Gaming Bookmark has been added

Predictions

Gaming

TMT Predictions 2021

Perspective from Japan: Business trends in the transitioning gaming industry

Explore Content

- 1. Future outlooks based on the evolutionary trajectory of gaming consoles

- 2. Full-scale development of cloud gaming and the turning point for the gaming industry

- 3. The potential of capital alliances in gaming company expansion strategies

- 4. Shifts toward an era of Experience Sharing – community changes and influence

【The original report for this translation was issued in April 2021. Things may have changed since then.】

In this report, we examine business trends in the gaming industry from each of the following four perspectives: "console manufacturers", "cloud gaming", "capital alliances", and "gaming communities".

As of 2021, in the console market, Sony is aiming to enhance the high-end gaming experience with high-definition graphics and haptic technology through the PS5's radical functional improvements. Meanwhile, the Nintendo Switch is creating hits through the development of software and services that appeal to a broad range of ages while leveraging past Intellectual Properties (IPs). At the same time, the entry of platformers including GAFAM into the cloud gaming market is in full swing, and we are beginning to see clear trends that may lead to changes in the traditional structure of the gaming industry.

While analyzing the perspectives of console manufacturers and cloud gaming stakeholders to investigate the current status and outlook of the gaming market during this transitional period, we also summarize the trends in capital alliances, which are considered important for game companies attempting to expand their business and present directions for strategies. Furthermore, we focus on “gaming communities” as an ingredient to be used for grasping the newest trends for game users, who are indispensable for companies looking to develop their gaming business, and we analyze the development of these communities as well as key points for awareness. Each of these sections should be useful for deriving hints and keywords toward anticipating the future of the gaming market. We hope that this chapter will help gaming industry stakeholders interpret changes in the market from their own individual standpoints and consider how to develop their company's business in the future.

1. Future outlooks based on the evolutionary trajectory of gaming consoles

Recent game console sales status

As of March 2021, the latest home video game console1 devices on the market are Sony's PlayStation 5 (PS5) and Microsoft's Xbox Series X/S, both of which were launched in November 2020. Each has a dedicated edition for downloading games online, as well as an edition with a traditional disk drive. This reflects the changes in lifestyles accompanying such factors as the improved speed of home internet connections. Meanwhile, Nintendo has seen a steady increase in sales of the Nintendo Switch since its 2017 launch, and has also launched the Nintendo Switch Lite in 2019, which is an inexpensive model that only supports handheld play mode and is not compatible with the Nintendo Switch dock for enabling TV output. See Table 9-1 for the current number of units sold for each company.

Differences in business policies based on each company's hardware specs

A look at the latest hardware deployed by each company highlights clear differences in business policies.

First, one of Sony's key concepts is to revolutionize the gaming experience by utilizing the "sense of immersion" that they have been aiming for with their head-mounted VR units. One example of this is the haptic5 technology built into the PS5 controller which digitally reproduces the sense of touch. The main unit itself also strives to create a sense of immersion through improved ray tracing6 for greater realism and using high-speed7 loading to enable a seamless gaming experience. As the number of multi-platform games is continuing to increase recently, the company's strategy is clearly for differentiation through hardware using haptics technology, which cannot be achieved by mobile applications or gaming PCs.

Microsoft's Xbox Series X has enhanced hardware specs on par with the PS5, but they did not make any particular alterations to the controller this time. While manufacturing for the Xbox has currently been discontinued, the company's gesture and voice recognition device, Kinect, has played a major role in fostering early immersive experiences8, and eyes are on the direction that this will take in the future. Meanwhile, Microsoft previously offered a beta version of its cloud service, Project xCloud9, but now it has combined this with its subscription service "Xbox Game Pass Ultimate10". Microsoft's strategy seems to be to bring users into the company's economic sphere, regardless of the hardware being used.

Meanwhile, Nintendo is placing emphasis on experiences built around how games are operated through expanding its line of peripheral devices rather than on the Switch unit itself. Nintendo Labo11 (as of this report written in March 2021, their most recent release was in 2019), Ring Fit Adventure12, and Mario Kart Live Home Circuit13 are examples of how Nintendo's policy differs from the other two companies as it aims to enhance experiences through external attachments rather than the evolution of the Switch itself. The linking of Switch controllers (Joy-Cons) with external attachments was an idea born from both the hardware and software sides in the pursuit of the Joy-Con's possibilities. Nintendo has taken its first step outside of the traditional territory of video games14 toward becoming "a company that creates new forms of entertainment". We can see that the company is looking to use its own devices as a starting point for expanding the home entertainment experience for users, integrating the concept of "play" in a broader sense, including crafts and exercise.

The rise of cloud gaming and startups

In the past, gaming platforms and devices used to be domains held exclusively by gaming companies, but traditional console manufacturers are facing the emergence of rivals due to the recent entry of platformers such as GAFAM as well as startups.

The common keyword for both Google and Amazon is "streaming".

Google began services in North America and Europe for its cloud gaming platform Stadia15 in November 2019, and Amazon has also announced its own service, Luna16. These services do not require specialized devices such as stationary consoles, as processing and execution is handled via the cloud. A supported device such as a PC as well as a controller is all that users need to enjoy games. In 2020, Facebook launched a way of playing cloud games within Facebook Gaming17. Unlike the previous two companies' efforts, this is not based on a monthly subscription, but is rather being rolled out on a free-to-play basis as of its launch. Apple provides a game subscription service, Apple Arcade18, and it also continues to open its doors to cloud game developers through methods such as its 2020 revision of its App Store guidelines19. For detailed information on cloud gaming, please refer to "Full-scale development of cloud gaming and the turning point for the gaming industry".

Meanwhile, turning our attention to startups, one company cited as unique is KAT VR. While current commercial VR devices offered in arcades allow users to walk in virtual space by actually using their feet, existing home devices do not allow users to do the same. However, KAT VR's VR mechanical device can reflect 360 degrees of human motions in VR games, making it possible to create experiences that increase the sense of immersion of actually walking in the game world by yourself20, 21

Future outlook for game consoles

In addition to the rise of players such as GAFAM, startups, and other businesses, there has been a rapid increase in the popularity of games among casual consumers over the past decade due to the spread of smartphones and game applications. Another important factor driving changes against this backdrop is the fact that the game user base is expanding significantly. Along with this trend, there is increasing diversification in elements such as devices/platforms, game content, and transmission channels, and the flexibility in the combination of choices in the environment surrounding game users has increased dramatically.

Main examples of diversifying choices

- Devices/platforms: Consoles/PCs/mobile applications (smartphone, tablet, etc.)

- Game contents: A broad range of targets, from high-quality games to casual games

- Transmission channels: Discs/downloading/online/cloud

Console manufacturers are facing a major turning point in this environment. There are three main directions that may be considered as prospects for console manufacturers to focus on in the future.

- Focus on pursuing a gaming experience that can only be achieved through consoles, fostering extraordinary experiences/immersion through improving hardware specs

- Limit emphasis on the role of the console to being only an interface for gaming, and instead work on strengthening applications/contents to enable multi-platform releases

- Rather than being limited to the company's own assets, consider consoles as a single module and expand functions through acquisitions/alliances with other companies as well as overseas companies.

With the advent of cloud gaming, which allows users to play games on any device, console manufacturers will be required to find ways to emphasize the value and appeal of consoles' unique qualities. Consoles are devices that are fundamentally optimized for playing games, and console manufacturers may need to pursue directions that leverage this characteristic by creating "experiences that amaze users". There is also the view that the "experiences" here are not necessarily limited to high-end technology such as the VR and haptics mentioned in option 1. The creation of new experiences through the combination of peripheral devices could also be said to represent new value. Even in cases like option 2. or 3. where companies use consoles as interfaces and modules, there will still be a need to foster experiences that draw in users according to each situation.

In this regard, we expect that it will become essential to answer user demands by identifying trends in the user community and the contents being handled. For this, it will also be key that companies are flexible in making use of measures such as acquisitions and alliances when there is a capability that the company needs.

When looking into the future of consoles, it is also important to consider how contact points with games are created in the course of game users’ growth. In Japan, the majority of current console game users' gaming experience is assumed to have begun at an early age with consoles as a starting point. On the other hand, in South Korea, PC games are widespread, and many people's first experience with games was from the PC games they were exposed to in their childhoods, while their first contact with consoles was around the age of entering university22. From these examples, it can be inferred that the devices one has played with in childhood influence one's choice of gaming environments in later years, and companies may need to consider this in their strategies. In this regard, we must also keep in mind that the rapid spread of smartphones is shifting the gaming contact point for many Japanese game users to mobile devices (smartphones, tablets, etc.), particularly for casual gamers. There will be an even greater need for companies to choose correctly when making strategic decisions in the future, including how to promote the value that only consoles can offer, how to continue to attract the next generation of game users, or whether to change the company's business model.

Identifying directions, such as which users the company should target, and the degree of focus given to both "high-end" and "low-end" contents and devices as the company develops its gaming business, will become a key point for consideration in the future console market.

1. Devices/equipment for playing console video games

2. Sony, “Summary of Consolidated Financial Results for the Third Quarter of FY2020” 2021/2/3: https://www.sony.co.jp/SonyInfo/IR/library/presen/er/pdf/20q3_sonyspeech.pdf

3. Global consolidated cumulative sales volume; Nintendo, “Information for Shareholders and Investors: Performance and Financial Information - Sales Results of Video Game Consoles (nintendo.co.jp)”, accessed 2021/3/24: https://www.nintendo.co.jp/ir/finance/hard_soft/index.html

4. PS5 and Xbox Series X|S launch sales match, but don’t improve on, previous generation, Ampere Analysis Insights, 2021/2/17: https://www.ampereanalysis.com/insight/ps5-and-xbox-series-xs-launch-sales-match-but-dont-improve-on-previous-generation

5. Haptics = "Technology that digitally reproduces the sensation of a person touching an object, making it feel as if they are touching it even though they are not actually touching it; Technology to stimulate the "sense of touch", one of the five senses - Ventures into haptics, Sony Interactive Entertainment, 2020/12/2: https://www.sony.co.jp/SonyInfo/technology/stories/Haptics/

6. Ray tracing: Technology that tracks the movement of photons in the air and simulates refraction and reflection to create images in a method similar to reality; "What I learned about the role the PlayStation 5 will be responsible for in the next six years by actually playing it", ITMedia, 2020/10/5: https://www.itmedia.co.jp/news/articles/2010/05/news086_3.html

7. Real device reviews: The reality of “Game experiences turning into social media” on the PS5. The surprisingly silent, high-speed loading was amazing. BUSINESS INSIDER, 2020/11/6: https://www.businessinsider.jp/post-223666

8. Microsoft Kills off Kinect (For Good This Time) With Xbox Series X, GIZMODO, 2020/7/16: https://gizmodo.com/xbox-series-x-kills-off-kinect-for-good-this-time-1844412885

9. I tried playing Microsoft's cloud service "Project xCloud". You can play consumer games whenever or wherever you like without a hitch as long as you have the play environment for it, 4gamer.net, 2020/12/5: https://www.4gamer.net/games/453/G045384/20201204060/

10. Microsoft, “Project xCloud (preview) | Xbox”, accessed 2021/3/24: https://www.xbox.com/ja-JP/xbox-game-streaming/project-xcloud

11. Nintendo, “NINTENDO LABO”, accessed 2021/3/24: https://www.nintendo.co.jp/labo/

12. Nintendo, “Ring Fit Adventure”, accessed 2021/3/24: https://www.nintendo.co.jp/ring/index.html

13. Nintendo, “Mario Kart Live Home Circuit”, accessed 2021/3/24: https://store-jp.nintendo.com/list/software/70010000012353.html

14. Nintendo, “Management Policy Briefing/March 2018 term, Third Quarter Results Briefing, Q&A (summary)”,2018/2/3: https://www.nintendo.co.jp/ir/pdf/2018/180203.pdf

15. Google,“Stadia”, accessed 2021/3/24: https://stadia.google.com/

16. Amazon.com, “Amazon Luna”, accessed 2021/3/24: https://www.amazon.com/luna/landing-page

17. Facebook, Entry into Cloud Gaming (not available for iOS due to Apple's restrictions, however), ITmedia, 2020/10/27: https://www.itmedia.co.jp/news/articles/2010/27/news060.html

18. Apple, “Apple Arcade”, accessed 2021/3/24: https://www.apple.com/jp/apple-arcade/

19. Apple opens its doors to cloud game service provision through the App Store. Requirements are strict, however, resulting in backlash from manufacturers, AUTOMATON, 2020/9/12: https://automaton-media.com/articles/newsjp/20200912- 136588/

20. KATVR , “KAT VR - Official Developer Site | About KAT VR”, accessed 2021/3/24: https://www.kat-vr.com/pages/kat-vr-learn-more

21. Treadmill-style full-body experience home arcade unit "KAT Walk C" is scheduled to appear on Kickstarter, Dospara Express, 2020/6/8: https://www.dospara.co.jp/express/vr/spo1511766

22. KOCCA(Korea Creative Content Agency), “2019 Game Users Survey Report”, 2019

2. Full-scale development of cloud gaming and the turning point for the gaming industry

Two directions for discussion concerning cloud gaming

Sony launched sales of its next-generation console, the PS5, in November 20201. Reservations are pouring in for the PS5, and the console is said to be off to a good start. Meanwhile, however, competition in the industry is expected to become even fiercer in the future as major IT platformers such as GAFAM (Google, Amazon, Facebook, Apple, and Microsoft) enter the gaming industry one after another. The game services provided by these IT platformers are all cloud game services. Cloud games are characterized by the fact that they do not require dedicated hardware/game consoles and can be played on the user's device of choice, and by the fact that they use a subscription model with continuous, fixed charges.

There are two major arguments on the future of Japan's gaming industry. First, there are those who see cloud gaming as a threat, with opinions such as: "Cloud gaming provided by GAFAM and others will disrupt the existing gaming industry and replace everything", or "GAFAM and others will swallow the Japanese gaming industry". In particular, the fact that image processing and data storage are performed in the cloud means that dedicated game consoles become unnecessary. This leads the possibility that cloud games are likely to have a negative impact on the business of leading Japanese operators such as Sony and Nintendo, whose business has traditionally been centered on their own game consoles. This discussion often uses the analogy of the evolution of video streaming, which has replaced physical media such as DVD and Blu-ray with digital.

Meanwhile, the other side of the argument is that, cloud gaming services are designed to perform computational processing in the cloud, which limits transmission quality and server computing power. Because of this, they are unable to provide a satisfactory customer experience to game users, which gives traditional game consoles the advantage. Designated gaming consoles perform extensive computation processes in order to process input from the controller and reflect the results of this on the display at a speed that matches the characteristics of each games. In particular, realistic expression of physics and 3D video processing have become widespread in recent popular games such as "Ghost of Tsushima2" for the PS4. It is assumed that these types of customer experiences will be technically difficult to achieve in cloud gaming.

There is also the standpoint that gaming only becomes a true experience when hardware (e.g., the feel of the controller) and software are fully integrated with each other. Furthermore, some believe that cloud gaming services provided by IT platformers do not have enough content that meets the demand of the market to attract users with their game titles.

Background of IT platformers' entry into cloud gaming

Why are IT platformers entering the cloud gaming market one after another in the first place? Simply put, the main objective is to build and expand the company's economic sphere by bringing users into its platforms. For example, Google is adding the cloud gaming service Stadia3 to its existing services such as its search engine, storage, email, and YouTube as part of a service bundle in an effort to keep its hold on users. Amazon offers music, videos, e-books, and other services with a focus on its Amazon Prime next-day delivery service, and is looking to add Luna4, a cloud gaming service, to attract more users in the future. All of them are trying to create draws to bring in users by creating multiple sets of services and touch points that users find appealing and grow their businesses through cross-selling.

Issues such as technical barriers for running cloud games are expected to gradually be resolved. The three entrants, Amazon, Google, and Microsoft are all global cloud vendors, and will probably use their own infrastructures for evolving data center/communications technology to steadily solve technical issues. As for the content shortage, it is predicted that the companies will move forward with partnerships/acquisitions of blue-chip companies. They may also produce their own original games as seen in the trends in video streaming that led to Netflix and Amazon Prime Video planning and producing original contents.

On the other hand, there are business opportunities for Japanese companies as well. For example, Japanese telecommunications carriers SoftBank and KDDI are also moving in line with IT platformers' trends by making steady efforts toward entering the cloud gaming market. Both companies have partnered with NVIDIA to offer cloud gaming service GeForce NOW in a subscription format for the Japanese market. Rather than generating significant revenue from cloud gaming on a stand-alone basis, telecommunications carriers are predicted to use cloud gaming as a killer use case to prove the capabilities of 5G's enhanced broadband and low latency technology, and drive its penetration throughout Japan. It is assumed that companies are aiming to improve the profitability of their entire consumer business by bundling cloud gaming with their mobile business as offered contents along with their 5G network service in the future. As the market for cloud gaming expands, telecommunications carriers may gain significant business opportunities while verifying the need for 5G.

The necessary perspectives for the turning point in the gaming industry

However, it is undeniable that cloud gaming provided by IT platformers will become a threat to existing players in the Japanese game industry. Even if the performance of dedicated game consoles, the handling of controllers, and Japan's unique and wonderful game content are enough to bring game users in currently, IT platformers boast a myriad of highly convenient touchpoints, massive computing power, big data and cash, and this will have a profound impact on the existing gaming industry as these platformers steadily resolve their own issues and increase their presence in the gaming market.

While the current gaming business will not be immediately replaced by cloud gaming, it is expected to become an option for consumers within the next few years, enabling them to access and immediately play high-performance games from their smartphones and other non-console devices. Games in which the devices and customer experience are closely connected, such as VR games, are expected to become more popular, so devices designed specifically for playing games will continue to remain in some form. Even if this is the case, however, the form gameplay has taken up until now may inevitably have to change.

The gaming industry is currently at a major turning point. In order to survive, Japanese companies must continue to redefine their strategies based on a solid understanding of platformer trends, as well as trends in technology such as the cloud, 5G, and big data. It will also be necessary to consider how to leverage the relationships with in-house services, utilization of new technologies, and cooperation with other industries.

1. PlayStation®5 Japanese domestic release set for November 12, 2020, Pre-orders to start on September 18. Available at retailers and e-commerce sites nationwide, Sony Interactive Entertainment, 2020/9/17: https://www.jp.playstation.com/press-releases/2020/20200917/

2. PLAYSTATION.COM, “Ghost of Tsushima”, accessed 2021/2/19: https://www.playstation.com/ja-jp/games/ghost-of-tsushima/

3. Google,“Stadia”, accessed 2021/2/19: https://stadia.google.com/

4. Amazon.com, “Amazon Luna”, accessed 2021/2/19: https://www.amazon.com/luna/landing-page

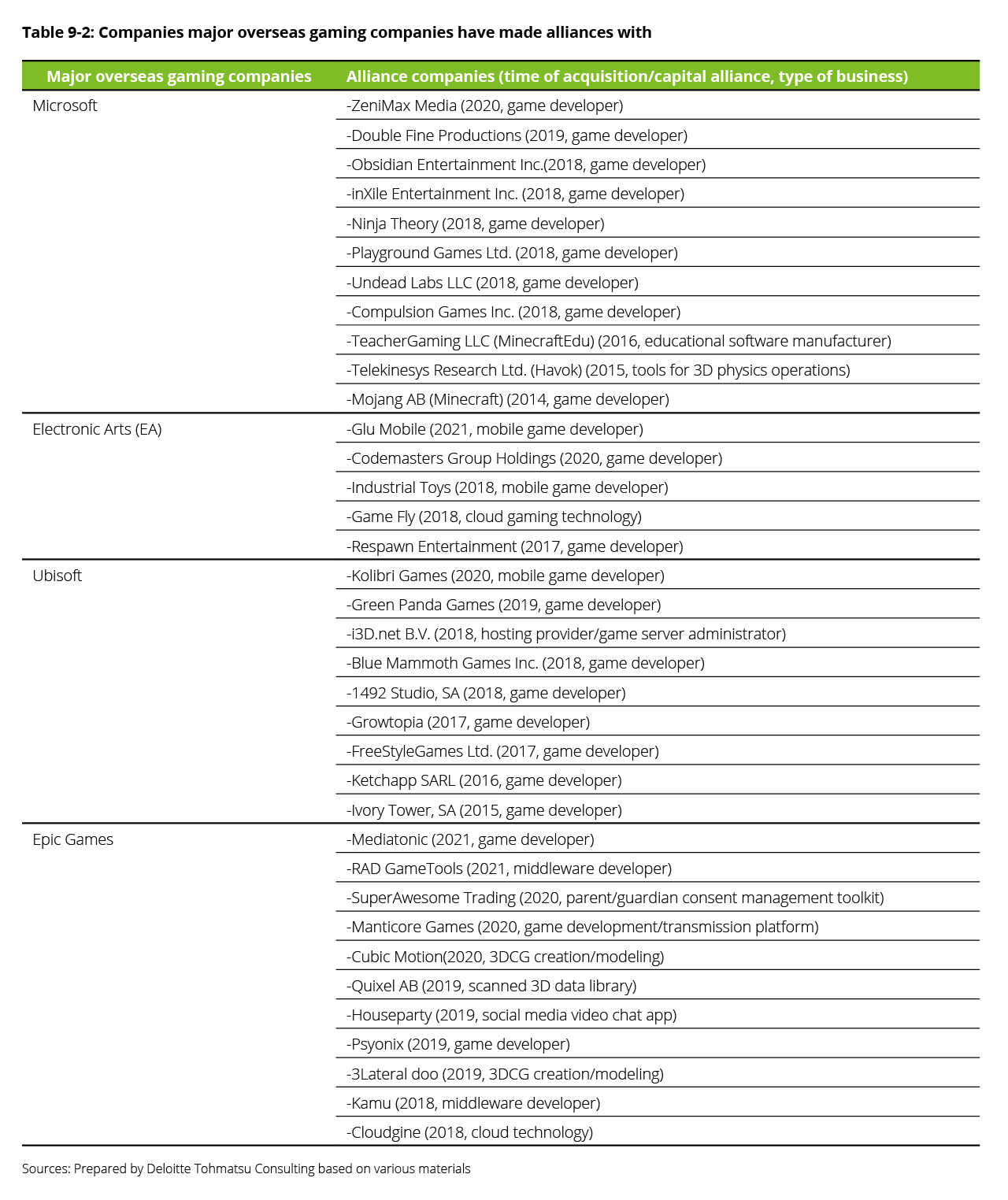

3. The potential of capital alliances in gaming company expansion strategies

Recent gaming industry restructuring trends

In recent years, the gaming industry has seen a series of major acquisitions by major gaming platformers, major game developers, and IT platformers.

In 2014, Microsoft purchased Minecraft developer Mojang for USD 2.5 billion. After this purchase, it continued to make purchases of large game studios, including Ninja Theory Ltd, Playground Games, and Undead Labs in 2018, and ZeniMax Media (with subsidiaries that include Bethesda Game Studios and id Software) in 2020 for USD 7.5 billion.

Apart from these, there were also acquisitions such as Sony Interactive Entertainment (SIE)'s 2020 purchase of Insomniac Games (USD 229 million) and Electronic Arts' purchase of Codemasters Group Holdings (USD 1.2 billion).

The following factors exist in the background of these major acquisitions:

- Intensifying competition among gaming platforms (console/cloud gaming/mobile, etc.) for user acquisition

- Increasing need for efficiency in response to the increase in software development scale and costs associated with improvement of hardware specifications

- Longer development periods separating AAA titles1 from smaller titles

- Intensification of smartphone game development in China

Due to these factors, aggressive acquisition activity in the gaming industry is expected to continue in the future.

Global trend of developing business through the acquisition of gaming companies

In the midst of these trends, there are many cases of large acquisitions being made overseas as companies clearly define their own areas of strength and endeavor to use acquisitions to strengthen those areas. Companies are also making acquisitions to respond to future changes in gaming industry business models, including the growth of the cloud gaming market and the spread of subscription- based sales formats. Behind this is the increased competition to bring in users as well as the growing importance of portfolio strategies in developing game titles.

Major game developers such as Electronic Arts and Ubisoft are enhancing the brand value of their AAA titles and strengthening their support for mobile games and cloud gaming. They are also actively making acquisitions of companies that own gaming-as-a-service (GaaS) games, which are a category of games for generating continuing revenue, and are expanding into areas where they can continue to generate revenue during large-scale production periods for their own AAA titles.

Microsoft has continued to make major acquisitions of game development companies starting at the end of the Xbox One's lifespan with the purchase of Mojang (which owns Minecraft) and continuing to the present day. The company aims to increase users on its own Windows and Xbox platforms by increasing the number of high-quality games available only on its platforms.

This activity comes against the backdrop of the Xbox One lagging significantly behind the PlayStation 4 in sales, and is Microsoft‘s attempt to regain lost ground. By enhancing the value provided by its Xbox Game Pass and Project xCloud offerings, Microsoft was able to increase the amount of exclusive content offered only on its platform and make it more attractive. Additionally, in March 2021, Microsoft was in talks to buy gaming community service Discord2. This could be interpreted as Microsoft’s attempt to get the jump on its competitors by strengthening the vertical integration of its service development through extending its reach even as far as the gaming user community. (UPDATE: Microsoft and Discord ended the deal talks about a month later.)

Furthermore, Epic Games launched the Epic Games Store after its capital alliance with Tencent with the objective of increasing opportunities for the use of the company‘s 3D creation platform, Unreal Engine. It is also pushing forward with acquisitions of companies that can enrich Epic Games’ assets provided through its engine; or, due to the success of the company‘s own contents, Fortnite. It also purchased the company that owns Fall Guys, which is game content offering experiences of connecting to virtual worlds.

As described above, large-scale acquisitions are occurring as major overseas manufacturers actively seek acquisitions/capital alliances with companies that have complementary functions in order to enhance or fully demonstrate their strengths.

Recent trend of Japanese gaming companies leveraging acquisitions to expand their business

Meanwhile, when we look at the Japanese gaming market, we can see that Japan ranked third in revenue per country after the U.S. and China, with approximately USD 19 billion in revenue in 2021 (to date). While Japan accounts for just over 10% of the global market share and no longer holds the overwhelming advantage in the gaming industry that it once had, it continues to demonstrate significant influence3. In the Japanese gaming market, the sudden rise of the console gaming market as a trend in the 1990s and 2000s resulted in the emergence of many game developers and console companies, and these Japanese companies built up a large share of the market. However, since around 2005, mainly in Western countries, PC game and console markets have rapidly expanded, and Japan's market share has been declining.

There are several factors behind this decline, including the following: the Japanese market remained at a certain size; Japanese companies devoted themselves to developing specific genres such as JRPGs4 that mainly focused on the Japanese market; these companies lagged behind overseas companies in developing high-resolution and large-scale games in the increasingly sophisticated gaming environment that began in the PS3 era; and the companies were late in following overseas trends towardFPS5 and open world6 games

Overseas gaming companies have expanded their businesses in line with the latest trends through acquisitions and capital alliances allowing them to take advantage of their strengths.

In Japan, however, there have been few large-scale acquisitions. Instead, companies either leverage their own IPs or make acquisitions sporadically to improve profitability and to enhance the game development environment by acquiring development contractors and wholesalers that they already have established business relationships with. As an exception to this, SIE has made major acquisitions/partnerships aimed toward building an overseas studio network and securing assets for content in their global strategies for PlayStation. In these efforts, they have established a development environment and made alliances with platforms and eSports businesses that support the gaming community. From the inter-studio sharing of technology that can be witnessed from this, as well, there is a need for other companies to conduct similar approaches.

Using overseas case studies to learn about the possibilities of Japanese acquisitions/capital alliances

In the preceding paragraphs, we compared trends for acquisitions/capital alliances in Japan and overseas. The importance of business portfolio strategy is emphasized in these trends. The increasing size of existing studios, trends toward concurrent development operations, and use of acquisitions to increase development studios are all moves designed to enable continuous launches of large- scale contents.

Meanwhile, Google and Amazon do not currently seem to be having much success with their game development businesses.

Since the beginning of 2021, Google's Stadia dedicated game development studio was shut down7, and Amazon's game development department is scrapping several plans for games8. These may have been based on the companies determining that it is more efficient to secure content through collaboration with other companies than it is to operate a vertically integrated in-house platform. It is also possible that a clash between data-driven decision making and game development culture, which requires significant investments over a period of several years, hindered the companies' efforts.

From these case studies, the key point that Japanese gaming companies should take away is that; where advantages from a technological standpoint that existed up until the Playstation2 era are already gradually disappearing; it will become extremely important to manage portfolios and to work on developing contents from a medium- to long-term perspective in order to maximize the value of the company's IP. In particular, it is important to have middle/long term perspective when using/reviving past IP assets and human resources, rather than sticking to short-time sales figures. Konami's 2020 hit "Momotaro Dentetsu: Showa Heisei Reiwa mo Teiban!" serves as a good example of this.

In recent years, with the development of large- scale games, the number of IPs with global appeal has decreased. Companies should continuously update their IPs as well as aim toward building a stable revenue base. In order to achieve this, it is necessary for them to invest in development infrastructure and diversify monetization methods, even as they look ahead to the consolidation of the industry. This will enable them to transfer their IPs to a system that enables efficient development/operations while the company still has the strength. In particular, it is very important to hold a medium- to long-term perspective when developing games. Concretely, bringing in stakeholders from early on to develop and improve the IP while contributing to the growth of these stakeholders will be the key to success, as in the case of Electronic Arts' EA Sports brand, which integrates the "FIFA", "NBA LIVE", and "Madden NFL" series. Gaming companies will need to go beyond in-house game development to bring in stakeholders involved with IPs, as well as development communities and game user communities, and build a system where, by contributing to these communities, the company ultimately benefits itself.

1. AAA title: "Triple-A" title: Indicates titles in the gaming world that aim to/are expected to become hits, and that maintain high quality through high development expenses over long development periods

2. Microsoft negotiates acquisition of Discord – officials say amount is for just over USD 10 billion, Bloomberg, 2021/3/23: https://www.bloomberg.co.jp/news/articles/2021-03- 23/QQEFE4T0AFB601

3. Top 10 Countries/Markets by Game Revenues, newzoo, accessed 2021/3/22: https://newzoo.com/insights/rankings/top-10-countries-by-game-revenues/

4. JRPG: A term that indicates products created in line with a certain pattern seen in Japanese roleplaying games as compared to overseas RPGs. While JRPGs as a genre have many fans (including those overseas) due to numerous games that left an impact on players in the early years of console gaming, they are also used as an example to point out issues in Japanese games such as their low level of technological advances

5.FPS (First-person shooter): Shooting games played from the perspective of the main character

6. Open World: Aims for level design allowing players to move about freely within the virtual world forming the game's setting

7. Google to close exclusive game development studio for Stadia, focus on third-party support and strengthening its platform, engaget Japanese edition, 2021/2/2:

https://japanese.engadget.com/google- stadia-internal-studio-close-jade-raymond-211608266.html

8. Amazon's game development division, "Amazon Game Studios“, continues to see development halts. What are the reasons behind its failure? Gigazine,2021/2/1:

https://gigazine.net/news/20210201-amazon-game-studios-failure/

4. Shifts toward an era of Experience Sharing - community changes and influence

Community's past meaning of "a connection between players"

The term "community" has a broad range, and its definition varies depending on the area in which it is applied, but in the game industry, communities have long existed as "loose connections among people who actually play a particular game".

In the past, when arcade games were in their prime in Japan, there were small communities centered around amusement arcades where players would gather, and for a long time, especially overseas, there have been "LAN parties" where users would gather in one place, bring their own PCs, and enjoy playing multi-player or cooperative games through a Local Area Network (LAN) connection. Even later on, when MMOs1 and other online games based on the internet flourished, while these communities went virtual, their essence remained the same. Now, however, gaming communities are changing into something that goes beyond a simple connection between players of each game.

Changes in consumer behavior and communities brought on by streaming

The reason behind the change is the spread of real-time streaming platforms such as YouTube and Twitch, and the expansion of the viewer base. Another important factor is the increasing number of players who are streaming their own gameplay, as the barriers have been lowered for establishing a hardware/software environment for streaming and preparing a good internet environment.

In fact, Twitch, which focuses on game streaming, has grown more than twelvefold, from an average of about 100,000 simultaneous views in 2012, when the service was first launched, to about 1.26 million views in 2019, just before the start of the COVID-19 pandemic. The average number of simultaneous channels also increased more than 22-fold between 2012 and 2019, surpassing 50,000 channels, and is approaching 120,000 channels as of March 20212.

In other words, game streaming has increased and the consumer behavior of "watching game streaming" has spread at the intersection between gaming and streaming. This is bringing in new users who do not play those games and seems to have had led the gaming community to expand.

But here, we need to be aware that "the users who do not play games" is divided into two groups. The first group is composed of users who only watch streaming but do not play games themselves. The second group is of users who also play games themselves but have not yet played the games they are watching in the streaming.

As mentioned above, game communities used to be "connections among players based on specific games“, but now they have transcended the boundaries of individual games to become organic connections between users that develop and interact with each other and are directly affected by user behavior. In this type of community, users can be both streamers and viewers, and the communities tend to be relatively smaller than the communities for professional gamers or famous streamers, which have a fixed relationship with a large number of viewers supporting them. Looking back at the aforementioned Twitch data, we can see that while the average number of simultaneous views has increased, the number of channels has expanded much faster than that, so the average number of views per channel is smaller than before. This backs our hypothesis that the nature of game communities has been changing.

Communities as a place for " Experience sharing“

A symbolic example that shows how these streaming communities work is “Among us”. “Among Us" is a cooperative game for up to ten players which is designed to require discussions among players from time to time using in-game chat or external voice chat tools. Its objective is for players to win by surviving to the end by identifying and eliminating the two enemies who have disguised themselves among allies.

The game was developed by only three people and attracted little attention when it was released in June 2018. Two years later, however, in July 2020, a famous Twitch streamer featured the game in his streaming channel, triggering a global surge in popularity. The game was downloaded 42 million times in the first half of September 2020 on the PC gaming platform Steam, and 84 million times for iOS and Android in September alone3. As a result, it became the number one ranking download worldwide in both iOS and Android stores with 264 million downloads4 throughout 2020.

The reason why it is thought to have gotten popular so explosively is that it is the type of content "looks great in streaming", being very compatible with live streaming, and also because users who had not yet played the game were able to "get a real sense of how fun it was" through reliving another player's experience in real-time. Certainly, the COVID-19 pandemic had a large effect by limiting opportunities to go outside and communicate with others, but this big success seems to show the influence of the community as a place where streamers can share their experiences candidly with viewers.

Influence held by communities

However, as mentioned earlier, the future of gaming communities is not a world where specific professional gamers or famous streamers share their experiences to their audience one-sidedly inside individual communities. It is a world where the communities spread out innumerably from a large number of general users, and where those users share their experiences among them and influence one another.

There, users who join multiple communities are predicted to increase their sense of belonging to each community as well as their influence on each other much more through their mutual communication enriched by various tools. This influence is not necessarily always beneficial, however.

As in the case of “Among Us”, when a specific game is featured in a community, it may stimulate the community users' willingness to buy the game, but at the same time it may also weaken the users' motivation to play it themselves.

This issue is particularly pronounced in game streaming and has become a controversial topic in the entire game industry, including their opinion both for and against game streaming itself. With this, game companies have been moving to establish guidelines over streaming. Guidelines vary from company to company, with some being more restrictive and others being more permissive.

For example, Square Enix has established guidelines for each title in its popular "Dragon Quest" series and has traditionally prohibited streaming the ending part of the game across the entire series. However, in March 2021, they revised the guidelines to allow streaming if a certain period of time has passed after the titles released to the market5. At the same time as the revision, the company also announced a message to encourage "communication that arises through games", which was the company’s positive response to the changes in game communities.

As games are being accepted by wider groups of people than ever before, the influence of communities will become much stronger. This will likely become hard to ignore, especially in terms of branding and community development.

1. Massively Multiplayer Online (MMO): A large-scale online game format where numerous players participate

2. TwitchTracker, "TWITCH STATISTICS & CHARTS", 2021/3/9: https://twitchtracker.com/statistics

3. How Among Us, a social deduction game, became this fall’s mega hit, CNBC, 2020/10/14: https://www.cnbc.com/2020/10/14/how-among-us-became-a-mega-hit-thanks-to-amazon-twitch.html

4. 'Among Us' most downloaded mobile game globally in 2020, CNBC, 2021/1/9: https://www.cnbctv18.com/technology/among-us-most-downloaded-mobile-game-globally-in-2020-7948421.htm

5. Square Enix, "DQ Paradise: Dragon Quest official website: Streaming guidelines: 2021/03/19: http://www.dragonquest.jp/guideline/

Authors

Ryosuke Fujii

Deloitte Tohmatsu Consulting LLC Manager

Mainly engages in new business planning, GTM (Go To Market), PMO and other areas for telecommunications companies, manufacturers, and media companies. In recent years, he has been involved in initiatives for new businesses/digital transformation using new technology. In his personal life, he plays FPS and RPG games, among others.

Kai Asano

Deloitte Tohmatsu Consulting LLC Manager

Since joining Deloitte as a new graduate, he has engaged in consulting for entertainment business (including major gaming companies) and major manufacturers. His major focus has been on initiatives that include marketing strategies and investigating business strategies, including for new businesses. He has kept an eye on trends in gaming industry news for many years and specializes in gaming market trends in Japan and overseas, as well as the game development status of various companies.

Sae Iwai

Deloitte Tohmatsu Consulting LLC Manager

Assumed her current position after working at a major IT software vendor. Engages in the planning and implementation of business strategy formulation, overseas business and corporate establishment, business reform, IT governance reform and other areas, mainly for major manufacturing and telecommunication companies. She specializes particularly in trends in the overseas gaming market and online gaming market.

Explore Content

- 1. Future outlooks based on the evolutionary trajectory of gaming consoles

- 2. Full-scale development of cloud gaming and the turning point for the gaming industry

- 3. The potential of capital alliances in gaming company expansion strategies

- 4. Shifts toward an era of Experience Sharing – community changes and influence