Eurozone economic outlook, April 2024

Despite easing inflation and a strong labor market, consumers in the eurozone are still holding back on spending.

Eurozone economies have had a mixed start in 2024: The good news is that inflation has been easing faster than economists had initially expected, and labor markets are still surprisingly robust; but the bad news is that there are still no clear signs of household spending—the key driver of the 2024 outlook—starting to pick up, leaving an economic recovery somewhat postponed. Altogether, we can expect a year of moderate growth with gradually increasing economic activity.

Economic situation is fragile and divergent across sectors and countries

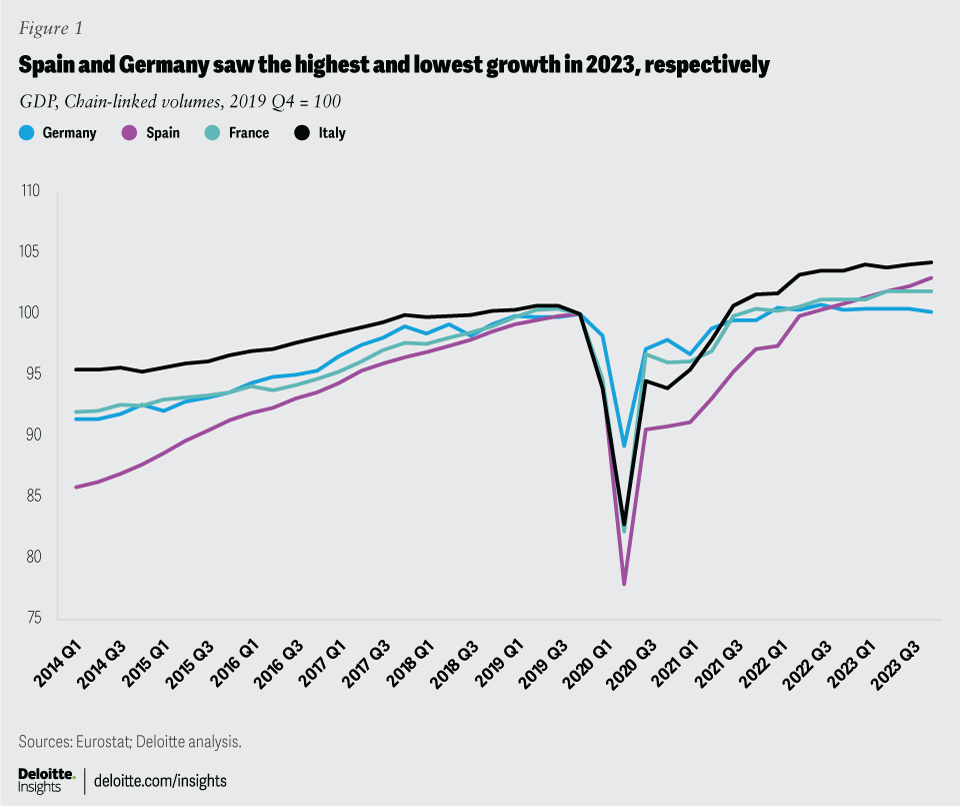

Economic growth (in terms of gross domestic product) in the eurozone slowed from a 3.4% annual pace in 2022 to 0.4% in 2023. The slowdown was more pronounced in the second half of the year, with GDP contracting slightly in the third quarter before stagnating in the fourth.

A combination of factors drove this weakness. Annual figures show that consumer expenditure expanded only slightly, as consumers were reluctant to spend more in the face of still-high inflation and increased savings due to high interest rates and economic uncertainty. Yet, the robust labor market prevented a greater slowdown.

Investment activity also lost momentum as elevated financing costs and uncertainty made many investment projects look less attractive. Furthermore, subdued foreign demand caused the eurozone’s export levels to contract; but the trade balance remained positive overall as imports contracted even more, comparatively.

Yet, these developments were not spread uniformly across sectors or across countries. Looking at the economic activity (measured by value added) by sectors, manufacturing contracted in 2023 and construction grew only slightly, marking a slowdown from prior years. Economic activity slowed in services as well, but to a lesser extent since the sector is generally less prone to increases in energy prices and financing costs, given it is less energy- and capital-intensive. In particular, information and communications, as well as sectors including entertainment, recreation, and other services, were still able to expand with healthy growth rates.

Among countries, Germany was the poorest performing of the major eurozone nations, with its GDP contracting slightly in 2023 (figure 1). (The German economy contracted by 0.3% in 2023, after growing 1.8% in 2022.) The decline of German economic activity was broad-based, but energy-intensive and energy production–related industrial sectors struggled especially. On the other hand, the Spanish economy did grow by 2.5% owing to continuing tourism growth, which profited from increasing international tourism. Between these two extremes lie the moderately growing economies of Italy and France.

{kind=link}

Inflation and private consumption will likely determine the pace of the recovery

Lately, inflation has been easing faster than expected, with the European Central Bank revising its inflation forecasts downward in early March.1 Yet, services inflation has been stagnant around 4% since November 2023,2 mainly because wage growth is still strong and softening only slowly—this plays a crucial role for services inflation as the sector is labor-intensive.

This is probably the main reason why the European Central Bank wants to see more data before discussing the date for its first rate cut, which is expected to occur in June at the earliest. The last mile of disinflation is known to be the hardest for central bankers to address: After the effects of high energy and food prices recede, it’s a matter of reducing stickier core inflation, in which wages and prices set by firms play a critical role.

However, easing inflation (and thus, higher real income) has not yet led to evidently higher willingness to make purchases among consumers: Retail sales stagnated in January3; consumer sentiment is currently moving roughly sideways4; and savings intentions remain elevated among consumers (figure 2).5 These factors point to a possible postponement of the recovery of household expenditures to later in the year. On the other hand, the recovery might be slightly stronger if part of these savings will be used later (as interest rates come down and uncertainty fades) for consumption to fulfill pent-up demand.

{kind=link}

Sentiment indicators: Sectoral differences to continue

The outlook for businesses varies across sectors. The situation in manufacturing seems to remain difficult as indicated by the HCOB Manufacturing purchasing managers’ index, which did not follow the upward trend of the previous months but plateaued in February and March still in contractionary territory.6

While index values for German manufacturing are hardly moving upward, other major eurozone economies seem to be recovering much more quickly. The industrial confidence of the European Commission stands well below its long-term average, with no clear direction. Altogether, the manufacturing sector is unlikely to deteriorate further; the pace of decline seems to be softening despite a quick rebound being more or less unlikely.

For services, the outlook looks brighter. The latest reading for services purchasing managers’ index climbed above 50 for the second month in a row, signaling more positive development in the near future. The European Commission services confidence index improved in December and January but deteriorated in February. Though these figures do not indicate a strong boom for the eurozone services sector yet, moderate growth looks realistic.

The composite index for the eurozone increased again in March, currently holding the line at 50, indicating stagnation rather than deterioration.

Outlook in numbers

We expect a consumption-driven recovery to start slowly in the second quarter of 2024 as disinflation continues, nominal wages increase, and thus real incomes continue rising. Investment activity should start to pick up later as financing conditions start to ease and economic uncertainty diminishes. Overall, economic activity should gradually increase with GDP growing by 0.6% in 2024 and 1.6% next year. We expect inflation to decrease to a 2.3% annual rate in 2024 and 1.9% in 2025.