South Africa economic outlook, November 2024

Investor sentiment and domestic confidence have improved post elections, but structural reforms and growing fixed investments are imperative for South Africa’s long-term prosperity and growth

The newly elected coalition and the economy till now

Following the national elections on May 29, 2024, the African National Congress, in power since 1994, received only 40.2% of votes.1 Thus, unable to secure a parliamentary majority, it formed a coalition government with the centrist and pro-market Democratic Alliance—its main opposition—as well as other small parties.

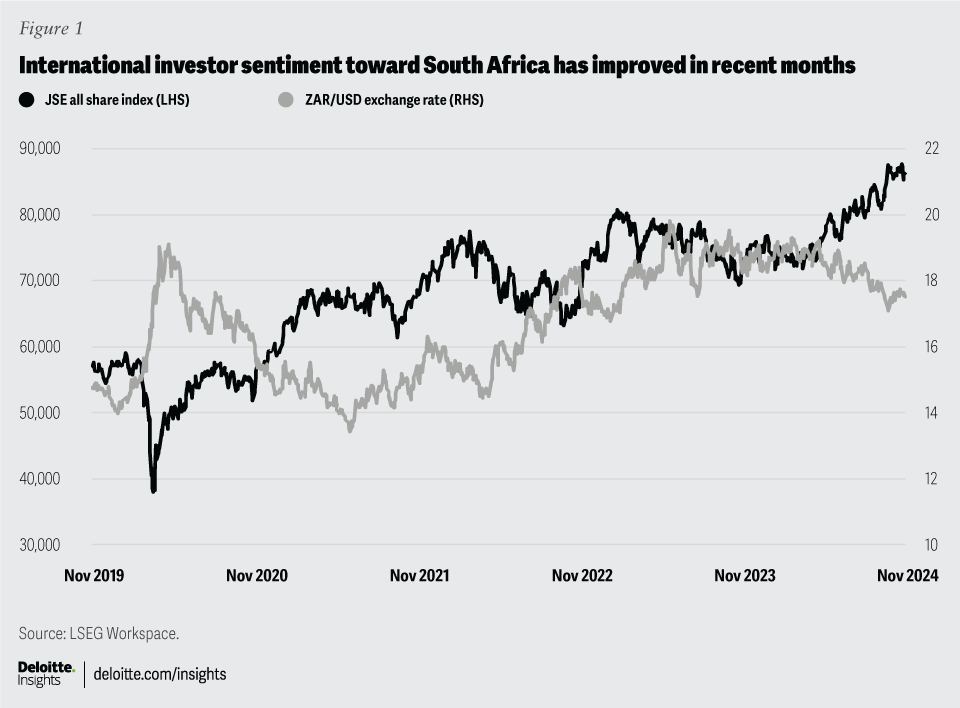

The result is the 10-party Government for National Unity (GNU), representing about 70% of voters (although voter turnout did drop to 58.6% from 66% five years before). Arguably, this could be the best outcome for the economic future of the young democracy.2 For one, the reelection of President Cyril Ramaphosa for a second term has ensured policy continuity, while the formation of the GNU boosted international investor sentiment toward South Africa—amid an improved global economic landscape and the start of the global rate-cutting cycle (figure 1).

There have been some key, postelection gains in financial markets. Between the end of February and the end of September 2024, the country’s sovereign risk premium improved from 327 to 240 basis points.3 South Africa’s 10-year bond yield dropped to below 10%—its lowest in almost three years.4 The rand appreciated to its strongest level against the US dollar in almost two years in September 2024 (although it lost some of these gains on account of the US dollar strengthening, post US elections),5 while stocks listed on the Johannesburg Stock Exchange had their strongest third quarter in over a decade.6

The run up to the elections also coincided with the suspension of loadshedding.7 By the end of October 2024, South Africans celebrated more than 200 successive days (over two quarters) of no loadshedding, following years of intermittent power outages, and many other structural constraints in sectors such as transport and logistics, which had crippled the economy and limited its potential. The suspension was driven by a reduction in unplanned outages of power-generation units, their ongoing planned maintenance, and a boost in the country’s energy availability factor—up from 55.3% over April 1 to Oct. 3, 2023, to 63.2% over the same period this year.8

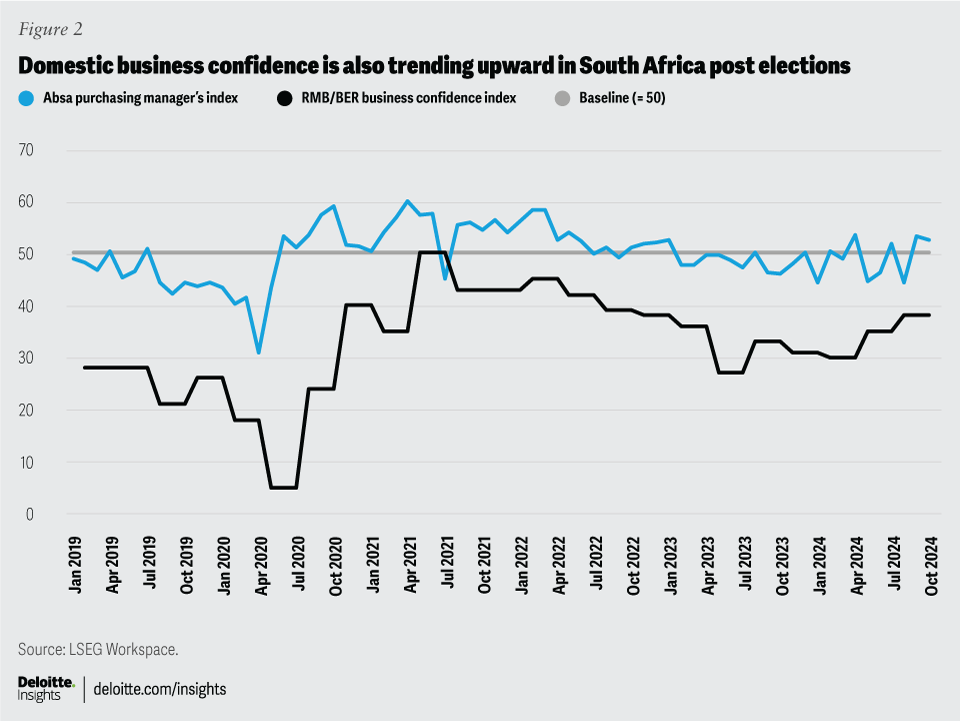

This has helped boost confidence (which dropped sharply ahead of the elections) on the supply side of the economy, as shown by various business surveys. The Absa purchasing manager’s index increased into expansionary territory at 53.3% in September and stayed positive in October (52.6%), while the Rand Merchant Bank/Bureau for Economic Research business confidence index reached its best reading (38 index points) in almost two years in the third quarter of 2024 (figure 2), and jumping to 45 in the fourth quarter.9 Still, this confidence (cautious as it may be) will need to continue, while also translating into real economic gains—which it is yet to do, and we expect it to take time.

A sector-by-sector view of the economy

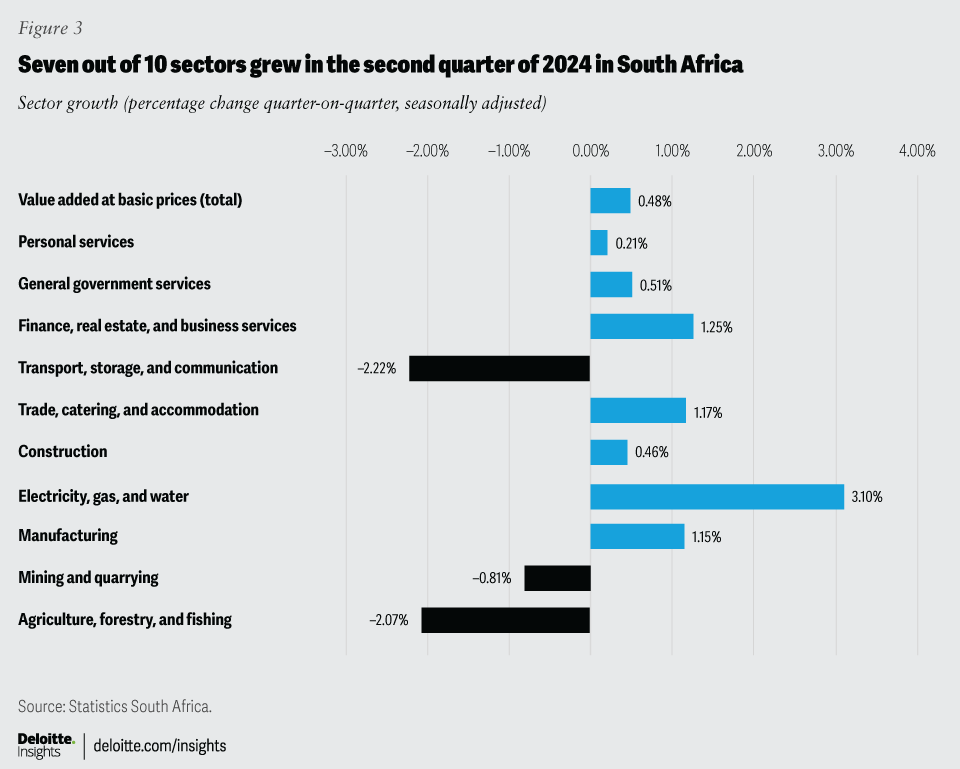

Numbers for the first half of 2024 were underwhelming: Year on year, the first six months of the year saw the economy expand by 0.5%.10 Gross value added from manufacturing contracted by 0.7%, compared with the first six months of 2023—but these numbers did bounce back in the second quarter of 2024, growing at 1.1% quarter on quarter, seasonally adjusted, versus a decline of 1.4% in the previous quarter, as loadshedding was suspended.11

The mining sector also contracted, although only by 0.1% over the first half of the year, with constraints mostly from rail and port inefficiencies undermining the sector. At quarter-on-quarter and seasonally adjusted rates, value-added numbers from this sector saw declines in both the first and second quarters of 2024—of 1.7% and 0.8%, respectively.12

In contrast, the trade, catering, and accommodation sector, as well as the finance, real estate, and business services sector saw a positive first half, while transport, storage, and communication contracted over the same period. All in all, after 0% real gross domestic product growth in the first quarter of 2024, second-quarter values came in at 0.4%, with seven industries showing marginal (but still positive) growth (figure 3).13

Economic growth, inflation, and central bank rate cuts

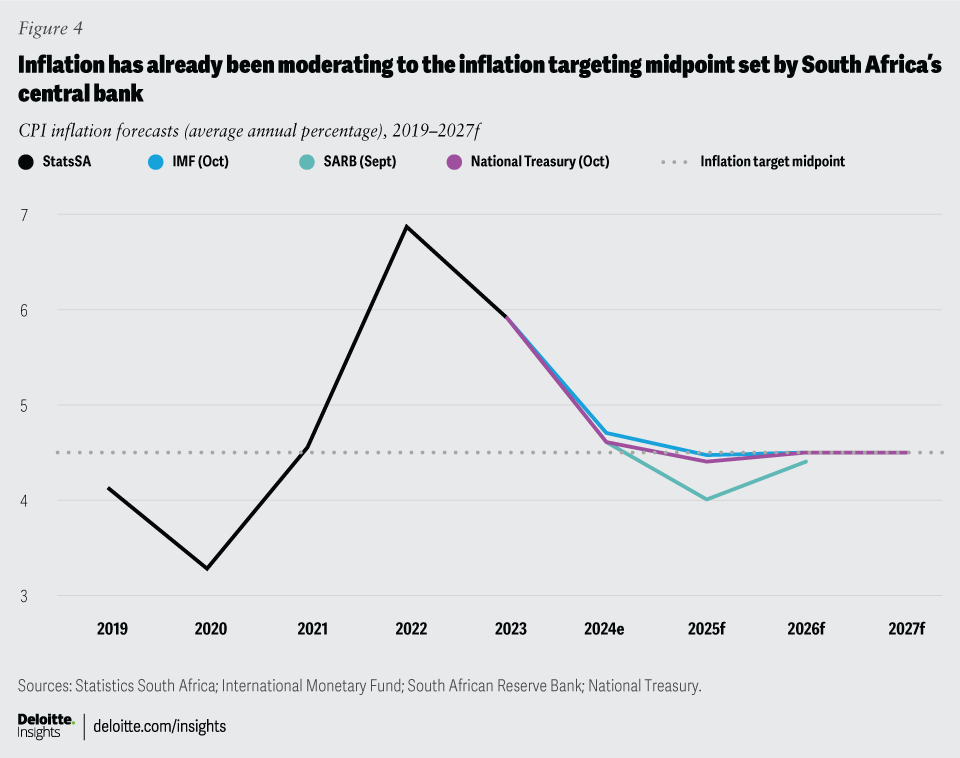

Growth is expected to quicken somewhat in the last two quarters of 2024, particularly as the tailwinds of no loadshedding, subdued inflation, and subsequent lower interest rates boost balance sheets of households and corporates alike.14 Consumer price index inflation already dropped to 5.2% year on year in April 2024, down from 5.6% in February 2024. By August it dropped lower to 4.4%, which is just below the midpoint of the 3% to 6% inflation target band set by the South African Reserve Bank (SARB) (figure 4). A further slowing down of inflation to 3.8%, in September, and 2.8% in October—the lowest value recorded since June 2020—was largely due to the strength of the rand, falling fuel prices, and slowing food price inflation.15

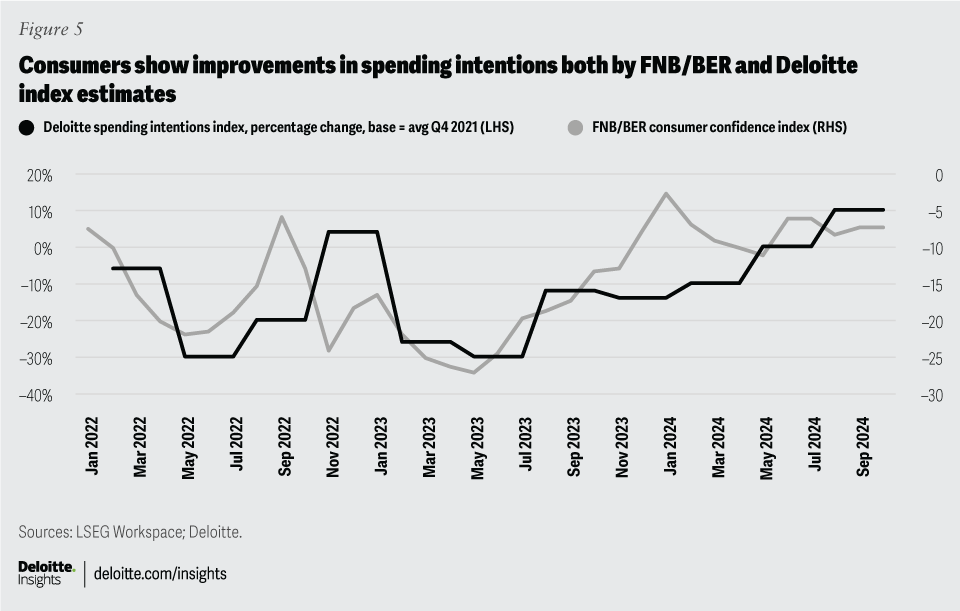

This trend saw the SARB start its rate-cutting cycle in mid-September 2024, reducing the repo rate by 25 basis points and again in November 2024.16 Further rate cuts are expected through various quarters of next year. This should boost consumer confidence and increase household consumption, in turn supporting medium-term real GDP growth. In the third quarter of 2024, consumer confidence—as measured by the First National Bank/Bureau for Economic Research (more commonly, FNB/BER) consumer confidence index—stands at its highest value in five years, although still sub-zero (that is, below the neutral level),17 while Deloitte’s spending intentions index has seen improvements since May 2024, from –1% to 4% over September 2024 and October 2024 (figure 5).18

Consumers have also had some cushioning in the form of savings from their retirement funds after the two-pot retirement system was legislated on Sept. 1, 2024.19 More than 1.1 million taxpayers had made withdrawals from their “savings pot” by Oct. 11, 2024, with a total of 21.4 billion rand being paid out.20 This is expected to help households struggling with the cost-of-living crisis for more than two years to pay off debt and increase spending. After negative year-on-year growth in the first two months of 2024,21 real retail trade sales have expanded modestly in subsequent months, increasing to 4% year over year in June 2024 and 3.2% in August 2024,22 in tandem with declining consumer price index numbers.

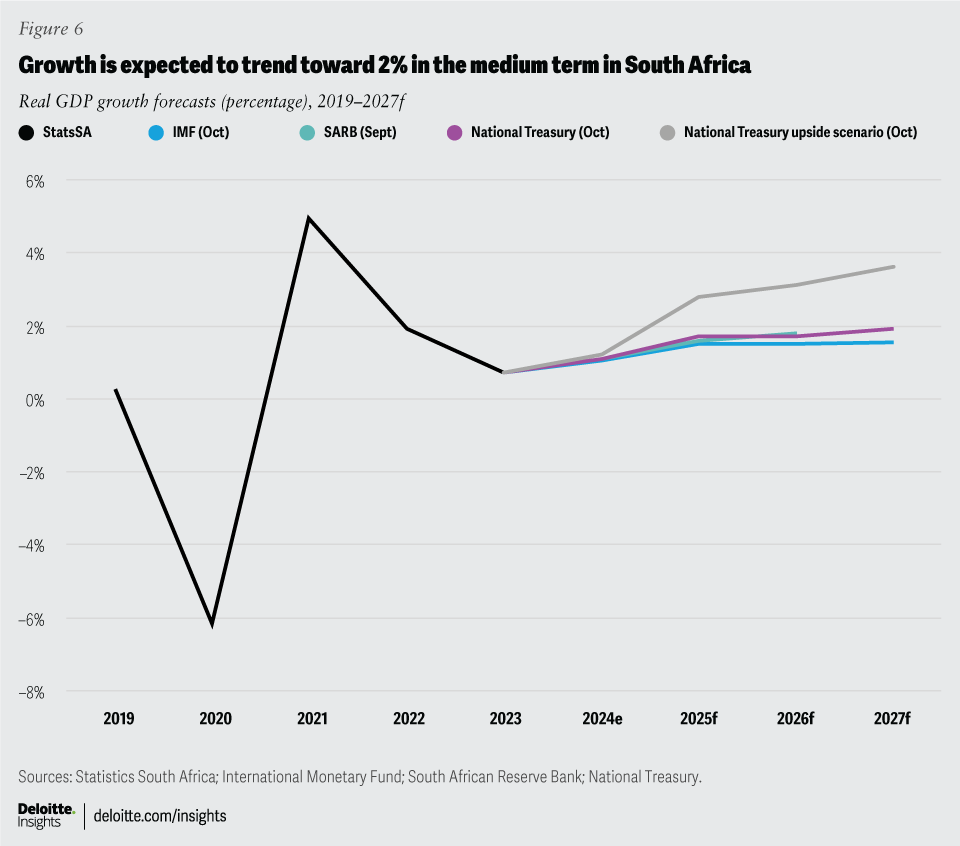

Despite some of the structural and cyclical improvements mentioned, South Africa’s immediate-term growth outlook is still left wanting, with limited benefits from the above translating into real economic gains over the next six to 12 months. In 2024, real GDP growth is expected to come in around 1.1% (as per the latest forecasts from the International Monetary Fund in October 2024, National Treasury in October 2024, and SARB in September 2024), up from 0.7% in 2023.23

The medium-term outlook has been revised upward by organizations such as the International Monetary Fund, but toward the lower end of various forecast agencies, to 1.5% on average.24 The SARB forecasts the economy to grow by 1.6%, 1.8%, and 2.5% in 2025, 2026, and 2027, respectively (an average of 2% over the next three years), as per its September 2024 estimates. It also expects inflation to be largely under control, trending around the 4.5% midpoint in 2024 and over the next three years (as shown in figure 4).25 National Treasury forecasts a more benign outlook for real GDP growth, averaging 1.8% over the medium term (figure 6).26

With tailwinds such as positive global sentiment and improved local confidence, how will South Africa achieve a higher growth trajectory that ultimately aligns with the job-creating 2030 National Development Plan target of 5.4% real GDP growth through 2030?27

Mini budget and government plan focus areas

The recent reading of the Medium-Term Budget Policy Statement (MTBPS) on Oct. 30, 2024 by Finance Minister Enoch Godongwana delivered no “silver bullet” solution to address the country’s growth challenges (and also was not expected to). Termed the “mini budget,” it was the first update on state finances since the formation of the GNU and provided an opportunity to confirm policy continuity from a fiscal, macroeconomic, and structural reform perspective. It reconfirmed the government’s stance toward fiscal consolidation and stabilizing public debt, although fiscal ratios in the current fiscal year are expected to slip somewhat due to lower revenue collection.28

Still, the government has committed to anchor fiscal policy by targeting a primary budget surplus for the rest of the decade, with the primary budget surplus achieved in fiscal year 2023 to 2024 being the first in 15 years.29 In the medium term, this will help to tackle the fiscal deficit, which is expected to widen over the current fiscal year (fiscal 2024 to 2025) from an initially expected 4.5% to 5% of GDP, and also see debt as a share of GDP stabilize in the next fiscal year (as previously expected)—although at a somewhat higher ratio of 75.5%, from 75.3%.30

While government looks to maintain fiscal prudence and macroeconomic stability, two key focus areas stand out in its plan to spur on economic growth. One, the relentless commitment to implementing structural reforms to create a more productive and competitive economy; and two, the focus on unlocking growth-enhancing infrastructure investments, although mostly from the private sector, to boost fixed investment spending.31 This is not new thinking, but it is important—and this is now gaining wider traction in creating a more pro-business environment in South Africa.

Commitment to implementing structural reforms

As noted in a previous edition of this publication,32 various plans have been set in motion to address supply-side constraints via the reform program, Operation Vulindlela (OV), launched in 2020. These are bearing fruits, slowly. The first phase of the program has focused on sectors including energy, rail, water, and telecommunications.33 The finance minister announced that this program will be expanded to include other areas as part of phase 2. In the first phase, reforms under OV have attracted over 390 billion rand in investment in the energy sector.34 The focus on the ongoing implementation of structural reforms—although at times painful and resulting in short-term trade-offs—is at the core of the GNU’s medium-term strategy.

OV phase 2 is expected to continue to focus on initiatives in energy (restructuring of state utility, Eskom, and establishment of a competitive energy market), logistics (including transport sector reforms linked to rail and ports, with a bill signed midyear to bring in private participation in rail), water (including ensuring water security, reduction of leaking water infrastructure and increased private sector participation), data and e-visas. OV phase 2 is also set to broaden the areas of focus to assist and boost local government capacity, tackle spatial inequality, and invest in digital public infrastructure.35

It is also supported by the Government-Business Partnership, launched in October 2023, to help address issues in electricity and logistics (both key sectors under OV) as well as crime and corruption. This collaboration also announced its second phase recently, now under GNU, and its commitment to also include youth unemployment (more than 43.2% of those between 15 and 34 years of age are unemployed, higher than the country’s official unemployment of 32.1%)36 as a priority area.37

What is important with the focus on structural reforms is both the depth and the speed of implementation. While the focus has broadened as shown with phase 2, the speed of implementation will require more attention. National Treasury models suggest that faster reforms that unlock larger energy investments and reduce port and rail challenges would theoretically see real GDP growth increase by 1.1 percentage points in 2025, and a further 1.4 and 1.7 percentage points in 2026 and 2027, respectively, lifting economic growth to above 3% in the next two years.38 The Bureau of Economic Research has published similar upside scenario forecasts, assuming speedy reform implementation.39

Focus on investment to drive infrastructure growth

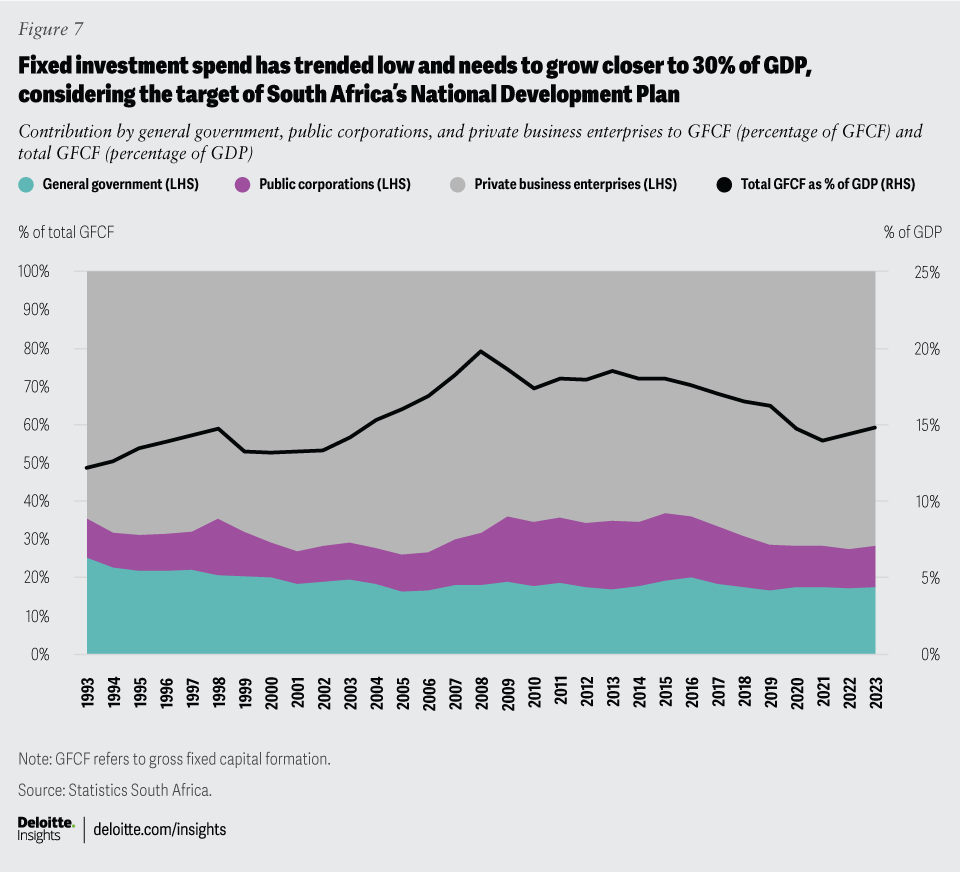

Infrastructure investment—with a shift from consumption- to more capital-based expenditure in the economy—has been touted by the National Treasury in recent budget and MTBPS speeches. As indicated in a previous edition of this outlook,40 gross fixed capital formation as a share of GDP in South Africa has been trending below required levels for years (figure 7). In 2023 it was about 15% of GDP—which equates to half (30%) of what is targeted in the National Development Plan.41 The past two decades only saw gross fixed capital formation peak ahead of the 2010 FIFA world cup,42 in 2008—at around 20% of GDP.43

Private enterprises have been driving the fixed-investment agenda and effective delivery of, in particular, energy infrastructure. However, they have also shown reluctance to invest given structural constraints, including tough operating conditions, crime and corruption, weak demand, and overall limited business confidence. Unlocking faster growth will require greater capital formation, and effective ways to deliver infrastructure to create the foundation for the economy to grow in the future.

Reform implementation will unlock opportunities

While faster implementation of such reforms will contribute to boosting confidence and unlocking fixed investment, government is also looking at new ways to attract private sector investment for public sector projects. Focus is on project preparation and creating a pipeline of bankable projects (a long-standing challenge in South Africa), strengthening public-private partnerships (PPPs) through reforming their frameworks, as well as using risk-sharing initiatives and financial instruments to unlock greater private funding.

The latter, for example, will include a blended finance-supported credit guarantee vehicle that will help to de-risk public sector infrastructure projects to draw in both private lenders and developers. Based on the lessons and experiences of the Renewable Energy Independent Power Producer Procurement Programme, the mechanism is expected to be applied to independent transmission projects: South Africa requires at least 14,000 kilometers of transmission lines over the next decade,44 starting from the end of next year.45

Building on the budget review in February 2024, the MTBPS indicated that government has finalized amendments to regulations that govern PPPs in South Africa, to be released before end of November 2024. These reforms, which incorporate public and private sector comments, are expected to streamline PPP regulations and reduce complexity, and help unlock greater private capital for public projects. Also, given the need for infrastructure funding in the longer term, new financing mechanisms are being explored, including amending infrastructure to an asset class via the new Securities Regulations of the Banks Act. This could help unlock new investment vehicles such as asset-backed securities that could be traded based on pooling infrastructure loans, or the creation of infrastructure investment trusts.46 These tools could though come in helpful as South Africa looks to unlock greater private funding for climate and green projects, particularly in support of the Just Energy Transition.

These are important steps in the right direction, but they remain paced and the results of greater confidence, and a continued focus on reforms and unlocking fixed investment spending will still take time to trickle through to faster and job-creating economic growth. And there will likely be bumps along the way, not least from the challenges that come with a coalition government (including divergent views on crucial policy areas, as already seen), but also from possible downside risks to growth in the global environment, linked to inflation, geopolitics, continued economic weakness in China, and others.

Nevertheless, after underperforming for more than a decade, South Africa has entered a new era and has a window of opportunity to turn things around and pen a new story—one that utilizes the foundation stone of reforms and growth-enhancing infrastructure spending to create a society that is more inclusive, job-creating, and sustainable in the medium to long term.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}