Tax Incentives Related to Investments in Carbon Neutrality Bookmark has been added

This article is a content of “Japan Incentive Insights”, a search service for preferential tax systems and subsidies in Japan. The information in this article is based on the data as of August 30, 2024, and may differ from the most recent information.

Japan Incentive Insights : Tax Incentives Related to Investments in Carbon Neutrality

1. Overview

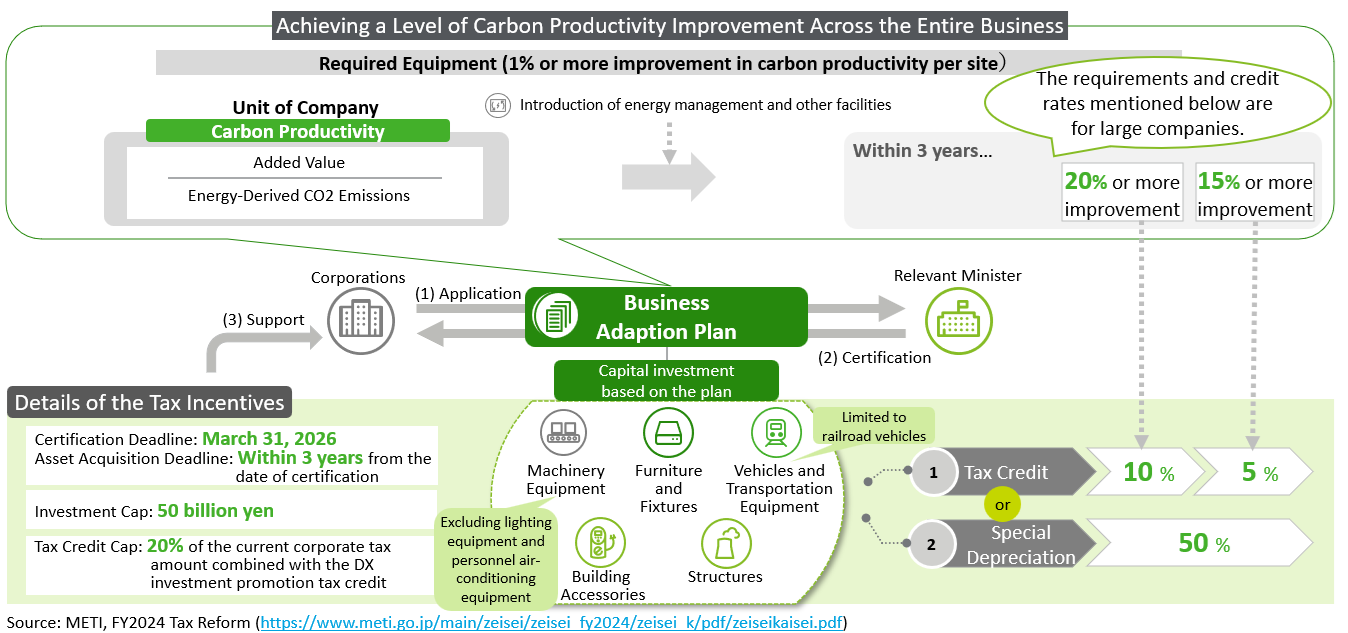

A tax incentive related to investments in carbon neutrality ("CN Tax Incentive") was established in Japan to accelerate decarbonization investments by private enterprises aiming for carbon neutrality by 2050. This tax incentive can be applied to the introduction of equipment that simultaneously achieves decarbonization of production processes and enhancement of added value. For example, this could include acquiring equipment that offers higher energy efficiency compared to older models previously utilized in factories. If applicable, businesses can benefit from a tax credit covering a certain percentage of their equipment acquisition costs (ranging from 5% to 14%), or opt for a special depreciation of 50%. These benefits are available up to a maximum investment limit of 50 billion yen.

For the application of the CN Tax Incentive, it is necessary to submit a "Business Adaptation Plan" that outlines the decarbonization effects expected from the investment, and obtain certification from the relevant ministries by March 2026 (the facility investment must be completed by March 2029). The certification process may take about six months. Meeting the certification requirements necessitates early consideration and efficient promotion due to the need for coordination among multiple internal departments and related government ministries.

2. Examples of Certified Equipment

As of the end of March 2024, 166 cases have been certified under the CN Tax Incentive. Common types of equipment investments include:

(1)Production equipment

Replacing aging production equipment with more energy-efficient facilities, significantly enhancing productivity, and reducing CO2 emissions.

(2)Cogeneration and biomass boiler systems

Updating power generation facilities that use heavy oil or coal to lower-carbon fuels such as LNG, city gas, or biomass.

(3)Private consumption solar power generation equipment

Installing solar power generation facilities totaling over 1 MW (or with an installation area exceeding 10,000 square meters) on factory roofs or idle land and using the generated electricity for in-house consumption at the company’s factories or offices.

3. Preparation for Application

Companies planning to invest in large-scale facilities (over 1 billion yen) aimed at achieving decarbonization should consider applying for the CN Tax Incentive. This applies not only to updating existing facilities but also to acquiring new equipment during the construction of new factories.

If you are considering applying for the CN Tax Incentive, please consult with Deloitte Touche Tohmatsu for further guidance.

Related Links

- Japan Tax & Legal Inbound podcast/webcast Series

- Dbriefs Podcasts

- Apple Podcast - Deloitte Dbriefs Asia Pacific

- tax@hand

Dbriefs Asia Pacific SNS & Video

Facebook | Twitter / X | LinkedIn | YouTube

Recommended for you

Opens_in_a_new_window