Təfərrüatlar

Base Erosion and Profit Shifting (BEPS)

Tax is in the headlines in a manner few could have predicted – even a year or two ago. This has led to a range of issues for businesses to consider, including the OECD's Base Erosion and Profit Shifting project.

Mətn ilə tanış olun

- About BEPS

- OECD time table and actions

- International tax reform and transparency

- Global debates on responsible tax, anti-avoidance and BEPS

About BEPS

The OECD began work on their BEPS project to address concerns that current principles of national and international taxation were failing to keep pace with the global nature of modern trading and business models. In particular, a perception that existing rules give businesses too much opportunity for arbitraging tax rates and regimes.

While views vary, one clear and consistent message is that the matters on the OECD Action Plan agenda are set to significantly shape the means by which governments collect tax and companies align their tax affairs and business models in the decade ahead. Given the OECD’s pace of work, change is inevitable and will be swift.

Endorsed by the G20 Finance Ministers and Central Bank Governors, the Action Plan will likely be delivered in a short 18 to 24 months timeframe.

View the OECD’s site on Base Erosion and Profit Shifting here.

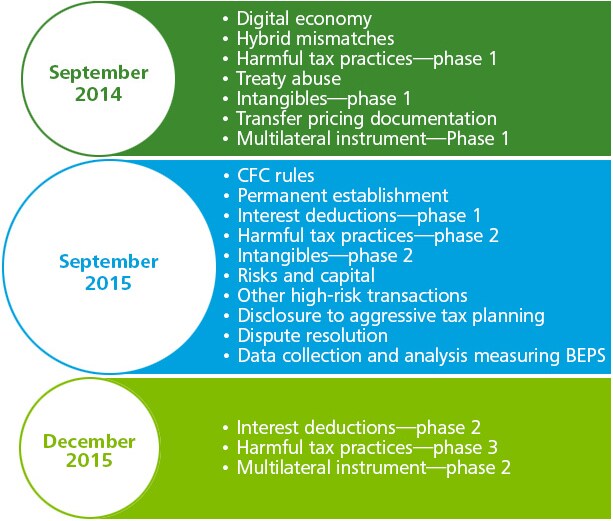

OECD Timetable and actions

OECD’s BEPS Action Plan identifies fifteen specific actions that are needed for governments to address the challenges outlined above. The OECD has set the below timeline for itself to address these fifteen actions in three phases.

Click on each of the links below to find a brief description and expected output of each of the 15 BEPS Actions, along with related documents, commentary, and videos.

|

|

|

|

|

|

|

Limit base erosive via interest deductions and other financial payments |

|

Counter harmful tax practices more effectively taking into account transparency and substance |

|

|

|

|

|

|

|

|

|

|

|

Establish methodologies to collect and analyze data on BEPS and the actions to address it |

|

Require taxpayers to disclose their aggressive tax planning arrangements |

|

|

|

|

|

Major changes: International tax reform and transparency

A briefing paper from Deloitte UK discusses two major tax issues affecting businesses today: international tax reform (OECD’s Base Erosion and Profit Shifting (BEPS) project) and corporate transparency about their tax affairs.

Tune into the Topic: Global debates on Responsible Tax, Anti-avoidance, and BEPS

Discussion and perspective on current tax topics and BEPS from Deloitte partners from Belgium, Canada, the United States, the UK, and France.

Major changes: International tax reform and transparency

Tune into the Topic: Global debates on Responsible Tax, Anti-avoidance, and BEPS