deloitte-private-global-survey

Perhaps no other crisis in modern history has had as great an impact on daily human existence as COVID-19. And none has forced businesses throughout the world to accelerate their evolution as their leaders worked to respond and recover on the way to thriving in the postpandemic environment.

Deloitte Private’s latest global survey of private enterprises reveals that executives in every region used the crisis as a catalyst, accelerating change in virtually all aspects of how we work and live. They stepped up their digital transformation through greater technology investment and deployment. In-progress initiatives were pushed toward completion, while those that were on the drawing board came to life. They sought out new partnerships and alliances. They pursued new opportunities to strengthen their supply networks and grow markets. They increased efforts to understand their purpose beyond profits, seeking new ways to grow sustainably and strengthen trust with their employees, customers, and other key stakeholders. They also embraced new possibilities in how and where work gets done.

In other words, as the world slowed, the pace of change picked up speed.

If there’s one overarching theme that has supercharged these efforts along the way, it’s been the importance of resilience. How can they best position their organizations to handle not just the next crisis, but all of the other competitive threats and disruptions that are inseparable from doing business around the world today?

The survey showed that many private enterprises see themselves as well on their way to becoming more resilient. In addition, their resilience is informing their outlook—more resilient organizations are more confident about their future, more inclined to invest for growth, and more advanced in their thinking about their purpose and role in society.

Moving forward, moving faster

The executives we polled say that in just about every business area, their company accelerated their plans, whether it was undergoing digital transformation, embedding purpose into their strategy, refocusing on important priorities such as sustainability, or other steps meant to make them more competitive and relevant in today’s business climate.

In this year’s survey, we took that thinking a step further, asking the respondents to reflect on seven elements of organizational resilience:

- Strategy: Defining the transformation journey and ambition

- Growth: Driving customer focus, product innovation, and revenue growth

- Operations: Transforming and modernizing operations

- Technology: Accelerating digital transformation

- Workforce: Transforming the work, workforce, and workplace

- Capital: Optimizing working capital, capital structure, and business portfolio

- Society: Stewarding environmental and social resources

The executives believe growth and technology are among the most important elements for resilient organizations. But they also see the need to align their strategy and ambitions, invest in their people, strengthen their capital position, and steward environmental and social resources (figure 1).

Lingering COVID-19 risks

The global COVID-19 pandemic has wreaked havoc on private businesses around the world. Supply chains—which 60% of our respondents believe need to be redesigned as a direct result of the pandemic—were stressed like never before, with trade corridors temporarily severed and manufacturing capacity greatly reduced.

Many companies have brought the future of supply networks closer, considering not just efficiency but also resilience and redundancy. They are using the crisis to better understand their interdependencies and increasing investments in areas such as digital supply networks to better anticipate, sense, and respond to unexpected changes.

Our respondents believe the wide-ranging impacts from the pandemic will continue to be felt not just for the next 12 months, but for the next several years.

While COVID-19–related risks are front and center, leaders must be careful not to let others go unattended. They will still need to stay ahead of constantly evolving challenges like cyberattacks and increased market competition, and likely dedicate greater attention to environmental, sustainability, and governance (ESG) issues and the impact of climate change on their operations.

Expecting a rebound

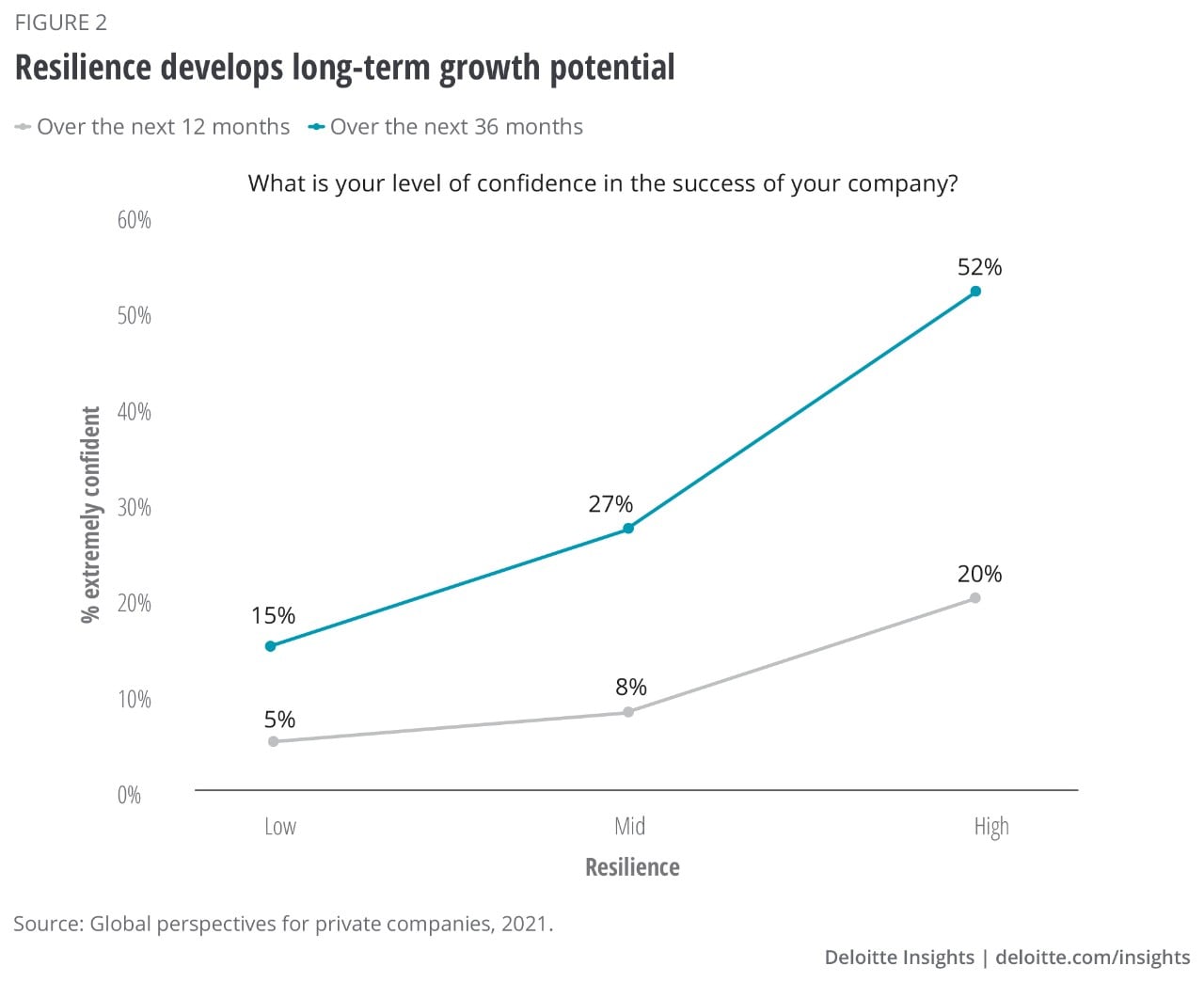

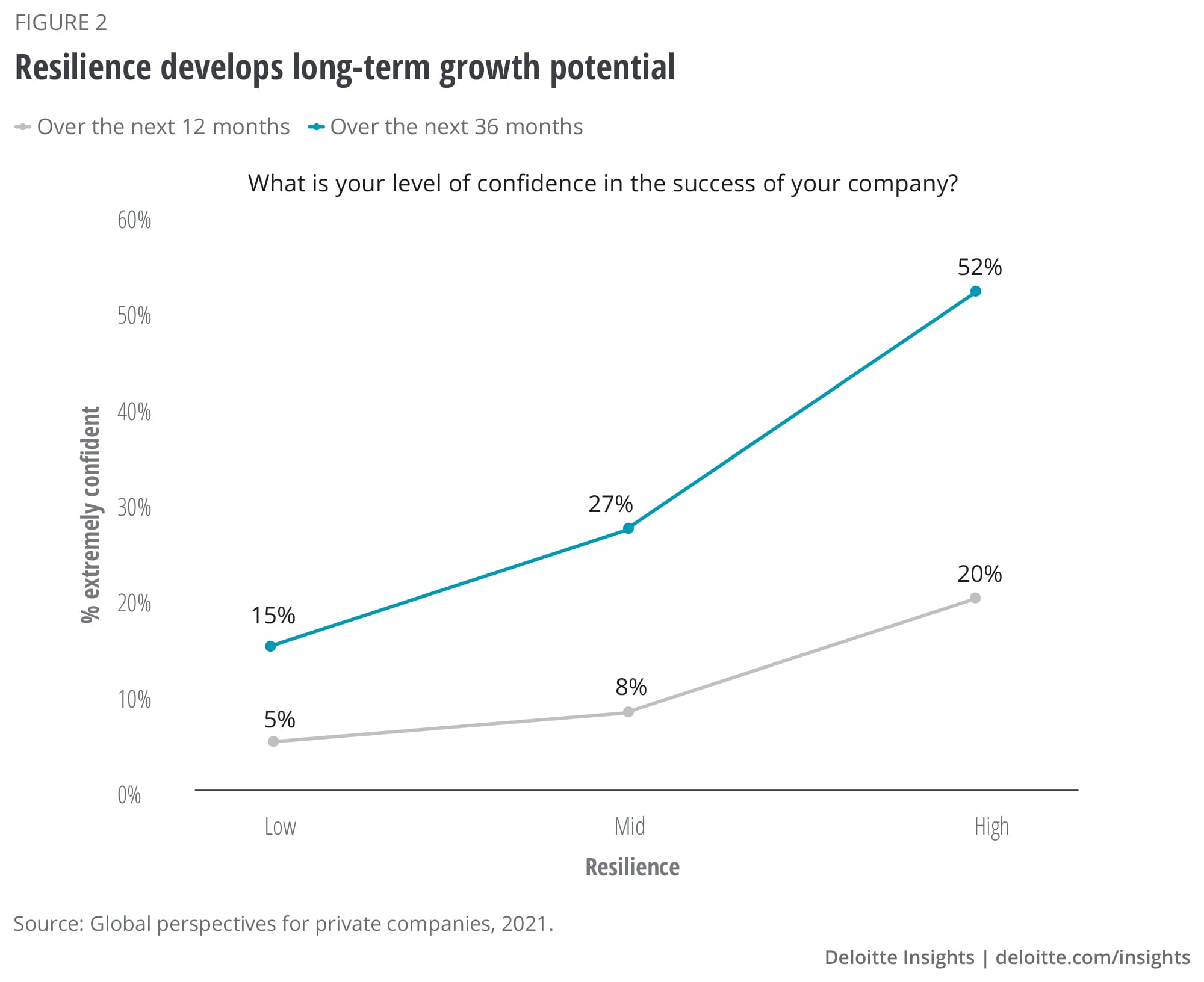

Despite a slight decline in revenue growth expectations for the next 12 months, the survey shows that the majority of respondents believe their companies will snap back from the crisis, with more than two-thirds expressing high confidence in their company’s success during the next 12 months. Here, the most resilient organizations are also the most optimistic (figure 2).

The executives are most confident about their ability to boost productivity, an objective that also shows up as their top growth strategy for the coming year. But digital transformation is also rated highly. The difference in how highly resilient companies view the importance of digital transformation to their growth versus those with low resilience was 18 percentage points, the widest gap in the survey.

While organic growth was prioritized by most respondents over mergers and acquisitions as a main growth strategy, many characterize their company as likely or very likely to be acquisitive over the next 12 months. Highly resilient enterprises are likely to be the most active.

M&A is poised to have an outsized influence in shaping the post–COVID-19 landscape, with companies adopting a combination of defensive and offensive strategies to safeguard existing markets, accelerate their recovery, and position themselves to capture market leadership. Sustainability is also likely to be a cornerstone of deal-making in the new era, as it intertwines with corporate purpose to define commercial success.

Workforce plans

The companies in our survey express caution about their hiring plans for the coming year, with only 11% predicting an increase in headcount and 8% projecting a decline. The remaining 81% of the market is split between holding current employment levels steady, hiring on a contract basis, or hiring on a limited basis.

Leading businesses are beginning to integrate well-being into work by focusing on meeting the needs of various worker segments, building digital wellness and productivity, and giving workers more autonomy to make meaningful decisions about what and how they contribute.

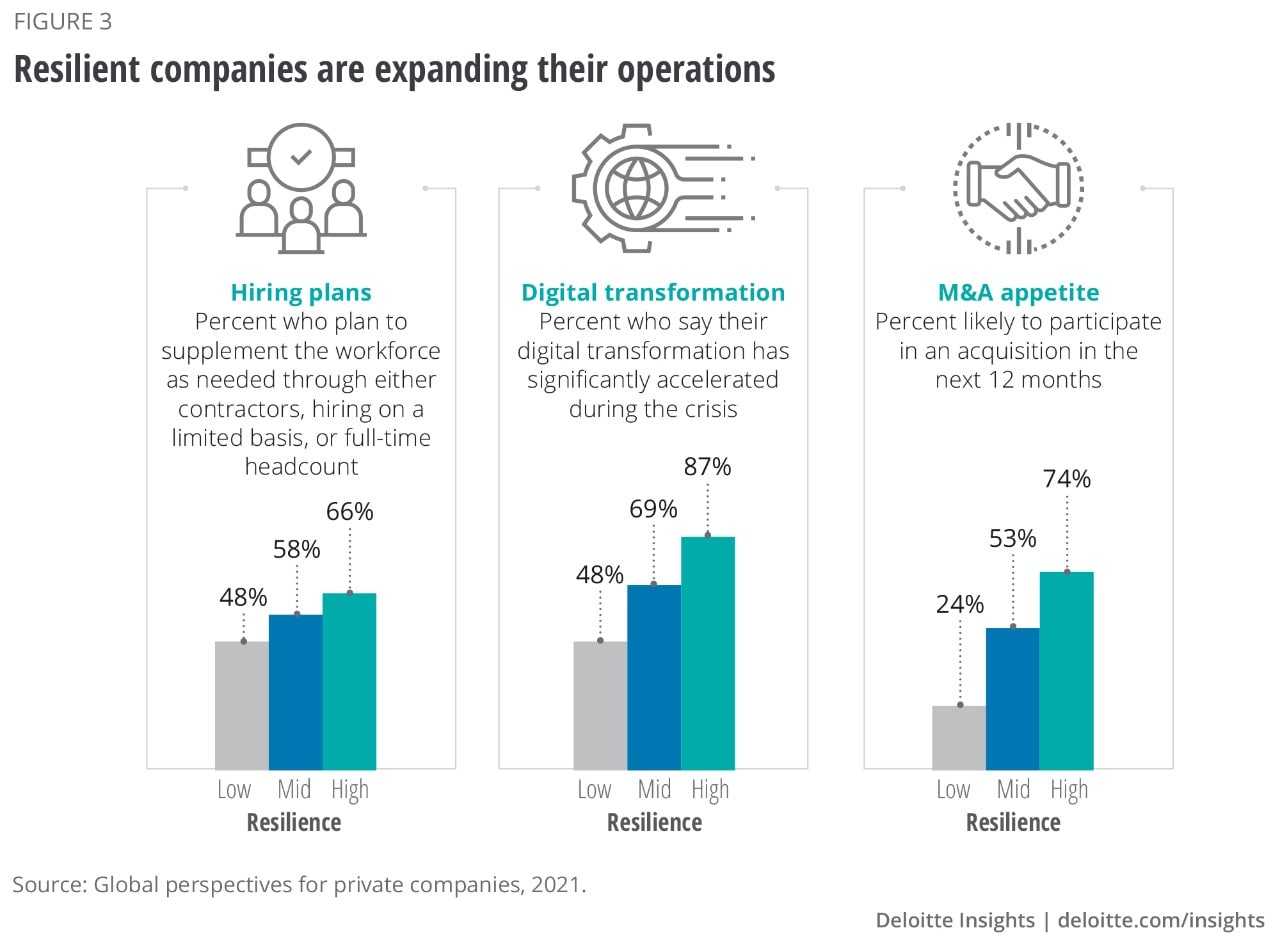

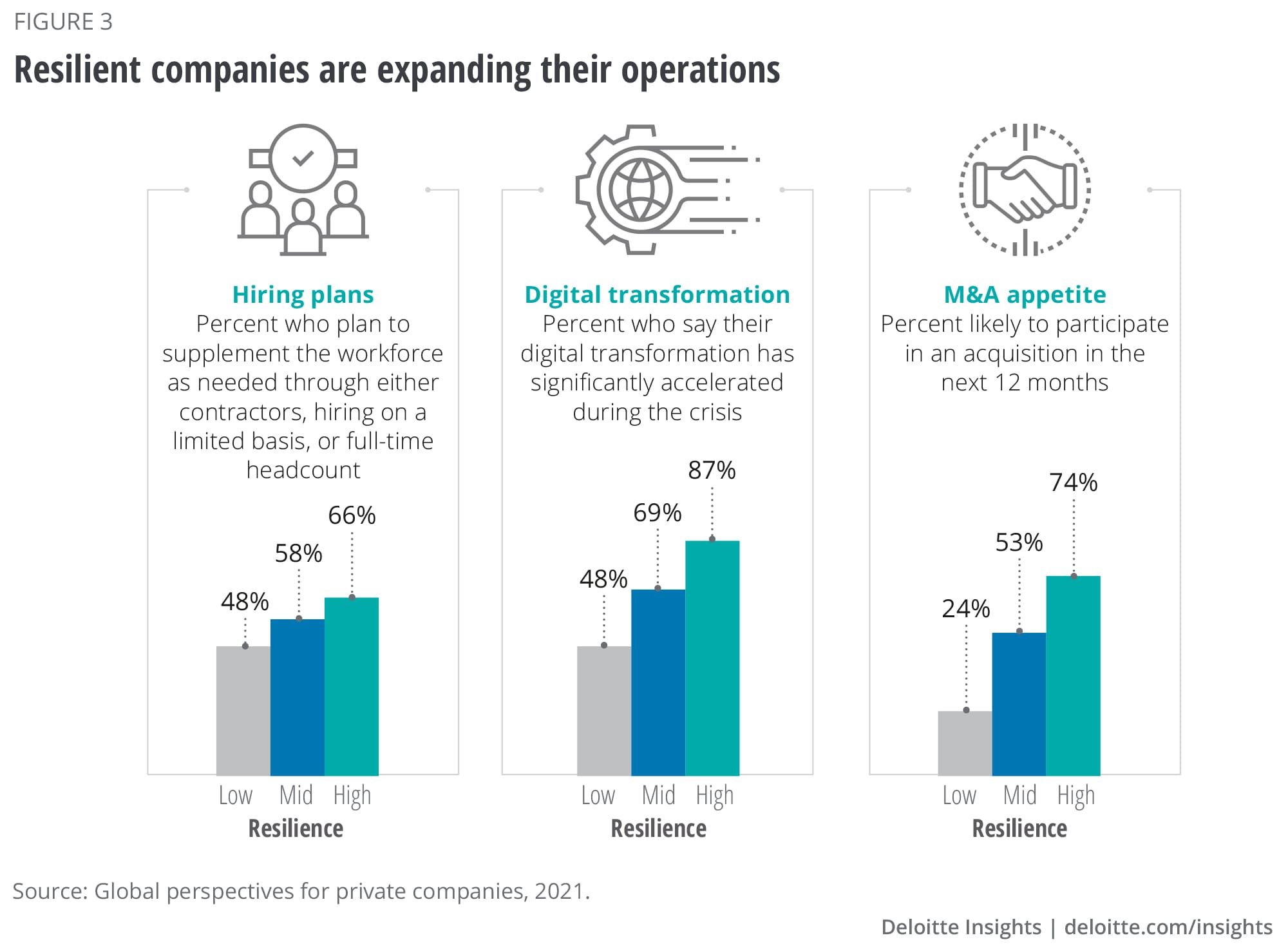

Some private companies have already laid the groundwork for this through flexible workforce arrangements and by redesigning their organizations to be more agile and accomplish more with smaller, independent teams. Such moves have helped private companies in our survey build resiliency—19% say they have fully transformed the nature of work at their organizations already and 38% say they are midway through such changes. And now those efforts are positioning them to add to their ranks, as those with high resilience scores say they are more likely to supplement their workforce in the coming year than those at the low end (66% vs. 48%; figure 3).

Leveraging a diverse and inclusive workforce, among the least important growth strategies for companies with low resilience scores, was a much higher strategic priority for those in the top tier.

Digital transformation

Our survey finds the executives have broad expectations about the gains that technology investments will deliver for their organizations. Among other benefits, they believe digital transformation will help improve customer engagement, boost sales volumes, strengthen their ability to manage, and minimize costs. Many of them are much closer to realizing these ambitions than before the pandemic.

Highly resilient organizations were nearly twice as likely (80% vs. 43%) as those with low resilience scores to say that their process of digital transformation was either conducted prior to the crisis or is currently underway (figure 3).

Information security is primed to be the most popular technology spending area in the coming 12 months, but cloud computing and data analytics are close behind. A significant portion of the respondents also predict their companies will invest in emerging technologies, such as robotics, autonomous vehicles, and drones.

{kind=link}

{kind=link}

Redefining purpose and trust

Our survey shows the already widespread efforts around purpose and trust took on new meaning last year. Almost 70% of the respondents said purpose increased in importance for their organization as a direct result of the COVID-19 crisis, with Asia/Pacific leading the way.

Employees whose safety is prioritized trust their employers to continue to do right by them and put their needs first. Transparency is also critical: In a March global roundtable of organizations that hold Deloitte’s Best Managed Companies distinction, executives highlighted the importance of frequent, open communications as a key ingredient in building trust with their employees, especially in times of uncertainty. Trust is also a central issue when it comes to the imprint companies leave on the world.

Maintaining a sense of urgency

We hear time and time again that being private affords companies a certain degree of nimbleness, which can matter greatly at critical inflection points. Still, even the most visionary private companies had to be surprised at how quickly the future has arrived, in large part due to the COVID-19 pandemic.

Agility, purpose, culture, and the ability to maintain a long-term view have helped private companies during the pandemic accelerate their transformation. We are gaining a better understanding today of the qualities that help leaders build more resilient organizations and how they enable their companies to think and act differently. We are also learning how resilience is informing the leaders’ outlook and driving them to be more confident and future focused.

We may never see another pause on activity like we saw due to COVID-19. Acceleration and resilience will likely prove to be themes with plenty of staying power. The challenge for private company leaders is to embrace and embed both throughout their organizations.