In whose interest? Examining the impact of an interest rate hike has been saved

In whose interest? Examining the impact of an interest rate hike Issues by the Numbers, June 2016

01 July 2016

Explore the impact that rising interest rates could have on the US economy as seen through the lens of five economic sectors: the financial services industry, households, the nonfinancial corporate sector, state and local government, and the federal government.

Barring an unexpected setback to the economy, the United States has likely reached the end of the era of ultralow interest rates that began at the height of the financial crisis. Over the seven-year period from December 2008 to December 2015, as the Federal Open Market Committee (FOMC) of the Federal Reserve Board (Fed) kept the federal funds rate near zero, interest on everything from autos and mortgages to money market accounts and bonds remained at very low levels. These low interest rates, combined with challenging economic conditions and regulatory changes, shaped the debt decisions made by different sectors of the economy. (This article divides the US economy into five broad sectors: the financial sector, the household sector, the nonfinancial corporate sector, the state and local government, and the federal government.) As interest rates begin their gradual rise, the various players should rethink the math of their spending and financing decisions—and for one player in particular, the federal government, that math will require making difficult choices.

View the related infographic

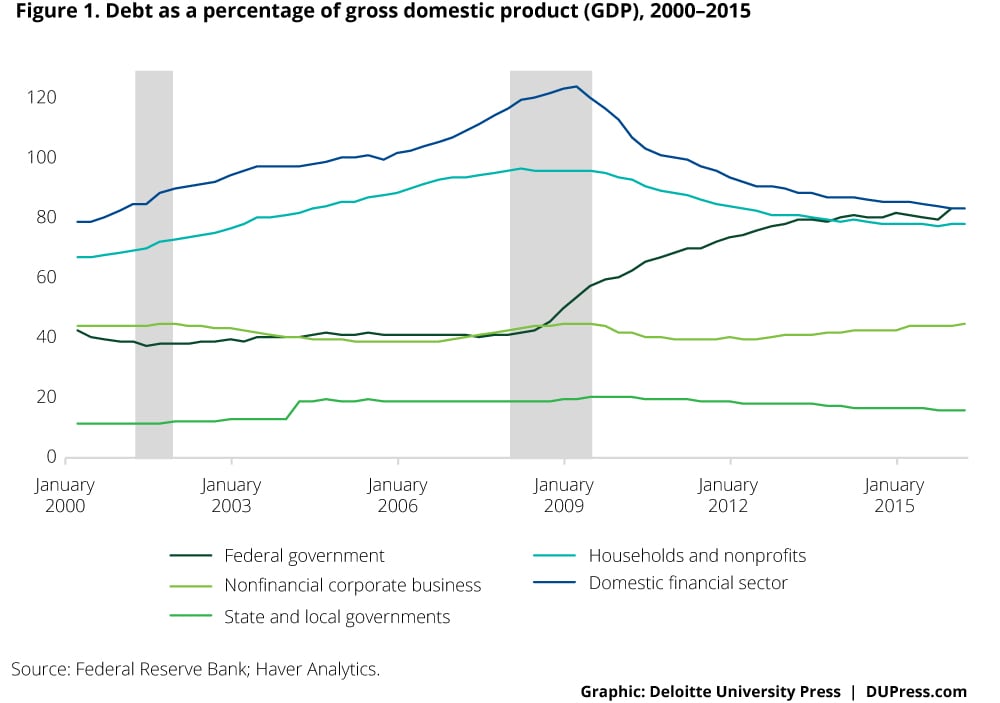

Click hereAs shown in figure 1, relative to the size of the economy, the financial sector and households have reduced their debt load since the crisis; that is, they have deleveraged. By the same measure, nonfinancial corporations and state and local government have kept their debt load fairly constant. The big outlier is the huge increase in federal government debt, which has more than doubled from the precrisis level of around 40 percent of gross domestic product (GDP). The federal government is also the sector whose future trajectory is most certain: Absent a major change in tax or entitlement spending laws, the combination of persistent annual deficits combined with rising interest rates will likely cause the federal government’s debt-to-GDP ratio to continue to rise.

The financial sector: Poised to benefit

When the 21st century began, the domestic US financial sector’s debt was not only the largest among all the five sectors; it was growing rapidly.1 During the 2008 crisis, this sector’s debt touched an all-time high of approximately 125 percent of GDP. However, the bursting of the housing bubble, losses stemming from the growing amount of bad debt, and the regulatory reforms that followed caused this sector to quickly deleverage.

Perhaps most importantly, banks tightened their loan criteria, which helped improve loan performance and asset quality.

With home values falling and bankruptcies on the rise even before the recession “officially” started in December 2007,2 the value of the assets held by various financial institutions declined. The Fed stepped in to provide credit to financially troubled institutions in exchange for bonds and securities through various asset purchase programs. Simultaneously, government-sponsored enterprises (GSEs) were placed into conservatorship, and the Treasury committed to invest in these GSEs to keep them solvent. These measures helped financial institutions reduce the share of risky assets on their balance sheets and reassure the public of the financial system’s soundness. However, they also expanded the Fed’s balance sheet and increased the Treasury’s contingent liabilities.

In the years since the crisis, depository institutions (henceforth referred to as banks)—the financial sector’s biggest segment—have been repairing their balance sheets. Perhaps most importantly, banks tightened their loan criteria, which helped improve loan performance and asset quality. The outcome is reflected in a reduction in net charge-offs and delinquencies, which are now at precrisis levels (figure 2).

Stricter banking regulations have been a major driver behind banks’ efforts to correct their balance sheets. Even as the sector’s debt condition began to improve before the end of the recession, the search was on for ways to prevent similar near-catastrophic events in the future. The Fed, together with US federal banking agencies (including the Federal Deposit Insurance Corporation [FDIC]), made significant changes to the country’s banking regulations, implementing stricter norms that required banks to increase their levels of both liquidity and capital.3 The reasoning behind these requirements is that having sufficient capital holdings should enable banks to absorb losses in a severely adverse economic environment, allowing them to continue to lend to households and businesses. At the same time, having sufficient liquid assets should help banks to meet near-term obligations, such as withdrawals by depositors, in the event of a bank run.4

US banks responded to these regulatory changes by steadily improving their capital ratios as they raised more capital and limited dividend distribution. Currently, a number of ratios measuring banks’ capital position are at an all-time high (figure 3). Similarly, banks are currently funding 75 percent of their liabilities using total deposits and are holding more liquid securities (the sum of Treasury securities, mortgage-backed securities, state and municipal securities, and equity securities) as assets (figure 4). Taken together, banks’ improved capital situation and increased liquidity have made the banking sector healthier and more resilient.

Impact of a rate hike: Players in the financial sector whose investments rely on interest income, such as insurance companies and pension funds, should see improvements in their bottom line. Most immediately, the Fed will have to pay banks higher interest rates on the excess reserves they store at the Fed, which currently total approximately $2.3 trillion.5 A rise in the net interest margin—the difference between what is paid to depositors and what is charged for various loan categories—is a likely additional benefit: Banks have been witnessing a steady decline in their net interest margins due to the recent record-low interest rates.6 Unlike some countries whose central banks have adopted a negative interest policy, US financial institutions do not, in general, charge depositors to hold their money; instead, they pay depositors some amount of positive interest, however small. Consequently, the low interest rates on loans have put pressure on revenues across the banking sector, forcing banks to depend on fee-based revenue sources and to improve operating efficiency to boost profitability. In the initial phases of policy rate hikes, banks will likely earn more interest on their assets without experiencing an equivalent increase in deposit rates, if they do not choose to raise interest rates on deposits immediately.

Households: Deleveraged, but still vulnerable

Similar to the financial sector, US households have reduced their debt considerably since the 2008 crisis—often involuntarily. The fall in total household debt since 2008 has been primarily due to a reduction in mortgage debt: Falling house prices and tightening mortgage underwriting caused mortgage charge-offs to turn negative as delinquencies and foreclosures rose, both of which contributed to the decline in mortgage debt.7 Consumer credit debt also declined immediately following the crisis; however, unlike mortgage debt, it has risen since 2012 at a robust pace (figure 5).8

While some of the reduction in household debt since 2008 was involuntary—as with deleveraging associated with bankruptcy—several factors suggest that households today are on a healthier footing than they were before the crisis:

- The savings rate remains higher than it was during the last expansion

- Growth in net household worth (the difference between household assets and liabilities) is above its 30-year trend

- House prices (in most areas) have rebounded, as have the equity markets

However, not all households have reduced their liabilities at the same pace. Data from the Survey of Consumer Finances show that lower-income households (those below the 60th percentile) have had less success in deleveraging.9 Indeed, these households have increased their leverage ratio relative to the precrisis period (figure 6). Since these lower-income households also are the ones that suffered the largest losses in net worth postcrisis, their ability to manage higher debt payments going forward may be limited (figure 7).

Impact of a rate hike: Even though many households have reduced mortgage debt, low interest rates may have created new challenges. Consumer credit debt is expanding at a pace similar to the period prior to the 2008 crisis, and the consumer debt service ratio has seen an uptick since 2013 (figure 8).

Student loans and auto loans are the biggest contributors to consumer credit debt; the share of the former has been rising sharply. Student loans now make up 38.2 percent and auto loans 29.7 percent of consumer credit debt, compared with 22.6 percent and 32 percent, respectively, prior to the recession.10 Rising new serious delinquencies in student loans indicate that many holders of these loans are already stressed (figure 9).11 Auto loan delinquencies have also grown over the past two years, although not at the dramatic pace of student loan delinquencies. Auto loans and interest on credit card balances are highly sensitive to short-term interest rates, which means that as the Fed starts raising rates, new auto loans and carried credit card balances will become more expensive. This, combined with their falling net worth and the fact that they have taken on greater debt, makes it likely that people at lower income levels will feel the pinch from higher interest rates, and the delinquency rates for all types of consumer debt could rise.

The nonfinancial corporate sector: Not immediately threatened

When measured as a percentage of GDP (as in figure 1), the nonfinancial corporate sector’s leverage position appears to have been relatively stable. However, when its debt securities are matched against its total liabilities, it is clear that, unlike the household and the financial sectors, the nonfinancial corporate sector quickly reversed its deleveraging trend and started releveraging after 2009. Many of these firms took advantage of the availability of cheap credit to issue debt securities and take on new obligations. The percentage of total liabilities represented by debt securities has increased consistently since 2007, while debt has increased by close to $4 trillion during this period (figure 10).

A look at corporate spending reveals that leverage levels have been rising without an equivalent increase in capital investment or investments in equipment and software assets, which implies that these companies have not utilized the borrowed funds to expand existing business operations or boost production, which could stimulate economic growth (figure 11). Rather, these companies have been using this new, cheaper debt to refinance older, more expensive debt and buy back equity shares.

Impact of a rate hike: As the Fed gradually tightens its policy rates, nonfinancial corporations’ interest payment obligations are likely to remain low for a few years, since the debt these companies hold tends to be of longer maturity. As of 2015, short-term debts represent only 27 percent of their total debt holdings, and because of their high levels of cash holdings, these companies have a high ratio of liquid assets to short-term liabilities (figure 12). Therefore, there appears no immediate threat to this sector due to rising policy rates.

However, even though this picture is positive overall, the nonfinancial corporate sector is currently witnessing a spike in debt defaults, particularly among the most risky bonds. According to Moody’s, the US speculative-grade default rate rose to 3.2 percent in Q1 2016 from 2.7 percent in Q4 2015, and will likely climb to a six-year high of 4.4 percent this year.12 In 2015, defaults were mostly concentrated in the oil and gas industry due to falling oil prices and weakening cash flows—9 of the 15 US nonfinancial corporate defaults were among oil and gas companies in Q4 2015.13 However, non-commodity sectors are also witnessing liquidity pressures and negative rating trends. Interest rate hikes this year by the Fed may exacerbate the default situation further, as a hike will increase borrowing costs and hurt cash flow for low-rated corporate borrowers. This, in turn, will make it difficult for these companies to resolve liquidity issues.

State and local governments: Budgetary challenges ahead?

State and local governments’ leverage rose during the recession, peaking in 2009 at 20 percent of GDP. Since then, this debt category has grown at a pace slightly slower than the economy as a whole; it currently stands at 16.5 percent of GDP (figure 13). As almost all states and local governments are required to maintain a balanced operating budget (covering current expenditures with revenues), most of the debt accumulated at the state and local level is for longer-term capital projects.14 In line with its purpose, 99 percent of the total debt outstanding is long-term debt.15 As shown in figure 13, the amount of debt outstanding has only recently been rising significantly faster than revenues. However, given the low-interest environment of this period, interest payments remained flat.

Ninety-nine percent of the total debt outstanding is long-term debt.

Impact of a rate hike: A rise in interest rates would be a particular challenge for state and local governments, since interest payments are funded out of the operating budget—the budget that must be balanced each fiscal year. However, given the long-term nature of outstanding state and local debt, it will take a prolonged period of higher interest rates to seriously impact most states’ and localities’ budgets.

The federal government: A growing deficit

Of all US industry sectors, the federal government has increased its borrowing most quickly in recent years—a trend that is projected to continue, as spending on mandatory programs and net interest is expected to rise even as revenues remain relatively flat. The Congressional Budget Office (CBO) projects that, between 2016 and 2026, revenues will remain at just over 18 percent of GDP, with their dollar value growing from $3.4 trillion to $5.0 trillion—a $1.6 trillion or 49 percent increase. During the same period, however, government spending is projected to rise from $3.9 trillion to $6.4 trillion—an increase of $2.5 billion, or 63 percent.16

As shown in figure 14, this disparity between federal revenues and spending will raise the annual deficit from this year’s 2.9 percent of GDP—just slightly higher than the long-term average of 2.8 percent—to 4.9 percent of GDP in 2026. As these deficits continue to accrue, the debt level will rise from the current 75.6 percent of GDP to 86.1 percent in 2026.

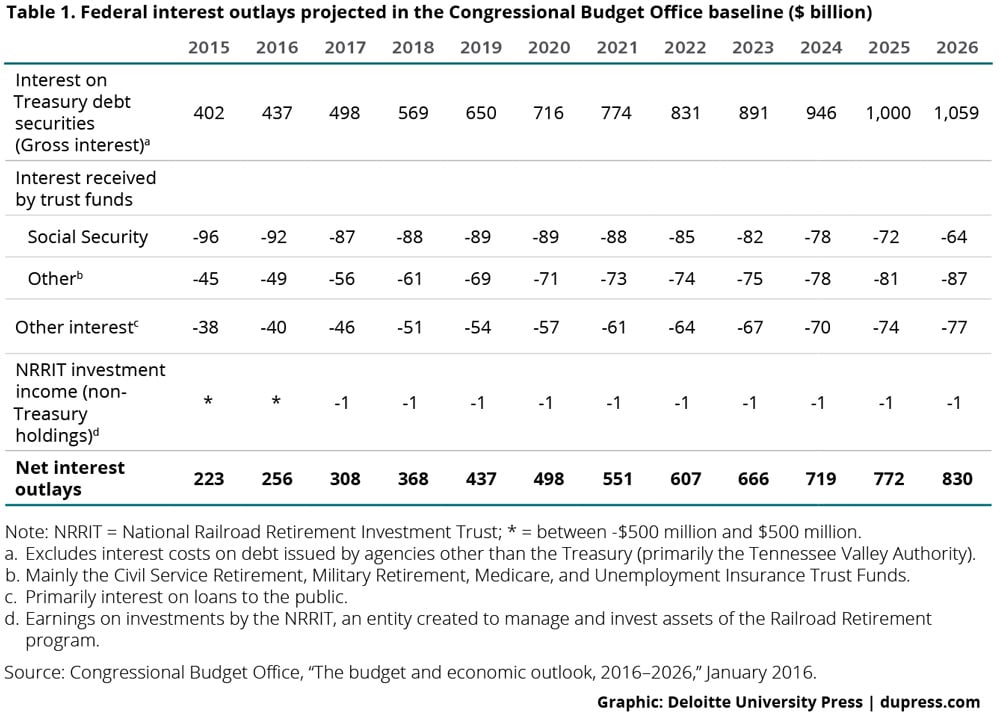

Impact of a rate hike: Figure 15 shows the components of the projected spending increase. While the rise in net interest accounts for just 23 percent of the increase, the actual dollar amount of interest paid will more than triple from $255 billion in 2016 to $830 billion in 2026. This jum results from the combination of more debt to finance and a projected r ise in interest rates. The CBO’s projections for the federal funds rate closely follows the FOMC’s most recent economic projections, which predicts that the federal funds rate will gradually rise over the next few years and reach the longer-run target of 3.5 percent in fiscal year 2020.17 As a result of the rising federal funds rate, a gradual increase in the three-month Treasury bill to 3.2 percent and a rise in the 10-year Treasury note to 4.1 percent underlie the CBO’s outlay projections. It should be noted, however, that even though these rates are much higher than any seen since the Great Recession, they are not out of line with prior experience. For example, even though net interest will rise from 1.4 percent of GDP this year to 3.0 percent in 2016, it represented 3.2 percent of GDP in 1991.

ise in interest rates. The CBO’s projections for the federal funds rate closely follows the FOMC’s most recent economic projections, which predicts that the federal funds rate will gradually rise over the next few years and reach the longer-run target of 3.5 percent in fiscal year 2020.17 As a result of the rising federal funds rate, a gradual increase in the three-month Treasury bill to 3.2 percent and a rise in the 10-year Treasury note to 4.1 percent underlie the CBO’s outlay projections. It should be noted, however, that even though these rates are much higher than any seen since the Great Recession, they are not out of line with prior experience. For example, even though net interest will rise from 1.4 percent of GDP this year to 3.0 percent in 2016, it represented 3.2 percent of GDP in 1991.

While the net interest paid by the government consists primarily of interest paid for debt financing by the US Treasury (gross interest), some categories of offsetting interest income—or, in the parlance of government budgeting, “negative outlays”—exist. Table 1 shows the breakdown of the various categories related to interest. The first row shows the combined effect of higher interest rates and greater debt to be financed; the remaining rows show the offsetting interest income. This income comes from sources such as the Treasury’s ability to earn higher returns from investing Social Security and other trust funds in higher-paying Treasuries (as required by law), and the difference between the interest rates charged for categories such as federal student loans (the largest component of “other interest”) and the Treasury rates used to finance the loans.

Will slowing the economy pay off?

Since the anticipated impact of higher interest rates is slower growth, the question becomes: Why would the Fed purposely act to slow the economy? We see at least two reasons. First, the Fed needs to raise rates so that it has room to lower them when the next recession occurs. And second, by acting early, the Fed likely hopes to choke off inflationary pressure before it starts to build. High inflation can be extremely damaging to both consumers and businesses. Fortunately, since we have not yet started to see a buildup of inflationary pressures, the Fed can afford to act slowly, with small, incremental interest rate increases. This, combined with the restructuring that most US sectors have undertaken, should ease the transition as we move to a more normal stance for monetary policy.