No respite in sight: US export growth faces a shaky 2016 has been saved

No respite in sight: US export growth faces a shaky 2016 Behind the Numbers, March 2016

22 March 2016

Patricia Buckley

Patricia Buckley

US export growth took a hit in 2015 and the prospects for 2016 are not looking good—so which industries are feeling the most pain?

Explore

View the Behind the Numbers collection, a monthly series from Deloitte’s economists.

With a fast-rising dollar and slowing global growth, US exporters had a difficult 2015. Since both these factors are likely to persist throughout 2016, a look at recent patterns of US export growth should shed light on industry prospects in 2016.

Factors impacting export growth

The US dollar began appreciating rapidly in mid-2014 and has since then risen by approximately 20 percent. While not yet at a historical high, this represents a significant loss of competitiveness for US exporters. Given that the United States is a rarity among nations with rising interest rates and reasonable growth prospects, we can likely expect to see further appreciation this year.

However, a high dollar is not the only headwind facing US exporters. Many US trading partners experienced relatively slower growth in 2015 and are not expecting much better in 2016, according to projections by the International Monetary Fund (IMF). As shown in table 1, goods exports1 to 15 of the United States’ top 20 export markets declined in 2015 as compared to 2014. The declines were particularly significant in exports to Canada (-$32.1 billion), Brazil (-$10.8 billion), and China (-$7.5 billion)—three countries that experienced sizable slowdowns in growth last year and that are not expected to rebound to their 2014 rates in 2016. The only sizable increase in exports was to the United Kingdom, where the value of exports grew in 2015 by $2.5 billion. However, slower growth projections for the United Kingdom in 2016 might put even this one bright spot at risk this year.

Table 1. Goods exports and GDP growth for the top 20 US export partners

| Exports | GDP | ||||||||

| 2014 | 2015 | Level change | Percent change | 2014 | 2015 | 2016 | |||

| Canada | 312.4 | 280.3 | -32.1 | -10.3% | 2.4 | 1.0 | 1.7 | ||

| Mexico | 240.2 | 236.4 | -3.9 | -1.6% | 2.1 | 2.3 | 2.8 | ||

| China | 123.7 | 116.2 | -7.5 | -6.1% | 7.3 | 6.8 | 6.3 | ||

| Japan | 66.8 | 62.5 | -4.4 | -6.5% | -0.1 | 0.6 | 1.0 | ||

| United Kingdom | 53.8 | 56.4 | 2.5 | 4.7% | 3.0 | 2.5 | 2.2 | ||

| Germany | 49.4 | 49.9 | 0.6 | 1.2% | 1.6 | 1.5 | 1.6 | ||

| South Korea | 44.5 | 43.5 | -1.0 | -2.2% | 3.3 | 2.7 | 3.2 | ||

| Netherlands | 43.1 | 40.7 | -2.4 | -5.6% | 1.0 | 1.8 | 1.9 | ||

| Hong Kong | 40.9 | 37.2 | -3.7 | -9.0% | 2.5 | 2.5 | 2.7 | ||

| Belgium | 34.8 | 34.1 | -0.7 | -2.0% | 1.1 | 1.3 | 1.5 | ||

| Brazil | 42.4 | 31.7 | -10.8 | -25.4% | 0.1 | -3.0 | -1.0 | ||

| France | 31.3 | 30.1 | -1.2 | -3.9% | 0.2 | 1.2 | 1.5 | ||

| Singapore | 30.2 | 28.7 | -1.5 | -5.0% | 2.9 | 2.2 | 2.9 | ||

| Taiwan | 26.7 | 25.9 | -0.8 | -3.0% | 3.8 | 2.2 | 2.6 | ||

| Australia | 26.6 | 25.0 | -1.6 | -6.0% | 2.7 | 2.4 | 2.9 | ||

| Switzerland | 22.1 | 23.0 | 0.9 | 4.1% | 1.9 | 1.0 | 1.3 | ||

| United Arab Emirates | 22.1 | 23.0 | 0.9 | 4.1% | 4.6 | 3.0 | 3.1 | ||

| India | 21.6 | 21.5 | -0.1 | -0.4% | 7.3 | 7.3 | 7.5 | ||

| Saudi Arabia | 18.7 | 19.7 | 1.0 | 5.3% | 3.5 | 3.4 | 2.2 | ||

| Colombia | 20.1 | 16.5 | -3.6 | -17.9% | 4.6 | 2.5 | 2.8 | ||

Source: US Census Bureau, March 2016; International Monetary Fund, October 2015.

Goods versus services

Goods exports (shown in table 1) are significantly larger than service exports, accounting for approximately 70 percent of total exports. In 2015, goods exports totaled $1.5 trillion as compared to $710 billion of service exports.2 As shown in figure 1, the downturn in exports was felt more acutely in the goods component. Although not as severe as the 18.2 percent contraction experienced in 2009 at the height of the Great Recession, the 2015 contraction in goods exports was 7.3 percent—a decline on par with the contraction seen in the 2001 recession. Exports of services also contracted in 2015—but only by a very small amount (0.1 percent).

Goods

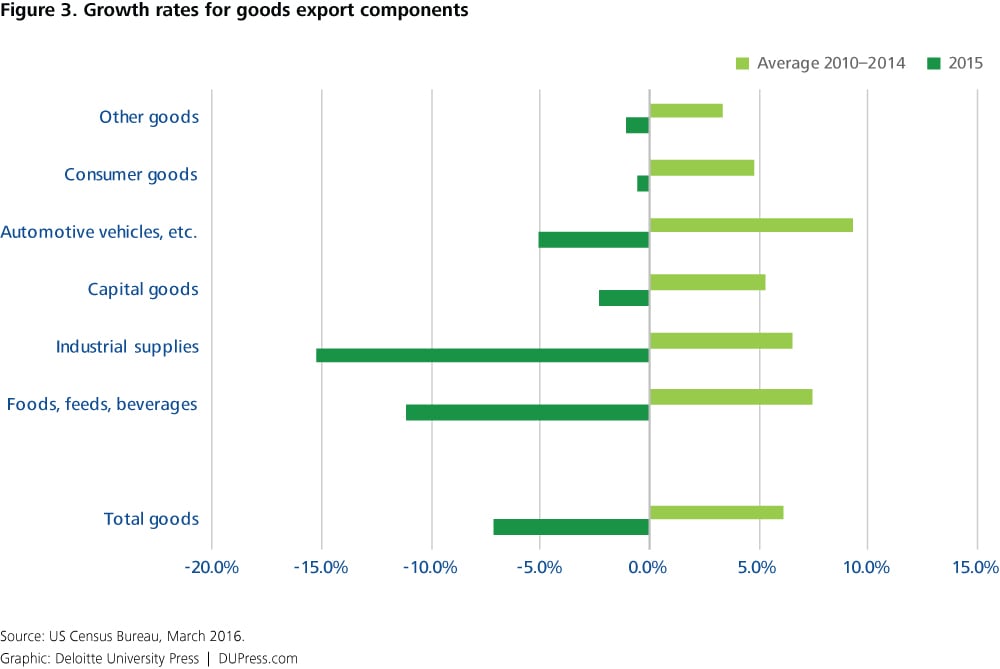

Figure 2 shows the major categories of goods exports. They are heavily weighted toward capital goods ($538.3 billion) and industrial supplies ($428.2 billion), which together account for 64 percent of the goods exports.

All categories of goods exports contracted in 2015 after averaging growth of between 3.4 percent and 9.3 percent per year between 2010 and 2014 (see figure 3). The largest declines, both in percent terms and dollar amount (not shown in the figure) were industrial supplies and materials (down 16.1 percent or $80.3 billion) and foods, feeds, and beverages (down 11.5 percent or $16.6 billion). The declines in both these categories were a function of slowing world growth driving down commodity prices; in the case of industrial supplies and materials, slowing demand was exacerbated by an oversupply of oil.

Just over a quarter of industrial supplies and materials exports consist of fuel oil, crude oil, and other petroleum products. On a nominal basis, exports of this category of industrial supplies and materials fell by $49.5 billion or 30.7 percent. However, on a real or cost-adjusted basis, exports of this petroleum group actually rose by 7.2 percent; that is, revenues declined even as export volumes rose.3 Other components of industrial supplies and materials, such as chemicals and plastics, also had their prices held down because they use petroleum as a feedstock or are energy intensive. These and other parts of industrial supplies and materials, such as cotton, copper, and lumber, were also hit particularly hard by the global slowdown as countries such as China reduced demand—commodities follow a world price benchmark. Food, feeds, and beverages suffered a similar fate as world demand for food-related commodities, such as soy beans and corn, also fell.

The other categories of goods exports did not experience the same downward pressure on prices as commodity-related exports did. As shown in figure 4, the nominal and real changes in exports of capital goods (such as civilian aircraft, industrial machinery, and medical equipment), automotive, and consumer goods were fairly similar.

Services

As shown in figure 5, the categories of service exports are wide ranging, including everything from travel—people traveling to the United States from abroad—to insurance services.

Overall, services exports grew 6.0 percent per year on average between 2010 and 2014. This growth ceased abruptly in 2015 when services exports contracted slightly by 0.1 percent. However, as shown in figure 6, the slowing world economy and rising dollar did not impact all categories equally. Exports in four of the sectors actually declined in 2015: government services, charges for the use of intellectual property (which include industrial processes; computer software, trademark, and franchise fees; and movies, books, and broadcasting), financial services (securities brokerage services, financial management, credit card services, securities lending, and electronic funds transfer), and transport (primarily sea and air transport of people and freight). Transport is the only category in services exports where the difference between nominal and real changes is substantial. Price adjusted, or the volume of transport services, rose slightly in 2015 even as the nominal value fell in the face of lower fuel costs.

Only insurance services reported stronger export growth in 2015 than it did in the prior four years.

The remaining categories had slower export growth in 2015 than during the 2009–2014 period. These include telecommunications, computer and information services, maintenance and repair, other business services and travel. Travel, the largest service export component, consists of business travel (23 percent) and personal travel (77 percent). Of the $136.9 billion that foreigners spent while visiting the United States, 2.5 percent was on travel for health reasons and 22.5 percent was for educational purposes. The remaining 75 percent was for discretionary personal travel.4 In 2014, discretionary personal travel fell for the first time since the Great Recession and, given the cost sensitivity of this component, it seems highly likely that it fell again in 2015.5 The growth of the second-largest services export category, other business services, also slowed in 2015. Just under half of the other business services are exports of professional and management consulting services, including legal, accounting, auditing, public relations, advertising, and other business consulting. This large export group also includes research and development services and technical services such as architectural and engineering, construction, industrial engineering, and mining.

Looking forward

The outsized impact of falling oil prices on the nominal value of exports of industrial supplies and materials should mitigate in 2016 because even if the price of oil remains low, it does not have much room to fall further. However, slowing global growth will limit export potential, particularly among commodities. The dollar is far more likely to rise further than it is to fall in 2016, which means that the price differential between more differentiated products will not favor the United States. One category, in particular, that will be under pressure is personal travel to the United States and this could negatively impact the leisure and hospitality industry this year.