/figures/US-164917_Figure1.jpg){kind=link}

/figures/US-164917_Figure2.jpg){kind=link}

/figures/US-164917_Figure3.jpg){kind=link}

/figures/US-164917_Figure4.jpg){kind=link}

/figures/US-164917_Figure5.jpg){kind=link}

/figures/US-164917_Figure6.jpg){kind=link}

/figures/US-164917_Figure7.jpg){kind=link}

/figures/US-164917_Figure8.jpg){kind=link}

/figures/US-164917_Figure9.jpg){kind=link}

/figures/US-164917_Figure10.jpg){kind=link}

/figures/US-164917_Figure11.jpg){kind=link}

/figures/US-164917_Figure12.jpg){kind=link}

/figures/US-164917_Figure13.jpg){kind=link}

/figures/US-164917_Figure14.jpg){kind=link}

/figures/US-164917_Figure15.jpg){kind=link}

/figures/US-164917_Figure16.jpg){kind=link}

/figures/US-164917_Figure17.jpg){kind=link}

/figures/US-164917_Figure18.jpg){kind=link}

/figures/US-164917_Figure19.jpg){kind=link}

/figures/US-164917_Figure20.jpg){kind=link}

/figures/US-164917_Figure21.jpg){kind=link}

United States Economic Forecast has been saved

Thanks to Lester Gunnion, who played a key role in developing and producing this forecast.

Cover image by: Russell Benfanti

/primary/US164917_Banner.jpg/jcr:content/renditions/cq5dam.web.1920.400.jpeg)

Each month yields a stream of official economic data releases. For the most part, newspapers bury stories about this data somewhere deep inside, while economists and financial market traders pour over it for nuggets of information about how the economy is developing. But the November 10 release for the October 2021 Consumer Price Index (CPI) was different. The highest quality US newspapers made the CPI the top story for the day, with generous front-page coverage as well as pages of supporting commentary in the middle of the front section. It’s not like it was a “slow news day.” It was the culmination of an increasing media focus on inflation, which is at odds with the consensus among economic forecasters. Many economists agree with Fed officials and staff that the current price increases are “transitory,” even if Fed Chair Jerome Powell has “retired the term.”1 Surveys of economists, such as the Wall Street Journal Forecasters’ survey, show that most forecasters do, in fact, expect inflation to moderate by the second half of 2022. Why do economists remain so optimistic?

The pandemic changed the global economy very quickly. Businesses have scrambled to keep up, first as activity plunged in the spring of 2020, then as recovery occurred faster than expected … but with large changes in the structure of demand. In the United States, nonresidential construction remains 20% below the prepandemic level, while consumer purchases of durable goods soared to almost 30% above the prepandemic level before starting to decline in the second half of this year. Faced with such large swings in demand, it’s not surprising that businesses have had trouble calibrating their operations and, in many cases, finding key supplies. The broad shift from services to goods has been particularly difficult, since it’s often much harder to ramp up goods production quickly than it is to ramp up production in services industries.

The result is a series of shifts in prices. Some of the most dramatic price rises have been for commodities such as crude oil (up 67% from the beginning of the year through October), copper (up 26%), or chickens (up 25%). But such commodity price rises happen on occasion, and don’t lead to systemic inflation. They usually represent one-time changes in prices, reflecting the changing scarcity of different goods and services. And scarcity can change over time. Airline fares, for example, rose dramatically earlier in the year, but have since fallen back (and are still over 20% below the prepandemic level).

This makes the October rise in consumer prices look a lot less scary. In fact, October’s rise came after three months in which the core inflation rate was well within “reasonable” bounds. All economic data is volatile, and the one month of higher inflation could well fade away.

There are some worrying signs. First, the rise in shelter costs—the largest component in the CPI—has remained moderate even as house prices have grown quickly. There is some evidence that the methodology for calculating shelter prices causes house price changes to be reflected in the CPI with a lag of a year or so. If that’s the case, we may start seeing shelter prices accelerate, keeping measured inflation high.2 Second, an increasing share of the components of the CPI are seeing accelerating price rises, which suggests the possibility that the price hikes are becoming embedded in business dealings—an important element in translating one-time price hikes into systemic inflation. Third, some wages have begun to rise more quickly than they did pre-pandemic. While significant wage rises are still limited to those industries and workers that were most affected by the pandemic (in particular, leisure and hospitality), overall employment costs do seem to be accelerating. That’s the most worrisome signal; if higher prices for select commodities and goods become embedded into everybody’s views about future prices, inflation could become widespread. That could certainly require a policy response.

For now, the evidence that inflation could become systemic is not very strong. Keep in mind that in the 1970s, it took years (and a shockingly large rise in oil prices) for inflation to become embedded in the expectations of households and businesses. So far, there aren’t any signs that long-run expectations of inflation are rising. This is a good indication that it would take many months of continued reports such as October’s CPI release before inflation becomes a serious long-term threat to economic stability.

Deloitte’s new forecast includes a scenario in which inflation becomes a significant problem. We expect that this scenario has a relatively low probability, however. The flurry of concern about inflation based on the October CPI release says more about the difficulty the news media faces in reporting on economic events than it does for the potential of actual inflation breaking out.

One further key point about the current inflation problem: It is the result of the pandemic, but also the highly successful attempts in the developed world to preserve incomes for the relatively low-paid workers, who were most at risk from the pandemic (both economically and medically). Those higher incomes allowed demand to pick up to levels that created some of the shortages that now plague the economy. But that’s a much better economic outcome than the alternative: letting the pandemic create widespread misery among workers and families in pandemic-sensitive industries. If inflation is the cost of that prevention, it’s a price that was well worth paying.

Baseline (60%): Growth recovers in late 2021 and early 2022 as the impact of COVID-19 wanes. Households continue to increase spending on pent-up demand for services such as entertainment and travel. However, spending on durable goods stalls as consumers switch back to prepandemic patterns. Business investment continues to grow rapidly, particularly in information processing equipment and software. Investment in nonresidential structures remains weak, however, as the oversupply of office buildings and retail space weighs on the market. Housing construction remains strong but gradually falls, as the current level of construction is greater than population growth can support. The infrastructure spending bill and a modest Build Back Better plan raise the level of government spending for most of the forecast period. All of this helps elevate demand above the pre–COVID-19 trend for several years. Inflation remains above the Fed’s target in 2022, but gradually settles back to the 2% range as demand for goods falters and businesses solve their supply chain issues. The pandemic jump-starts the widespread adoption of new technology, leading to faster productivity growth. The unemployment rate gradually falls back to below 4%. The Fed raises rates in 2022 and continues to raise rates at a relatively fast rate in 2023, since the economy is clearly moving toward full employment.

Paging Dr. Pangloss (5%): Dr. Pangloss, a character in Voltaire’s Candide, would repeat that “all is for the best in this best of all possible worlds.”3 Our baseline forecast is optimistic but not Panglossian, with some lagging sectors likely to hold back growth. What could turn out better? Well, the labor force might grow faster than we expect in the baseline, in which we’ve assumed that older people who left the labor force don’t return once the pandemic is over. Consumer spending, particularly for durable goods, remains strong. And global growth recovers more quickly, helping to support the US economy (and to keep prices in check). The result: A faster recovery in 2021 and 2022 and continued slightly faster growth over the forecast’s remaining years. Of course, it’s not quite all for the best, as inflation picks up a bit and interest rates move back toward their (higher) long-term averages.

Relapse (20%): The discovery of the Omicron variant underlines the risks that COVID-19 continues to pose to the US economy. New variants are constantly being found.4 In this scenario, the current vaccines are not as effective against one or more new variants. People return to some social distancing and cut back on purchasing goods and services that are perceived as “risky.” This creates another one-quarter drop in GDP at the end of 2021. A muted government response results in financially stretched businesses failing and weak balance sheets create the conditions for a more traditional, slower recovery from the recession. This is particularly the case because—after two outbreaks in two years—consumers permanently reduce spending on travel, entertainment, food, and accommodations, requiring a painful readjustment of the economy.

Back to the 70s (15%): Households and businesses see price hikes from pandemic-related shortages and react by raising prices and wages. The reaction, and consequent rise in inflationary expectations, creates an inflationary spiral. Consumer prices are rising at a steady rate of over 5% by the end of 2022, causing the Fed to raise interest rates to limit demand. In 2023, inflation continues, but a “growth recession” causes the unemployment rate to rise. The Fed is reluctant to engineer an actual recession, and inflation settles in at a 4% rate over the five-year forecast horizon.

The near-term outlook for consumer spending turns on two big questions:

1. Will consumers spend down all those pandemic-era savings?

In 2020, households saved about US$1.6 trillion more than we forecasted before the pandemic. Some of that went into investments, but many households have a lot more cash on hand now than they normally would want. How much of that will they spend as the pandemic impact wanes? One possibility is that many consumers will remain cautious and hold on to those savings even as they are able to get out and spend. Another possibility: Spending booms for a while longer as the impact of Delta wanes. The baseline Deloitte forecast assumes a modest decline in the savings rate below its long-term level, and that’s enough to support very strong growth in consumer spending this year. But spending could be even stronger if households decide to cash in more of those savings.

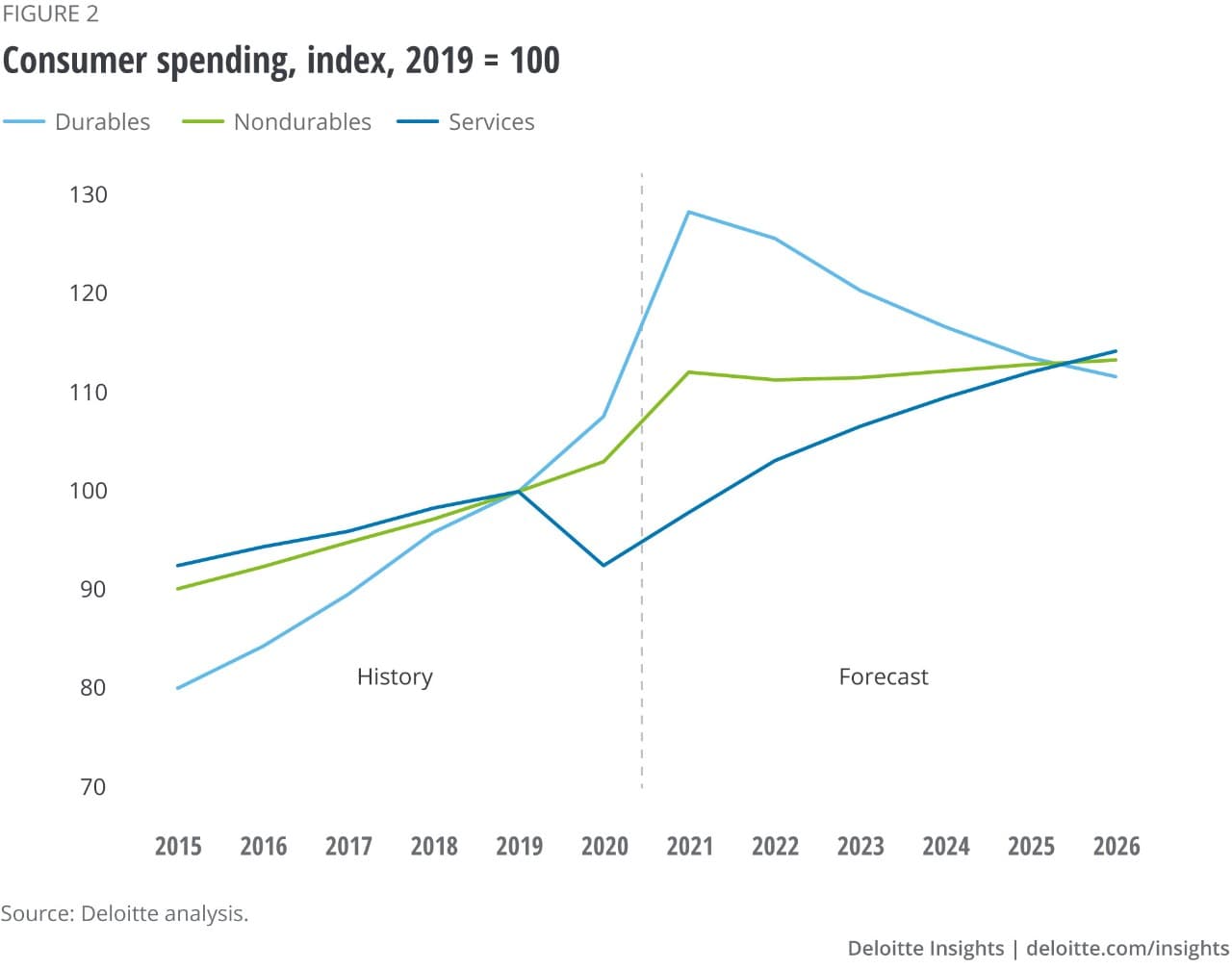

2. When consumer services recover, what happens to durable goods?

The pandemic sparked a remarkable change in consumer spending patterns. Spending on durable consumer goods jumped US$103 billion in 2020, while spending on services fell US$556 billion during the same period. Households substituted bicycles, gym equipment, and electronics for restaurants, entertainment, and travel. Once households can again purchase services, will they begin buying fewer goods? That may be happening, as durables spending fell for six straight months ending in October. Our forecast assumes that, over the next few years, durables spending continues to slowly fall, because consumers no longer need to acquire durable goods, and increase the share of their income going to services instead.

Deloitte’s forecast assumes that durable goods spending continues to fall over most of the forecast horizon as consumer spending “renormalizes” and consumers move back toward spending on services. For a more detailed consumer spending forecast, see Deloitte’s consumer spending forecast, Consumer spending forecasts: Services find their way back after a forgettable 2020.

In the longer term, we expect the pandemic to exacerbate some existing problems. The pandemic has thrown the problem of inequality into sharp relief, straining the budgets and living situations of millions of lower-income households. These are the very people who are less likely to have health insurance—especially after layoffs—and more likely to have health conditions that complicate recovery from infection. And retirement remains a significant issue: Even before the crisis, fewer than four in 10 nonretired adults described their retirement as on track, with one-quarter of nonretired adults saying they had no retirement savings.5 Low interest rates will worsen Americans’ preparation for retirement, while the stock market boom will have little impact on most people’s balance sheets.6

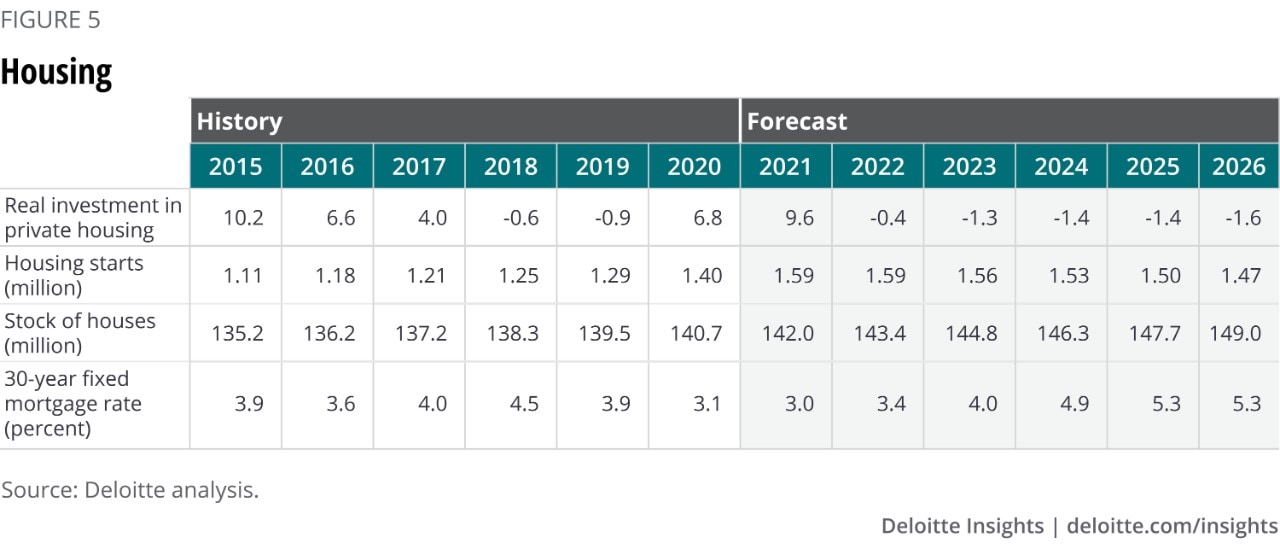

The housing sector outperformed the broader economy in the wake of the pandemic, as buyers and sellers found ways to navigate the pandemic’s restrictions. A host of factors combined to boost housing demand over the past year:

Residential investment weakened for the third quarter in a row in Q3. However, demand for houses remains high, and homebuilder confidence remains above pre–COVID-19 levels. The spread of the Delta and Omicron variants could potentially strengthen the case for remote work, therefore boosting housing demand. Additionally, data indicates that more vacant developed lots of land could be available for homebuilding, driving an uptick in short-term housing supply.

Deloitte expects demand to cool due to reduced affordability in the medium term. Nominal home price increases are likely to more than offset the impact of low mortgage rates on demand. And interest rates are set to rise in the forecast as the recovery eventually gathers speed. Despite the slowdown, demand is likely to exceed supply in the medium term as builders continue to grapple with supply chain issues and land-use restrictions. The Deloitte baseline forecast expects house prices to rise faster than inflation through the forecast horizon.

Demographics suggest that housing is not likely to become a key driver of economic growth in the foreseeable future. Population growth has slowed to about 0.5% per year (compared to over 1% during the 2000s’ housing boom). The baseline forecast assumes that housing starts will gradually fall over the five-year horizon to 1.3 million starts in 2026. Faster medium-term growth would require faster population growth, most likely from immigration. Otherwise, the current heightened demand for housing is likely to be a short-term phenomenon.7

Nonresidential investment slowed in Q3. Investment in structures continued to weaken, but investment in equipment also fell. Investment in transportation equipment and computers fell. The fall in equipment investment might reflect supply chain problems rather than business demand as the chip shortage might have limited businesses’ ability to purchase cars, light trucks, and computer equipment.

Nonresidential structures investment, on the other hand, continues to be down (more than 20%) from the prepandemic level. Most likely, the business case for office buildings and retail space collapsed with online shopping and the shift toward working at home. Mining structures also took a big hit because of the decline in oil prices earlier in the pandemic. There are signs that construction of mining structures has begun to reverse, which may help to boost the sector temporarily. However, the overall recovery of the nonresidential construction is likely to be limited by the continued low demand for office and retail space.

Despite the decline in Q3, investment in equipment was up 5.1% from the prepandemic level in Q3. The Deloitte forecast assumes continued growth, as the need for transportation equipment (to move goods) and information processing equipment (to support telework) is likely to remain strong.

Intellectual property investment accelerated during the pandemic (after dropping in the first quarter of 2020). That’s mostly because of investment in software, and likely reflects the investments needed for telework. We expect this category to remain strong over the next few years as businesses continue to require software to accompany their investments in information processing equipment.

Financing investment will remain easy. Nonfinancial businesses are sitting on a pile of cash, and interest rates are low. In our baseline forecast, the 10-year Treasury yield rises to a relatively low (by historical standards) 4.5% and stays there through the end of the forecast horizon. Even adding in the potential for a corporate tax hike, the cost of capital is likely to remain very low. That will give businesses plenty of ability to pay for all those new computers and servers, not to mention the software to run them. But even with such easy financing terms, office and retail space will be unable to generate sufficient returns to entice businesses to increase capacity.

Real US exports remain substantially below the prepandemic level, while real imports are now higher than they were in late 2019. Deloitte’s baseline forecast assumes that exports will grow more quickly than imports as global financial and economic conditions normalize. More normal financial conditions will create more opportunities for investment outside the United States and less desire to hold dollars to avoid risk, lowering the dollar and making the United States more competitive globally. As a result, there is a modest improvement in the current account deficit over the forecast horizon.

Of course, much depends on how trade policy develops. Over the past few years, many analysts have begun to face the possibility of deglobalization. Global exports grew from 13% of global GDP in 1970 to 34% in 2012, but the share of exports in global GDP started to fall, globalization then began to stall, and opponents of freer trade took power in some key countries. All this suggested that the policies that fostered globalization may likely change in the future.

COVID-19 may have accelerated this trend. Although the pandemic is a global phenomenon, leaders have made major decisions about how to fight it—in both health and economic policy—on a country-by-country basis. The most striking examples of this are the US withdrawal from cooperation in the World Health Organization—although President Biden rescinded the move on his first day in office—and the unilateral decisions of both China and Russia to deploy their own vaccines before the completion of phase 3 trials. And countries with vaccine manufacturing facilities rushed to vaccinate their own citizens rather than cooperating on a global vaccination plan.

On top of this, the United States–China trade conflict continues. The White House has shown some interest in returning to a multilateral approach to trade—for example, by supporting Ngozi Okonjo-Iweala for World Trade Organization director general. However, US Trade Representative Katherine Tai has made a point of stating that trade policy should be aimed at helping US workers.8 And as of October—almost nine months after President Biden took office—most of the Trump-era tariffs remain in place.

Many businesses have been considering rebuilding their supply chains to create more resilience in the face of unexpected events such as the pandemic and changes in US trade policy. The imperative for such changes has become stronger with the increasing supply chain issues and port delays facing importers of key components and consumer goods. It’s impossible, of course, to simply and quickly refashion supply chains to reduce foreign dependence. American companies are expected to continue to source from China in the coming years. But companies will likely accelerate attempts to reduce their dependence on China (a process they had begun before the pandemic). Building more robust supply chains may mean moving production back to the United States, or perhaps to Mexico or some other, closer source. Or it may mean a portfolio of suppliers rather than a single source—even if the single source is the cheapest.

Reengineering supply chains will inevitably mean a rise in overall costs. Just as the “China price” held inflation in check for years, an attempt to avoid dependency on China might create inflationary pressures in the later years of our forecast horizon. And if markets won’t accept inflation, companies will have to accept lower profits in order to diversify supply chains. Globalization has offered a comparatively painless way to improve most people’s standard of living; deglobalization will involve painful costs and may limit real income growth during the recovery.

Meanwhile, short-term trade flows are hostage to the virus. Port shutdowns, container shortages, and other supply chain woes will continue to increase month-to-month volatility in trade—and perhaps provide business executives more reason to find more robust (and more expensive) alternatives.

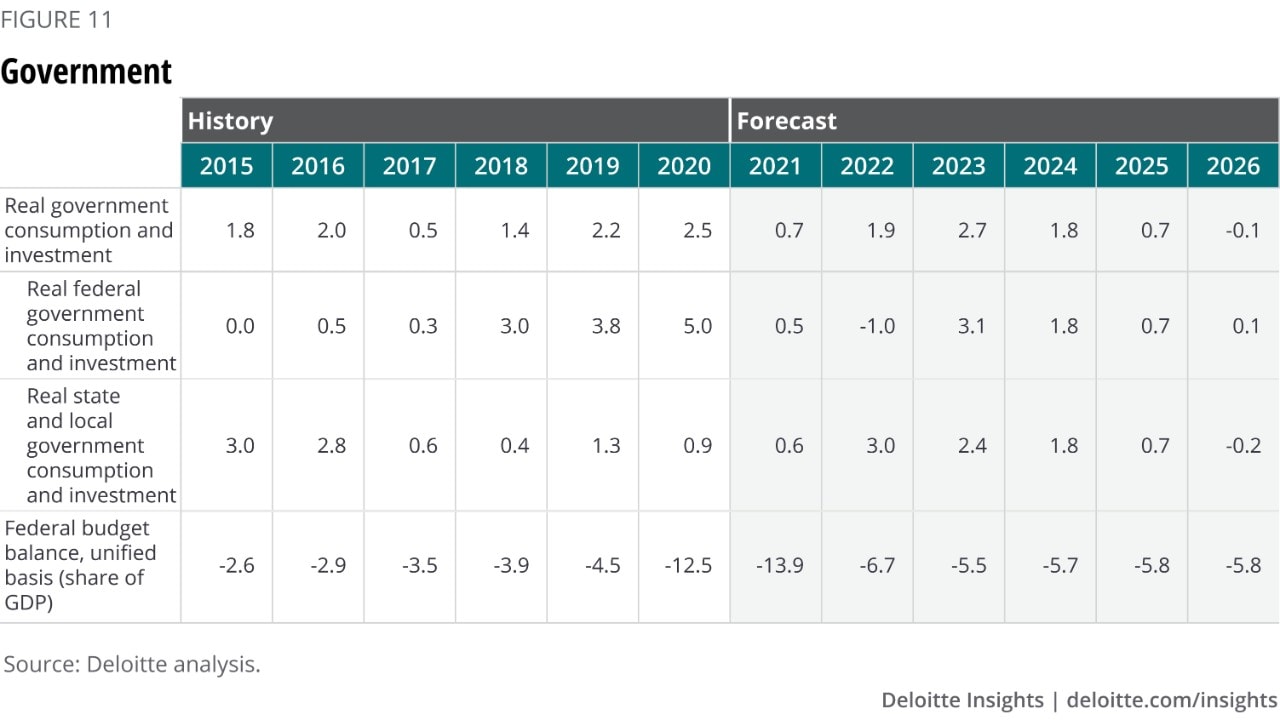

The cone of uncertainty about the Federal budget has become a bit smaller lately.

First, the Bipartisan Infrastructure bill is now completed and signed. The federal government is now committed to providing about US$500 billion in new money for infrastructure spending over the next five years. The word for this bill is “sprawling,” as it includes money for a wide range of projects, from improving the electrical grid to Amtrak, the US rail passenger company. It may take several years before anybody notices, but the bill will probably make a material difference in many people’s lives.

Second, Democrats continue to negotiate the Build Back Better bill. This bill is designed to incorporate the portions of the administration’s long-term plans that could not be included in the bipartisan bill. It has essentially been shrinking, as the slim Democratic majority in the Senate means that two conservative Democratic senators (and some Democrats in the House) have to be satisfied that the bill addresses concerns about the scope of some of the programs and about funding. Whether the bill finally passes remains a question (which may even be decided before this forecast is published).

Third, the prospect of a government debt ceiling crisis has arisen again. The exact date of the potential crisis is unclear—perhaps in late December, perhaps in January. The Republican minority in the Senate can block attempts to raise the debt ceiling, but the Democratic majority retains the initiative in proposing solutions. The result in October was that the Republicans agreed to raise the debt ceiling for a short period of time. As it becomes clear that a crisis point is approaching, pressure will likely grow on the Republicans to agree to raise the debt ceiling, perhaps for a longer period. Both parties continue to play the game of “chicken” with this dangerous issue, and a longer-term resolution does not appear to be on the table.

So far, the budget process is playing out in a manner consistent with our previous forecasts. We assumed that the infrastructure plan passes, but that the budget reconciliation bill (the Build Back Better plan) is more modest than the original proposal. Our five-year horizon is not long enough to capture the impact on longer-term productivity. But we don’t expect the spending to raise inflation, both because of Fed policy and because recent experience suggests that the US economy can operate with low inflation at relatively low unemployment rates. None of the scenarios in the Deloitte forecast assumes that the debt ceiling becomes a constraint for more than a trivial amount of time; if that were to be the case, the impact on the global economy (and the US economy) could be quite large.

Our forecast assumes deficits will fall by 2022 to about US$1.4 trillion per year, and then rise slowly. That’s a hefty amount, one that inevitably raises the question of whether the US government can continue to borrow at such a pace. The answer is that it can—until investors lose confidence. At this point, most investors show no sign of concern about US debt. In fact, very low interest rates on US government debt indicate the world wants more, not less, American debt. We anticipate no problem over the forecast horizon.

But the government will face a crisis if it does not eventually find ways to reduce the deficit and consequent borrowing. The crisis may be many years away, and current conditions argue for waiting. It would, however, be a bad idea to wait too long once those conditions lift.

The conversation about labor markets has switched—and fast. Not long ago, employment was about 10 million below the prepandemic level and the main question was how difficult it would be to get all those workers back on the job. Now business commentary is full of talk about labor shortages and stories about employers struggling to find workers. That seems a bit odd since employment is still down about a million after the October jobs report.

Pundits have seized on several reasons why businesses are experiencing so much trouble hiring workers:

Generous government benefits kept people out of the labor force. This explanation makes some sense, but there are reasons to doubt that it is the whole story or, perhaps, even a major part of the story. Growing research literature indicates the original US$600 weekly supplement to unemployment insurance did not affect businesses’ ability to rehire workers during the earlier part of the recovery.9 However, anecdotal evidence is strong enough to suggest that the unemployment insurance supplement is contributing to the problem. The last of these benefits ended in September, however, and labor force participation has remained surprisingly low.

Childcare has prevented a significant number of people from reentering the labor force. The Bureau of Labor Statistics (BLS) estimates that the labor force participation among parents of children under 18 years fell about one percentage point in 2020. The good news is that this problem is on its way to being solved, with schools reopening. Day cares, however, are among the businesses that have the most trouble finding staff, which limits the ability of parents of small children to reenter the labor force.

Health remains a concern for people who are at risk of COVID-19, particularly those who cannot be vaccinated due to a high risk of complications.

About half of the decline in the labor force is among people 55 years and older. Many of these people have probably retired, in the sense of expecting to remain permanently out of the labor force, but some can likely be enticed back with the right compensation packages and flexible working hours and conditions.

As is the case in many areas, the pandemic accelerated trends that were evident before it started. Slow labor force growth and continued high demand had already created conditions that required companies to offer higher wages to lower-skilled workers and to be more imaginative about hiring.10 In the post–COVID-19 world, companies that make extra effort to find the workers they need and provide conditions to attract those workers will have an important competitive advantage.

Deloitte’s baseline forecast assumes that job growth is very strong over the next few years as employers do, in fact, find and rehire those missing workers. The unemployment rate falls, reflecting not only the job growth, but the fact that a significant number of older people have left the labor force permanently. Over the longer horizon, labor force growth slows to just 0.2% per year, presenting continuing challenges for employers.

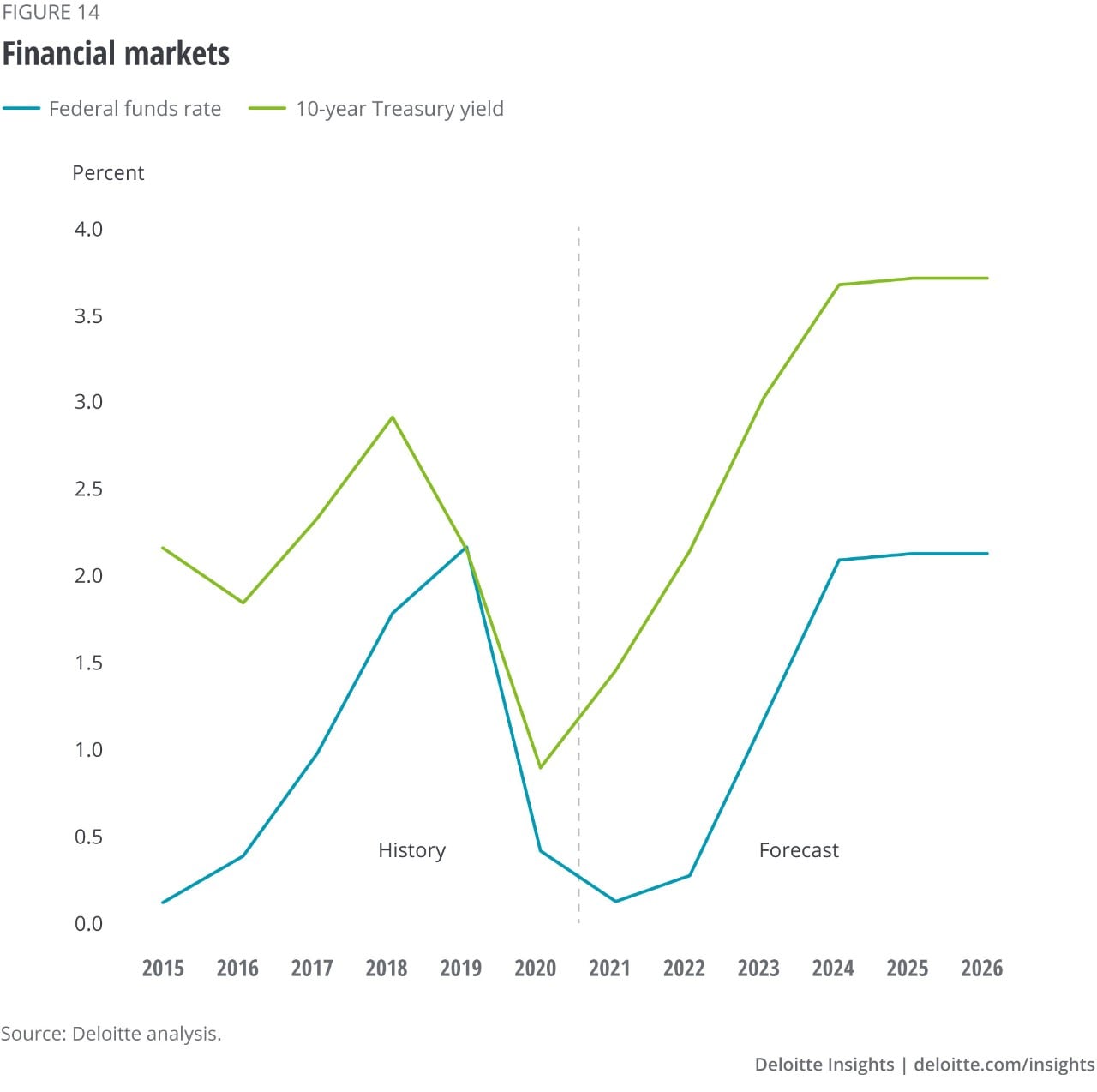

The Fed’s actions have been one of the bright spots of the US response to the pandemic. When the virus first began spreading, there was a significant possibility that a financial market meltdown would exacerbate the country’s economic problems. The Fed’s prompt and strong actions kept financial markets liquid and operating, preventing that additional level of pain.

With GDP now above the prepandemic level, strong employment growth, and some signs of incipient inflation, the Fed has started to unwind its pandemic response. “Tapering” purchases of long-term assets (“quantitative easing” or QE) began at the early November FOMC meeting, and some commentators are talking about the Fed completing the process of shutting down purchases of new long-term assets by the middle of 2022. That would be a fast reversal of the policy, but one that would leave Fed officials more comfortable with the next step, which is starting to raise interest rates. The end of QE, however, will not end questions surrounding the Fed’s policy. It will still own more than US$7 trillion in long-term assets (both Treasuries and mortgage-backed securities). The Fed may eventually actively sell these, or it may elect to let them “runoff” by not replacing them as they mature. Discussions about the Fed balance sheet will continue for some time.

At the November FOMC meeting, Fed officials indicated that they expected to hike in the Fed funds rate toward the end of 2022. The Deloitte forecast assumes continued strong economic growth, which we believe opens the door for two hikes in 2022 and continued hikes in 2023, as the Fed returns the target funds rate to “normal.” By 2024, our forecast has the Fed funds rate at 2.8%, our estimate of the “equilibrium” rate. We expect long-term rates to rise as well, reflecting the global economic recovery and the rise in short-term rates. By 2026, the 10-year Treasury stands at 4.5%. That may seem high today, but is, in fact, a low level in historical context.

Of course, interest rates are always the least certain part of any forecast: Any significant news could, and will, alter interest rates significantly.

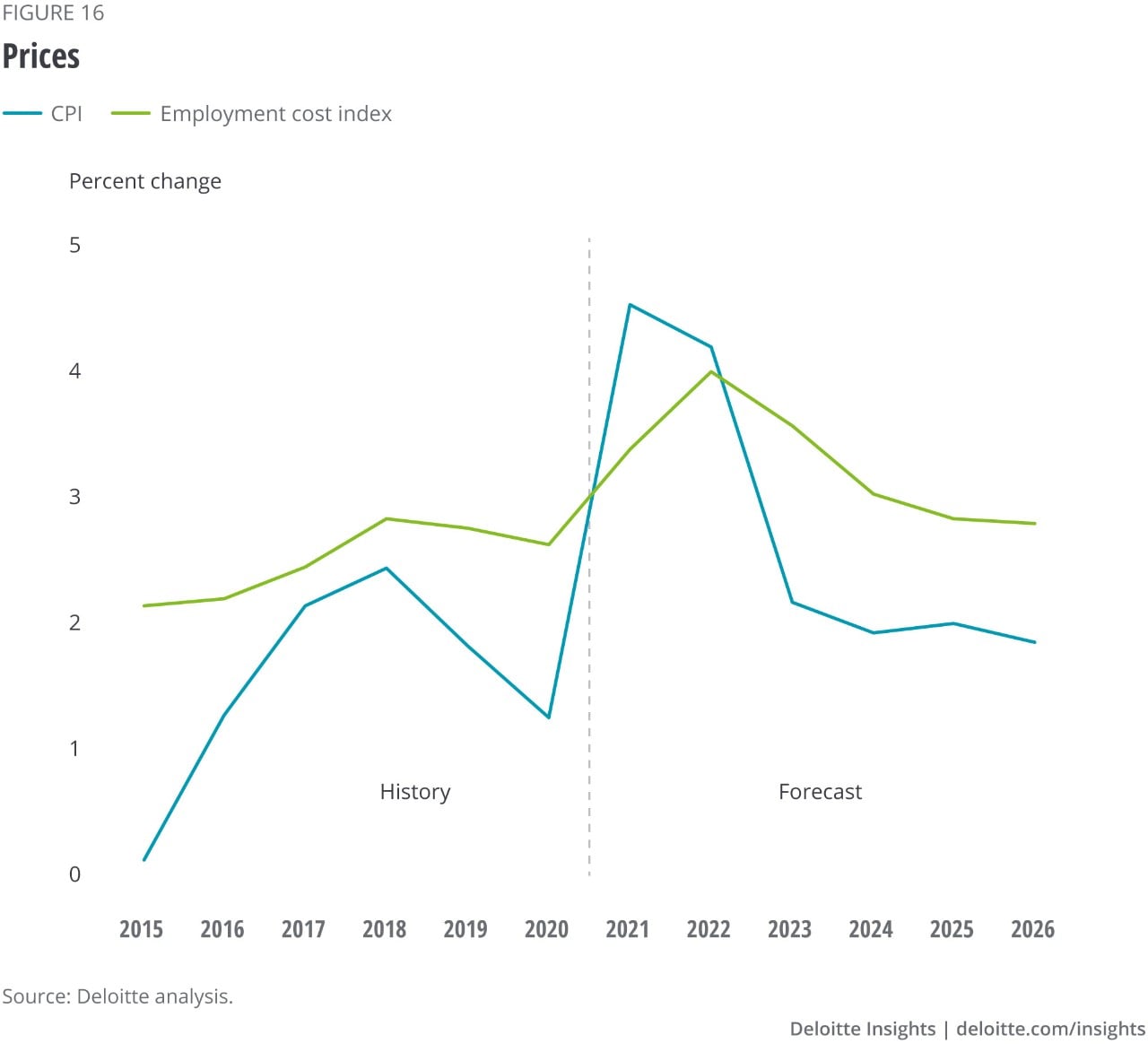

The news media has been flooded with reports about inflation recently. But that commentary is at odds with the actual inflation data. The data indicates the potential for a problem, but there are few signs of a significant increase in inflationary pressures of the type that required a severe recession (in 1982) to reverse.

CPI inflation first accelerated in March 2021, although the March increase was mainly due to higher energy costs. The next three months—April to June—saw much higher core inflation. Most of the acceleration, however, was due to a few specific pandemic-related categories. And then inflation decelerated back to acceptable levels for three months,11 although the news media ignored this. However, many economists understood that the signals were consistent with the “transitory” inflation story the Fed was describing.

In October, inflation accelerated again, and the acceleration was more widespread than in the April–June period. Much of the October’s inflation reflects the same supply chain issues as were exposed earlier (especially the lack of computer chips for automobiles). In some cases, hefty price rises have left prices still below their prepandemic level (airfares, for example). And the overall level of inflation (6% on a year-over-year basis) is still relatively mild compared to inflation in the early 1980s (about twice that rate) or in many other countries that have experienced inflationary problems.

But there were some warning signs in the October inflation data. Among them are the spread of inflation to some areas that are not recovering from a postpandemic price decline (apparel, for example), and the rise in shelter prices. Shelter, and its subcomponent that measures the implicit rise in housing prices for homeowners (“owners’ equivalent rent of residences”) appears to respond with a lag to higher housing prices. And housing prices by the widely used FHFA measure are up 27% from the prepandemic level, while owners’ equivalent rent is up just 5.2%. We may see elevated readings for the CPI over the next year as the CPI for shelter catches up with housing prices.

The Deloitte forecast continues to assume that the current inflation is “transitory” in the sense that it will dissipate over time. Companies are already finding ways around many of their supply chain problems, as evidenced by the fact that factory utilization is increasing in most industries (with motor vehicles the striking exception). And our forecast of declining demand for consumer durables suggests that the need for expanded production will gradually decline, reducing the bottlenecks that are currently frustrating producers and leading to higher prices. Our forecast shows inflation remaining at around 3.5% in 2022 before falling back to the 2% range.

Thanks to Lester Gunnion, who played a key role in developing and producing this forecast.

Cover image by: Russell Benfanti