The authors would like to thank Dan Hamling, Negina Rood, Gautham Dutt, and Mark LaViolette for their contributions to this chapter.

Cover image by: Jaime Austin and Sofia Sergi

Canada

India

United States

United States

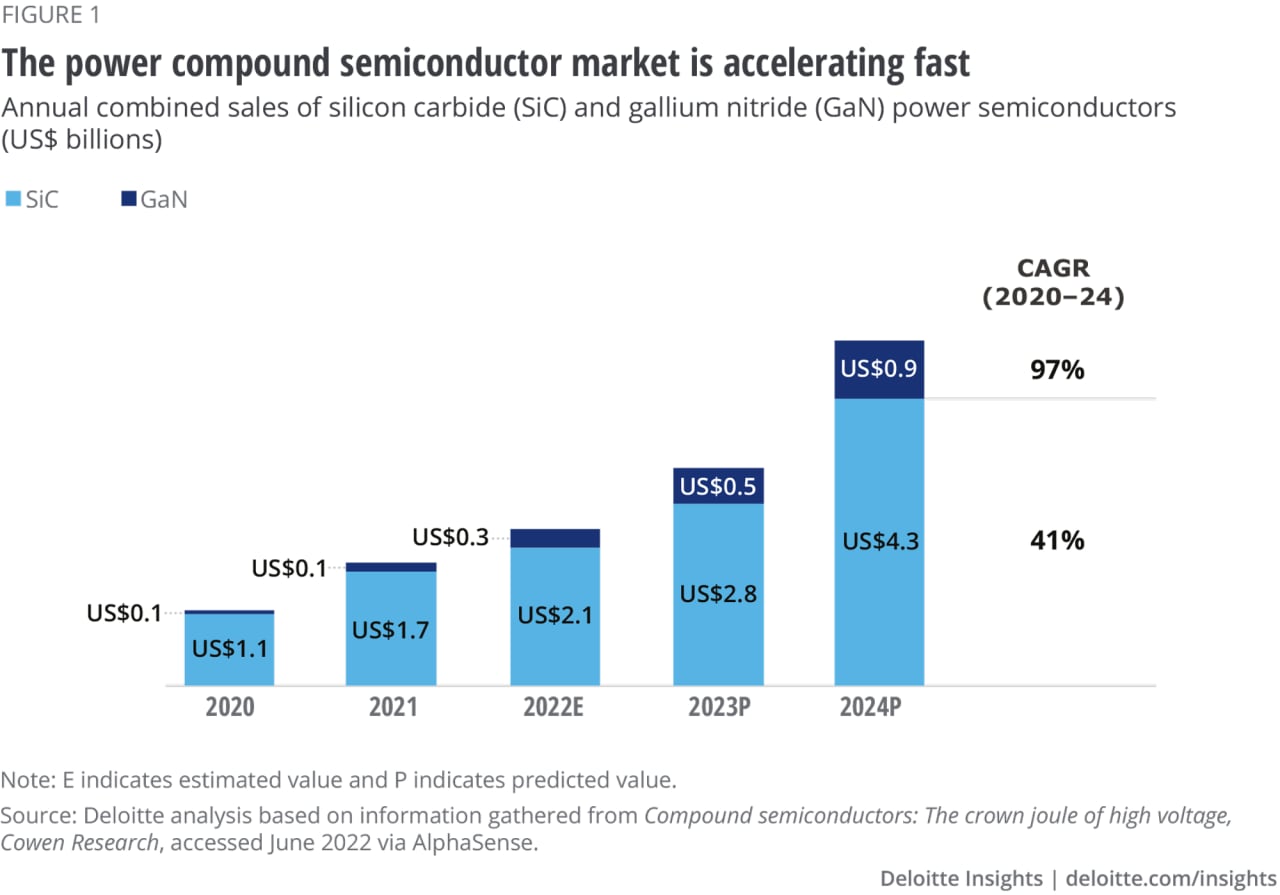

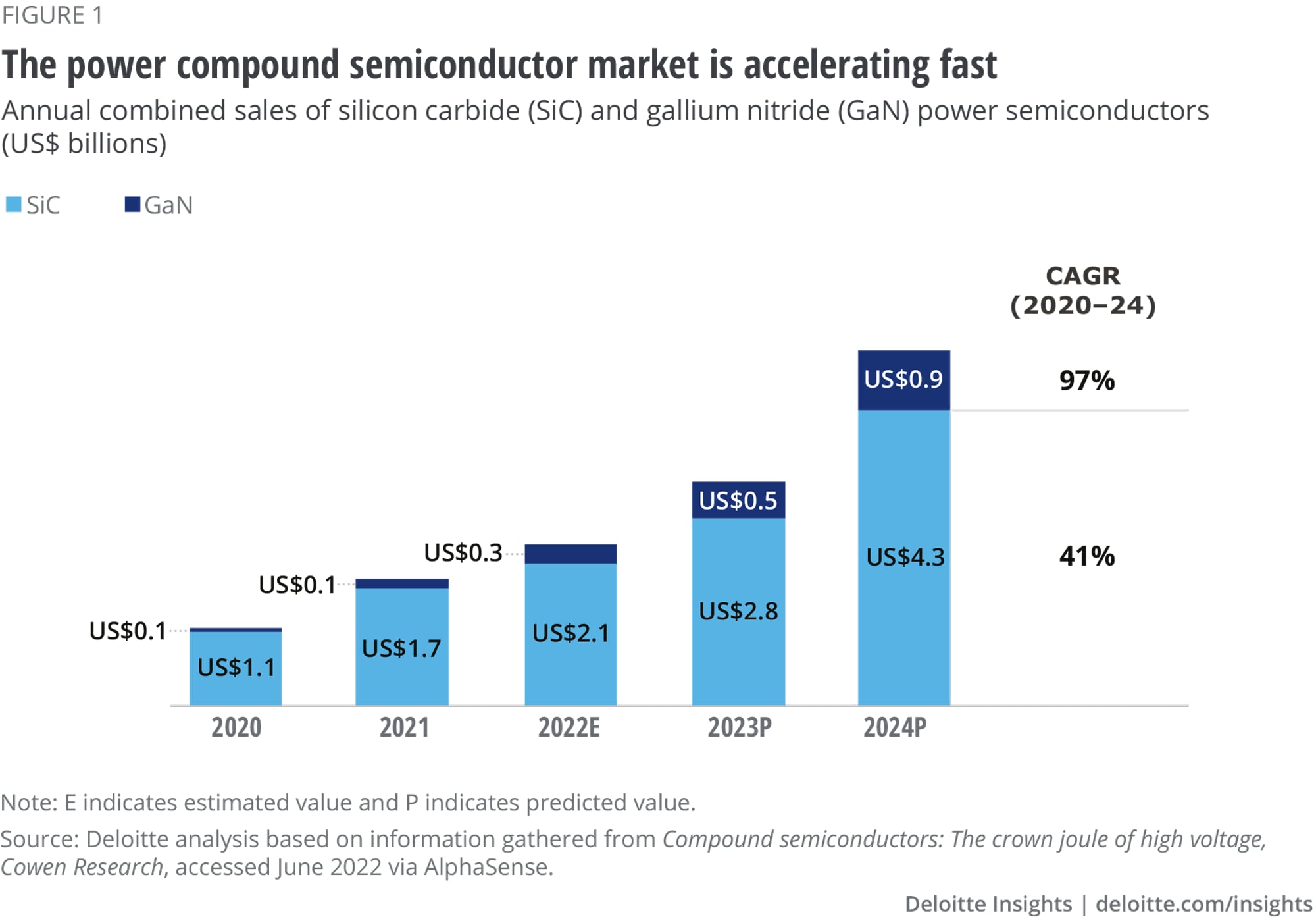

Though silicon has long been the standard for making the chips in our phones, computers, and data centers, it has one troublesome weakness: It’s not well suited for the higher voltages and power levels needed for increasingly common applications such as battery electric vehicles (BEVs), super-efficient consumer electronics chargers, powerful solar panels, and advanced military applications. That’s why Deloitte Global predicts that chips made of high-power semiconducting materials, primarily gallium nitride (GaN) and silicon carbide (SiC), will sell a combined US$3.3 billion in 2023, up almost 40% from 2022. Though that’s only a fraction of 2023’s anticipated US$660 billion global semiconductor market,1 the expansion of this fraction could go into turbo mode. Growth in these types of chips, collectively known as power compound semiconductors, is expected to accelerate to close to 60% in 2024, recording revenues of more than US$5 billion. And given their importance in fast-growing industries and national security, countries, and regions are working hard to ensure they have adequate local manufacturing capacity.

First, a caveat: Power compound semiconductors are not expected to make silicon chips obsolete. Silicon is and will likely continue to be a semiconducting wonder material. A silicon chip the size of a thumbnail can contain billions of transistors that run on scant milliwatts of power at a volt or two. That means that consumer battery-powered devices last for many hours and data centers don’t get too hot.

But the silicon processors in PCs, smartphones, and data centers are low-voltage devices, working at around 1–1.5 volts. That’s nowhere near the 120 or 240 volts that even an ordinary household power outlet delivers. If a smartphone chip were connected directly into those sockets, it would literally fry.

A host of rapidly growing applications need higher voltages still, and that means chips that can handle tens, hundreds, or even thousands of volts. For example, fast direct-current chargers for BEVs run at 480 volts,2 and while BEVs’ internal battery and motor systems typically run at 400 volts today, most BEVs are expected to operate at 800 volts by 2025.3 Other uses for power compound semiconductors include wind turbines, solar farms, power supplies of all kinds, electric trains, aerospace and defense systems … and the list goes on.4 Although special silicon-based power semiconductors called power MOSFETs have been used in such equipment for years, chips based on GaN and SiC allow these systems to be smaller, cheaper, more efficient, and denser, as well as enabling them to operate at higher frequencies and temperatures.

By 2026, consumer electronics chargers are expected to compose 66% of the GaN chip market, while automotive applications, mainly BEVs, could account for as much as 60% of the SiC chip market.

Interestingly, GaN and SiC chips don’t really compete directly with each other: They each have a market they dominate. By 2026, consumer electronics chargers are expected to compose 66% of the GaN chip market,5 while automotive applications, mainly BEVs, could account for as much as 60% of the SiC chip market.6 Both uses have sustainability benefits as well as pragmatic ones.

GaN chips are well suited for use in chargers for consumer electronic devices, of which there are more than 10 billion worldwide.7 That’s actually a more complex process than one might think. Specialized chips sit between the 120 or 240 volts that come out of the wall plug and the batteries on a smartphone, which charge at 5 volts. These chips, in conjunction with the power management ICs (PMICs) typically in the smartphone, make sure the battery charges smoothly and safely as it gets closer to full charge, without overheating. For this use, silicon power MOSFETs are increasingly giving way to GaN chips, which are smaller than equivalent silicon chips and therefore can be squeezed into smaller chargers. The biggest gain, though, is for the planet: GaN chip chargers operate at 98% efficiency, compared with 90% efficiency for silicon chip chargers.8 Eight percentage points might not seem like much, but across 10 billion devices, they add up to gigawatts of energy saved each year.

SiC chips are expected to garner an estimated US$2.8 billion in revenue in 2023, and this figure will likely continue to expand on the back of BEV industry growth. The number of BEVs sold worldwide doubled to 6.6 million in 2021 from 2020, and sales in Q1 2022 were three-quarters higher than in the same period in 2021.9 Further, as of Q2 2022, BEVs represented one in ten new passenger vehicles sold in Europe10—a new high—and one analyst is forecasting that in July 2023, more than half of all new vehicles sold in the United Kingdom will be BEVs.11 In fact, especially as BEVs move from 400 to 800 volts internally, the prediction that SiC chips will record revenues of as much as US$2.8 billion in 2023 could prove conservative. One leading SiC semiconductor manufacturer reported on its Q2 2022 earnings call that SiC chip sales had doubled quarter over quarter; it also announced that it expected SiC chip sales for the full year to double to about US$1 billion, and that it had increased its three-year-forward order book of SiC chip sales to US$4 billion from the previous guidance of US$2.6 billion.12

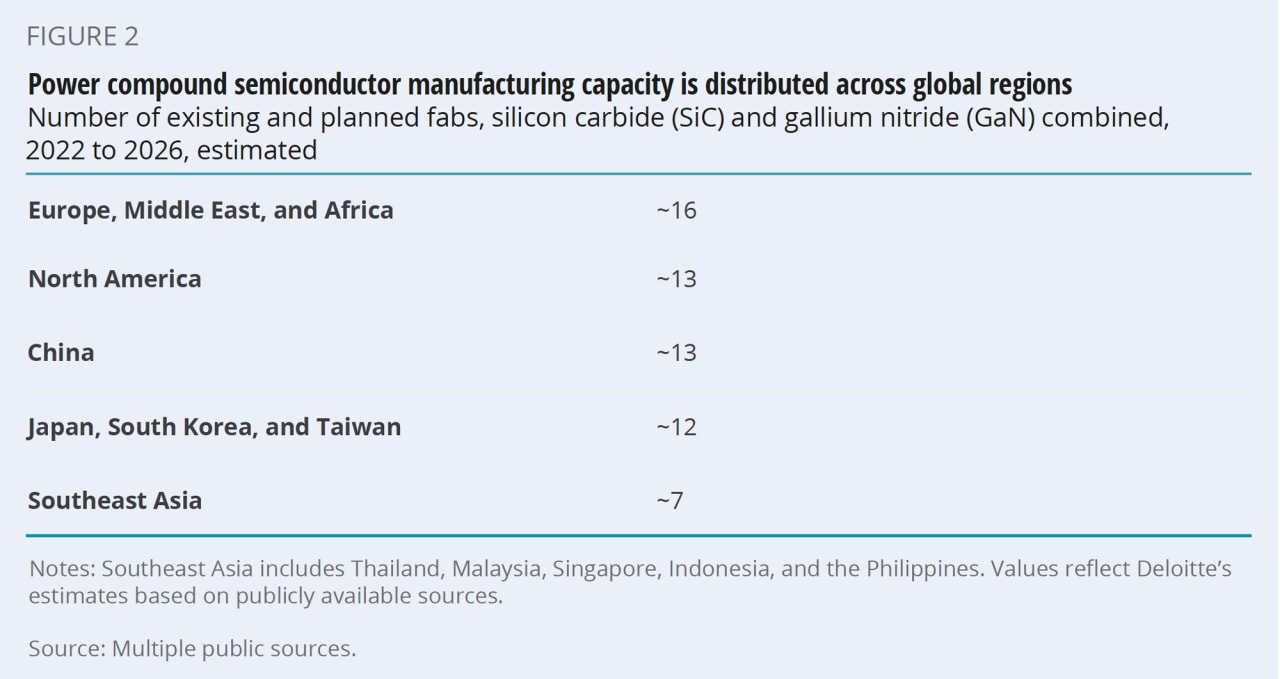

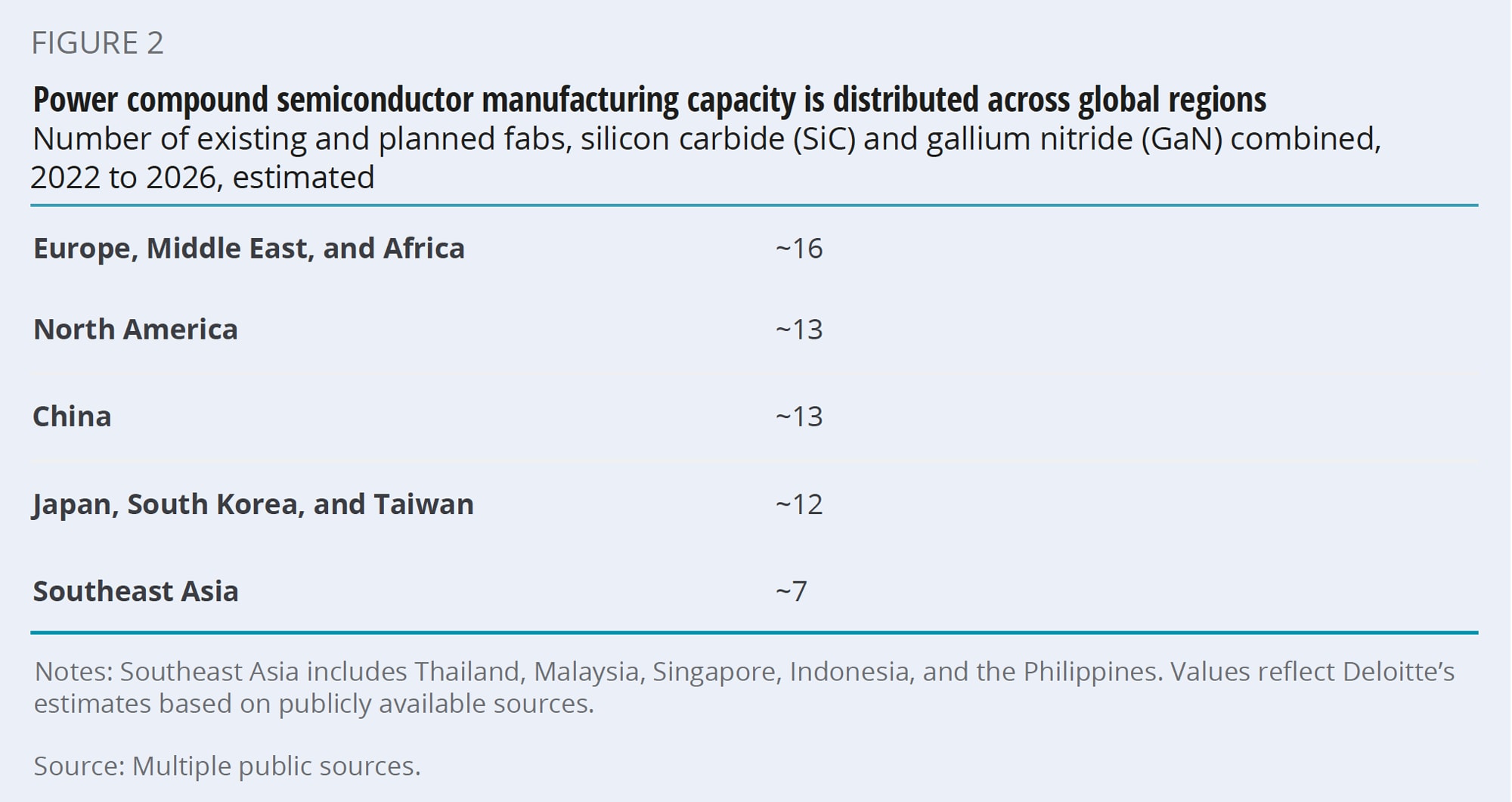

A few things need to happen before GaN, SiC, and other power semiconductors truly boom. First, new facilities (fabs) for making these chips would have to be built—and new SiC and GaN fabs are indeed moving into production around the world (figure 2). However, both the fabs and the materials needed for them raise thorny supply chain and national security issues. Silicon, carbon, and nitrogen are all abundant and available, but currently almost all gallium comes from France, Kazakhstan, and Russia.13 As with other elements and gases used in semi manufacturing with a small number of possible sources, manufacturing risk is therefore higher.

On the other hand, the geographical distribution of power semiconductor manufacturing differs significantly from traditional silicon semiconductor manufacturing, where 80% of global capacity is concentrated in East Asia—almost all of it in Taiwan, South Korea, Japan, and China.14 Although these four countries have their fair share of existing and planned power semiconductor fabs, so too do the Europe, Middle East, and Africa region; the United States; and, to a lesser extent, Southeast Asia (figure 2).15 Hence, from a supply chain perspective, the power semiconductor industry, as well as the BEV and renewable energy industries that rely on them, seems comparatively self-sufficient and resilient.

An interesting challenge for power semiconductor manufacturers is the difficulty of developing technology-specific design tools, manufacturing tools, and packaging, test, and assembly capabilities for each technology. For instance, SiC wafers need to be etched, doped, and thinned differently from silicon chips.16

With so much technology and tools to be developed, it’s not surprising that a lot of money has been pumped in to manufacture and develop these highly specialized chips. In China, three major SiC manufacturers have earmarked a total of US$4 billion in capital expenditures (capex) for this purpose during 2022 and beyond.17 Moreover, the country continues to see large rounds of PE and VC funding for SiC-based start-ups (estimated at US$1.5 billion total in June 2022 alone).18 In 2021, China even witnessed the first SiC IPO of more than US$300 million, as well as another filed by a substrate producer.19

It’s not just China, either. SiC and GaN makers in the US, Europe, Japan, and South Korea committed to making at least US$10 billion in total capex in 2022.20 A GaN company in Canada raised almost C$200 million from VCs, a US GaN company went public via SPAC for over US$1 billion, and a big French SiC company bought a smaller French SiC company late in 2021.21

Neither SiC nor GaN are expected to replace silicon in the trillions of chips for which silicon is now, and will likely always be, superior. But although they will remain niche, power semiconductors’ advantages in withstanding high voltages—and the need for more of the products they support—mean that this is one niche market that’s likely to grow significantly faster than the silicon chip mainstream.

World Semiconductor Trade Statistics (WSTS), "The World Semiconductor Trade Statistics (WSTS) has released its new semiconductor market forecast generated in August 2022," August 22, 2022.

View in ArticleBased on Deloitte’s analysis of Hui Zhang and Haiwen Liu, "Potential applications and impact of most-recent silicon carbide power electronics in wind turbine systems," Wind Energy Conversion Systems (2012), pp. 81–109; Energy Efficiency & Renewable Energy, “Silicon Carbide in solar energy,” accessed September 26, 2022; CAF Power & Automation, “Silicon carbide, moving towards a more sustainable train,” January 27, 2021; Military+Aerospace Electronics, “Silicon carbide MOSFETs for aerospace and defense power electronics applications introduced by SSDI,” January 22, 2019.

View in ArticleAmos Zeeberg, “What’s down the road for silicon?,” The New York Times, May 16, 2022.

View in ArticleThe Motley Fool, “ON Semiconductor (ON) Q2 2022 earnings call transcript,” August 1, 2022.

View in ArticleThe authors would like to thank Dan Hamling, Negina Rood, Gautham Dutt, and Mark LaViolette for their contributions to this chapter.

Cover image by: Jaime Austin and Sofia Sergi

{kind=link}

{kind=link}