Predictions

VoLTE / VoWiFi — capacity, reach, and capability

TMT Predictions 2016

Executive summary

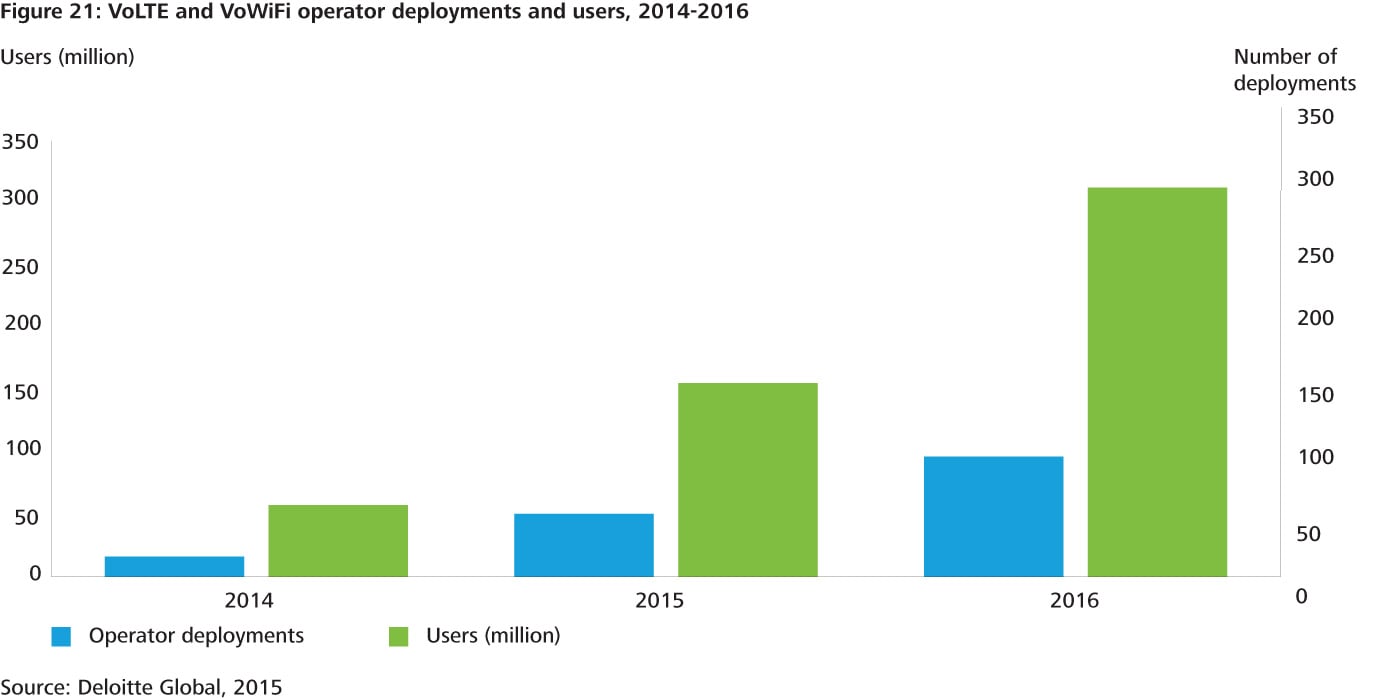

Deloitte Global predicts about 100 carriers worldwide will be offering at least one packet-based voice service at the end of 2016, double the amount year-on-year, and six times higher than at the beginning of 2015. We estimate that approximately 300 million customers will be using Voice over WiFi (VoWiFi) and / or Voice over LTE (VoLTE); double the number at the start of the year and five times higher than at the beginning of 2015.

For most carriers launching VoLTE or VoWiFi in 2016, the primary motivation is likely to be to increase network capacity and extend the reach of their voice services. While VoLTE or VoWiFi technologies enable a range of value-added services, such as video calling, we expect the majority of carriers to exploit this additional functionality in later years, with the initial focus being on coverage and capacity.

VoLTE increases capacity as it allows operators to move voice calls off 2G and 3G networks and onto the LTE (4G) network. The often lower frequency spectrum that is freed up can be reused for data services. Additionally the LTE interface is more efficient at carrying calls relative to traditional calls: it can support up to twice as many voice users in a given bandwidth (per megahertz). Additional cost savings can be obtained from retiring legacy infrastructure, and not having to run two infrastructures in parallel, one for data and one for voice.

VoLTE also offers a range of enhancements over standard voice. For example it offers the ability to use a data connection while being on a call, superior voice call quality, faster call connection, fewer dropped calls and the ability to switch from a voice call to a video call. However while early adopters in 2016 are likely to be most fervent users of this additional functionality, many users may not notice the variation in voice quality.

Carriers are likely to use VoWiFi to extend coverage, particularly indoors, and as a result help improve customer satisfaction with the operator and lessen the likelihood of churn. The majority of mobile calls are made indoors (at least twice as many smartphone users make voice calls indoors than outdoors), but providing good internal coverage can be technically complex and expensive, particularly for lower floors and internal rooms. VoWiFi extends reach at a relatively low marginal cost. In some regards VoWiFi may even reduce operator costs, as calls placed on a smartphone would be carried over the consumer’s broadband network, freeing up some cellular capacity.

VoWiFi may at first glance appear very similar to VoIP, but there are two critical differences. Firstly it is a network operator managed and controlled service, which, for users, should mean that the call is less likely to be dropped. Secondly, VoWiFi offers native calling: there is no need to open an app to make or receive calls. A VoIP call can only be received when that specific app is open.

Long term, most operators will likely launch both VoLTE and VoWiFi services as a natural evolution towards IP-based-only communication. However, short term some carriers may decide to launch one of the two services first. The decision will likely be influenced by three main factors: the potential cost savings, the need to improve indoor coverage, and the customers’ interest in enhanced communication services.

Consumers have high expectations for voice quality, so operators should only launch VoLTE and VoWiFi services when those services are stable. Also, carriers should determine how best to advertise the two services so that consumers value the quality of voice calling and perceive the enhancements provided as value added services. This could counteract the declining trend of smartphone users not making phone calls and moving to OTT alternatives.

VoLTE / VoWiFi — capacity, reach, and capability

1 For a complete list of references and footnotes, please download the full PDF version of the TMT Predictions 2016 report.

Deloitte Global predicts about 100 carriers worldwide will be offering at least one packet-based voice service at the end of 2016, double the amount year-on-year, and six times higher than at the beginning of 2015. We estimate that approximately 300 million customers will be using Voice over WiFi (VoWiFi) and / or Voice over LTE (VoLTE), double the number at the start of the year and five times higher than at the beginning of 2015.

Source: Deloitte Global, 2015

For most carriers launching VoLTE or VoWiFi in 2016, the primary motivation is likely to be to increase network capacity and extend the reach of their voice services. While VoLTE or VoWiFi technologies enable a range of value-added services, such as video calling, we expect the majority of carriers to exploit this additional functionality in later years, with the initial focus being on coverage and capacity.

VoLTE increases capacity as it allows operators to move voice calls off 2G and 3G networks and onto the LTE (4G) network. The often lower frequency spectrum that is freed up can be reused for data services. Additionally the LTE interface is more efficient at carrying calls relative to traditional calls: it can support up to twice as many voice users in a given bandwidth (per megahertz). Additional cost savings can be obtained from retiring legacy infrastructure, and not having to run two infrastructures in parallel, one for data and one for voice.

VoLTE also offers a range of enhancements over standard voice. For example it offers the ability to use a data connection while being on a call, superior voice call quality, faster call connection, fewer dropped calls and the ability to switch from a voice call to a video call. However while early adopters in 2016 are likely to be most fervent users of this additional functionality, many users may not notice the variation in voice quality.

Carriers are likely to use VoWiFi to extend coverage, particularly indoors, and as a result help improve customer satisfaction with the operator and lessen the likelihood of churn. The majority of mobile calls are made indoors (at least twice as many smartphone users make voice calls indoors than outdoors), but providing good internal coverage can be technically complex and expensive, particularly for lower floors and internal rooms. One study found that about 40 percent of UK consumers have a mobile blackspot at home and almost a third reported regular issues making or receiving mobile calls from home.

One response to blackspots is to deploy additional cellular towers or small cells to increase network reach, but this is complex technically, time-consuming (due for example to required planning consents) and costly. Another approach would be to place femtocells (tiny base stations) in consumers’ homes: each of these would cost tens of dollars.

VoWiFi may at first glance appear little different from VoIP, but there are two critical differences. Firstly it is a network operator managed and controlled service, which, for users, should mean that the call is less likely to be dropped. So other activity on the same network is less likely to disrupt a voice call than would be the case on a VoIP call, which is carried on a best efforts basis. For carriers, being in charge of the service also means that they have more control over the revenue stream. Secondly, VoWiFi offers native calling: there is no need to open an app to make or receive calls. A VoIP call can only be received when that specific app is open.

VoWiFi extends reach at a relatively low marginal cost. Operators need to deploy an IP multimedia subsystem (IMS). If they already have VoLTE, this will already have been paid for. In some regards VoWiFi may even reduce operator costs, as calls placed on a smartphone would be carried over the consumer’s broadband network, freeing up some cellular capacity.

Further, VoWiFi can reduce cost for an operator as it enables traffic to be off-loaded to another network. The cost savings could be significant: a US carrier with 15 percent VoWiFi penetration and a national footprint could enjoy spectrum and capacity savings per year of approaching half a billion dollars.

Long term, most operators will likely launch both services as a natural evolution towards IP-based-only communication. However, short term some carriers may decide to launch one of the two services first. The decision will likely be influenced by three main factors: the potential cost savings, the need to improve the indoor coverage, and the customers’ interest in enhanced communication services.

Bottom line

Operators need to weigh up benefits against the cost of deploying an IMS. One analyst firm has calculated that the cost of deploying and operating an IMS solution could be up to $10 million with a VoLTE subscriber base of around 2.5 million. If the base rose to 75 million, there would be significant economies of scale, with the the annual operating cost estimated at about $45 million.

In the short term, device and network interoperability may be a barrier for uptake. VoWiFi and VoLTE support varies by handset, and each carrier has enabled a different set of these devices. In some cases, VoWiFi may be supported on a consumer all-you-can-eat tariff, but not on the enterprise tariff. Furthermore, packet-based calls may require calling and called devices to have the same software version enabled. For VoLTE, both parties need to have compatible handsets, be in 4G range, be subscribed to 4G (rather than just having 4G capability), and, for a period of time, be on the same network.

Carriers should also bear in mind the potential cost implications for incorporating emergency service support (providing a user’s location) into VoLTE and VoWiFi. The IMS signaling system needs to support the Emergency IMS subsystem to ensure that the call goes through.

Consumers have high expectations for voice quality: operators should only launch VoLTE and VoWiFi services when the service is stable. The network should be configured so as to prioritize voice packets. Real-time monitoring and auctioning of network performance KPIs such as bit-rate, latency, jitter and packet loss are also recommended. Operators should include a fallback for non-native VoLTE calls, or calls in areas where 4G coverage is lacking or limited.

Operators should also advise on some of the quirks of the service at this stage: for example a VoWiFi call cannot roam onto a circuit-based 2G or 3G call when out of WiFi range: it can only move onto a VoLTE network.

Carriers should determine how best to advertise the two services so that consumers value the quality of voice call and perceive the enhancements provided as value added services. This could counteract the declining trend of smartphone users not making phone calls and moving to OTT alternatives.

TMT Predictions 2016 Authors

@DeloitteTMT