India economic outlook, October 2024

India’s resilient growth is reflected in labor market improvements with a lag as evident from fiscal 2023-2024 data. Government measures and growth of emerging sectors will support job growth and consumer spending—fueling India’s journey to ‘Viksit Bharat’.

India’s economy is emerging with resilience as the dust settles after a high-stakes elections period.1 Its gross domestic product grew 6.7% year over year in the April-to-June quarter.2 While that was the slowest rate in five quarters, India remains one of the world’s fastest-growing large economies, and Deloitte’s analysis predicts continued strength in the year ahead. Growth is likely to pick up, driven by increasing consumer spending, especially in rural India, as inflation subsides, and agricultural output improves after favorable monsoon conditions.

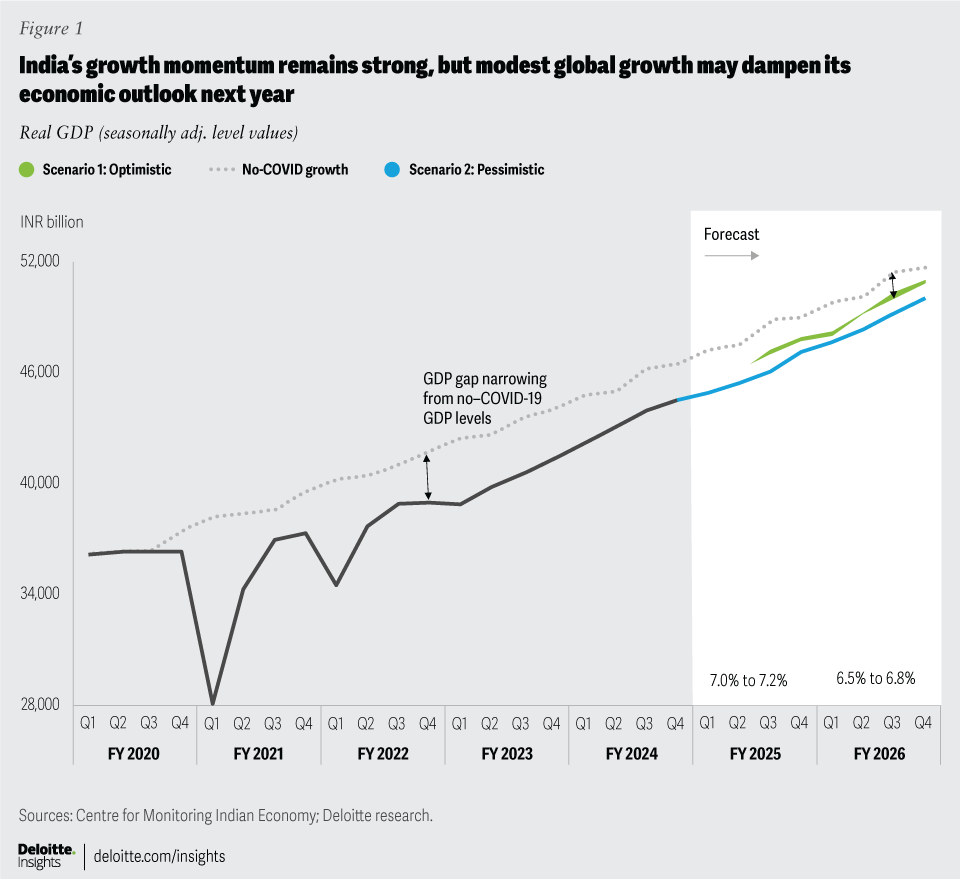

Deloitte retains its annual GDP growth projection to be between 7% and 7.2% in fiscal 2024 to 2025 and between 6.5% and 6.8% the following fiscal. A tempered global growth outlook and a delayed synchronized recovery in Western economies—compared to what was previously expected—will likely weigh on India’s exports and outlook for the next fiscal year. At the same time, India may benefit from higher capital inflows, translating into long-term investment and job opportunities as multinational companies around the world look to reduce operational costs further.

The last edition of this outlook highlighted exciting new consumption spending trends in the rural economy.3 However, sustaining this shift hinges on bolstering purchasing power and ensuring a stable income source for its people. This phenomenon motivated us to investigate if the trends in the Indian labor market could continue to boost consumer spending. Consequently, the focus in this edition is on key developments in the labor market—particularly the impact of the pandemic and its subsequent recovery—using data from Periodic Labour Force Survey (PLFS) reports published since 2017.

The latest report (2023 to 2024)4 points to some green shoots in labor market trends—with a rise in the share of salaried positions and services subsectors demanding higher qualifications, including business and professional services in the areas of technology and finance. Female participation in the labor force has also increased, particularly in rural areas. However, a heavy reliance on agricultural jobs continues, and informal employment remains prevalent.

We believe the government’s focus on boosting manufacturing and improving youth employability, coupled with India’s young and aspirational population, presents a unique opportunity for economic growth. As the country advances toward becoming a US$5 trillion economy by fiscal 2027 to 2028,5 expanding manufacturing and emerging industries and transitioning toward clean-energy alternatives are likely to create high-quality, formal, and green jobs. This will help many Indian states that are aspiring to grow rapidly, as they are already investing in these areas to tap into India’s demographic advantage. Subsequently, the improvements in the labor market will likely be reflected in future surveys.

Decoding the first quarter of fiscal 2024 to 2025

India’s GDP grew by 6.7% year over year in the first quarter of fiscal 2024 to 2025 (that is, the quarter from April to June 2024), aligning with our projected range of 6.5% to 6.7%.6 Although this marks the slowest growth in five quarters, the Indian economy showed resilience, especially during the part of the quarter coinciding with the general elections.

The two methods of estimating economic activity are decoded as follows.

The expenditure approach points to strong private consumption growth, which grew 7.4% in the first quarter from a year earlier—a seven-quarter high. With inflation easing and stronger farm outputs, consumption spending recovered, especially in rural areas. Meanwhile, gross fixed-capital formation spending grew 7.5%, a strong rate despite election uncertainties, modest corporate profits, and substantial income repatriation from foreign capital flows. Exports grew 8.7% in the same period, primarily because of strong services exports. While goods exports did well, exports in certain segments—such as gems and jewelry—contracted and the momentum of higher-value goods remained strong. Imports grew 4.1% in the quarter, down from the 8.3% growth in the prior quarter, resulting in a positive net contribution of trade to GDP.

The production approach points to stronger-than-anticipated manufacturing activities, which grew 7% year over year in the first quarter, and robust construction (10.5%), pushing India’s gross value-added growth to a 6.8% annual rate in the first quarter of fiscal 2024 to 2025, compared with the prior quarter’s 6.3%. After three consecutive quarters of poor growth, agriculture showed signs of recovery, growing at 2%: We believe this recovery will strengthen further as India receives plentiful rainfall this monsoon season.7 This bodes well for rural demand and growth in overall consumption spending during the festive season.

India’s near-term outlook

The resilient growth of 6.7% in the first quarter amid political and economic uncertainties has increased our confidence in India’s outlook this year, suggesting strong economic fundamentals driving economic activity. Five factors will drive growth in the next three quarters.

- Rural consumption spending is rebounding due to moderating inflation, specifically in food. Besides, better rainfall (over June to September, precipitation in the country as a whole was 109% of its long-period average in 2020, and it has been the third highest since 1994) and all-time high production and stock of kharif crops8 (such as rice and paddy sown during the monsoon season from June to August) point to robust agricultural output this year, thereby further pushing rural demand.9 This will likely factor into spending during festive months and beyond.

- The government’s reduced capital expenditures during the election will likely be made up for in the latter half of the year, thereby boosting the overall economy.

- Manufacturing sector capacity utilization is at an all-time high of 76.4%, which suggests that private investments in the sector will pick up. Higher capex will also crowd in investments.

- Oil prices are expected to remain modest and range-bound, which will help reduce import bills and, therefore, the current account deficit. Besides, low oil prices will also reduce the cost of imported intermediate goods and raw materials, bringing down production costs.

- Last but not least, as US elections conclude in November and the Federal Reserve looks to ease monetary policy further by the end of the year, higher liquidity, policy stability, and a modest growth outlook in the United States could incentivize global investors and multinational corporations to invest outside the United States. India will likely benefit from these trends and see higher capital inflows translate into long-term investment and job opportunities.

We expect India to grow between 7% and 7.2% in fiscal 2024 to 2025 in our baseline scenario, followed by between 6.5% and 6.8% in fiscal 2025 to 2026 (admittedly, slightly lower than previously estimated) (figure 1). India’s slightly slower growth in the subsequent year will likely be tied to broader global trends, including sluggish growth and a delayed synchronous recovery in the West, as anticipated earlier. Slowing global trade and supply chain disruptions due to intensifying geopolitical uncertainties will also affect demand for exports. Despite these challenges, we will continue to see the difference between actual GDP and no–COVID-19 levels progressively narrowing as growth picks up pace.

{kind=link}

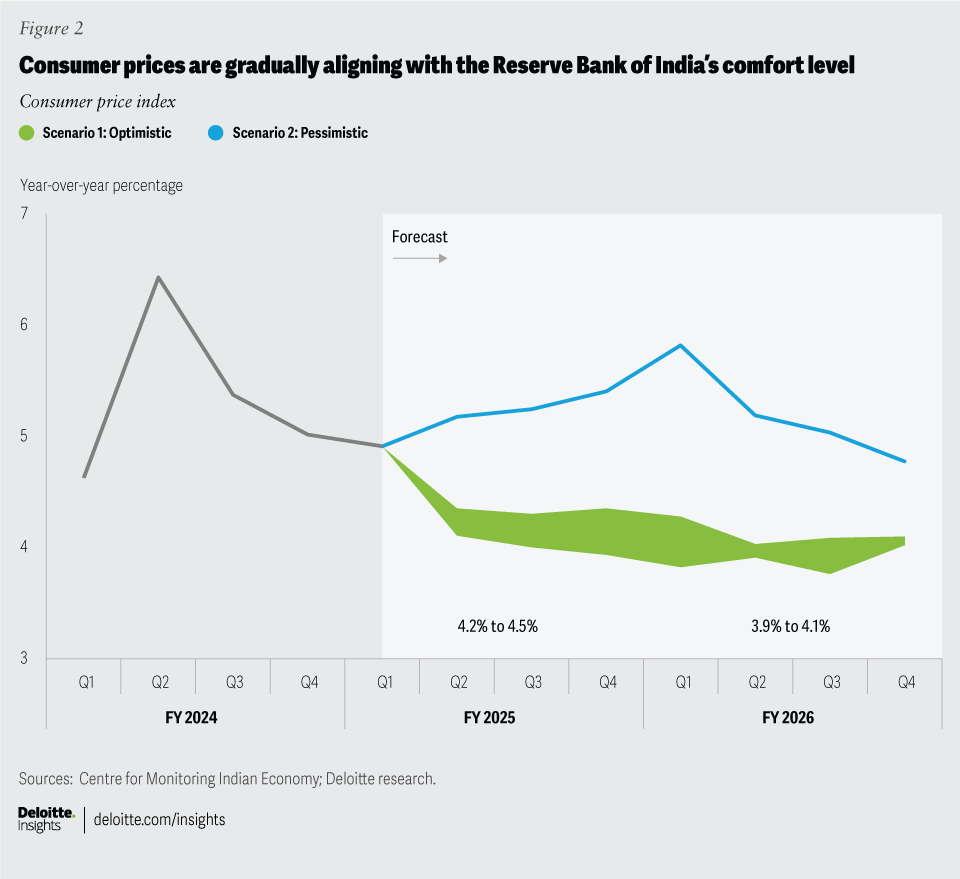

Inflation concerns are fading as expected, with better rainfall and proactive government interventions improving the food supply chain. Inflation may ease further in the latter half of the year. However, stronger growth may also pressure inflation as demand outpaces supply. We expect inflation to slowly revert to the Reserve Bank of India’s target level of 4% from early next year and remain within its comfort zone over the forecast period (figure 2).

{kind=link}

A sneak peek at India’s labor market

The last edition of this outlook examined the evolving consumption patterns of rural and urban consumers.10 While we noticed a significant shift in consumption behavior among rural consumers, sustaining that behavior remains contingent on the purchasing power of rural India, which, in turn, will depend on job creation in the economy, ensuring a steady household income.

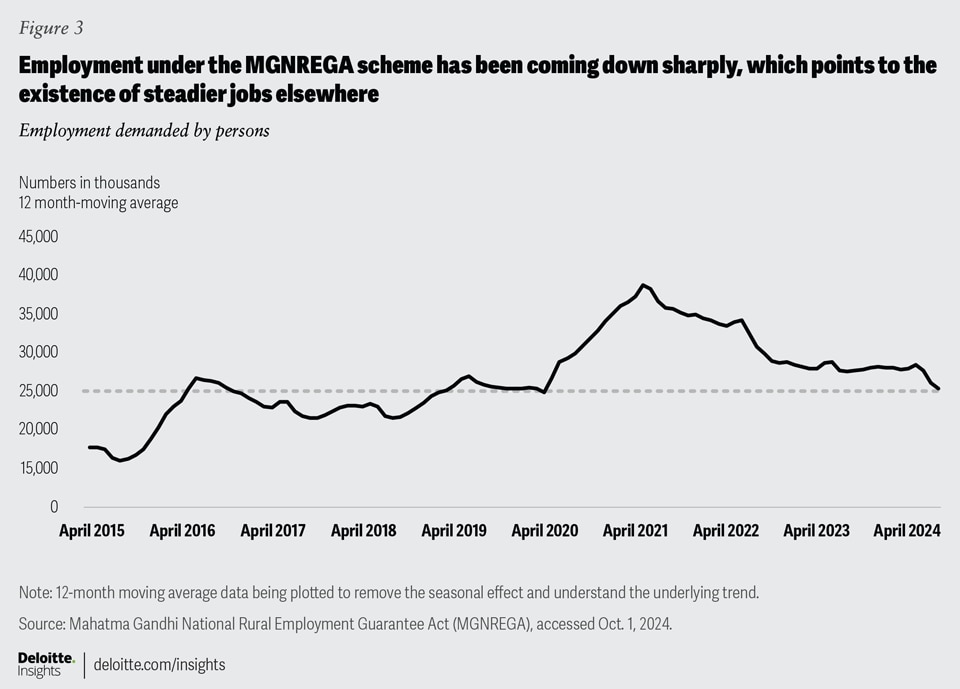

The good news is that rural demand is finally turning the corner. After remaining modest for most of the post-pandemic period, growth is visible in the rising consumption of the fast-moving consumer goods (FMCG) category (as reported by major FMCG companies in fiscal 2024 to 2025).11 The other proxy indicator for rising stable employment opportunities in the rural economy is the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA): The scheme provides temporary jobs to employ people who have limited or no alternate stable income opportunities. For the first time since the pandemic, the scheme’s 12-month moving average12 employment demanded number has fallen below pre-pandemic levels in August 2024 (figure 3).

While the rise in farm-sector employment due to above-average monsoons and increased labor demand for kharif sowing likely reduced reliance on the scheme, a steady decline probably also points to the possibility of individuals finding better-paying job opportunities elsewhere. The fall has been the sharpest since the beginning of fiscal 2024 to 2025.

{kind=link}

Emerging labor market trends

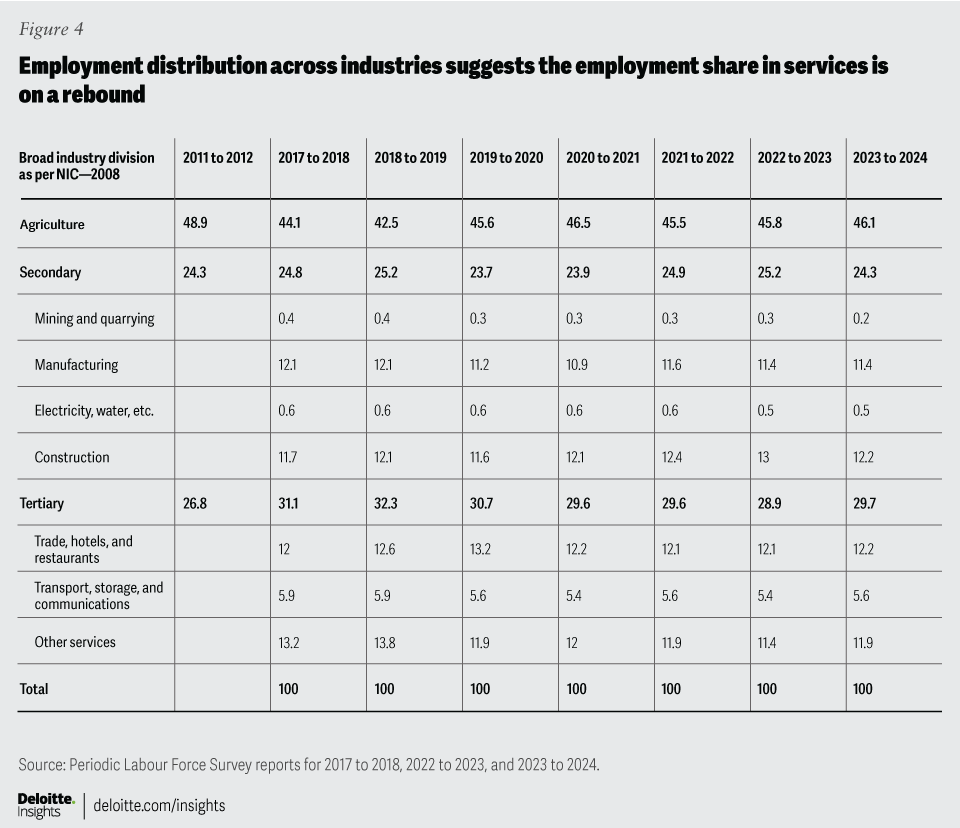

India has always relied heavily on agriculture for employment—with the largest share of Indian workers working in the sector.13 However, dependence on agriculture and related activities as a primary income source had been trending down in rural areas until the pandemic (figure 4). This trend reversed during the pandemic and later, with many migrant workers choosing to stay back and continue working in the sector even as movement restrictions were lifted, and pandemic fears subsided.

PLFS reports, including the latest one—for 2023 to 2024—highlight some interesting trends.

The green shoots: The latest report has good news about the labor market.

- The share of employment in the secondary sector rebounded postpandemic due to strong job creation in construction. Initiatives like the National Infrastructure Pipeline and increased government capex drove job creation in construction (figure 4).

- Employment shares in the manufacturing and services sectors modestly improved. While schemes such as production-linked incentives helped recover the job share in manufacturing, a strong pickup in activities in the services sector helped improve the sector’s employment share from 2023 to 2024. This is particularly interesting since the “other services” category, which consists of business and professional services, saw the biggest improvements.

- The female participation rate in the labor force for ages 15 years and above increased from 22% in 2017 to 2018 to 40.3% in 2023 to 2024. The jump is much higher in rural areas (22.8 percentage points) than in urban areas (7.8 percentage points) during this period, pointing to improved inclusivity and growing women’s empowerment in rural India.14

{kind=link}

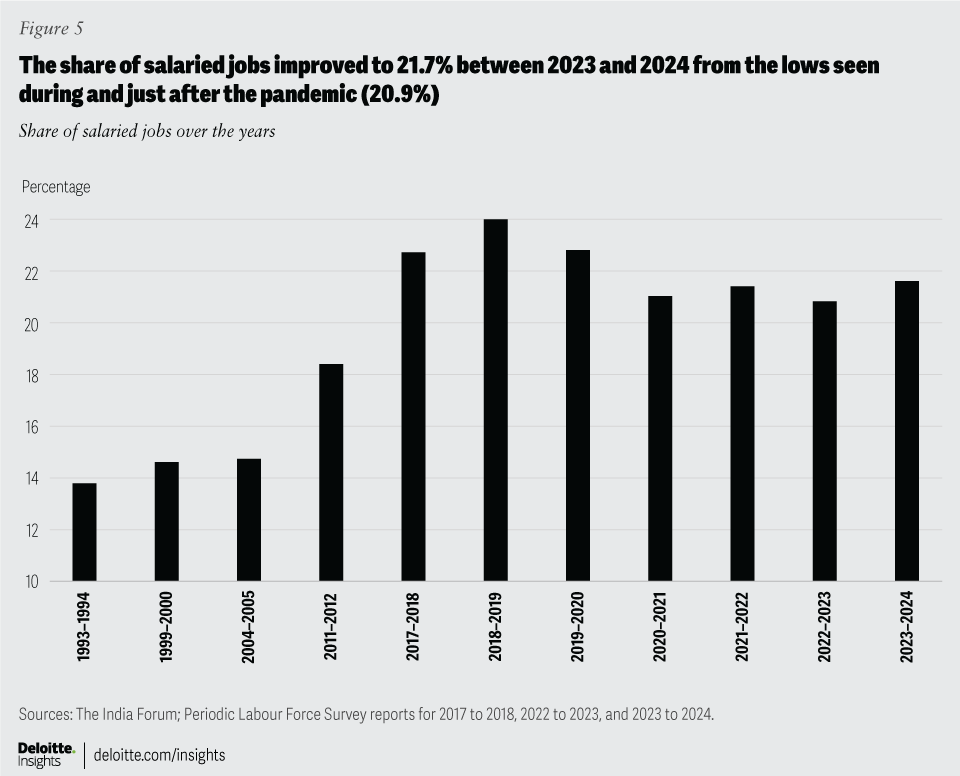

- The share of salaried workers in total employment that declined during the pandemic also pointed to a revival, according to the latest PLFS report. The share of formal jobs steadily rose until 2020 and then declined after the pandemic (figure 5).15 From 2019 to 2020, the share of salaried jobs accounted for almost 23% of total jobs, up from 18.5% between 2014 and 2015. After the pandemic, this share fell to 21%. The latest PLFS data for 2023 to 2024 points to an improvement in the share, which rebounded to 21.7%. Besides, the salaried employees’ average wage or salary earnings (in INR) also improved during fiscal 2023 to 2024 and have been several times higher than that earned by self-employed and casual workers.16 The rebound in the services sector and its employment share helped improve the share of formal jobs.

{kind=link}

The challenges: The surveys point to the accentuation of persisting challenges postpandemic.

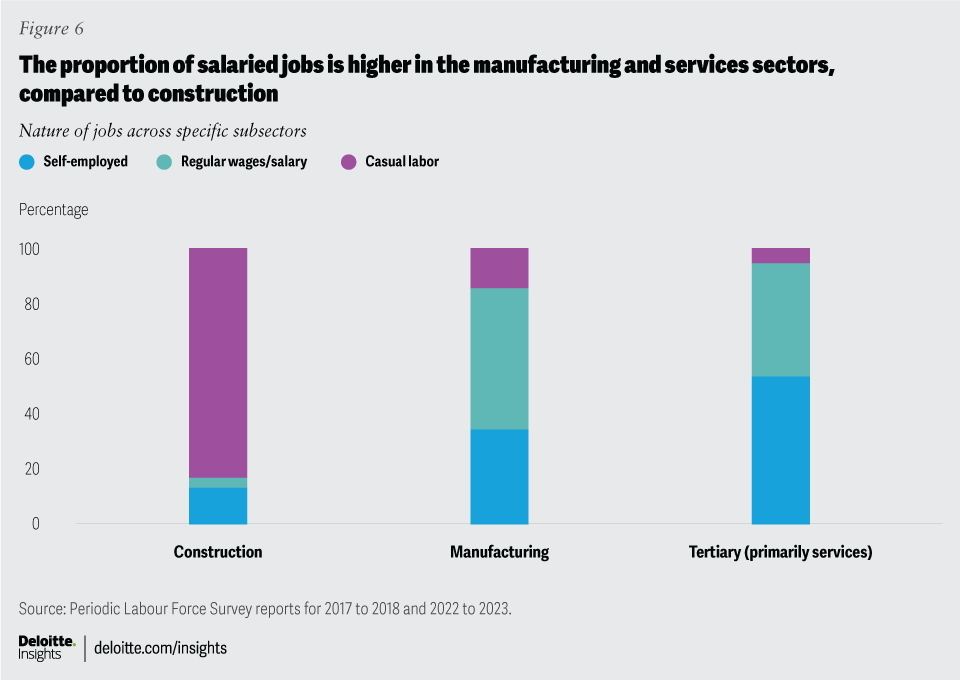

- The high share of informal jobs: The share of jobs in agriculture and construction has grown postpandemic. Incidentally, both the construction and agriculture sectors have the highest concentration of casual and self-employed workers (figure 6). Such jobs usually do not provide any social protection from the employers’ side. On the other hand, the manufacturing and services sectors create more salaried jobs, but their share in total jobs has been modestly improving.17

{kind=link}

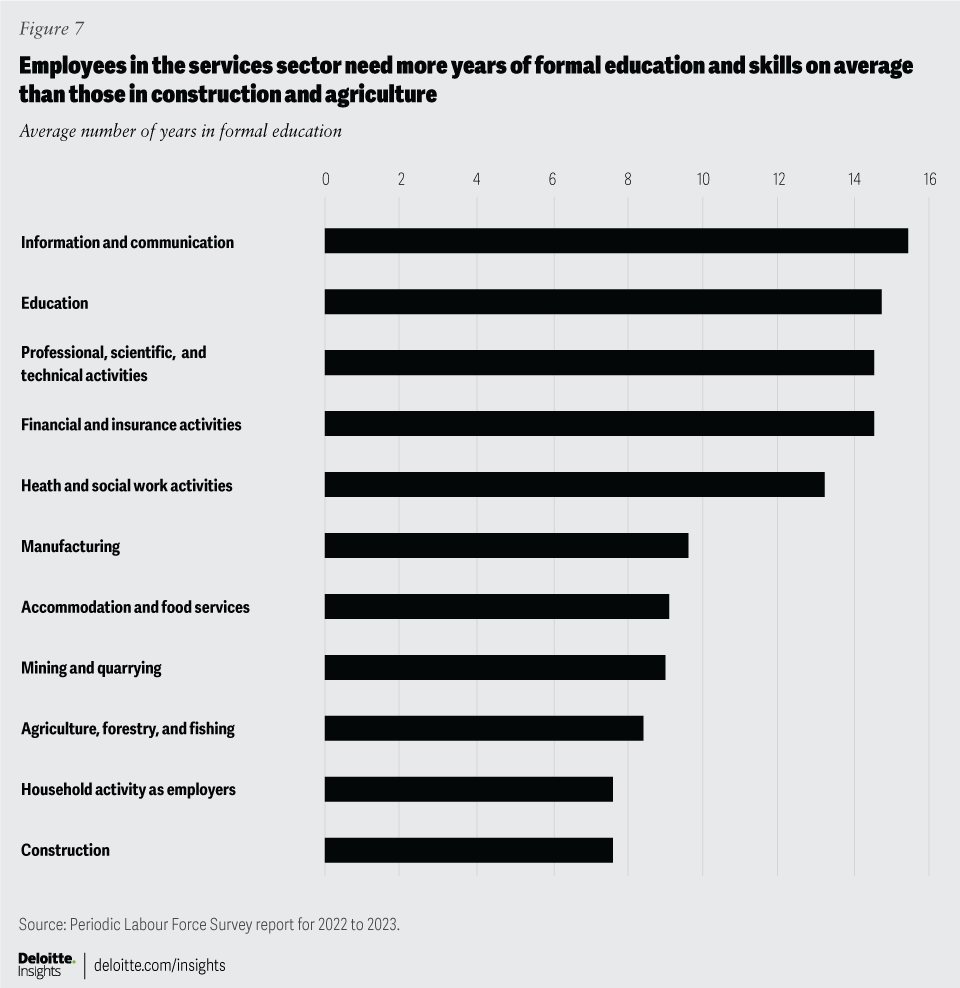

- Workers stuck in low-skill jobs: Jobs in construction and agriculture and allied services are relatively low-skill ones—this is a major concern as these two sectors are also the biggest employers in India. Figure 7 shows the least average number of years of formal education required for jobs in construction (7.6 years), agriculture (8.4 years), and self-employment in household activities (7.6 years). On the other hand, the average number of years of formal education is the highest in the services subsector.

{kind=link}

The jobs of the future

India will need more formal and quality jobs to ensure better income distribution as it becomes a US$5 trillion economy in the medium term and advances toward its long-term goal of embodying Viksit Bharat or a fully developed nation by 2047.18 In this regard, the government’s focus on expanding the manufacturing sector is critical, as transitioning workers into this sector increases the likelihood of securing formal employment, given that 51.4% of manufacturing jobs are salaried ones (figure 6). This shift will significantly enhance income stability for those currently lacking regular wages or social security, particularly in rural areas. Moreover, the growth of the services sector will aid job formalization, encouraging workers to pursue formal education and enhance their skills.

The rise in emerging industries such as semiconductors and electronics will further create opportunities that require advanced education and specialized skills, driving the creation of more high-quality jobs. Additionally, India’s push toward clean-energy alternatives is set to generate green jobs across various sectors, including energy, agriculture, tourism, and transport.

One of India’s greatest strengths is its young, aspiring population. Researchers have a consensus that the ability to learn decreases with age, suggesting that younger people are more likely to learn new skills relatively quickly.19 One study found that younger minds and brains are intrinsically more flexible and exploratory.20 This positions India to gain rapid and substantial returns from investing in skill development.

Recognizing the potential of youth, the government recently announced initiatives to drive paid internship programs and provide education loans for higher education. These will go a long way in improving the employability and skills of the Indian youth. Encouragingly, many states also strive to become significant players in the growing Indian economy, and they are actively investing in formal job creation and skill development. While there may be a lag before the labor market data fully reflects these efforts, the benefits will undoubtedly begin to surface in future surveys.

Key assumptions for Deloitte’s projections

Deloitte’s assumptions can be grouped into two buckets, namely an “optimistic” and a “pessimistic” scenario, with the former being more likely.

Optimistic scenario

The world will enjoy synchronous growth in the latter half of 2025 with minimal impact of regional wars on global supply chains and the economy. Election outcomes in the United States and the European Union will reduce uncertainties and help these economies to see strong rebounds over the next two years. Political stability, policy continuity, and strong reforms in India increase investor confidence and boost investment, leading to increased jobs and higher income.

- The US Federal Reserve cuts policy rates twice this year as inflation moderates.

- Crude oil prices remain low and range-bound owing to modest growth in China’s economy, while the pace of the global energy transition keeps oil prices from rising.

- The Reserve Bank of India maintains a tighter monetary policy to keep inflation under check, a vigil on unsecured lending, and the interest differential with the US Fed policy rate attractive for global investors.

- Government efforts toward expense consolidation continue, supported by buoyant revenues and higher dividends from public sector undertakings and the Reserve Bank of India.

- The dollar price index could swing either way depending on election outcome results and growth in the United States. This could cause the Indian rupee to marginally appreciate.

Pessimistic scenario

Regions with ongoing conflicts see prolonged uncertainties with wars in the Middle East spreading into other parts of the world. Because of political and policy changes, the United States and Europe enter a recession. China’s economy slows down, and global trade and investments fall. The crisis in the global banking system and continuous supply chain disruptions cause inflation to remain high, and the monetary policy stance in the West remains tight.