Gearing for change: Preparing for transformation in the automotive ecosystem has been saved

Gearing for change: Preparing for transformation in the automotive ecosystem Charting the pathways to the future of mobility

29 September 2016

Fewer cars making more trips and driving more miles—that’s one future for the extended automotive ecosystem. Shared and autonomous vehicles will likely make personal mobility more affordable and convenient, transforming the transportation landscape in cities and beyond.

Explore

Visit the Future of Mobility collection

Watch a video of Ben's journey

Listen to the podcast

Subscribe to receive updates on Future of Mobility

Explore Deloitte Review, issue 20

The last revolutionary mobility shift arrived gradually. After the motorized vehicle was introduced in the 1890s, horse-drawn carriages and automobiles rode side-by-side on city streets for three decades; in 1914, there were still more than 4,600 carriage companies operating in the United States.1

But by the start of World War II, fewer than 90 carriage companies survived, making this a cautionary tale that may resonate with automakers today—a little uncomfortably. Almost a century of incremental change later, the extended automotive industry is on the brink of a comparable transformation, away from personally owned driver-driven vehicles and toward shared autonomous mobility and it may occur at a much greater pace than the transition from horses to cars. We have seen the beginnings of this shift firsthand in the hundreds of conversations we have had with C-suite executives, academics, technologists, and governmental leaders since our initial perspective, The future of mobility, was published.2 And new evidence emerges nearly every day, as both auto industry incumbents and new entrants position themselves for the future.

Key findings

If personal mobility becomes more affordable and convenient through shared autonomous vehicles, and adoption rates are similar to the introduction of smartphones and the emergence of the commercial Internet, it will have profound implications for the mobility ecosystem. We estimate people could travel up to 25 percent more miles by 2040 than they do today. And while the shift to shared autonomy is likely to happen earlier and faster in more densely populated urban centers and rollout over time at different rates to suburban and rural areas, the overall rise in shared mobility could be significant. To serve this increased demand, new types of vehicles could emerge that will make many more trips every day than today’s personally owned driver-driven vehicles and will likely have a longer useful life. If this happens, total vehicles sold annually could decrease by as much as 40 percent in that same time frame.

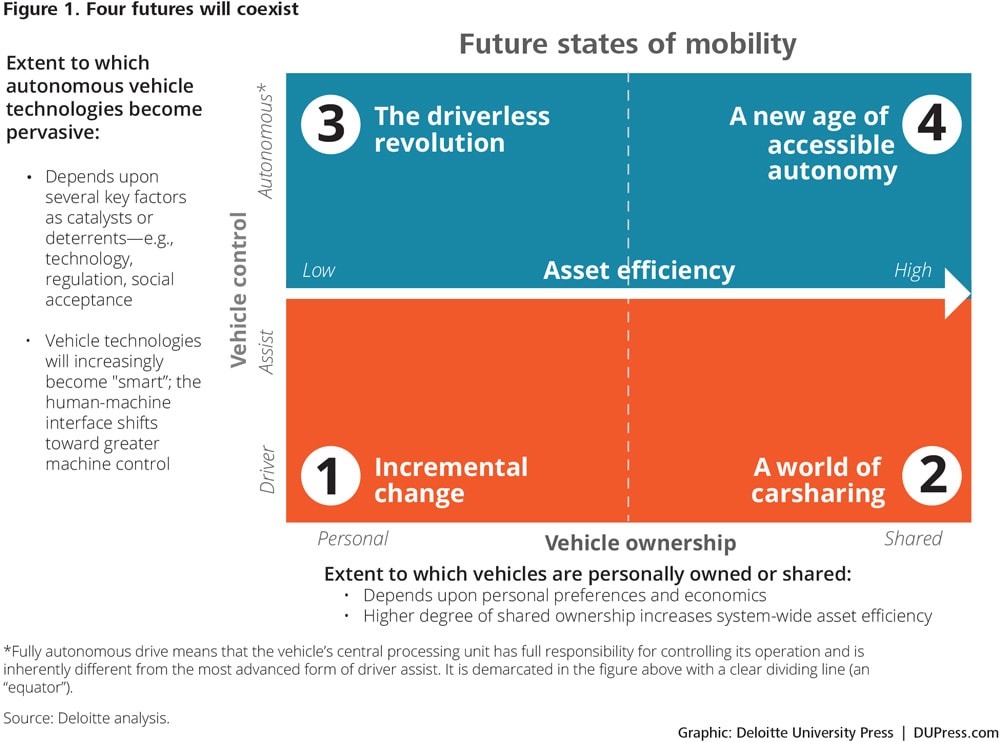

We see these developments yielding four future states of mobility (see figure 1). In future state 1, vehicles remain personally owned and driver-driven, much as today. In future state 2, driver-driven vehicles are accessed on demand, via taxis, limos, and car- and ridesharing. Future state 3 consists of personally owned autonomous vehicles. And future state 4 envisions a world of shared self-driving vehicles. The four states will likely arise unevenly, and all are likely to exist simultaneously.

* Definition: By autonomy and autonomous vehicles (AV), we refer to stage 4 of the NHTSA’s scale of autonomy—i.e., full self-driving automation in which the passengers are not expected to take control for the entire duration of travel.

Given these four future states, key questions remain unanswered: How quickly will the future arrive? And how sweeping will the transformation be? To address these uncertainties, we set out to model how the US mobility ecosystem might evolve over the next 25 years. Here you’ll find some of our initial findings about the scale and speed of expected change. Like all such efforts, this one is built on a set of assumptions that heavily influence how these results play out. We have an effort under way to more comprehensively model adoption and look forward to sharing that in the near future.

A methodology for forecasting the future

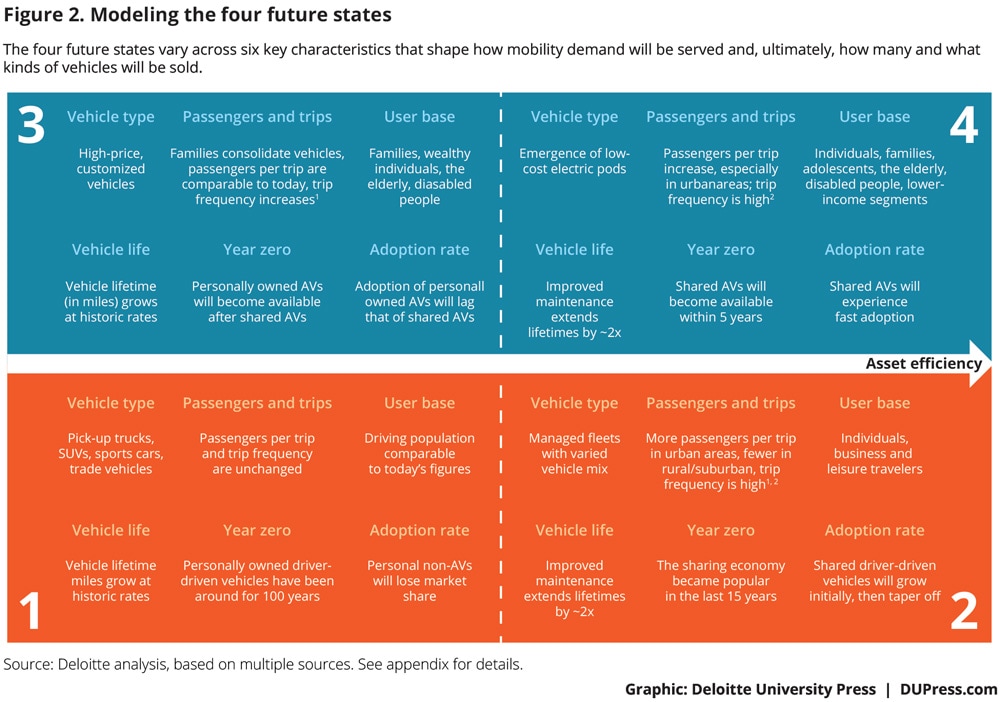

To capture overall shifts in the extended automotive industry, we chose to model new US vehicle sales through 2040. Drawing on historical data, third-party projections, and our own assumptions, our forecast incorporates an array of factors that will affect total miles driven and annual vehicle sales. Some of the key inputs include vehicle life, how much vehicles are used and by whom, and when automakers will bring self-driving cars to market, as well as critical assumptions about consumer adoption rates (see figure 2). As with any forecast, it presents a simplified view of what will be a complex future and holds many factors constant.

The four future states vary across six key characteristics that could shape how mobility demand might evolve, be served and, ultimately, how many and what kinds of vehicles will be sold.

We then estimated vehicle sales in each future state through three steps:

Project miles driven. We determined the current demand for mobility as the breakdown of miles that individuals travel (“people miles”) in urban, suburban, and rural environments and via personally owned and shared vehicles. We then applied a growth factor to those numbers to account for rising demand due to population growth (see below for additional discussion about the factors affecting total people miles).

Allocate miles to future states. Next, we assumed that shared autonomous vehicles will be launched and commercially available by 2020, and that automakers will make personally owned autonomous vehicles available soon after, in 2022. We recognize that technological change is hard to predict and may come sooner or later. We then allocated miles driven across future states using different assumptions about adoption rates to forecast how quickly consumers might embrace shared mobility and autonomous vehicles across urban, suburban, and rural populations over time (see sidebar, “Understanding adoption rates”). Because we are exploring services and technologies that are nascent, we looked at how quickly other recent technologies have been adopted. In particular, we used smartphone and cellphone adoption in the United States and Internet adoption globally as proxies for how quickly shared and autonomous vehicles might spread. Making different assumptions about the appropriate adoption rates would yield different—perhaps dramatically different—results. Other technologies, such as electricity, radio, television, and the washing machine, took significantly longer to reach similar levels of penetration than the proxies in our model.3 As such, these findings are a first approximation, and we are exploring research into more robust estimates of how adoption of shared and autonomous vehicles might actually unfold.

We also took into consideration that new modes of mobility will enable additional population segments to become independently mobile, both due to potentially compelling economics and the convenience of driverless technology.4 These steps yield an estimate of people miles driven across each of the four types of mobility for each of the three geographies: urban, suburban, and rural.

Analyze impact on unit sales. Last, we converted people miles traveled to vehicle miles traveled based on the average number of passengers per vehicle. Then, we used vehicle replacement rates based on miles traveled and vehicle lifetime miles, adjusted for expected technical advances such as the use of electric powertrains, the decreased frequency of accidents, and the better maintenance given to shared vehicles, to determine annual vehicle sales. (See appendix for a note on sources.)

As with any forward-looking estimate, our findings are necessarily subject to significant uncertainty and hinge on several key assumptions. That said, we believe our approach provides a solid foundation for initially thinking about the speed and magnitude of the changes coming to the mobility ecosystem over the next quarter century.

Understanding adoption rates

Technology adoption typically follows an “s-curve” pattern, in which a small group of early adopters establishes proof of concept before the majority follows suit, while a small percentage of holdouts resist adoption as long as possible.5 The velocity of adoption can vary significantly, but the trend has been toward increasing swiftness. It took 38 years for 50 million users to begin listening to the radio, but the Internet achieved the same milestone in just four years.6

Rather than attempt to determine adoption rates from “the ground up” using, for example, consumer attitudes, for this exercise we assumed that the adoption of shared and self-driven vehicles would follow a similar pattern as other recent technologies. In our analysis, we posited three possible trajectories of adoption—fast, medium, and slow—which we used as proxies compared with the actual adoption rates for smartphones in the United States, conventional cell phones in the United States, and the Internet globally (see figure 3). These technologies had sufficient historical data and similarities to the mobility innovations in which we were interested: They were expensive when first introduced, required significant infrastructure investment, and exhibited strong network effects. That said, there are important differences: The automobile is, for instance, a much larger fixed capital asset that most households turn over relatively slowly. Accordingly, applying different assumptions about the speed of adoption could significantly alter the model results.

Different technologies are adopted at different rates across different geographies. We use smartphones and cell phones in the United States as well as the Internet globally as a proxy for the potential growth of shared and autonomous mobility across urban, suburban, and rural areas.

Fewer cars on the road as shared and autonomous vehicles proliferate

How quickly will change happen, and how sweeping will it be?

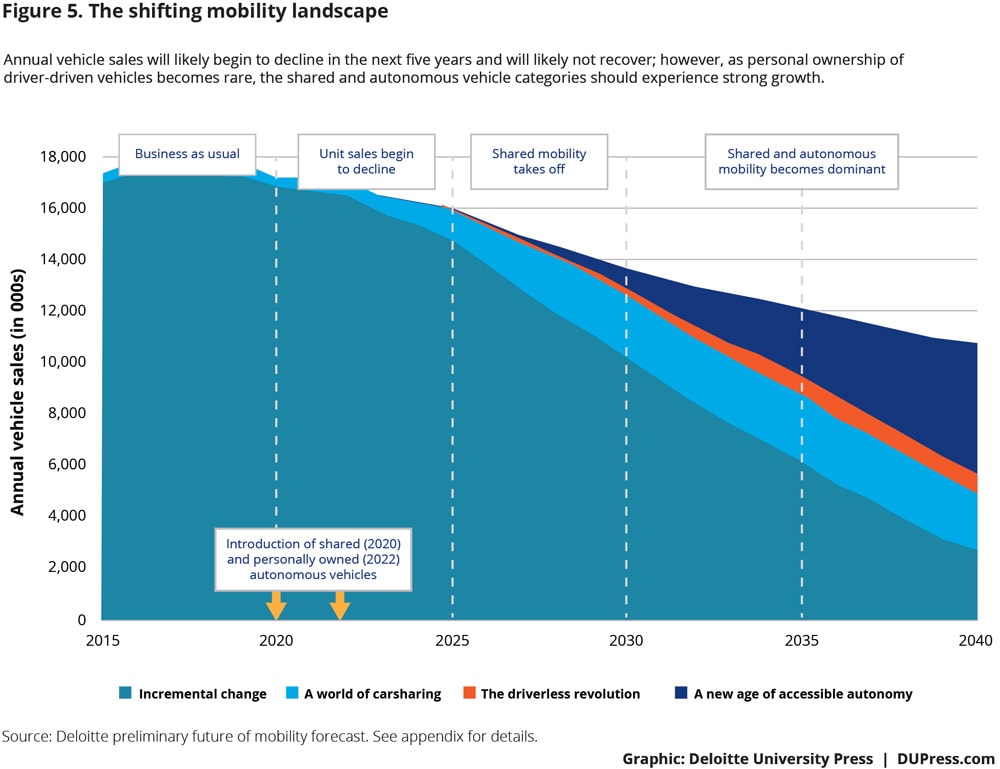

Our analysis suggests that the number of miles traveled will rise in the future—and that the mix of vehicles serving those miles will shift dramatically. Population growth and the accessibility of mobility for groups currently short of transportation options—adolescents, elderly, lower-income population segments, and people with disabilities—will likely cause total miles driven to increase by as much as 25 percent by 2040 (see figure 4). In the near term, shared driver-driven vehicles will cover an increasing portion of those miles, but after the expected introduction of fleet-based autonomous technology around 2020, shared autonomous vehicles will eventually account for the majority of miles driven.

As the population grows and more segments gain access to mobility, miles driven will likely increase by up to 25 percent, with shared mobility accounting for the majority.

At the same time, greater vehicle utilization and longer expected vehicle lifetimes will not result in an increase in the vehicles needed to serve this increased demand. Shared vehicles spend less time sitting idle and therefore drive many more miles annually; autonomous fleets may improve upon that further by using advanced algorithms that optimize routes, predict demand, and minimize empty miles. As a result, fewer vehicles can meet a higher demand. Future vehicles could also last longer, which would further decrease sales, due to the better maintenance of managed fleets compared to private vehicles, the use of electric powertrains with fewer moving parts and therefore less wear and tear, and the increased modularity of pod-like vehicles, enabling easier and cheaper maintenance.

These assumptions could also lead to a significant shift in unit sales from today’s personally owned driver-driven cars to shared and autonomous mobility.

By 2040, nearly half of new sales could be shared autonomous vehicles, while another 7 percent could be personally owned and autonomous and 20 percent shared driver-driven vehicles; just one in four new cars is likely to be akin to today’s personally owned driver-driven vehicles (see figure 5). By then, too, total annual new vehicle sales in the United States could decrease by as much as 40 percent from today’s historically high levels.

Annual vehicle sales will likely begin to decline in the next five years as personal ownership of driver-driven vehicles declines and shared autonomous vehicles experience strong growth.

Pathways to the future

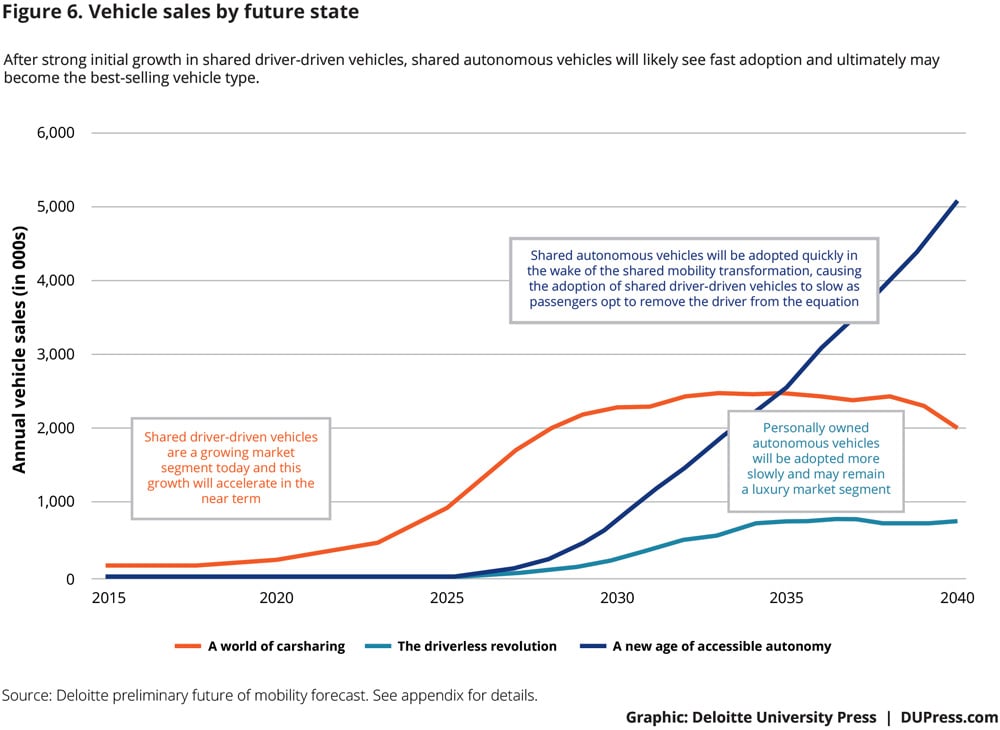

How will the adoption of shared and autonomous mobility unfold over the next 25 years? We expect a slow shift first toward shared driver-driven vehicles, before the eventual adoption of autonomous technologies (see figure 6).

The initial shift from personally owned to shared mobility is already under way, with ridesharing services available in more than 200 cities in North America.8 Ridesharing has been around for almost two decades, however, it is only with the digital revolution that it has become popular. As location-enabled apps make ridesharing more convenient, reliable, and cheaper, we expect strong growth especially in urban areas until the early 2030s, after which sales of shared driver-driven vehicles will level off at around 20 percent of total unit sales. In the late 2030s, sales of shared driver-driven vehicles will likely begin to decline as more and more fleet operators opt to replace drivers with artificial intelligence by purchasing autonomous vehicles.

Based on current pilot efforts, we expect the shift toward autonomous vehicles to begin with the introduction of shared self-driving fleets in 2020. At this point, because many consumers then will be familiar with shared mobility and its improved affordability, we anticipate the adoption of shared autonomous vehicles to follow a faster path than shared driver-driven mobility, accounting for about a tenth of vehicle sales around 2030, a quarter by 2035, and almost half by 2040.9

Personally owned autonomous vehicles could come to market shortly after fleets have tested and proven the technology—in 2022 in our model—but could follow a slower adoption curve. Uncertainty about the technology and the significantly higher cost of personal ownership, in addition to the convenience and benefits of shared mobility, will likely cause some consumers to either slowly adopt AVs in their family fleets or even forgo personal ownership. Additionally, personal autonomous vehicles, which might be highly customized, could also be expensive, further limiting demand.

After strong initial growth in shared driver-driven vehicles, shared autonomous vehicles will likely see fast adoption and ultimately may become the best-selling vehicle type.

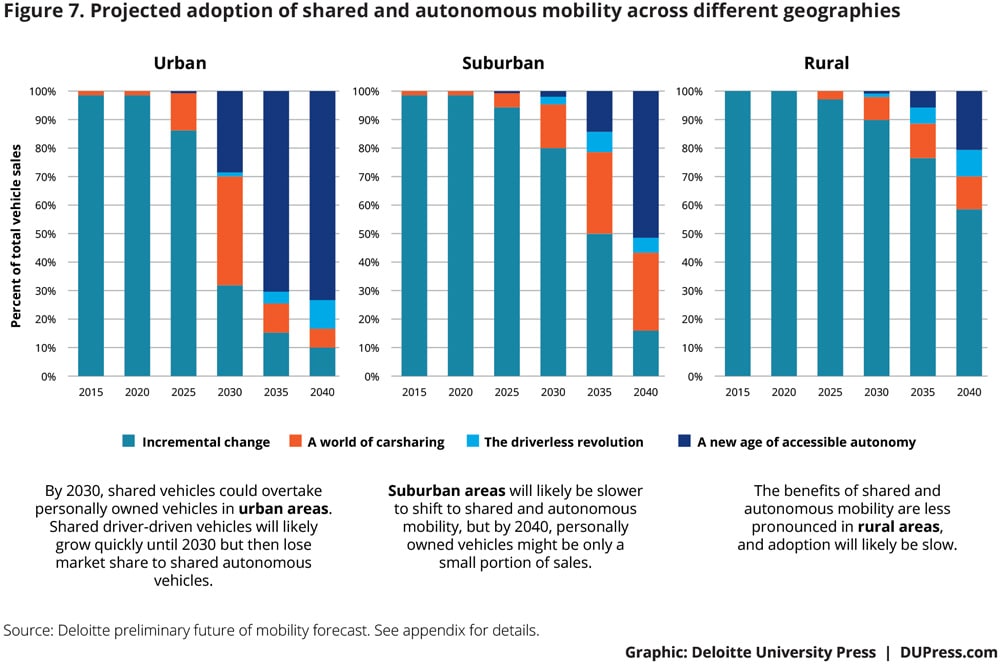

These shifts will occur unevenly and at different rates across urban, suburban, and rural populations (see figure 7). Urban areas are likely to lead the way in the adoption of shared autonomous mobility; by 2040, we estimate that more than 80 percent of miles traveled in urban areas could be done in shared self-driving vehicles. In suburban areas, shared autonomous mobility will also be in high demand, accounting for about half of all miles traveled in 2040, albeit at a slower pace of adoption. In rural areas, we anticipate personally owned driver-driven travel to remain significant—over 40 percent of miles traveled in 2040—as the benefits of shared and autonomous mobility are harder to realize and the pain points associated with traffic in cities, such as parking and traffic jams, are less pronounced.

Don’t miss the forest: Despite uncertainty, change is coming

Our findings carry important implications for companies in the extended automotive ecosystem. With vehicle sales likely decreasing significantly over the coming decades, companies that have traditionally served demand for goods and services around personally owned driver-driven vehicles will likely need to transform their business models to take advantage of new opportunities arising in the future of mobility. If our forecast holds, they will not have long to prepare for these changes, given that sales could begin declining within five years and that consumers will increasingly adopt shared and autonomous mobility over the next decade. The speed of the transformation of the automotive ecosystem may require companies to develop new technological capabilities and business models and engage in new kinds of partnerships across traditional sector boundaries.

Of course, this analysis is by no means definitive—rather, it’s a starting point for a broader discussion that we hope to foster. Even accounting for the many uncertainties and differences of opinion inherent in such projections, it is clear that change is coming to the mobility ecosystem. How will you prepare for the transformation?

Appendix

We use a range of data to calculate the impact of the four future states on unit sales:

For miles traveled in rural and urban areas: “Highway statistics,” US Department of Transportation

Federal Highway Administration, www.fhwa.dot.gov/policyinformation/statistics.cfm.

Since data on urban areas includes suburban areas, we follow economist Jed Kolko’s methodology to back out the suburban share: Kolko, “How suburban are big American cities?”, FiveThirtyEight, May 21, 2015, http://fivethirtyeight.com/features/how-suburban-are-big-american-cities/.

For shared vehicle data, we use a combination of data on the size of the rental car fleet and vehicle usage in miles used to calculate annual miles driven by rental cars: Auto Rental News, “2015 U.S. car rental market,” Fact Book 2016, page 8, www.autorentalnews.com/fileviewer/2229.aspx; Scott McCartney, “Rental cars with higher mileage populate lots,” Wall Street Journal, August 28, 2013, www.wsj.com/articles/SB10001424127887324463604579040870991145200.

We include data on annual taxi mileage: Transportation Research Board, Between Public and Private Mobility: Examining the Rise of Technology-Enabled Transportation Services, National Academies of Sciences, Engineering, and Medicine, May 13, 2016, www.trb.org/Main/Blurbs/173511.aspx.

We incorporate annual miles driven by Uber and Lyft: Pavithra Mohan, “Uber is even bigger than you realize,” Fast Company, September 8, 2015, www.fastcompany.com/3050784/elasticity/uber-is-even-bigger-than-you-realize; Anne Freier, “Uber usage statistics and revenue,” Business of Apps, September 14, 2015, www.businessofapps.com/uber-usage-statistics-and-revenue/; SherpaShare, “Uber trips are becoming longer and faster, but are they more profitable?”, SherpaShare Blog, February 2, 2016, http://sherpashareblog.com/2016/02/02/uber-trips-are-becoming-longer-and-faster-but-are-they-more-profitable; Matt Rosoff, “Uber is now more valuable than Ford, GM, and a bunch of huge public companies,” Business Insider, December 4, 2015, www.businessinsider.com/uber-valuation-vs-market-cap-of-publicly-traded-stocks-2015-12; Alison Griswold, “Why General Motors is making a $500 million bet on Lyft,” Quartz, January 4, 2016, http://qz.com/585520/why-general-motors-just-made-a-500-million-bet-on-lyft.

For projected population growth, we tap World Bank projections: “Health nutrition and population: Population estimates and projections,” World Bank, http://databank.worldbank.org/data/reports.aspx?source=Health Nutrition and Population Statistics: Population estimates and projections.

We estimate when autonomous vehicles will be launched using a thorough scan of OEM, technology companies, and subject-matter expert statements and use data on the diffusion of other recent innovations to proxy adoption rates.

Looking at generational data from the World Bank as well as poverty data from the US Census Bureau allows us to estimate what additional population segments might become mobile in the future: “Health nutrition and population: Population estimates and projections,” World Bank; Carmen DeNavas-Walt and Bernadette D. Proctor, “Income and poverty in the United States: 2014,” US Census Bureau, September 2015, www.census.gov/library/publications/2015/demo/p60-252.html.

We use several sources for information on the average number of passengers per vehicle: Transportation Research Board, Between Public and Private Mobility; Office of Highway Policy Information, “Annual vehicle distance traveled in miles and related data—2014,” US Department of Transportation Federal Highway Administration, December 2015, www.fhwa.dot.gov/policyinformation/statistics/2014/vm1.cfm; and Taylor Soper, “Lyft’s carpooling service now makes up 50% of rides in San Francisco; 30% in NYC,” GeekWire, April 22, 2015, www.geekwire.com/2015/lyfts-carpooling-service-now-makes-up-50-of-rides-in-san-francisco-30-in-nyc/.

And to project vehicle lifetime, we take US government data and apply the historic rate of lifetime improvement going forward: National Center for Statistics and Analysis, Vehicle Survivability and Travel Mileage Schedules, National Highway Traffic Safety Administration, January 2006, www-nrd.nhtsa.dot.gov/Pubs/809952.pdf.