2023 Deloitte holiday retail survey

Holiday spirit (and spending) is back as shoppers and retailers gear up for a return to prepandemic spending levels.

Nick Handrinos

Brian McCarthy

Stephen Rogers

Lupine Skelly

Kusum Raimalani

As the US economy continues to stave off a recession, it wouldn’t have come as a surprise to see consumers pull back on their holiday spending this year. However, our findings from the 2023 Deloitte holiday survey indicate that consumers are steadfast in their intent to live in the moment and make this holiday season memorable. They plan to spend an average of $1,652 this season, surpassing prepandemic figures for the first time.

There are several factors at play. Participation levels have been inching up since record lows in 2021; this year, 95% of consumers say they plan to purchase during the holiday season. In addition, consumers are factoring in inflation, with three-quarters expecting higher prices year over year. We’re also seeing strong spending from the $50K–$99K and $200K+ income groups. In short, the tinsel is no longer in a tangle.

Although many shopping trends are finding equilibrium this year, there are still cracks in the foundation. Savings rates have dwindled, and 17% of respondents say they have student loans to start repaying this fall, causing some to cut back on holiday expenditures.

For retailers, a winning strategy may come down to driving value around key promotional events for inflation-wary customers. Expected participation rates for promotional events are robust, with a quarter planning to shop on October promotional days and 66% (versus 49% in 2022) planning to shop the week of Black Friday-Cyber Monday (BFCM). The promotional timing will be crucial as consumers intend to wrap up their shopping in just 5.8 weeks—a timeframe that has shrunk from 7.4 weeks prepandemic. The old retail adage of “having the right product, at the right price, at the right time” may ring true more than ever this year.

Read on for key takeaways and download the full survey findings.

Holidaying like it’s 2019!

Holiday spirit (and spending) has rebounded—consumers expect to spend $1,652, surpassing prepandemic levels for the first time. As consumers grapple with inflation expectations, they plan to spend 14% more YoY. However, the compounded annual growth rate has increased a modest 2.5% since 2019.

{kind=link}

What it means for retailers

Even as the economy continues its uncertain trajectory, consumers are looking to splurge on the holidays this year and make the season memorable. Many trends, including spending, have normalized or surpassed prepandemic levels, indicating consumers may be ready to put pandemic restraints behind them.

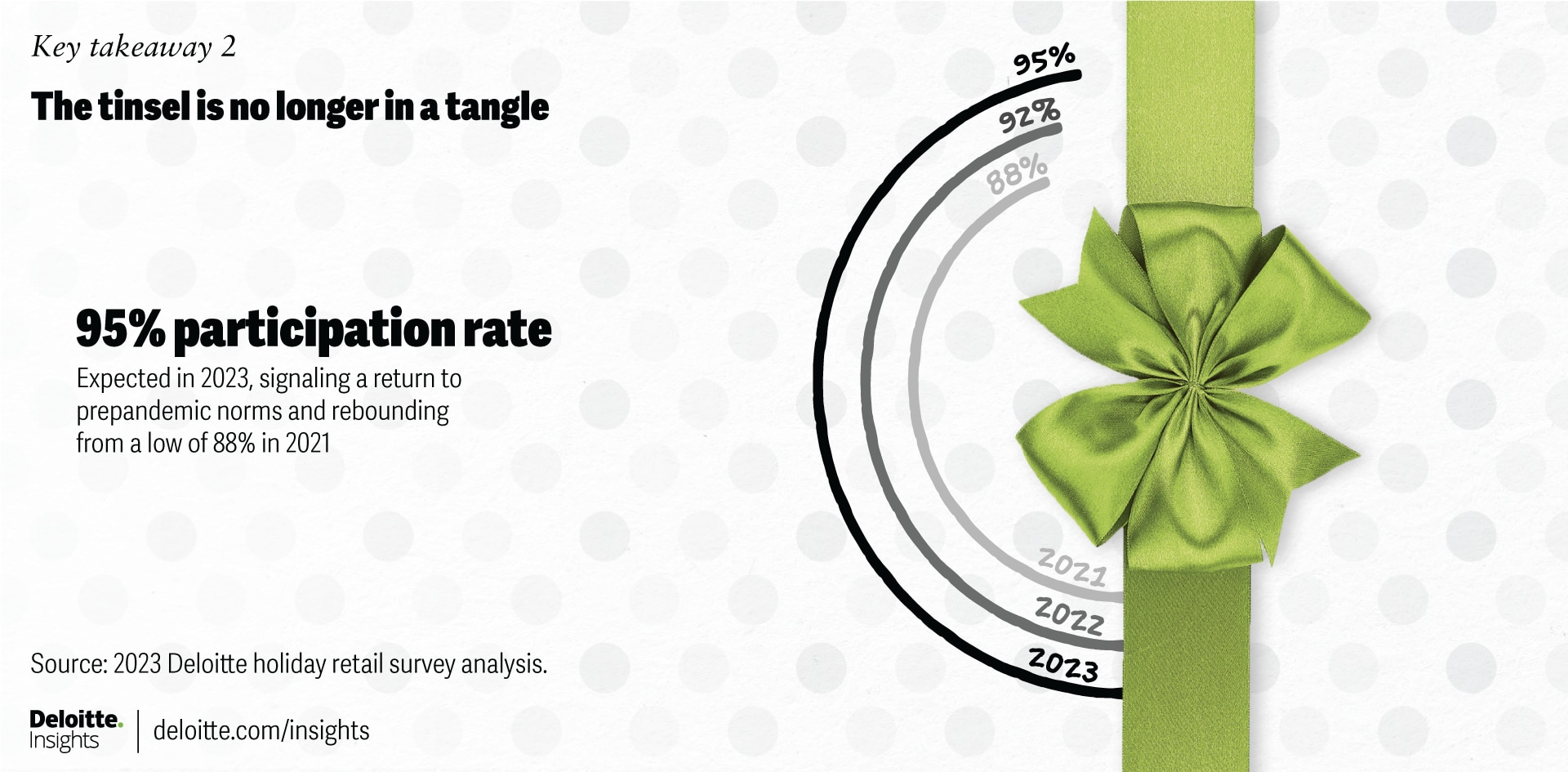

The tinsel is no longer in a tangle

As consumers look to put the fun back in festivities, three factors have contributed to the uptick in spend: Consumers are participating at a higher rate (95% versus 92% in 2022 and 88% in 2021); they’re expecting higher prices (72%); and the $50K–$99K (+26%) and $200K+ (+22%) income groups are splurging.

{kind=link}

What it means for retailers

The $50K–$99K and $200K+ income groups plan to invest heavily in nongift items after showing restraint the past two years. Retailers will have opportunities to appeal to these groups as they restock holiday decorations, furnishings, and holiday apparel.

‘Tis the season for balancing budgets

With consumers expecting higher prices, they are making adjustments to stretch their budgets. They plan to buy fewer gifts (eight versus nine in 2022), spend more on gift cards ($300 versus $217 in 2022), and pounce on promotional events, with 66% (versus 49% in 2022) intending to purchase during the BFCM week.

{kind=link}

What it means for retailers

With consumers on the hunt for a bargain, retailers’ best opportunities for gains may occur around promotional periods, especially as consumers only plan to shop 5.8 weeks this year, down from 7.4 weeks prepandemic.

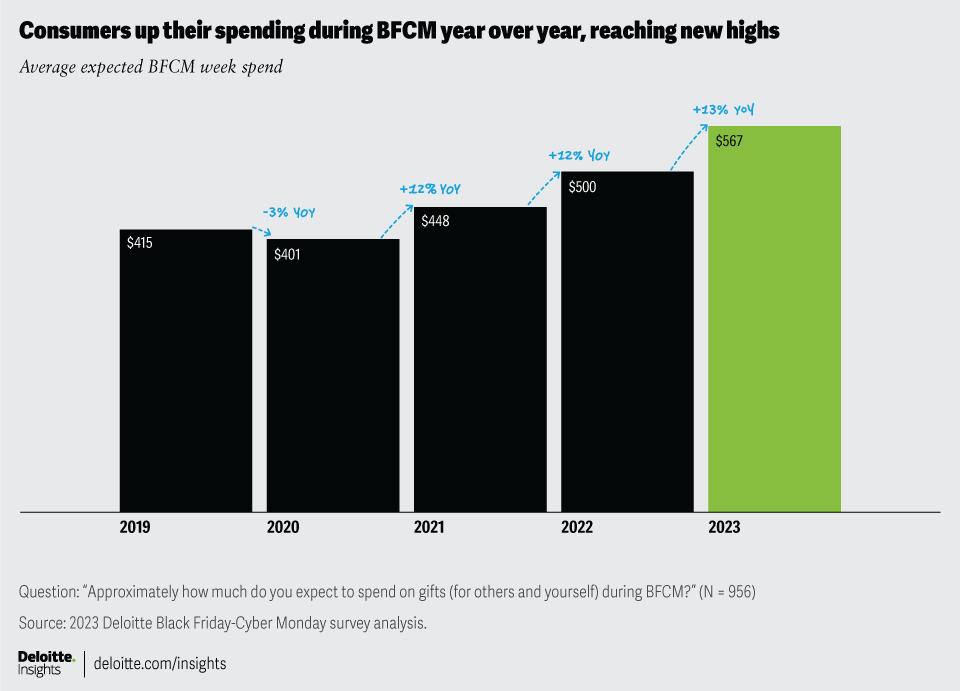

2023 Deloitte Black Friday-Cyber Monday survey trends

As inflation-wary consumers look to stretch their budgets, 80% plan to shop during Black Friday-Cyber Monday (BFCM) and spending is set to reach a new high of $567 (+13% versus 2022).

{kind=link}