Article

New Regulations for Sustainability-related Fund Names

BaFin Publishes Supervisory Notice regarding the ESMA Guidelines

Explore Content

- 80 % Threshold

- Minimum exclusions

- Climate Transition Benchmark (CTB)

- Paris-Aligned Benchmark (PAB)

- Transition Plan

At a glance:

- EU standardized requirements of the ESMA Guidelines on using sustainability-related terms in fund names are applied directly by BaFin.

- A distinction is made according to the following name components:

- Transition, social or governance-related terms

- Environmental or impact-related terms

- Sustainability-related words

- Depending on the fund's name, different requirements must be met:

- 80 % threshold for proportion of investments in accordance with the binding sustainable elements of the investment strategy

- Minimum exclusions under Climate Transition Benchmark (CTB) and Paris Aligned Benchmark (PAB)

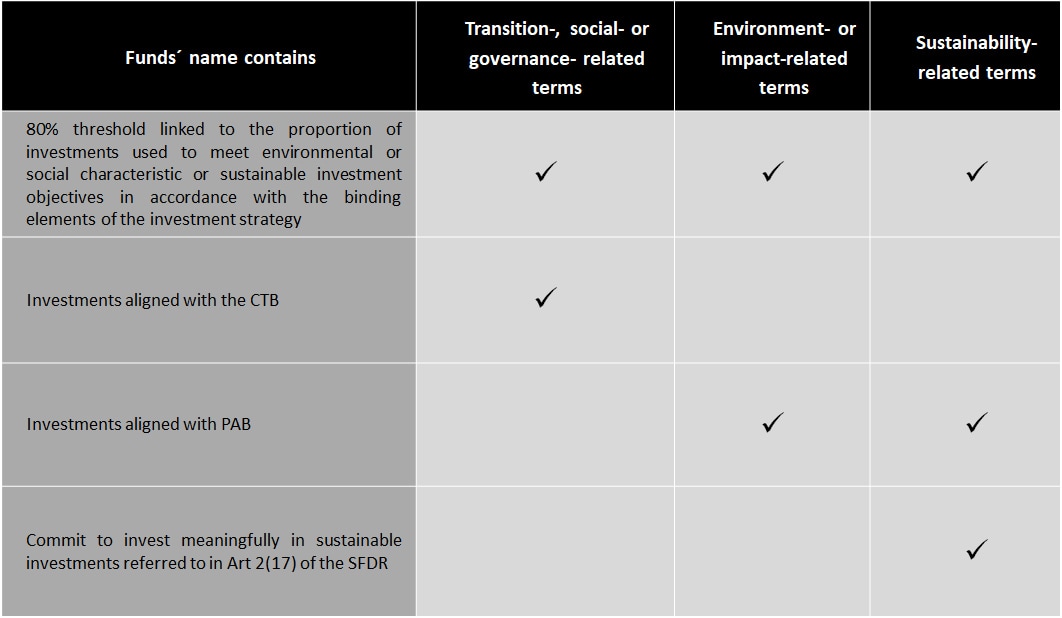

- The obligation under Art. 2 (17) SFDR to invest "meaningfully"

In July, BaFin issued a comprehensive statement on the implementation and application of the ESMA Guidelines for fund names in a supervisory notice1. BaFin explained how it is adopting the guidelines published by the European Securities and Markets Authority (ESMA) on 14 May 2024 on the use of sustainability-related terms in fund names (Final Report - Guidelines on funds' names using ESG or sustainability-related terms - the ESMA Guidelines)2 for German asset management companies (Kapitalverwaltungsgesellschaften - KVGs) and German investment funds in its administrative prac-tice. Guidelines of the European Supervisory Authorities (ESAs) are convergence tools intended to harmonize supervision within the EU. As soon as BaFin adopts the ESA measures in its administrative practice, do the guidelines have an effect on the application of supervisory law in BaFin's supervisory area.

For the first time, the ESMA Guidelines establish Europe-wide requirements regarding the conditions for the use of ESG- and sustainability-related terminology in funds´ names. These requirements apply to all EU-regulated funds, including special funds (alternative investment funds - AIFs). The aim pur-sued is to ensure increased clarity and transparency for investors. As the fund name may give inves-tors a first impression of the investment strategy and objectives which can therefore influence in-vestment decisions, it is crucial that investors are not being misled by the product name.

BaFin will take the ESMA Guidelines directly into account in its administrative practice. In practice, this is achieved by the fact that certain requirements must be met for the processing of all new appli-cations received by BaFin, depending on the name components used. This means that the mere pres-ence of sustainability terms in the name of the investment fund triggers a corresponding review of the investment conditions. This will replace BaFin's previous administrative practice for sustainable mutual funds.

A distinction is made between the following name components:

- Transition-, social- or governance-related terms;

- Environment or impact-related terms; and

- Sustainability-related terms.

80 % Threshold

With immediate effect, BaFin's administrative practice will apply the minimum threshold of 80% pro-vided for in the ESMA Guideline. The minimum threshold states that 80 % of the fund assets must be invested in such a way that they comply with the mandatory sustainable elements of the investment strategy. The 80 % threshold is the fundamental requirement for the use of sustainability-related terms in the fund name. It generally applies to KVGs that manage investment funds with transition, social, governance, environmental, impact or sustainability-related words in their name.

Minimum Exclusions

An additional requirement is to apply the so-called minimum exclusions provided for by the ESMA Guidelines. These are based on the Benchmark Regulation (EU) 2016/10013 . The Benchmark Regula-tion defines the Climate Transition Benchmark (CTB) and the Paris-Aligned Benchmark (PAB)4 as benchmarks. Whether the reference values of the CTB or the stricter reference values of the PAB ap-ply to the fund depends on the terminology used in its name.5

Climate Transition Benchmark (CTB)

Investment funds that use the terms "transition" or "transformation" - so-called transition funds - are subject to the less stringent standards of the CTB. Transition funds are funds that invest in companies, industries, etc. in order to achieve change, for example a faster phase-out of coal and lignite mining. For these funds, investments are possible in (to a limited extent), for example, companies with links to controversial weapons or those that generate 10 % or more of their revenue from the exploration, ex-traction or refining of crude oil. This is due to the core objective of these funds, which is to use the capital invested to accelerate sustainable change in companies.

Paris-Aligned Benchmark (PAB)

Investment funds including terms such as "environment" or "sustainability" in their name, are subject to the comparatively stricter requirements of the PAB. For funds measured against the PAB, for exam-ple, investments in undertakings with links to controversial weapons or those deriving significant rev-enues from fossil fuels (more than 10 %) are prohibited.

Transition Plan

In addition to complying with the minimum exclusions under the CTB, KVGs must set out a clear and measurable "transition plan" for the transition funds. The (interim) objectives of this transition plan can be defined by the companies themselves. They should be based on information that is compre-hensible and verifiable.6 As such, they can also serve as information material in fund sales prospectuses. ESMA has not yet provided more detailed guidelines on this.

Remaining Questions

Despite the publication of the ESMA Guidelines, some important questions remain unanswered, par-ticularly on terms open to interpretation. BaFin also comments on this in its supervisory notice and suggests that the undefined legal terms such as "meaningfully" in relation to investments in sustaina-ble investments within the meaning of Art. 2(17) SFDR must be discussed further in future work streams of ESMA, as this is the only way to achieve an EU-wide consensus.

The eligibility of "green bonds" 7 for funds that must comply with the ESMA Guidelines and thus the minimum exclusions has also not yet been conclusively clarified for all market participants. "Green bonds" are bonds that invest in companies or projects which contribute to environmental, nature or climate protection. When assessing green bonds, the mandated KVG must evaluate the entire issuing company, instead of just the specific project to be financed.

The Main Contents of the ESMA Guidelines at a Glance

Simplified presentation of the ESMA Guidelines.

To enlarge view, please click here.

To enlarge view, please click here.

Our team at Deloitte Legal has extensive experience in the implementation of amendment projects for fund documentation, including the amendment of securities prospectuses and investment condi-tions as well as support with BaFin approval procedures. We are happy to support and advise you on current challenges.

______________________________________

1 BaFin supervisory notice dated 25 July 2024, topic securities, ESMA Guidelines on fund names

2 ESMA, Final Report - Guidelines on funds' names using ESG or sustainability-related terms

3 Regulation (EU) 2016/1011, Benchmark Regulation

4 Article 12 (1) Delegated Regulation 2020/1818

5 The table below is an example.

6 Verifiability, e.g. through science-based targets (SBT).

Published: August 2024