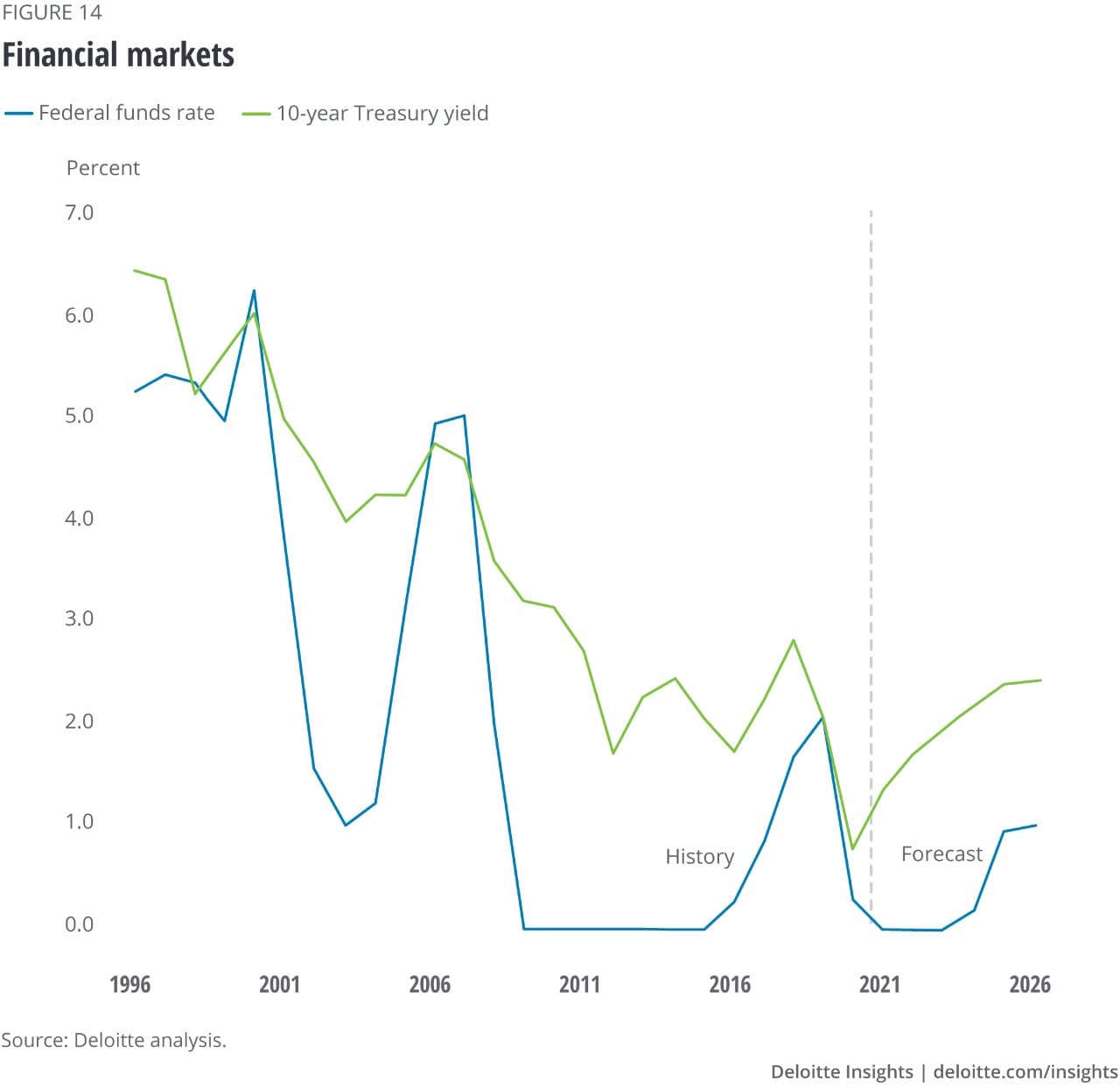

The Fed’s operations have been one of the bright spots of the US response to the pandemic. When the disease first began spreading, there was a significant possibility that a financial market meltdown would exacerbate the country’s economic problems. The Fed’s prompt and strong actions kept financial markets liquid and operating, preventing that additional level of pain.

There was a cost, of course: the Fed’s intervention in many different markets. The traditional concerns about the Fed buying private assets have gone out the window, and the Fed has created methods for direct lending from US states, counties, and cities (Municipal Liquidity Facility), small and medium-sized businesses (Main Street Lending Program), and purchases of corporate bonds (Primary and Secondary Corporate Credit Facilities).16 This is unprecedented: The Fed has traditionally avoided lending directly to nonfinancial firms. Other programs are aimed at stabilizing specific financial markets. Although the volume of lending for many of these facilities is still at a small fraction of the announced level, the Fed’s willingness to lend has calmed credit markets.

But there is a limit to what the Fed can do. It can keep financial markets operating, provide liquidity for markets, and even lend directly to companies so that they don’t shut down. But it can’t maintain the incomes of unemployed people, lend to state and local governments, or fund necessary health care spending. That’s why Fed Chairman Jerome Powell has emphasized the importance of action by Congress and the president.17 As he points out, the Fed has “lending, not spending, powers.” It would be foolish to expect Fed action alone to solve this economic crisis.

In the longer term, the Fed will want to wean markets off of its aid. But this is likely several years away. And since sales of these assets will precede hiking the Fed funds rate, we have assumed that the funds rate remains near zero over the five-year forecast horizon. We do assume a slow rise in long-term interest rates as financial markets “normalize.” But that leaves the 10-year Treasury yield at 2.5% by 2025. Interest rates are always the least certain part of any forecast: Any significant news could, and will, alter interest rates significantly.

But there is a limit to what the Fed can do. It can keep financial markets operating, provide liquidity for markets, and even lend directly to companies so that they don’t shut down.

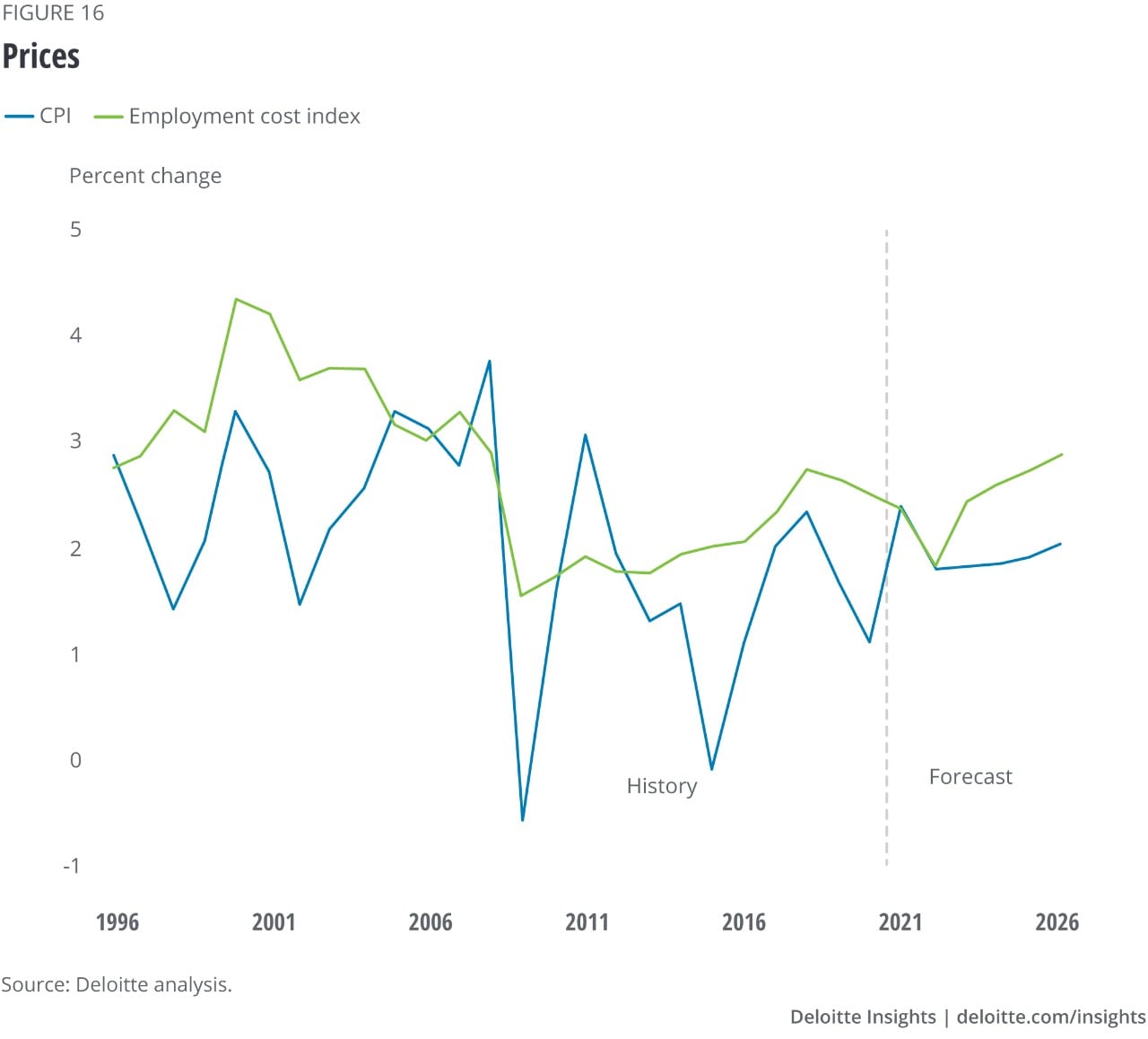

Talk of inflation picked up when Larry Summers published his analysis of the proposed relief bill.18 Summers focused his concerns on the fact that the gap between the economy’s capacity and actual production was about US$670 billion at the end of 2020, while the proposed bill totaled US$1.9 trillion. That suggests that GDP could be pushed up quite a bit above capacity in 2021 (assuming the entire amount is spent in one year), leading to shortages and, ultimately, higher inflation.

While Summers articulated concerns that have been percolating for some time, many challenged his analysis.19 First, the bill is a relief package, not a stimulus bill. A good deal of the money—for unemployment insurance, for example—will be spent only if unemployment is high (and by definition the economy is below capacity). Unlike in a traditional stimulus bill, the “cost” is not really indicative of additional demand automatically added to GDP. Second, estimates of capacity are imprecise. And although the Congressional Budget Office’s output gap estimate is only 3.0% (that is, output in 2020 Q4 was about 3% below capacity), the Fed estimates that the unemployment rate—if properly measured—could be close to 10%. Even at official levels, the labor market clearly has far more slack than that 3% capacity gap would suggest.

Most important, however, is the experience of the past 25 years. It’s clear that—contrary to the experience of the 1960s and ’70s—the US economy today can operate for extended periods of time above what economists believe is capacity without generating inflation. In the late 1990s, and then again in the late 2010s, the unemployment rate fell quite a bit below the level economists thought was consistent with stable inflation. At other times, the unemployment rate was very high. Yet through it all, inflation remained within a narrow 1.5% to 2.5% band. That experience argues strongly that President Biden’s pandemic relief bill is unlikely to generate sustained inflation.

That’s not to say that inflation spikes might not happen. Just as the pandemic created a sudden shutdown of some sectors of the economy, vaccination is likely to boost demand in many of those same sectors. The price for airline seats this summer might well spike as newly vaccinated Americans head out for long-delayed travel, while airlines struggle to rebuild their service networks. But inflation requires that such price spikes stimulate higher prices in other sectors, and that the need to raise prices be built into the economy. There are no signs that this is likely in today’s economy.

Unlike in a traditional stimulus bill, the “cost” is not really indicative of additional demand automatically added to GDP.

Thanks to Lester Gunnion, who played a key role in developing and producing this forecast.

Cover image by: Russell Benfanti