Perspectives

Housing remains hot in the headlines

How is the Government looking to take the heat out of housing and secure homes for New Zealanders?

So much has been said about housing in New Zealand that unless it’s your full time job to monitor the New Zealand housing crisis, it can be hard to keep up with what the problem is, what solutions have been tried, and what potential solutions remain to be tested in order to “fix” the “problem”. Budget 2021 confirms a number of measures to addressing the nation’s housing issue:

- A $3.8 billion Housing Acceleration Fund, including ring-fencing $350 million for a Māori Housing Programme

- Whai Kāinga Whai Oranga – a $380 million fund to support building of new Māori housing and repairs to current homes

- Additional funding for Kāinga Ora of $133 million to purchase land and allow for development risk

- Lifting income caps for first home buyers and house price caps to support First Home Grant and First Home Loan Products.

The Budget Economic and Fiscal Update (BEFU) noted that annual house price growth is forecast to reach a peak of 17.3% in the June 2021 quarter, before easing back to 0.9% by June 2022. House price inflation is expected to stabilise at 2.5% in 2025 as borders reopen and the population increases.

Click to enlarge

Problem definition

At its heart, the key problem is that New Zealand has too few houses. The housing shortfall has been estimated at 80,000 houses. This deficit of houses has accumulated over an extended period. Basic economics means that prices have gone up, and New Zealand’s houses are now unaffordable for many.

In March 2021, the Government announced some steps to help with our housing problem – an extension of the bright-line test to 10 years, and a denial of interest deductions for residential rental property, except for “new builds” (an, as yet, undefined term).

In late April of this year, the Government released a large number of reports received in the lead up to the March announcements. The following facts are taken from these reports and help explain the current state of housing in New Zealand and why serious action is needed. Consider it an aide-memoire.

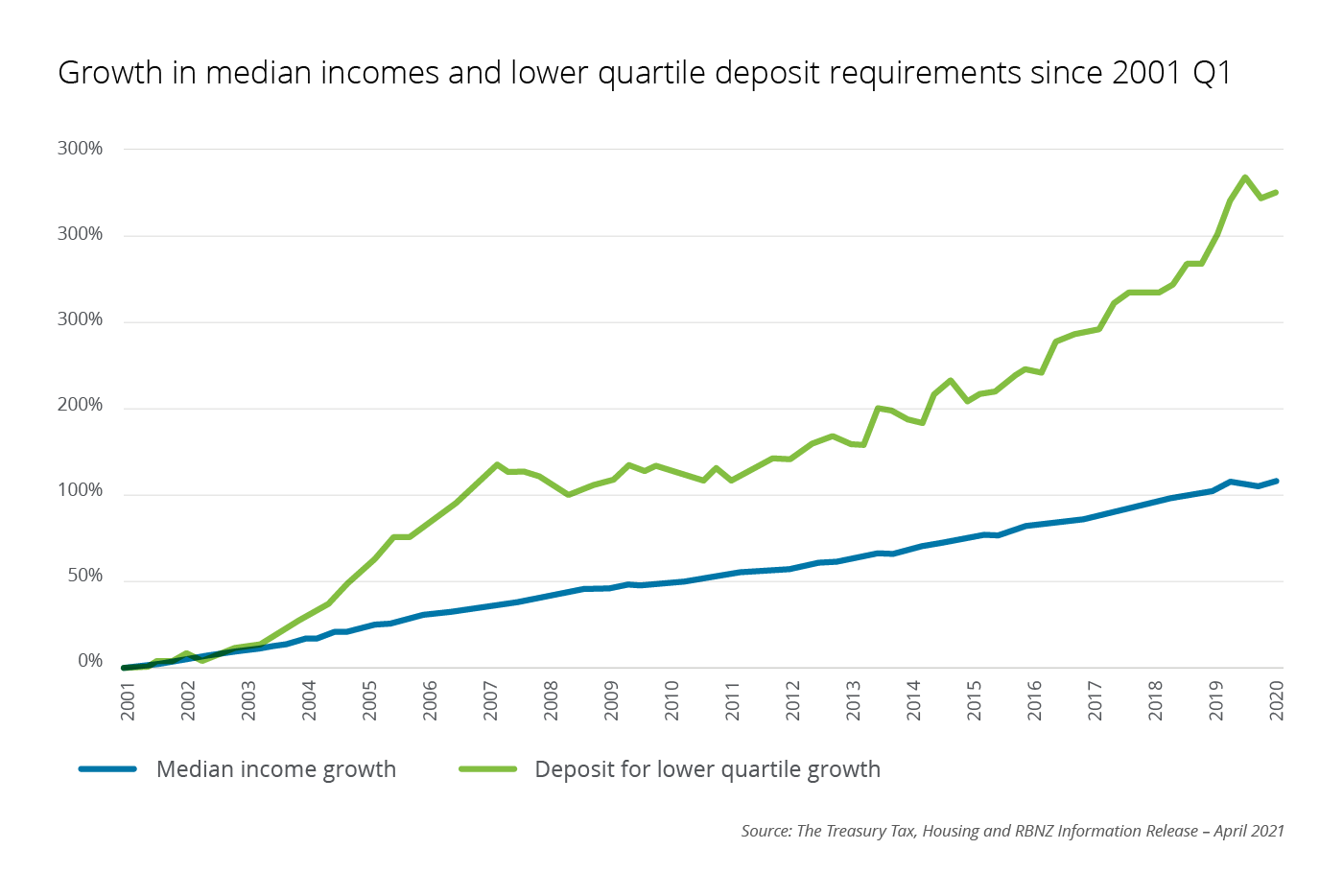

Affordability

- As few as 25% of renters could afford to service a mortgage for a modest priced existing home1 , assuming they could raise the required deposit. This is unlikely to change even with a 10-20% price drop, given the increases in the last 12 months.

- Between 25-30% of renters are spending 40% or more of their income on housing costs.

- There has been an increase in the proportion of households who rent. Between 1991 and 2018 the proportion increased 9%, from 22.9% to 31.9%.

- Home ownership rates have been decreasing over time, with minority groups experiencing the largest declines.

- Māori and Pacific people are significantly less likely to own their own home and are more likely to live in social housing. While overall 12.9% of the renting population live in a Kāinga Ora home, when breaking this down by ethnicity, 20.5% of Māori and 36.9% of Pacific renters are in these houses.

Click to enlarge

Click to enlarge

Click to enlarge

Supply

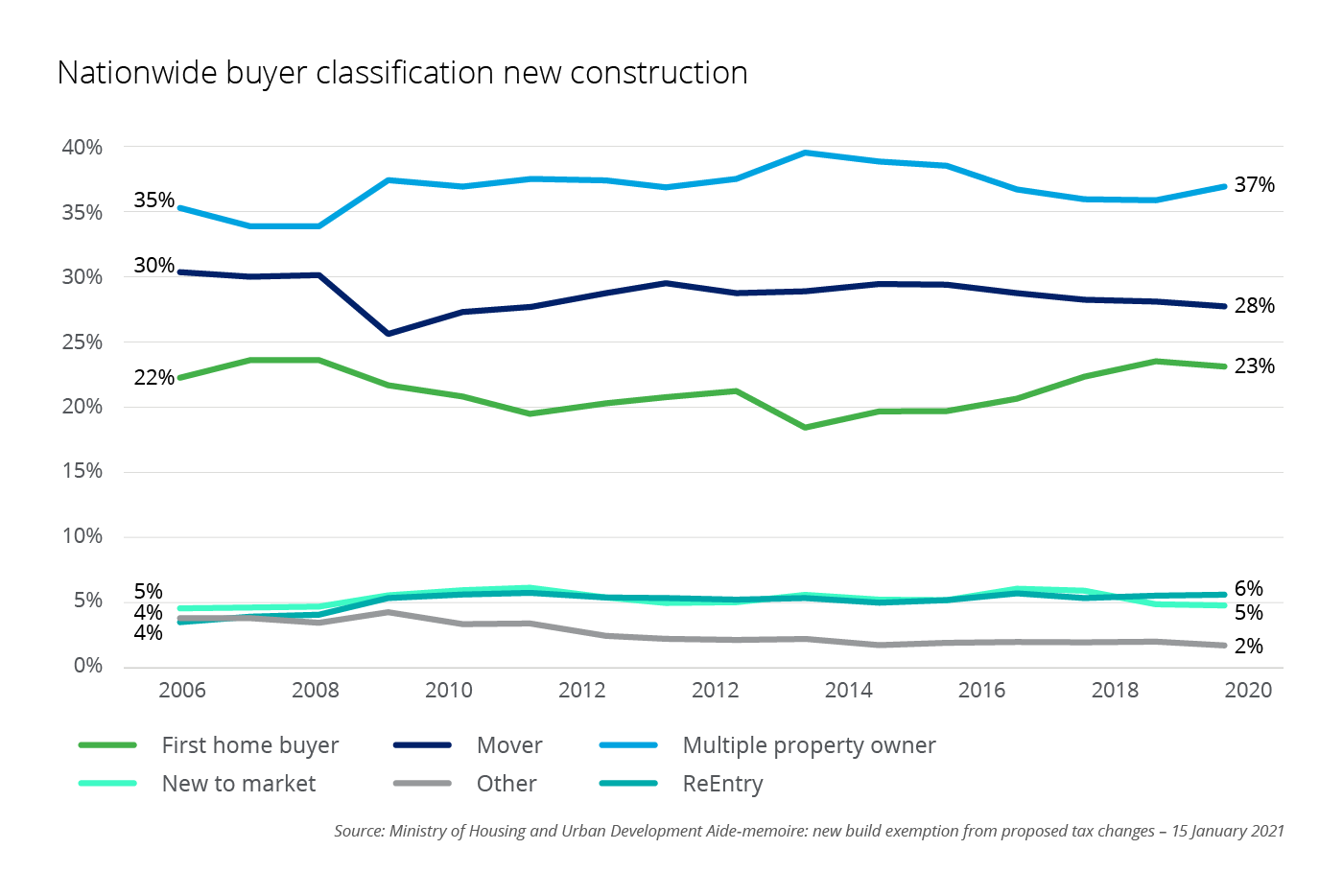

- Almost 40% of new-build properties were purchased by multiple-property owners (a proxy for investors) in 2020. Approximately 23% of new-builds are sold to first home buyers.

- However, as most first home buyers buy homes in the bottom half of the market, this means there are not enough first home buyers to maintain new-build supply at the same level as they cannot afford to purchase at upper price points. That is, it’s very important investors are still willing to purchase new builds.

- Only 3% of first home buyers purchase an apartment, whereas apartments make up 10% of the rental stock. (Anecdotally, this is somewhat due to less favourable lending conditions for apartment purchases due to perceived risks2 and many people are happy to rent in apartments but want more space when looking to purchase their own home. Source: Newsroom)

- Building consents are at their highest level (in absolute numbers) since 1973, but we’re still building fewer houses as a percentage of population. On average there are 7.5 new homes per 1,000 people, but this also varies by region, with only two consents per 1,000 people in Rotorua.

• It is unknown how many vacant houses exist in New Zealand, but a 2015 study (using electricity usage data) found that 8,000 properties were vacant in Auckland (1.6% of all dwellings).

Click to enlarge

Are investors the problem?

- Fewer than 15% of property purchasers own ten properties or more.

- The median property holding time for investors is seven years, which is comparable with owner occupiers.

- Rental properties can be either profitable or unprofitable – 63% of property owners (182,219 taxpayers) have an average annual profit of $14,000; 37% (107,530) report rental losses, with an average loss of $9,000 per annum.

- In 2019 there was approximately $2.6 billion of taxable rental profit and $970 million of rental losses.

- 50% of investors have interest-only mortgages on their rental properties, which can lead to the belief they are predominately investing for capital gains.

Get in touch with the author