The future of fresh Strategies to realize value in the fresh food category

11 minute read

12 November 2019

Barb Renner United States

Barb Renner United States Brian Baker United States

Brian Baker United States Curt Fedder United States

Curt Fedder United States-

Shweta Joshi India

Shweta Joshi India Jagadish Upadhyaya India

Jagadish Upadhyaya India

Even with rising consumer demand for fresh foods and their prominence in stores, fresh food sales haven’t kept pace with total food sales. How can manufacturers and retailers drive fresh foods growth and realize untapped potential?

Consumer demand for fresh food continues to be strong: Two out of three consumers in the United States report an increase in their category purchases over the last two years.

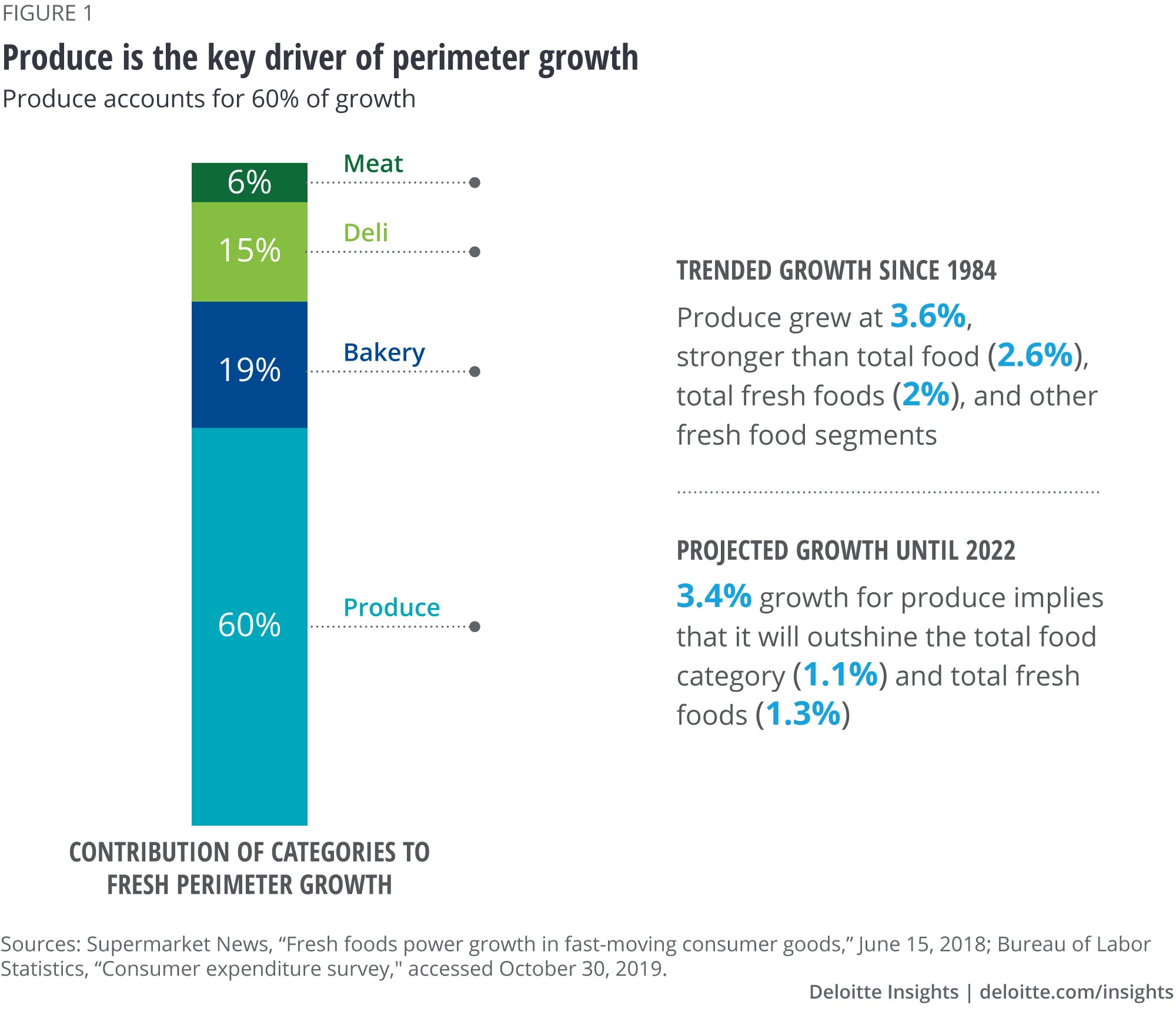

The increase in space allocated to the fresh perimeter of the store reflects the rise in consumer demand. But total fresh sales trail total food sales and are not living up to their potential. In terms of growth, produce is the only bright spot among fresh food segments—a trend projected to continue through 2020. To develop strategies to stimulate fresh food growth, Deloitte conducted surveys with consumers and food industry executives.

Consumer demand for fresh food continues to be strong

Learn more

Explore the Consumer products and retail collection

Read more about the Future of Fresh

In a hurry? Read a brief version from Deloitte Review, issue 27

Download the issue

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

Walking into a typical grocery store, the first thing consumers encounter is a dazzling array of fresh produce. As consumers circle the perimeter of the store, they encounter more fresh items: meat, fish, and dairy, to name a few. Nearly all consumers purchase some form of fresh foods monthly. Given the nature of this category, 74 percent buy fresh foods at least once a week. In terms of their fresh budget, over 60 percent of consumers spend up to a third of their average grocery budget on this category. Even though price is an important consideration for most, fresh foods purchases are also motivated by consumers seeking healthier versions of the food they purchase (80 percent) and avoiding preservatives and chemicals (77 percent).1

The importance of the fresh food category

The allocation of space devoted to fresh foods reflects the rise in consumer demand. From October 2015 to October 2016, the fresh perimeter of the store grew 2.1 times in comparison to the total food and beverage space. According to a Nielsen study, fresh foods are the primary driver of growth in retail stores, accounting for 49 percent of all dollar sales growth in the fast-moving consumer goods (FMCG) industry.2

But, sales in the fresh perimeter of the store are lagging total store sales and are not commensurate with the space devoted to the category. Total store sales between October 2015 and October 2018 grew 4.3 percent, whereas fresh perimeter sales grew only 4.0 percent, from US$171 billion to US$178 billion, during the same period.3 Much of the fresh perimeter growth was driven by produce (see figure 1).

With fresh growth rates not living up to their potential, a key question emerges: considering the prominence given to fresh foods in stores, how can manufacturers and retailers grow the fresh food category and realize untapped potential? To answer this critical question, a comprehensive understanding of the fresh food category should be considered from the demand side (consumers) and the supply side (manufacturers and retailers). We conducted extensive market research with both audiences to understand their motivations, drivers, and challenges (for more details, see the sidebar, “About the surveys”).

About the surveys

To gain deeper insight into fresh food consumers as well as fresh food manufacturers and retailers, Deloitte conducted two proprietary, quantitative surveys among consumers and food industry executives:

- Consumers: The respondent group comprised 2,000 adults in the United States, aged 18 to 70. To qualify for participation, respondents were influencers of fresh food purchases: 94.0 percent purchased fresh food more than once a month. To attain a representative view of the average US consumer, the demographic composition was mapped to the US census. The interviews were conducted in June 2019.

- Food industry executives: For this survey, 153 interviews among fresh food manufacturers and retailers were completed. The interviews were conducted in June 2019.

Definition of terms: For the purposes of the surveys, fresh food was defined as food not preserved (processed, frozen, or with preservatives) or spoiled. It was made clear that it only included fresh fruits and vegetables, meat, seafood, and deli/in-store food. Vegetables and fruits were defined as produce that has been recently harvested and treated properly postharvest. By meat, we meant meat that has recently been slaughtered and butchered. For fish, our description was that it has been recently caught or harvested and kept cold.

The fresh food consumer—not all consumers are alike

Current industry and media attention tend to paint fresh food consumers as one homogenous group—typically labeled as “health-conscious.” It’s true that, to some extent, fresh food buyers are similar in many ways. Overall, they:

- Are health-conscious and actively avoid chemicals in their food

- Trust fresh food to take care of their daily nutritional requirements and feel satisfied after consuming it

- Are concerned about food waste and troubled by pollution caused by mass food production

- Consider sustainability aspects when purchasing perishables

- Do not understand the difference between concepts of fresh, organic, natural, etc., and are unsure if organic food is better for them

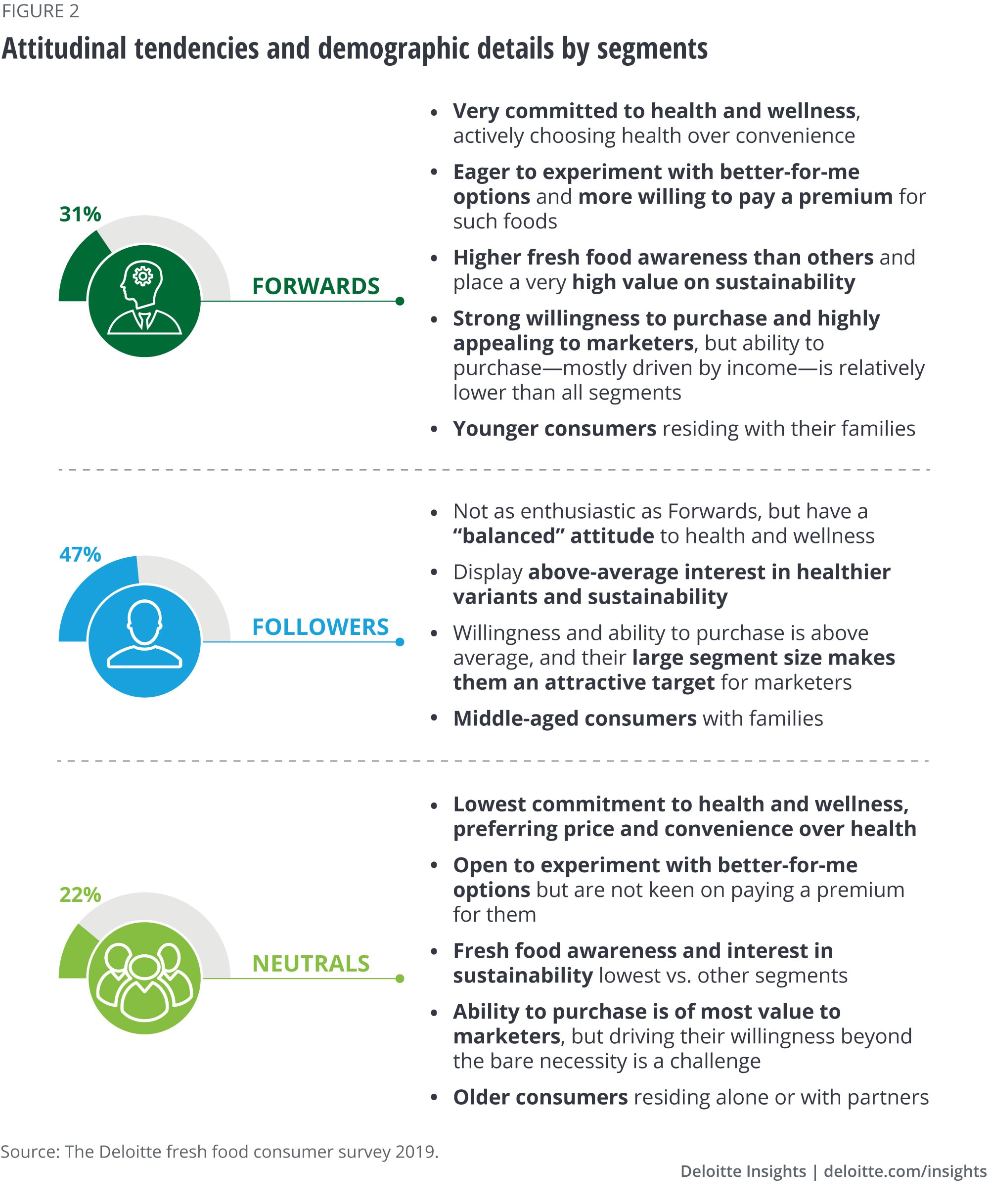

However, viewing all fresh food consumers through a single lens can limit the value that manufacturers can extract from this category. This is because analyzing at an overall level might lead us to believe that all fresh consumers behave alike. But consumer segmentation based on attitudes, made possible through advanced statistical analysis (cluster analysis), and their profiling based on purchase behavior, reveals three personas: Forwards, Followers, and Neutrals—each with their distinct expectations and buying patterns (see figure 2).

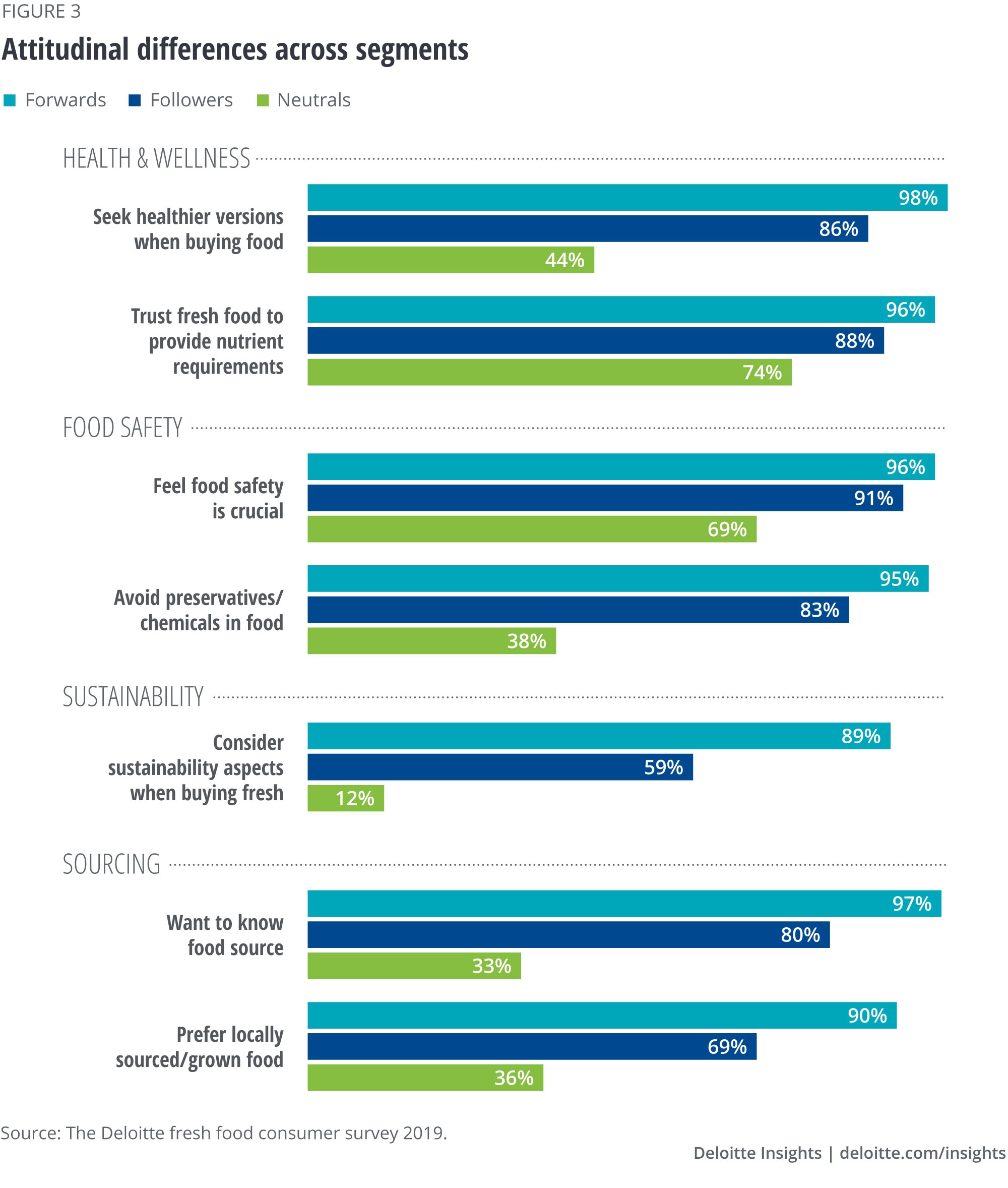

Delving further into the attitudes displayed by the three segments reveals how the personas cover the behavioral spectrum in each of the aspects of health and wellness, food safety sustainability, and sourcing (see figure 3). In most cases, responses from Forwards hit the positive end, Neutrals are on the negative end, and Followers are somewhere in the “rational” middle. This underscores the need to potentially look beyond an aggregated view of consumers and address the needs of each segment separately to extract greater value from the fresh foods category.

The role of health and wellness, price, and convenience

In general, when purchasing any product, consumers tend to make judgments about the importance of incomes and convenience. In terms of fresh food, health and wellness and sustainability concerns also play a significant role. When asked directly about the importance of these factors, consumers assigned high value to all of them. To tease out the influence of each and delve deeper into consumers’ judgment criteria, we applied another advanced statistical approach (trade-off/forced choice analysis).

Our analysis revealed the importance of these factors varies by consumer segment (see figure 4). For Forwards, health and wellness surpasses other factors. As such, this group is more likely to pay a higher price for fresh foods. However, for the other segments, which account for over two-thirds of consumers, price rises to the top. This suggests there is likely a price threshold these consumers will not cross, and that competitive pricing remains important to them. Interestingly, among Forwards, health and wellness concerns rise to the top when considering other types of food as well. This suggests that their desire for health and wellness products is a function of their attitudes rather than age—which also implies that as Forwards age, they will likely maintain their beliefs and not necessarily become Followers. They are more likely to evolve into a new segment interested in fresh foods comprising middle-aged adults with higher incomes. This suggests the need to revisit this segmentation every three to five years due to the dynamic nature of this evolving category.

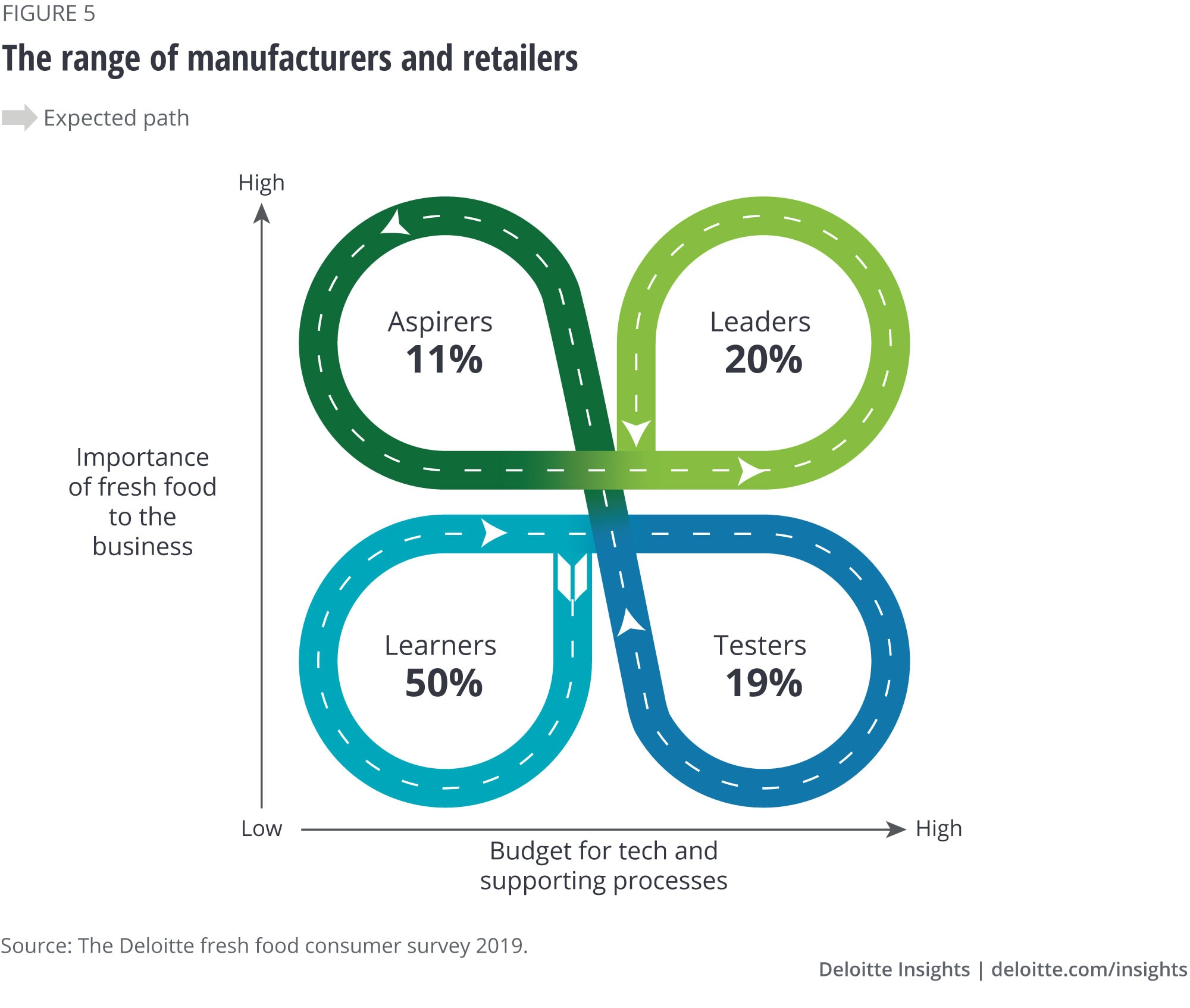

The range of manufacturers and retailers—modeling the behavior of leaders

Now let’s focus on the challenges and opportunities manufacturers and retailers face when marketing to the fresh foods consumer. When assessing companies on the criterion of percentage of revenue from fresh foods in relation to the annual budget for technology and supporting processes, four types of organizations emerge. We classified 20 percent as Leaders.

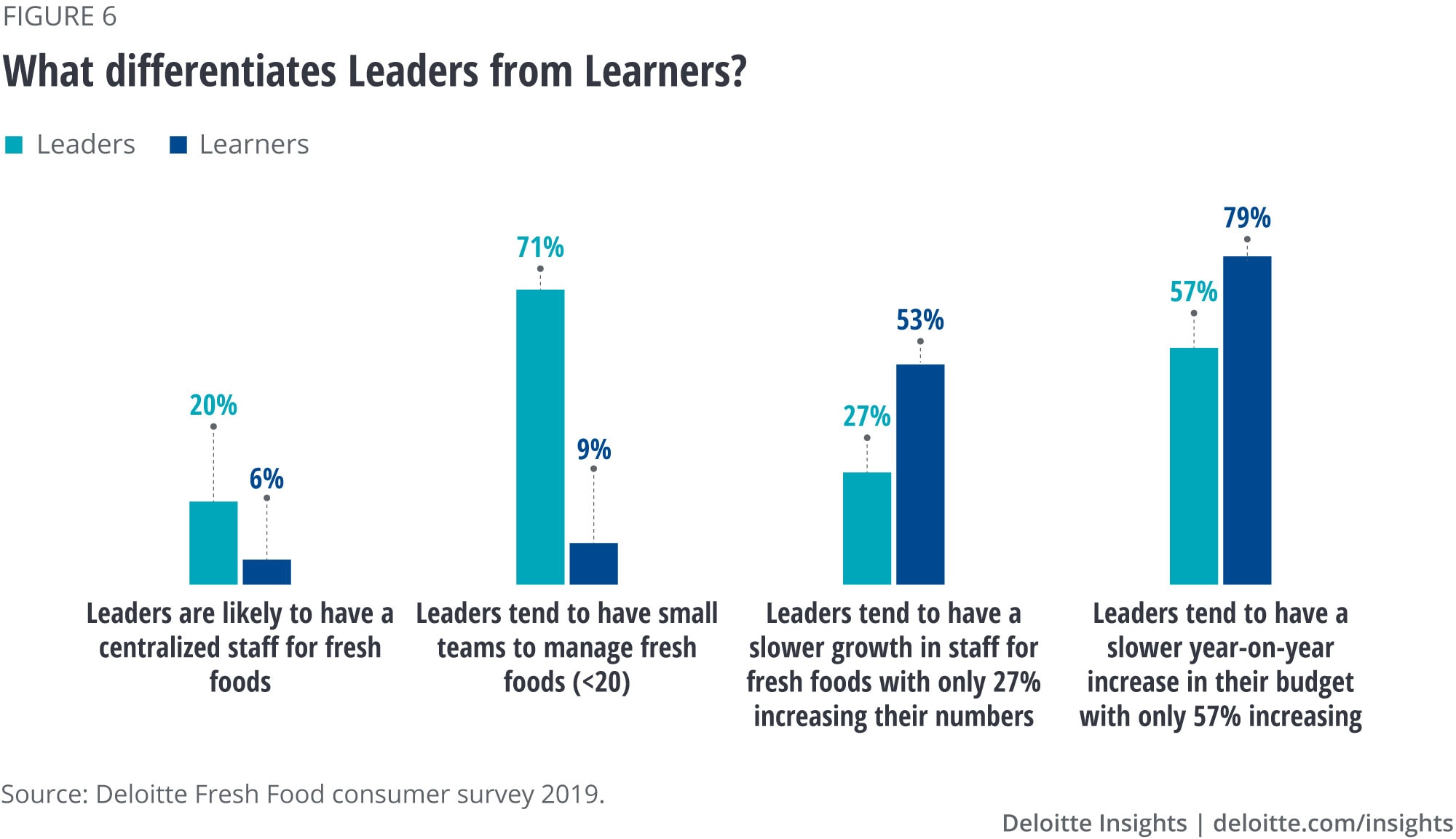

Leaders are organizations with a higher percentage of centralized staff (20 percent) as compared to Learners (6 percent) (see figure 6). Leaders also tend to have a greater focus on fresh foods as compared to Learners who have a more diversified portfolio.

With stronger investments in technology and supporting processes, Leaders are achieving higher fresh food sales with smaller teams. They are also taking a more cautious approach to growing their fresh food teams compared to Learners (see figure 6). This suggests Leaders may have invested in the right talent to achieve more with less. Investing in the right talent, combined with a centralized staff that provides greater visibility to fresh food processes, is likely helping leaders gain economies of scale, improve sales, and land in the top-right quadrant.

There is a path, however, for Learners to become Leaders. Learners could enhance their budget for technology and supporting processes to transform into Testers. Then, by focusing on efficiencies, Testers may improve their revenue from fresh foods and transform into Aspirers, and, eventually, Leaders.

Technology is an enabler of growth for both Leaders and Learners. All organizations would likely benefit from an assessment of their technology capabilities to chart a way forward. In general, as more companies place increasing emphasis on technology, implementation of more basic technologies (such as cold chain monitoring, quality sensors, and automation for on-farm handling and smart packaging) tends to be equal for both Leaders and Learners. And both Leaders and Learners are in the early stages of adopting advanced technologies (such as automation and robotics; blockchain; and big data and analytics).

Overcoming barriers to implementing technology and in the supply chain

Manufacturers and retailers could benefit from addressing the main barriers prohibiting technology implementation, which are “time required” (cited by 78 percent) and “lack of skilled talent” (cited by 28 percent). Similar barriers exist in implementing big data and data analytics. It’s interesting that time is the standout barrier—a full 50 percentage points higher than the next highest barrier, talent. Time may relate to several factors specific to the fresh food ecosystem:

- Companies may not be aware of newer technologies that have significantly reduced implementation time as well as time to help identify return on investment (ROI) compared to systems they had adopted in the past.

- Capturing ROI in this space can be problematic since most fresh departments tend to not have perpetual inventory (PI) or have master data created and managed in a way that will enable the level of discrete tracking required to successfully measure improvement based on newer technology.

- Further, as our research indicated, most companies do not have centralized fresh teams, thus making it difficult to get the right level of support to effectively architect and implement fresh systems.

- Lastly, there may be a cultural component to overcome, since companies tend to be more comfortable with systems that have traditionally worked for them in the past vs. newer ones.

Overcoming challenges in the fresh food supply chain could benefit both manufacturers and retailers (for example, see the sidebar, “From frozen to fresh”). The challenges faced by manufacturers focus on quality control of raw materials (25 percent), and storage and processing (20 percent for both). For retailers, however, the top three challenges are spoilage (32 percent), storage at the retail warehouse (24 percent), and product pricing (16 percent). Note that storage is a common issue for both groups. Spoilage is the biggest challenge retailers face. Spoilage is a significant issue in the United States, where approximately 50 percent of all produce is discarded—which roughly translates to US$160 billion annually.4 The potential to recoup this loss exists: A study by the UK Waste & Resources Action Program (WRAP) predicts that a 20 to 50 percent reduction in waste could save the industry between US$120 billion to US$300 billion.5

From frozen to fresh

McDonald’s transitioned from using frozen beef to fresh beef in Quarter Pounders in most of its US stores. This required revamping the complete supply chain: packaging equipment at suppliers, distribution trucks to maintain temperature during transit, and training of in-store employees to implement new food safety practices. Applying new technology in its supply chain and supporting this change with a marketing campaign helped McDonald’s boost year-on-year sales of Quarter Pounders by 30 percent and increase market share.6

Strategies to realize value in the fresh food category

Insights from our consumer and food industry executive surveys suggest there’s ample opportunity to stimulate the fresh food segment to realize untapped value in the market. This can be accomplished by both stimulating consumer demand and helping manufacturers and retailers operate more efficiently.

Stimulating consumer demand

To stimulate consumer demand, manufacturers and retailers would likely benefit from nuanced consumer segmentation and targeting similar to the segments we’ve identified. Apart from assuming health-conscious consumers would most likely be targets for fresh food, manufacturers have barely made any attempts to distinguish between consumers. This can draw their attention primarily toward consumers that exhibit characteristics of Forwards, leading to missed opportunities with Followers.

Conventional wisdom suggests that marketing to Forwards to maximize potential buying power could be most advantageous. While this is likely true, our research also indicates that at least for now, they have limited purchasing power. Instead, our research suggests that due to their size, there’s upside potential to grow fresh food purchases by expanding the target beyond Forwards to include Followers (who represent 47 percent of fresh consumers) due to their size and stronger purchasing power.

This finding is supported by an analysis of the US consumer expenditure survey, which demonstrates that middle-aged consumers (aged 35–64) have higher-than-average incomes and spend more than the average on fresh foods.7 Marketing to Neutrals may be a tougher challenge. But, by talking directly to Followers, there would likely be a trickle-down effect to Neutrals.

Targeting Followers can be accomplished through both media choices and communications. Media choices could include less emphasis on social media (which appeals to Forwards) and more presence in traditional print (magazines and newspapers). In terms of messaging, when communicating with Followers, the role of competitive pricing should not be discounted since they appear to be more price elastic than Forwards. Efforts to increase their fresh purchases could start with pricing and progress to consumer education. Highlighting the value proposition of fresh foods by consistently communicating the benefits of healthy eating and positively affecting their attitudes toward food safety, sourcing, and sustainability may further result in increased consumer spending on fresh foods.

Helping manufacturers and retailers operate more efficiently

There is potential for manufacturers and retailers to more efficiently manage the handling of fresh foods through modeling the key behaviors of Leaders, centralizing the fresh foods staff, and addressing specific manufacturer and retail challenges identified. This could result in lower costs to the consumer and, in turn, boost sales.

Technology solutions have the potential to address these barriers, while simultaneously alleviating concerns raised about time and talent required to implement them. These potential solutions could be designed to:

- Predict freshness: The traditional fresh food value chain is changing into a digitized always-on and fully integrated digital supply chain network powered by real-time data analytics. Even before a fresh food product is harvested, intelligent algorithms can analyze and estimate the quality and freshness of a harvest based on growing conditions. This information is communicated by sensors to create a digital measure of the freshness of the food and allows for the deployment of customized logistics.

- Improve supply chain management: As businesses face unanticipated disturbances in the distribution processes, dynamic supply chains can quickly identify alternative options for moving the highest quality product available at the right time through the right delivery channels. With complete supply chain transparency, the food that customers buy is always verifiable and food safety issues are identified before the product reaches the store or leaves the store shelf.

- Apply advanced analytics: Cognitive algorithms and real-time analytics go beyond traditional supply chain analytics and create an integrated network that is self-correcting. Changes in physical handling conditions are quickly diagnosed and communicated to maintain consistent product flow.

- Improve store operations: Store operations are augmented by digital workflows, removing employee guesswork out of predicting customer demand, managing inventory, and keeping the right stock on the shelf. The store becomes a reactive exhibit of freshness.

Conclusion

The future of fresh appears promising. There’s untapped consumer demand and multiple opportunities for manufacturers and retailers to more efficiently provide fresh foods to consumers. As Forwards grow older, and their incomes increase, it’s likely their dedication to fresh foods will continue. Additionally, if demand can be stimulated among the largest group of fresh consumers, Followers, even small increases in this group would be beneficial to the broader fresh food category. Such targeted consumer analysis, coupled with efforts from manufacturers around integrating the supply chain and improving efficiencies through the use of technology, can truly help realize the growth potential of fresh foods.

Consulting Services for Consumer Products

The consumer products industry today faces virtually unprecedented challenges and opportunities. Eroding brand loyalty, increased merger and acquisition activity, enduring recessionary consumer attitudes and the rising influence of digital technologies on shopping behavior all threaten traditional business models–but also give rise to new and exciting ones. In the face of changing consumer needs and behaviors, Deloitte’s Consumer Products team is working with clients to strengthen analytics, improve internal operations and develop new market-facing capabilities and channels. With experience across a wide range of sectors–including food and beverage, personal and household goods, agribusiness, apparel and footwear, and household durables–we position our clients to lead in the face of change.

Learn more

Get in touch

- Barbara L. Renner

- Partner

- Deloitte Tax LLP

- brenner@deloitte.com

- +1 612 397 4705

Related content

Explore consumer products and retail

-

2023 Deloitte holiday retail survey Article8 months ago

2023 Deloitte holiday retail survey Article8 months ago -

The consumer is changing, but perhaps not how you think Article5 years ago

The consumer is changing, but perhaps not how you think Article5 years ago -

Capturing value from the smart packaging revolution Article5 years ago

Capturing value from the smart packaging revolution Article5 years ago -

Cyber risk in consumer business Article 7 years ago

Cyber risk in consumer business Article 7 years ago -

The great retail bifurcation Article6 years ago

The great retail bifurcation Article6 years ago -

Looking beyond millennials for brand growth Article5 years ago

Looking beyond millennials for brand growth Article5 years ago